You plan to open an account with the bank. Now, you have the choice to open an individual savings account or a company current account. This is what people know in general. But do you know that there is an account which you can open for savings, but is not an individual savings account. This is called the HUF account.

It sits somewhere in between personal and business banking. It allows income from ancestral property, family businesses, or joint investments to be managed under one legal structure.

Many people overlook it simply because it is not discussed enough. But when used correctly, it can offer tax efficiency and better savings. So, let us explore the complete details of the HUF account here in this guide. Know the HUF benefits and who can open this account here.

What is a HUF Account?

The HUF full form is Hindu Undivided Family. It is a legal concept recognised under Indian law, where a family is treated as one separate entity for financial and tax purposes. Instead of income being divided among individuals, certain earnings and assets are held in the name of the HUF.

In simple terms, this is what a Hindu Undivided Family includes:

Members belonging to the same family by birth or marriage.

A Karta, usually the eldest member, who manages financial decisions.

A separate PAN and bank account in the HUF name.

Income from ancestral property, family business, or joint investments.

Understanding the HUF account helps you see why it is often used for structured savings and tax planning.

A HUF account is not only about tax saving. It plays an important role in tax saving, asset creation, and long-term planning. When families earn or invest together, this structure brings clarity and control.

Below is a detailed explanation of HUF account benefits, covering taxation, wealth creation, and financial discipline.

1. Separate Tax Identity and Lower Overall Tax

One of the most important HUF benefits is its separate tax status. A HUF has its own PAN and files a separate income tax return. This allows the same family income to be split across individual and HUF entities, which can reduce the overall tax outflow in a legal way.

2. Efficient Wealth Creation for the Family

A HUF account helps in building wealth collectively rather than in fragmented personal accounts. Income from ancestral property, family business profits, or joint investments stays within the HUF. Over time, this allows compounding to work at a family level. This supports long-term wealth creation.

3. Additional Tax Deductions and Exemptions

Another key HUF account benefit is access to tax deductions similar to an individual. A HUF can claim deductions under sections such as 80C, invest in tax-saving instruments, and enjoy basic exemption limits separately. This improves post-tax returns for the family.

4. Clear Separation of Personal and Family Finances

Many families mix personal and joint income, which creates confusion later. A HUF account creates a clean boundary. Family income is routed through the HUF. But all the personal earnings remain separate. This improves financial discipline and transparency.

5. Structured Investment Planning

A HUF can invest in mutual funds, fixed deposits, bonds, and even equities. These investments belong to the family unit. It means that these are not under any one person’s name. This structure ensures continuity of investments across generations. It also reduces dependency on one individual.

6. Support for Long-Term Succession Planning

One often ignored HUF benefit is smoother succession. It is important to know that the HUF continues even after the death of the Karta. The assets are not disrupted. This continuity helps families plan for future generations without frequent restructuring.

7. Better Use of Family Income Sources

Income sources like rent from ancestral property or profits from a joint family business fit naturally within an HUF. Routing such income through a HUF account avoids unnecessary tax pressure on one individual and keeps ownership clear.

8. Strong Foundation for Multi-Generation Wealth

An HUF account acts as a financial backbone for the family. It helps with savings and ensures that the family generates good wealth. This is why it is considered to be a great tool for families who wish to generate wealth and build long-term savings.

These HUF account benefits make it more than a tax structure. It is a long-term financial planning tool when used with clarity and proper advice.

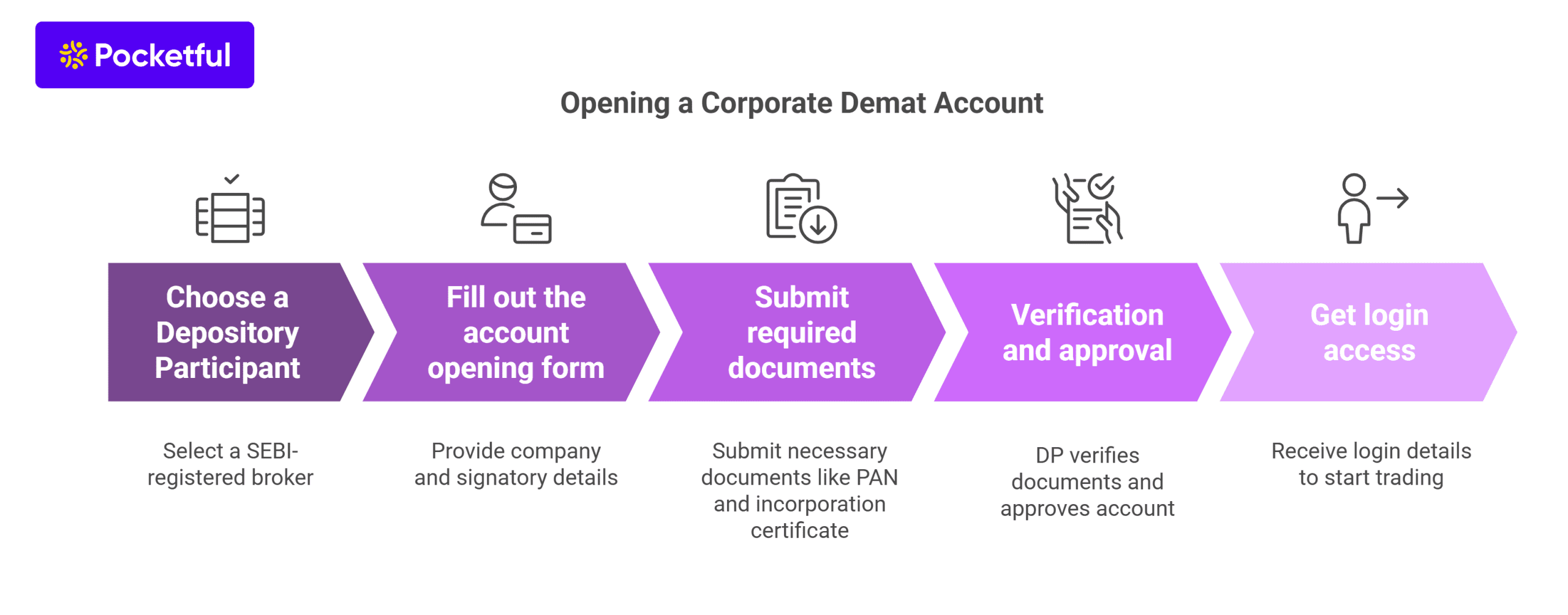

How to Open a HUF Demat Account

The process is slightly different from an individual Demat account and follows these steps:

1. Open a HUF Bank Account First: A HUF Demat account must be linked to an active HUF bank account. All investments and settlements flow through this account.

2. Ensure HUF PAN Is Available: The HUF must have its own PAN. Individual PANs of members cannot be used for HUF investments.

3. Submit Required Documents: You can open an account with any of the above. These can include direct via bank of through platforms like Pocketful. These are usually required:

HUF PAN card

PAN and address proof of the Karta

HUF deed or declaration

List of HUF members

Bank proof of the HUF account

4. Karta Operates the Account: The Demat account is opened in the HUF name, but it is operated by the Karta on behalf of all members.

5. Complete Broker KYC and Agreements: Once KYC is verified, the broker activates the HUF Demat account for trading and investing.

A HUF structure offers more than tax efficiency. It helps families manage income, invest together, and build wealth in a disciplined way over time. With a HUF Demat account, these benefits extend to market-linked investments as well.

If you are planning to use HUF account benefits for long-term wealth creation, opening a HUF Demat account with Pocketful can be a practical next step. Pocketful offers a clear and guided process to help your family invest with structure and confidence.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

In the stock market, when we buy the same shares at different times and prices, the question often arises when selling them: which purchase the system recognizes first. The answer is FIFO in Demat. According to this rule, the shares purchased first are considered the first to be sold. This directly impacts your taxes, profit-loss, and investment planning. In this blog, we’ll explain this rule in simple terms and explain why it’s important for investors.

Basics of Demat and Share Transactions

What is a Demat Account?

A Demat Account allows you to hold your shares and securities in digital form. Previously, shares were available in physical certificates, but today, all shares are held electronically through depositories like NSDL and CDSL. This advantage eliminates the hassle of paperwork, transfers, and losses.

How does a share transaction work?

Whenever you buy shares, they are credited to your Demat account. Similarly, when you sell shares, they are debited from the account, and the payment is credited to your trading account/bank account.

Example : Suppose you bought 100 shares in January at ₹3,000 and another 100 shares in June at ₹3,200. Now, if you sell 100 shares, the question arises: which lot will be considered sold? This is where FIFO in Demat comes into play.

What is FIFO in Demat?

FIFO (First In, First Out) is a rule that states that when you buy shares of a company at different times and at different prices, the first shares you buy are considered when selling them. This isn’t an optional method, but rather a standard practice applicable to every investor in India.

Depositories that manage demat accounts NSDL and CDSL automatically apply this rule. This doesn’t affect the execution of your order; meaning, when you sell shares in the market, they are sold as normal. The difference is reflected only in your accounting and capital gains tax calculations.

Example

Bought 50 shares at ₹100

Bought 50 shares at ₹120

Sold 50 shares

Under the FIFO rule, the system will assume you sold the first 50 shares at ₹100. This will directly impact your profit-loss and tax calculations.

Why is FIFO Important in Demat Accounts?

The FIFO rule isn’t just a technical process for investors, but a crucial part of everyday investing. It determines how share purchases and sales are recorded in your demat account and how taxes are calculated.

Simplifies Tax Calculations : FIFO clarifies which shares are considered short-term gains and which long-term gains. This reduces the chance of error when filing income tax returns.

Eliminates Record Confidence : When the same shares are purchased at different dates and prices, it can be difficult to keep track of them. FIFO makes it clear which shares are considered sold first.

Same Rules Apply to Every Investor : Depositories like NSDL and CDSL apply FIFO to all demat accounts. This means that regardless of which broker you trade with, the rules remain the same.

Transparency and Trust : If FIFO were not in place, investors could choose which lots to sell first, which could lead to tax calculation errors. FIFO prevents this arbitrariness and makes the system reliable.

Helping Investors Prepare in Advance : People often sell shares without understanding FIFO and are later surprised by the tax implications. Knowing this rule can help you plan in advance when it’s best to sell.

The example below will help you understand how the FIFO rule applies:

Date

Transaction

Quantity (Share A)

Price per Share

Total Value

Status as per FIFO

January 2023

Bought

100

₹200

₹20,000

First purchased shares

June 2023

Bought

100

₹250

₹25,000

Later purchased shares

February 2024

Sold

100

₹300 (assumed)

₹30,000

January lot of 100 shares considered sold

Therefore, the profit will be ₹30,000 – ₹20,000 = ₹10,000.

Since the period from January 2023 to February 2024 is less than 12 months, this will be treated as short-term capital gain (STCG) and will be taxed at 20%.

FIFO vs Other Methods

Different methods are used around the world to record the purchase and sale of shares. In India, only FIFO (First In, First Out) is valid, but it’s important to understand the other methods as well.

LIFO (Last In, First Out) : In this method, the most recently purchased shares are considered the first to be sold. If it were implemented in India, short-term gains would often be higher because recent purchases would be deducted first.

Weighted Average : Here, the purchase price of all shares is added to arrive at an average, and profit or loss is determined based on that. It doesn’t matter which lot was purchased first or last. This method is common in many countries.

Specific Identification : In this, the investor can choose which lot to sell. This provides flexibility, but also increases the possibility of tax evasion or fraud.

Why FIFO in India?

The Income Tax Department has mandated FIFO to ensure uniform rules apply to everyone and transparent tax calculations. This prevents investors from arbitrarily trying to evade taxes.

Impact on Investors : FIFO simplifies the process and ensures uniform rules for everyone. However, this can sometimes prove costly for traders who frequently buy and sell in short periods of time, as they have to pay higher short-term gains tax.

The FIFO rule directly impacts the tax treatment of shares and equity mutual funds.

1. Short-Term Capital Gain (STCG)

If you sell equity shares or equity mutual funds within less than 12 months, the profit is considered STCG. This has changed since July 2024 and is now taxed at 20% (previously 15%).

2. Long-Term Capital Gain (LTCG)

If shares or funds are held for more than 12 months, the gain is classified as LTCG. Since Budget 2024, LTCG is taxed at 12.5%, and does not receive indexation benefit. ₹1,25,000 exemptionLong-term gains up to the first ₹1,25,000 per financial year are exempt from tax. Any gains above this limit will be taxed at 12.5%.

3. Difference due to FIFO

FIFO assumes that the oldest shares purchased are sold first. This means that even if you want to deduct new shares, tax will be calculated on the oldest shares. This can sometimes be beneficial (less tax due to LTCG being applied), and sometimes it can be detrimental (more tax due to STCG being applied).

4. ITR and Other Charges

The LTCG exemption of ₹1,25,000 under Section 112A is now clearly shown when filing ITR. A surcharge and a 4% health and education cess are also added to the tax. Capital gains are calculated after deducting brokerage, STT, and transaction charges.

Tips to Manage FIFO Impact in Your Portfolio

Keep track of purchases and sales : Make it a habit to note the date and price every time you buy or sell shares. This will clearly show you which shares are likely to be long-term and when selling them will result in lower tax.

Use the right tools : These days, on platforms like Zerodha Console, Pocketful, you can easily see which lot will be deducted first according to FIFO and how it will be taxed.

Remember the 12-month limit : If a lot is about to complete 12 months, it would be wise to wait a bit. This will allow you to avoid short-term tax and take advantage of the long-term tax rate.

Use loss harvesting : Losing shares can sometimes prove beneficial. By selling them, you can balance the FIFO gain and reduce your tax burden.

Keep your records updated : Fast-and-fast mistakes often occur during tax filing. Having your data and transaction records clear will help prevent last-minute stress.

Conclusion

Understanding FIFO in Demat is important not only for tax purposes but also for making better investment decisions. This rule ensures that every investor’s accounting is consistent and there’s no confusion. If you understand how FIFO affects your portfolio, you’ll be able to time your investments and improve your tax planning. Ultimately, it’s wise to adopt the rule to strengthen your investment strategy.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

You must have an individual demat account in which you can hold securities to create long-term wealth. But most of you are not aware of the HUF demat account in which you can manage the investment as the head of your family, known as “Karta”. Using this account, you can create wealth for your family.

In today’s blog post, we will give you an overview of an individual and an HUF demat account, along with the differences.

What is an Individual Demat Account?

An individual demat account is a personal demat account opened by an individual to hold, buy and sell securities, including shares, bonds, etc., in electronic form. Only the account holder in whose name the demat account is opened can operate it. An individual bank account can be linked with this demat account.

Key Features of an Individual Demat Account

The key features of an individual demat account are as follows:

Nominee: The individual demat account holder can nominate various individuals in their demat account so that in case of the death of the account holder, the securities can be easily transferred to the near ones.

Multiple Accounts: One can open multiple demat accounts with different stock brokers, using the same PAN Card.

Taxation: All the gains earned from this demat account are taxed as per the norms of individual capital gain.

Unique ID: As an individual can open multiple demat accounts, all the demat accounts have a separate user ID and identification number.

When a Hindu Undivided Family is considered a legal entity registered under the Hindu Law, opening a demat account to invest in shares, mutual funds, bonds, etc, is known as an HUF Demat Account. However, the account is opened in the name of HUF, but the Karta of the family operates it. All gains earned from investments in the name of an HUF are taxed as a separate entity.

Key Features of HUF Demat Account

The key features of an HUF demat account are as follows:

HUF Name: The HUF account is opened only in the name of the HUF and PAN, and not opened in the name of an individual.

Separate Entity: An HUF is considered a separate legal entity, and all the income is taxable as an independent entity.

Eligible Investment: An HUF can invest in almost all kinds of investments, such as shares, mutual funds, bonds, etc.

One Demat Account: An HUF can open only one demat account against its PAN, but individual members can still have their own separate demat accounts using their personal PANs.

Difference Between an Individual and an HUF Demat Account

The key differences between an individual and an HUF demat account are as follows:

Particular

Individual Demat Account

HUF Demat Account

Owned By

An individual account can be owned by an individual.

This account can be owned by a Hindu Undivided Family.

PAN Card

An individual’s PAN Card is linked to it.

HUF Pan Card is used in it.

Operation By

This account is solely operated by an individual.

A HUF demat account can only be operated by the head of the family, known as “Karta”.

Taxation

All the incomes generated from this account are taxed in the hands of the individual.

All investment income is taxed separately in the hands of HUF.

Number of Demat Accounts

An individual can open multiple demat accounts using the same PAN Card with different brokers.

Only one demat account is allowed to be opened using an HUF Pan Card.

Transmission

In case of the death of the account holder, the securities are transferred to the nominee.

In case of Karta’s death, a new Karta is appointed instead of transferring units.

Objective

The objective of an individual demat account is to create an individual’s wealth.

A HUF demat account is generally used to create wealth for the family.

Document’s

Only the document of the individual is required.

Along with the document of the HUF Karta’s documents are also required.

If you are looking to create wealth for your family or create a legacy for them, then you can consider opening an HUF demat account and operate it as the Karta of the family. However, if you are looking to create wealth for yourself, then you can open an individual demat account and manage your investment accordingly.

Conclusion

In conclusion, both the individual and the HUF demat account facilitate the holding of securities, such as shares, bonds, and ETFs, in electronic form. However, both of these accounts differ in terms of ownership and operation. Having an individual demat account helps in creating wealth for an individual, whereas an HUF demat account builds wealth for a Hindu Undivided Family, and it is operated by the Karta, who will be the head of the family. Choosing among these demat accounts totally depends on the objective of creating wealth.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Is there any difference between an individual and an HUF demat account?

An individual demat account can be opened and operated by only an individual, whereas the HUF demat account can only be operated by the head of the Hindu Undivided Family, known as Karta.

Can a person who is a Karta open a separate individual account?

Have you ever thought about how your valuable investments and shares are safely kept in the stock market world? This safety locker is called the Demat account, it acts similar to a bank account that securely holds your money, as Demat account acts as your digital wallet safeguarding your stocks, bonds and mutual funds in an electronic form.

Demat entered as a game changer as in primitive times stocks, bonds and even mutual funds were given on a paper based certificate which was susceptible to loss, theft or damage. Demat account offers you a seamless, secure and easy to manage online market holdings, that is accessible to you from anywhere at any time.

Demat Account an Overview

A Demat account is an account that holds shares and securities in electronic form, eliminating the need for physical certificates. It simplifies trading, transfer, and safekeeping of investments in the stock market.

Today, having a Demat account is mandatory if you want to invest in the stock market. In the old days, when you bought shares of a company, you would get actual paper certificates. The problem was, these physical certificates could be lost, stolen, damaged, or even faked. Transferring them to someone else was a slow process filled with paperwork. With a Demat account, all these certificates are stored electronically, making investing safer, faster, and hassle-free.

Guide to Demat Account Charges

Demat account charges are not as complicated as they sound. We can break them down into two simple categories, charges from your broker like Pocketful and charges from the government and other bodies.

1. Demat Account Opening Charges

This is a one time fee that some brokers charge you just to set up your account. Many traditional banks and full service brokers still have this fee.

But here’s the great news. At Pocketful, we believe starting your investment journey should be free. That’s why Pocketful has zero demat account opening charges. You can open your account with us and start your journey without paying a single rupee.

2. Demat Account AMC Charges

Annual Maintenance Charges, or AMC, is a fee that brokers charge every year to keep your account active. You can think of it as a small “rent” for your digital locker. This is a charge you have to pay even if you don’t make any trades during the year.

Here Pocketful makes a huge difference. We want you to feel comfortable, whether you invest daily or just once a year. Pocketful has zero demat account AMC charges. This means you save money every single year, money that can stay in your pocket or be invested for your future.

Many other brokers in the market charge an AMC, which can range from Rs.300 to over Rs.900 every year. This is a recurring cost that our users simply don’t have to worry about.

3. Brokerage and Transaction Fees

Brokerage is the fee your broker charges when you buy or sell shares. This is one of the most important demat account fees to understand because it can directly affect your profits.

There are two main types of brokers:

Full-Service Brokers : They often provide research and advice but charge a percentage of your trade value. So, the bigger your investment, the higher the fee.

Discount Brokers (like Pocketful) : Provides you a great platform for you to invest on your own, but at a much lower cost. They usually charge a flat fee, which makes the cost predictable.

Here is Pocketful’s simple and transparent brokerage structure :

Equity Delivery : When you buy shares and hold them for more than a day, it’s called a delivery trade. At Pocketful, the brokerage for this trade is Rs.0.

Intraday Trading and F&O : If you buy and sell on the same day (intraday) or trade in Futures & Options, we charge a flat fee of Rs.20 per executed order, or 0.03% of the order value, whichever is lower. It’s simple, flat, and predictable.

4. Government and Depository Charges

These charges are not from your stockbroker. They are a part of the system for every investor in India, no matter which broker you choose.

DP (Depository Participant) Charges : When you sell shares from your Demat account, a small fee is charged by the depository (CDSL) and the DP (Pocketful). This is for the service of debiting the shares from your account. At Pocketful, this charge is just Rs.13.5 + GST per transaction.

Taxes (STT & GST) :

STT (Securities Transaction Tax) : This is a small tax paid directly to the government when you trade on the stock exchange i.e. 0.1% on both buying and selling.

GST : This is the standard Goods and Services Tax, which is 18% applied to the broker’s fees (like brokerage, transaction charges, SEBI turnover fees and other taxes).

Stamp Duty : This is a tax charged by the state government on all your ‘buy’ transactions. (0.015% on turnover of buy delivery orders)

Exchange Transaction Charges : The stock exchanges (NSE and BSE) charge a very tiny fee on your trades for providing the trading platform. (BSE: 0.00375% NSE: 0.00297%)

SEBI Turnover Fees : This is a small fee charged by Securities and Exchange Board of India when you buy or sell in the stock market. This fee is generally collected by your broker to cover regulatory and developmental expenses of SEBI. (0.0001% of the turnover)

To make it even simpler, here is a quick look at Pocketful’s main charges:

Charge Type

Pocketful’s Fee

Account Opening

₹0

Annual Maintenance (AMC)

₹0

Equity Delivery Brokerage

₹0

Intraday & Futures Brokerage

₹20 per executed order or 0.03% of turnover, whichever is lower

Safety : Your investments are held digitally, so there’s no risk of theft, loss, or damage.

Convenience : You can access and manage your portfolio from anywhere, at any time, using your phone or laptop.

Speed : Buying and selling happen quickly, with shares getting credited or debited from your account in just a day or two (T+1 settlement).

Easy Tracking : You can see all your different investments like shares, bonds, mutual funds at one single place.

Loan Facility : You can use the securities in your Demat account as collateral to get a loan from a bank if you require funds.

Disadvantages

Costs are Involved : There are multiple charges attached as we’ve discussed earlier. But by choosing a discount broker like Pocketful, you can minimize these charges, especially with our zero AMC policy.

Requires Technology : To operate a Demat account, you need a smartphone or computer and an internet connection. This can be a challenge for people who are not comfortable with technology.

Risk of Over trading : Because it’s so easy to buy and sell, some people might be tempted and can do emotional trading too often without a proper plan. This can lead to losses.

Key Factors to Consider

Go Paperless : Always choose email statements and contract notes. Asking for physical copies can lead to courier charges.

Trade Online : Placing orders over the phone with a dealer is called ‘Call & Trade’, this service usually has an extra charge. At Pocketful, it’s Rs.25 + GST per order. Using our free online platform is a smarter choice.

Consolidate Your Accounts : If you have multiple Demat accounts with other brokers that you don’t use, consider closing them. This will reduce confusion and help you avoid any maintenance charges they might be adding.

Intraday Timings : If you are an intraday trader, make sure to close your open positions before the market closes. If you don’t, the broker will automatically close them, which can attract an ‘auto-square off’ penalty. At Pocketful, this is Rs.25 + GST per order.

With a transparent partner like Pocketful, these charges are not hidden but are clear and manageable part of your plan. Our zero demat account opening charges and zero demat account amc charges are designed to remove the biggest cost barriers, especially for new investors.

Your financial future is in your hands. Now that you understand the costs, you can start your journey with confidence. Join the club of zero fees and infinite possibilities with Pocketful.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Yes, you can open multiple Demat accounts with different brokers. However, you cannot open more than one account with the same broker. All your accounts are linked to your single PAN card, which helps in tracking.

What is the main difference between a Demat and a Trading account?

Trading account is the ‘shopping cart’ you use to place buy and sell orders in the market. The Demat account is the ‘digital house’ where you safely store the shares you have bought, you need both to invest.

What happens to the shares in my Demat account if something happens to me?

Your Demat account comes with a nomination facility. You can appoint a nominee (like a family member) who will receive all the securities in your account in case of an unfortunate event. This ensures a smooth and easy transfer of your wealth.

Are shares safe with a discount broker?

Absolutely. Your shares are not held by Pocketful directly. They are held in your name with the central depository (CDSL), which is regulated by SEBI. This is true for all brokers, whether they are discount or full-service brokers.

Do I have to pay charges even if I don’t trade?

With many brokers, you have to pay the Annual Maintenance Charge (AMC) every year, even if you don’t trade at all. This is a key advantage with Pocketful, since our AMC is zero, you pay nothing if you are inactive. You only incur charges like DP charges when you actually sell shares.

Whenever you log in to your trading and demat account, you will see numerous figures displaying your balances, including ledger balance, available balance, and margins. Among all these, the ledger balance holds the key position. But do you know what exactly a ledger balance means?

In today’s blog post, we will give you an overview of what a ledger balance is, its importance, and the difference between a ledger balance and an available balance.

What is Ledger Balance in a Demat Account?

The ledger balance in a demat account is a balance which reflects the total settled funds in your trading account, which is linked to your demat account. This balance is the final figure reflecting all the purchasing, selling, and settlement processes of a day. However, it excludes all unsettled trades and any pending withdrawal.

A trader can track the net movement of funds resulting from the purchase and sale of shares, including brokerage fees and other charges.

Features of Ledger Balance

The important key features of a ledger balance are as follows:

Net Fund: The ledger balance reflects the net fund after adjusting all debit and credits.

Charges: All kinds of charges, including brokerage, STT, GST, etc., are factored into this ledger balance.

Updation: The ledger balance updates regularly. Whenever any financial transaction takes place in your demat account, the ledger balance updates immediately.

Unsettled Transactions: The ledger balance may sometimes display the amount from recent trades.

Verification: Ledger can be useful for an investor while reconciling the brokerage and other charges paid by a trader.

Difference Between Ledger Balance and Available Balance

The key difference between the ledger balance and available balance is as follows:

Particular

Ledger Balance

Available Balance

Settlement

Ledger balance may include the amount of unsettled trades.

Available does not include any amount of unsettled trades.

Frequency

Updates once per business day, typically overnight, after all transactions have been Processed.

This only updates whenever there is any kind of debit or credit of funds in your account.

Importance

It helps in tracking all the financial transactions of your trading and demat account.

The available balance only helps you in identifying the amount available for trade and withdrawal.

Settlement

Ledger balance includes the amount of unsettled trades.

Available balance does not include the amount from any unsettled trades; it only includes the amount which is available for use.

Objective

The objective of the ledger balance is to show you the overall fund position.

The objective of the available balance is to reflect the investable and withdrawal amount.

The key importance of the ledger balance in demat account is as follows:

Tracking Expenses: The ledger balance of a trader reflects all the charges, such as brokerage fees, taxes, etc. Hence, one can easily track all such expenses.

Reduce Overtrading: Once you know the ledger balance, you can avoid overtrading by evaluating the trading limit of the ledger account.

Transparency: Ledger balance account is an official record maintained by your stockbroker. This provides transparency on what kind of charges are deducted from your trading and demat account.

Planning: It helps in planning your future trade based on the available balance in your ledger account.

Mismatch in Balance: Ledger balance helps resolve the disputes related to any unnecessary expenses deducted from your demat account.

How ledger balance affects your trading decision

The key factors which can affect your trading decision are as follows:

Identifying True Purchasing Power: Ledger balance shows a complete picture of your account, hence it can give you an estimation of the amount which you can utilise for trading.

No Rejection of Orders: If you trade based on your available balance instead of your ledger balance, your order might get rejected due to insufficient settled funds.

Reinvestment: If you sold any shares, then the proceeds of such trade start reflecting in your available balance account immediately, but you can only invest based on the ledger balance.

Margin Eligibility: Brokers generally calculate the margins based on the ledger balance. Hence, if you plan to trade on margin, then the ledger balance can help you in calculating the margin availability.

Tips to Monitor Your Ledger Balance

The important tips that one should remember while monitoring their ledger balance are as follows:

Checking Balance: One should check their ledger balance before executing any trade, and should not rely on the available balance.

Pending Dues: Always keep a track of your ledger balance in order to avoid any penalties due to an unsettled amount.

Detail View: A trader is required to check the detailed ledger balance in order to check if there are any penalties or additional charges deducted by their broker.

Corporate Cycle: Equity trades follow a T+1 settlement cycle, which can help in evaluating the available ledger balance.

On a concluding note, a ledger balance in your demat account is a key figure which you need to check before placing any buy order. It includes the complete record of your trades, including credit, debit, charges, and any unsettled trades. Understanding your ledger balance can help you make informed decisions and avoid any penalties due to an insufficient balance. Therefore, it is advisable to check your ledger balance before executing any trade.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What is the difference between a ledger balance and an available balance?

The ledger balance will reflect total funds available in your demat account, including unsettled balances of a trade, while the available balance will reflect only the funds which can be used for trading or withdrawal.

Can a ledger balance show negative figures?

Yes, a ledger balance can be negative if your account has any pending charges or penalties that exceed your available funds.

What is the frequency of updating the ledger balance?

The ledger balance is generally updated by your broker on a real-time basis.

Can I withdraw my full ledger balance?

If your ledger balance has any unsettled trade, then you cannot withdraw it. You can withdraw only the available balance from your trading and demat account.

What happens if my trading account balance shows a negative figure?

Whenever your ledger balance shows a negative figure, it indicates that there might be some unpaid dues, such as pending margins, unpaid charges, annual maintenance charges, etc.

If you have ever faced difficulty in selling or pledging shares while trading in the stock market, then the old POA system has been a big reason behind it. Now SEBI has implemented a new system to make it better and safer – DDPI (Demat Debit and Pledge Instruction). This method makes the process of debiting and pledging shares in your demat account easy and transparent.

In this blog we will understand in simple language the meaning of DDPI, the role of DDPI in the stock market, its advantages, disadvantages and how to activate it.

What is DDPI?

DDPI i.e. Demat Debit and Pledge Instruction, is a document that you sign and give to your broker so that he can debit (sell) or pledge shares from your demat account only after your approval. This is a more secure and limited authority method than the old Power of Attorney (POA), in which the broker gets permission to only sell and pledge that too when you do the transaction yourself.

Why was DDPI introduced?

There was more risk in the old POA system : Earlier investors had to give POA to the broker, which gave them full authority to sell or transfer shares from your demat account. In many cases, some brokers misused this right, causing loss to investors.

It was necessary to provide a safe and controlled method to investors : SEBI realized that the POA system was becoming unsafe for investors. Therefore, in 2022, SEBI issued a new rule, making DDPI an alternative to POA. Through this, investors now allow only those transactions that they initiate themselves.

Changes necessary for transparency and trust : DDPI has promoted transparency and investor protection in the stock market. Now the broker cannot touch your shares unless you yourself give a sell or pledge instruction. This gives complete control to the investor.

POA vs DDPI: What’s the Real Difference?

Feature

POA (Old Method)

DDPI (New Method)

Scope

Broad: complete freedom to sell, transfer and pledge shares

Limited: only allowed to sell and pledge

Security Risks

Higher risk of misuse

Low as action only takes place with your approval

Revocation

The process is complex and time consuming

Easy as DDPI can be deactivated in just a few steps

Control

Broker had quite broad rights

The investor retains full control

Is DDPI Mandatory for Stock Market Investors?

It is not mandatory for all investors to implement DDPI i.e. Demat Debit and Pledge Instruction. SEBI has introduced it as an optional facility, which aims to provide more security and convenience to investors. That is, if you want, you can sign DDPI, and even if you do not, you can continue trading.

1. For which investors is DDPI more useful?

If you are an active trader and regularly buy and sell shares, or want to take margin by pledging your shares, then DDPI can prove to be very useful for you. This eliminates the need to enter OTP every time, which makes transactions quick and seamless.

2. What if DDPI is not there?

If you have not activated DDPI, then every time you sell shares, you will have to go through the eDIS (Electronic Delivery Instruction Slip) process. In this, an OTP comes on your registered mobile or email, which is entered only after which the shares are debited. This method can be a little time consuming, especially when orders need to be executed quickly in the market.

3. Where does DDPI not apply?

DDPI is required only in cases of selling shares or making a pledge. If you make investments like IPO, mutual fund, or SIP, then DDPI has no role in it. A different process is adopted for such investments in which DDPI is not required.

Activating Demat Debit and Pledge Instruction (DDPI) has become very easy these days. Whether you are opening a new demat account or using an existing one, you can activate DDPI either online or offline.

1. How to activate DDPI while opening a new account?

When you open a new demat account with a broker like Pocketful, the option to sign DDPI is given during the account opening process itself. This process is completely digital and you can easily complete it through Aadhaar-based eSign. Once signed, the broker registers the DDPI with your depository (NSDL or CDSL).

2. How to add DDPI to an already opened account?

If you have already opened an account and did not sign DDPI at that time, you can easily activate it later. For this, most brokers provide DDPI activation facility through online platforms or mobile apps.

3. How do Pocketful users activate DDPI?

If you have opened your account on the Pocketful App, the DDPI option is available at the time of account opening. If you did not sign up for DDPI at that time, you can activate it later.

4. How to activate DDPI on Pocketful App

Open the App > Go to Menu > Select Account Settings > Click on “DDPI” section > eSign using Aadhaar. The same facility is available on the web portal as well, where you can activate DDPI by filling the DDPI form or digitally.

5. How long does activation take?

In most cases, DDPI activation happens within 24 to 48 hours. Once it is activated, you can trade faster without the hassle of eDIS or OTP.

6. Using POA? Switch to DDPI now

If you have signed a POA earlier, you can switch to DDPI by requesting your broker. Most brokers now complete this process online, so you do not need additional documentation.

Benefits of DDPI for Retail Investors

DDPI is Safer than POA : DDPI i.e. Demat Debit and Pledge Instruction, is much safer than the traditional Power of Attorney (POA). POA gives brokers a lot of rights, whereas DDPI only allows limited and necessary tasks, which keeps your share account safe.

Get rid of OTP-based selling : If you have activated DDPI, you do not need to enter OTP every time you sell shares (as is the case with eDIS). This makes the trading experience smoother and faster, especially when you want to react immediately to market fluctuations.

Fast and Hassle-Free Execution : The trading process is much faster with DDPI because there is no need for manual steps like OTP or confirmation. This allows your deals to be executed immediately, which is especially beneficial for intraday traders.

Necessary for Margin Trading : If you want to trade through margin by pledging shares, then DDPI is necessary. It allows you to pledge your shares, which is not possible through POA or eDIS.

Control remains in your hands : DDPI gives you complete transparency and control. You decide for yourself what the brokerage firm can and cannot do. This gives peace of mind and you can invest without worry.

Completely Optional and Flexible : The best thing is that filling DDPI is not mandatory. If you do not want to activate it, you can opt for eDIS or POA. This gives you complete freedom to choose the option as per your convenience.

Limitations of DDPI

Not every brokerage is completely paperless : There is a perception that DDPI makes the entire process digital, but in reality, some brokers still ask for a signed physical copy for DDPI activation. This means you have to print the form, sign it and send it back which can be time-consuming and hassle in today’s digital age.

Not useful for all types of transactions : DDPI is used only for limited purposes, such as selling or pledging stocks. But if you want to transfer mutual funds, government bonds or other demat holdings, DDPI does not work there. Hence, you have to resort to different methods.

It is not easy to remove DDPI : If you want to cancel DDPI in the future, many brokers ask for an offline physical request for the same. This means you may have to fill and post a form to cancel DDPI, which makes the whole process a bit sluggish and inconvenient.

Not very important for those who trade less : If you trade only once or twice a month, you may not feel the need for DDPI. For such investors, eDIS (Electronic Delivery Instruction Slip) or OTP verification also works. DDPI is more useful for those who trade frequently or regularly.

Conclusion

DDPI i.e. Demat Debit and Pledge Instruction has made trading in the stock market a little easier. Now there is no need to enter OTP or give extra permission every time you sell shares – once DDPI is activated, the work is done quickly and securely. Yes, this is not necessary for all investors, but if you trade regularly and want to avoid frequent hassles, then DDPI can prove to be a good option. This is a small but important step towards smart trading.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

If you are an NRI with earnings in India and are looking for an option to deploy this income and earn returns, there are various options such as equities, mutual funds, bonds, etc. However, to invest in these assets, you are required to open a non-repatriable demat account.

In this blog, we will explain to you what a non-repatriable demat account is, and how it works.

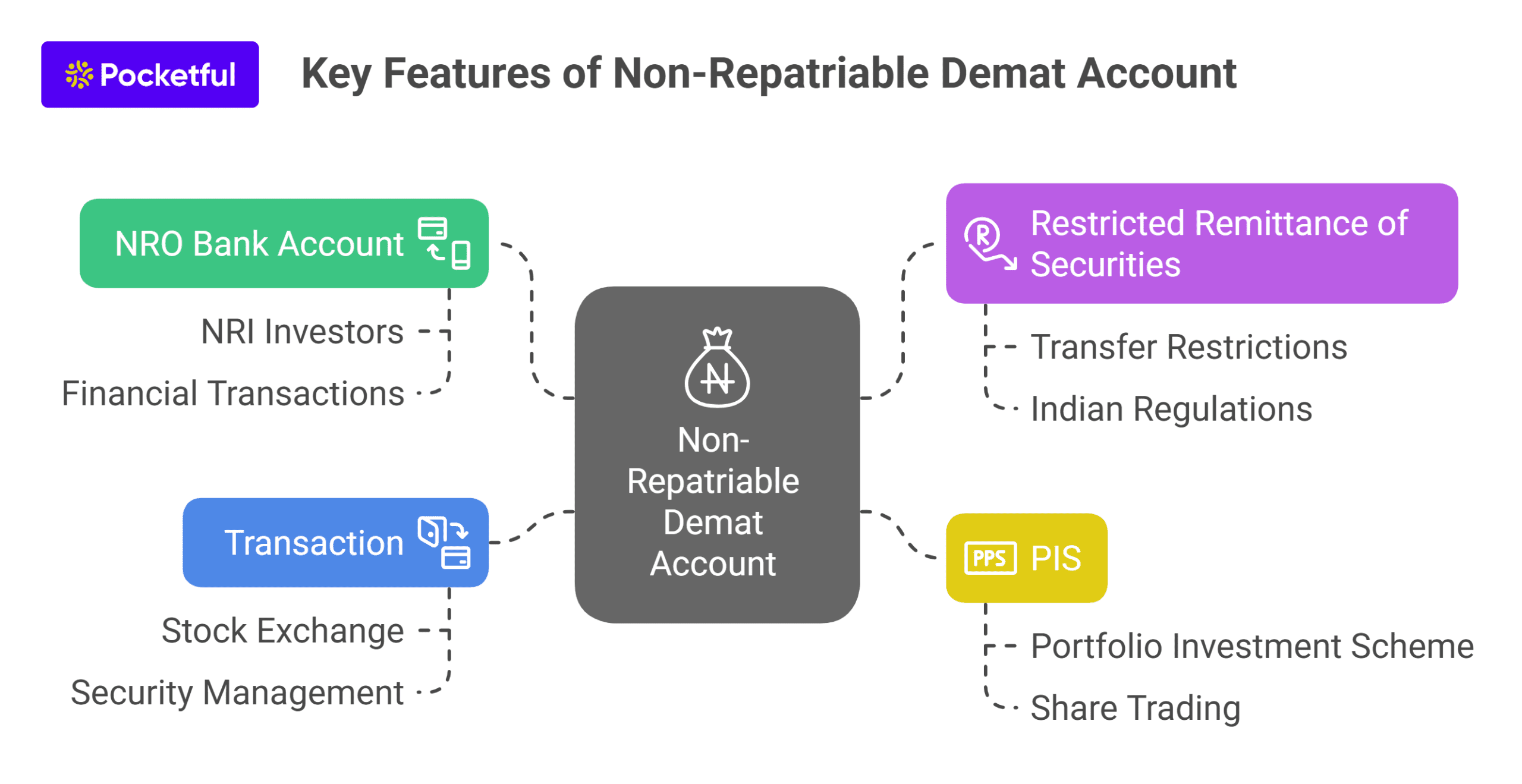

What is a Non-Repatriable Demat Account?

A Non-Repatriable Demat Account can be opened by non-resident individuals who wish to invest in shares, bonds, and mutual funds in India. There are certain restrictions on the transfer of funds of these accounts, i.e. the income earned on investments held in these accounts cannot be easily transferred out of India. Non-repatriable means funds cannot be freely transferred abroad, but remittance is allowed up to $1 million per financial year, subject to conditions. As it is mandatory to hold shares, etc., in electronic form in a demat account, a non-repatriable demat account makes sure that funds are not easily transferable from India.

The key features of a non-repatriable demat account are as follows:

NRO Bank Account: The non-repatriable demat account must be linked with the Non-Resident Ordinary bank account.

Restricted Remittance of Securities: The holdings in a non-repatriable demat account cannot be freely transferred out of India easily.

PIS: A non-repatriable account generally does not require a separate PIS (Portfolio Investment Scheme) account for buying and selling shares.

Transaction: It allows NRI investors to hold and sell securities on the stock exchange easily.

How a Non-Repatriable Demat Account Works

A non-repatriable demat account is specially for NRIs. Let’s see how this non-repatriable demat account works:

Investment: The non-repatriable demat account is used by an NRI to invest funds earned in India into Indian securities such as bonds, shares, mutual funds, etc.

Restriction on Transferring Funds: The funds in a non-repatriable demat account are not freely transferable. The interest and principal amount from the account can be transferred only after deducting tax.

NRO Account: The non-repatriable demat account is only for NRIs, and only a Non-Resident Ordinary (NRO) can be linked with a non-repatriable demat account.

Limited Investment: An NRI can invest only up to 5% in a company’s paid-up capital through these accounts.

Let’s understand how a non-repatriable demat account works through an example.

Mr. A has been an NRI working in Dubai for the last five years. He owns a flat in New Delhi, which he rented out for ₹20,000 per month. He wishes to invest the rent received from this flat into mutual funds in the form of an SIP. For this, he is required to open an NRO bank account, after which he needs to open a demat account, which is non-repatriable in nature, as he wishes to invest in mutual funds through a demat account. He linked his NRO bank account to his non-repatriable demat account and bought mutual funds. The principal and interest earned on the investment can be repatriated up to $1 million annually.

Difference Between Repatriable Demat Account and Non-Repatriable Demat Account

There are certain differences between Repatriable and Non-Repatriable Demat Accounts, which are as follows:

Particulars

Repatriable Demat Account

Non-Repatriable Demat Account

Objective

Freely invest in India and transfer funds to another country.

To invest in India and retain income within the country.

Bank Account

Only an NRE (Non-Resident External) account can be linked with a repatriable demat account.

A NRO (Non-Resident Ordinary) bank account is allowed to be attached to this demat account.

Fund

One can invest their foreign income and overseas savings through a repatriable demat account.

Income earned in India can be invested through a non-repatriable demat account.

Repatriation

Repatriation is allowed in this demat account as both principal and gains can be easily transferred to another country.

Repatriation of principal and interest earned is allowed up to $1 million per year.

Taxation

Some incomes may be exempted.

The income and gains generated through this demat account are fully taxable in India.

PIS Scheme

It requires PIS permission.

It does not always require PIS permission, as there are certain non-PIS routes available.

Limit

There is no limit on repatriation funds from this account.

There is a limit defined by the RBI to remit money from a non-repatriable demat account.

Suitability

This account is ideal for NRIs who wish to move funds out of India.

It is suitable for NRIs who want to keep their funds and use them in India.

On a concluding note, a non-repatriable account is mandatory for an NRI who wishes to invest in India and does not want to take the income outside. You can easily open a non-repatriable demat account with a registered stockbroker. However, there are certain restrictions placed by the RBI regarding the transfer of funds from this demat account, therefore, if you are an NRI and wish to invest income generated in India in the Indian stock market, then you must consult your investment advisor.

Frequently Asked Questions (FAQS)

Can anyone open a non-repatriable demat account?

Only an NRI (Non-Resident Individual) and any Person of Indian Origin (PIO) can open a non-repatriable demat account.

Which account is required to link with a non-repatriable demat account?

Only an NRO (Non-Resident Ordinary) bank account can be linked with a non-repatriable demat account.

Can I transfer funds to any other country from a non-repatriable demat account?

No, you cannot transfer funds from a non-repatriable demat account; however, the RBI has allowed certain exemptions through which you can transfer funds up to $1 million annually.

In which financial investment option can we invest through a non-repatriable demat account?

An NRI can invest in stocks, mutual funds, IPOs, ETFs, and Bonds through a non-repatriable demat account.

Can I convert a non-repatriable demat account to a repatriable demat account?

No, you cannot convert a non-repatriable demat account to a repatriable one. For this, you must close your existing account and open a new repatriable demat account.

डिजिटल दौर में निवेश की शुरुआत अब डीमैट अकाउंट के बिना मुमकिन नहीं। मार्केट में पॉकेटफुल, ज़ेरोधा, ग्रो, एंजेल वन, अपस्टॉक्स जैसे कई ऑप्शन मौजूद हैं, लेकिन इतने सारे विकल्पों के बीच सही प्लेटफ़ॉर्म चुनना अक्सर मुश्किल हो जाता है। किसी को लॉन्ग टर्म इन्वेस्टमेंट चाहिए, कोई एक्टिव ट्रेडिंग करता है, तो कोई सिर्फ़ म्यूचुअल फंड्स में पैसे लगाता है। इस ब्लॉग में 2025 के टॉप 15 डीमैट अकाउंट्स की लिस्ट दी गई है और उनके चार्जेज़, फीचर्स, फ़ायदे और किसके लिए कौन सा बेस्ट है आसान भाषा में समझाया गया है।

डीमैट अकाउंट क्या होता है और क्यों ज़रूरी है?

डीमैट अकाउंट यानी डिमैटेरियलाइज़्ड अकाउंट, एक ऐसा खाता होता है जिसमें शेयर और सिक्योरिटीज़ को डिजिटल रूप में रखा जाता है। पहले जब कोई शेयर खरीदा जाता था, तो उसकी फिज़िकल कॉपी मिलती थी यानी कागज़ पर छपा हुआ सर्टिफिकेट। लेकिन आज के डिजिटल ज़माने में सारी ट्रेडिंग ऑनलाइन होती है, इसलिए हर इन्वेस्टर को एक डीमैट अकाउंट की ज़रूरत पड़ती है।

जैसे बैंक अकाउंट में पैसे रखे जाते हैं, वैसे ही डीमैट अकाउंट में शेयर, म्यूचुअल फंड, बॉन्ड, ईटीएफ जैसे इन्वेस्टमेंट डिजिटल रूप में स्टोर किए जाते हैं।

ये अकाउंट दो मुख्य डिपॉज़िटरी – एनएसडीएल (नेशनल सिक्योरिटीज़ डिपॉज़िटरी लिमिटेड) और सीडीएसएल (सेंट्रल डिपॉज़िटरी सर्विसेज़ लिमिटेड) – से जुड़े होते हैं, जो इन सिक्योरिटीज़ को सुरक्षित डिजिटल फॉर्म में बनाए रखते हैं।

डीमैट अकाउंट के ज़रिए शेयर मार्किट में निवेश करना न सिर्फ़ तेज़ और आसान होता है, बल्कि इसमें फिज़िकल सर्टिफिकेट्स के गुम होने, चोरी या फ्रॉड का कोई रिस्क भी नहीं होता।

डीमैट अकाउंट खोलते समय किन बातों का ध्यान रखें?

डीमैट अकाउंट ओपन करना तो आसान है, लेकिन ब्रोकर बहुत सोच-समझकर चुनना चाहिए। नीचे कुछ इंपॉर्टेंट पॉइंट्स दिए गए हैं जो डिसीजन लेने से पहले ज़रूर चेक करने चाहिए:

सेबी-रजिस्टर्ड ब्रोकर: हमेशा ऐसा ब्रोकर चुनना चाहिए जो सेबी से रजिस्टर्ड हो, ताकि इन्वेस्टर फंड्स और डेटा सुरक्षित रहें।

अकाउंट ओपनिंग फीस: कुछ ब्रोकर्स ₹0 में अकाउंट ओपन कराते हैं, जबकि कुछ नॉमिनल फीस लेते हैं। शुरुआत में ये चार्जेस कंपेयर करना ज़रूरी होता है।

एएमसी (अकाउंट मेंटेनेंस चार्जेस): एएमसी हर साल लिया जाने वाला चार्ज है। कई ब्रोकर्स पहले साल फ्री देते हैं, लेकिन बाद में चार्ज बढ़ सकते हैं , इसे ध्यान से देखना चाहिए।

ब्रोकरेज चार्जेस: यह वो फीस है जो हर ट्रेड पर लगती है। डिस्काउंट ब्रोकर्स ₹20 पर ऑर्डर या उससे भी कम में ट्रेड अलाउ करते हैं। हाई फ्रिक्वेंसी ट्रेडर्स के लिए यह काफी इंपॉर्टेंट होता है।

मार्जिन इंटरेस्ट: अगर मार्जिन पर ट्रेड करना है, तो ब्रोकर कितना इंटरेस्ट चार्ज करता है, यह भी चेक करना चाहिए। हिडन चार्जेस से बचने के लिए ये पॉइंट ध्यान रखें।

रिसर्च टूल्स और इनसाइट्स: ब्रोकर्स जो इन-डेप्थ रिसर्च रिपोर्ट्स, स्टॉक स्क्रीनर्स और टेक्निकल टूल्स प्रोवाइड करते हैं, वो लॉन्ग-टर्म इन्वेस्टिंग के लिए बेहतर होते हैं।

कस्टमर सपोर्ट: एक ज़रूरी फैक्टर है। डीमैट अकाउंट में कोई भी प्रॉब्लम आने पर क्विक और हेल्पफुल सपोर्ट चाहिए होता है। इसलिए ऐसा ब्रोकर चुनना बेहतर है जिसकी कस्टमर सर्विस फास्ट और रिलायबल हो।

2026 के टॉप 15 बेस्ट डीमैट अकाउंट in India

ब्रोकर

अकाउंट ओपनिंग फीस

एएमसी (अकाउंट मेंटेनेंस चार्जेस)

ब्रोकरेज चार्जेस

यूनीक फीचर्स

पॉकेटफुल

₹ 0

₹ 0

पॉकेटफुल देता है ₹0 डिलीवरी चार्जेस की सुविधा।

कटिंग-एज टेक्नोलॉजी से एक ही जगह मल्टीपल एसेट क्लासेस में इन्वेस्ट किया जा सकता है।

ज़ेरोधा

₹ 0

₹300 + जीएसटी

₹20 या 0.03% प्रति ऑर्डर जो भी कम हो।

यूज़र-फ्रेंडली प्लेटफॉर्म और ईज़ी लर्निंग टूल्स।

एंजेल वन

₹ 0

₹240 (पहला साल फ्री)

₹20 प्रति ऑर्डर

डीटेल्ड रिसर्च और वर्सेटाइल मोबाइल ऐप।

आईसीआईसीआई डायरेक्ट

₹ 0

₹ 700

इक्विटी डिलीवरी पर 0.55%, इंट्राडे पर 0.275%

3-in-1 अकाउंट के साथ एक्स्टेंसिव रिसर्च।

कोटक सिक्योरिटीज़

₹ 0

₹ 600

इक्विटी डिलीवरी पर 0.49%, इंट्राडे पर 0.049%

एडवांस्ड ट्रेडिंग टूल्स और पर्सनलाइज़्ड एडवाइजरी।

अपस्टॉक्स

₹ 0

₹ 150

₹20 या 0.05% प्रति ऑर्डर

लो ब्रोकरेज फीस और आसान प्लेटफॉर्म।

5पैसा

₹ 0

₹ 300

₹20 प्रति ऑर्डर

फ्लैट ब्रोकरेज रेट्स और म्यूचुअल फंड इन्वेस्टमेंट्स।

शेयरखान

₹ 0

₹ 400

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.1%

ट्रेनिंग प्रोग्राम्स और एडवांस्ड ट्रेडिंग प्लेटफॉर्म्स।

मोतीलाल ओसवाल

₹ 0

₹ 199

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.05%

पर्सनलाइज़्ड एडवाइजरी और पोर्टफोलियो मैनेजमेंट।

एसबीआई सिक्योरिटीज़

₹ 0

₹750 (पहला साल फ्री)

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.05%

3-in-1 अकाउंट और स्ट्रॉन्ग बैंकिंग इंटीग्रेशन।

एक्सिस डायरेक्ट

₹ 0

₹ 750

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.05%

सीमलेस फंड ट्रांसफर और एडवांस्ड रिसर्च टूल्स।

आईआईएफएल सिक्योरिटीज़

₹ 0

₹ 250

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.05%

फ्री रिसर्च रिपोर्ट्स और एडवाइजरी सर्विसेज़।

एडलवाइस ब्रोकिंग

₹ 0

₹ 500

इक्विटी डिलीवरी पर 0.5%, इंट्राडे पर 0.05%

रिसर्च-ड्रिवन एडवाइजरी और डायवर्स इन्वेस्टमेंट ऑप्शंस।

ग्रो

₹ 0

₹ 0

₹20 या 0.01% प्रति ऑर्डर

ज़ीरो एएमसी और यूज़र-फ्रेंडली प्लेटफॉर्म।

पेटीएम मनी

₹ 0

₹ 0

₹20 प्रति इंट्राडे ऑर्डर और ₹20 डिलीवरी के लिए

पेटीएम इकोसिस्टम से इंटीग्रेटेड और लो ट्रांज़ैक्शन कॉस्ट्स।

ट्रेडर्स और इन्वेस्टर्स के लिए टॉप 15 डीमैट अकाउंट्स का ओवरव्यू

ट्रेडर्स और इन्वेस्टर्स के लिए टॉप 15 डीमैट अकाउंट्स का ओवरव्यू नीचे दिया गया है:

1. पॉकेटफुल

पॉकेटफुल एक नई पीढ़ी की डिस्काउंट ब्रोकिंग कंपनी है, जो इक्विटी, कमोडिटी, डेरिवेटिव्स जैसे कई निवेश विकल्प प्रदान करती है। इसका लॉन्च 2024 में हुआ था और यह पेस फाइनेंशियल ग्रुप के अंतर्गत काम करती है। पॉकेटफुल को 27 साल से अधिक अनुभव वाले प्रोफेशनल्स ने विकसित किया है, जिससे यूज़र को बेहतरीन और भरोसेमंद ट्रेडिंग एक्सपीरियंस मिलता है।

पॉकेटफुल की सबसे बड़ी खासियत यह है कि इक्विटी डिलीवरी ट्रेड्स पर कोई ब्रोकरेज चार्ज नहीं लिया जाता, साथ ही अकाउंट खोलने और अकाउंट मेंटेनेंस चार्ज भी फ्री है। इसलिए यह प्लेटफ़ॉर्म शुरुआती और अनुभवी दोनों तरह के निवेशकों के लिए एक बढ़िया विकल्प है।

मुख्य फीचर्स:

इक्विटी डिलीवरी ट्रेड्स पर शून्य ब्रोकरेज।

अकाउंट खोलने की प्रक्रिया बहुत आसान और केवल 5 मिनट में पूरी हो जाती है।

एपीआई सपोर्ट, जिससे अपनी ट्रेडिंग स्ट्रेटेजीज को कस्टमाइज़ और ऑटोमेट किया जा सकता है।

सबसे बेहतर किसके लिए: पॉकेटफुल उन यूज़र्स के लिए बढ़िया है, जो बिना किसी अतिरिक्त चार्ज के एडवांस्ड ट्रेडिंग प्लेटफॉर्म चाहते हैं।

2. ज़ेरोधा

ज़ेरोधा देश की सबसे बड़ी और भरोसेमंद डिस्काउंट ब्रोकिंग फर्मों में से एक है। इसे 2010 में कामथ ब्रदर्स ने शुरू किया था और इसने फ्लैट ब्रोकरेज मॉडल के जरिए ब्रोकिंग इंडस्ट्री में नया ट्रेंड सेट किया। ज़ेरोधा का प्लेटफ़ॉर्म तकनीकी रूप से बहुत एडवांस्ड और यूज़र-फ्रेंडली है, जो ट्रेडिंग को आसान, किफायती और सभी के लिए एक्सेसिबल बनाता है, खासकर नए इन्वेस्टर्स के लिए।

मुख्य फीचर्स:

सिंपल और यूज़र-फ्रेंडली ट्रेडिंग प्लेटफ़ॉर्म।

डेडिकेटेड कस्टमर सपोर्ट टीम, जो आपकी हर क्वेरी का जल्दी समाधान करती है।

वैरिसिटी (Varsity) नाम का फ्री एजुकेशन प्लेटफ़ॉर्म, जहां स्टॉक मार्किट से जुड़ी डीप जानकारी और सीखने के अवसर मिलते हैं।

बेस्ट फॉर:जो इन्वेस्टर्स लो ब्रोकरेज पर ट्रेड करना चाहते हैं और टेक्नोलॉजी-ड्रिवन प्लेटफ़ॉर्म पसंद करते हैं, उनके लिए ज़ेरोधा एक परफेक्ट चॉइस है।

3. एंजेल वन

एंजेल वन भारत की टॉप फुल-सर्विस ब्रोकिंग कंपनियों में से एक है, जिसकी स्थापना 1996 में हुई थी। यह प्लेटफ़ॉर्म इक्विटी, कमोडिटी, डेरिवेटिव्स समेत कई असेट क्लास में ट्रेडिंग और इन्वेस्टमेंट की सुविधा देता है। साथ ही, एंजेल वन इन्वेस्टमेंट एडवाइजरी सर्विसेज भी प्रोवाइड करता है, जो यूज़र्स की वित्तीय ज़रूरतों को बेहतर तरीके से पूरा करता है। इसका ट्रेडिंग प्लेटफ़ॉर्म एडवांस टेक्नोलॉजी से लैस है और यूज़र की सहूलियत को ध्यान में रखकर डिजाइन किया गया है।

मुख्य फीचर्स:

पर्सनलाइज़्ड कस्टमर-फोकस्ड अप्रोच, जो हर यूज़र को खास अनुभव देता है।

एंजेल वन ऐप में एडवांस्ड ट्रेडिंग टूल्स उपलब्ध हैं, जो ट्रेडिंग को आसान और प्रोफेशनल बनाते हैं।

पूरे भारत में स्ट्रॉन्ग ऑफलाइन प्रेजेंस और व्यापक ब्रांच नेटवर्क।

बेस्ट फॉर : जो ट्रेडर्स ऑफलाइन ब्रोकिंग सर्विस को प्राथमिकता देते हैं, उनके लिए एंजेल वन एक भरोसेमंद और बेहतर ऑप्शन है।

4. आईसीआईसीआई डायरेक्ट

आईसीआईसीआई डायरेक्ट भारत के टॉप स्टॉक ब्रोकर्स में से एक है, जो प्राइवेट सेक्टर की बड़ी बैंक, आईसीआईसीआई बैंक की सब्सिडियरी है। इसका सबसे बड़ा फायदा इसका थ्री-इन-वन अकाउंट है, जिसमें सेविंग्स अकाउंट, ट्रेडिंग अकाउंट और डिमैट अकाउंट को एक ही जगह लिंक किया जा सकता है। इससे फंड ट्रांसफर और ट्रेडिंग का प्रोसेस बहुत ही आसान हो जाता है, खासकर उन इन्वेस्टर्स के लिए जो सरलता पसंद करते हैं।

मुख्य फीचर्स:

देशभर में लोकल ऑफ़िस के ज़रिए मजबूत फिज़िकल प्रेजेंस।

क्लाइंट्स को रिसर्च और कंसल्टेंसी सर्विसेज उपलब्ध कराता है।

पर्सनलाइज़्ड वेल्थ मैनेजमेंट सॉल्यूशंस भी देता है, जिससे इन्वेस्टमेंट प्लानिंग आसान हो जाती है।

बेस्ट फॉर : जो इन्वेस्टर्स लोकल ब्रांच से सपोर्ट और हेल्प चाहते हैं, उनके लिए आईसीआईसीआई डायरेक्ट एक ट्रस्टेड और सुविधाजनक विकल्प साबित होता है।

5. कोटक सिक्योरिटीज

कोटक सिक्योरिटीज, कोटक महिंद्रा बैंक की एक डिवीजन है और भारत के टॉप प्राइवेट बैंकों में से एक मानी जाती है। यह यूज़र्स को उनके बैंक अकाउंट को सीधे ट्रेडिंग और डिमैट अकाउंट से लिंक करने की सुविधा देता है, जिससे फंड ट्रांसफर आसान हो जाता है। कोटक सिक्योरिटीज इक्विटी, कमोडिटी, डेरिवेटिव्स सहित कई इन्वेस्टमेंट ऑप्शंस प्रोवाइड करता है। इनके Neo Web प्लेटफ़ॉर्म और कोटक नियो मोबाइल ऐप रियल-टाइम मार्केट डेटा भी प्रदान करते हैं, जो ट्रेडर्स के लिए काफी उपयोगी है।

मुख्य फीचर्स:

इक्विटी और कमोडिटी ट्रेडिंग के साथ म्यूचुअल फंड इन्वेस्टमेंट की सुविधा।

ऑनलाइन एजुकेशनल इनिशिएटिव्स, जो स्टॉक मार्किट की समझ बढ़ाने में मदद करते हैं।

कोटक बैंक के ब्रांड सपोर्ट के कारण सिक्योरिटी और विश्वसनीयता का भरोसा।

बेस्ट फॉर : जो इन्वेस्टर्स स्टॉक मार्किट की नॉलेज ऑनलाइन ट्यूटोरियल्स से बढ़ाना चाहते हैं, उनके लिए कोटक सिक्योरिटीज एक बढ़िया ऑप्शन है।

अपस्टॉक्स एक न्यू-एज डिस्काउंट ब्रोकिंग प्लेटफॉर्म है जो ट्रेडिंग को तेज़, आसान और तकनीकी रूप से स्मार्ट बनाता है। यह यूज़र्स को एडवांस टेक्निकल एनालिसिस टूल्स, ऑप्शन चैन और स्ट्रैटेजी मोड जैसे फीचर्स के साथ अपने ट्रेडिंग डिसिज़न खुद प्लान करने की आज़ादी देता है। अपस्टॉक्स के ज़रिए आप इक्विटी, कमॉडिटी और डेरिवेटिव्स में इन्वेस्ट कर सकते हैं – वो भी मिनिमम कॉस्ट पर।

मुख्य फीचर्स:

सिंपल और यूज़र-फ्रेंडली मोबाइल ऐप जो बिगिनर्स के लिए भी एकदम परफेक्ट है।

मल्टीपल वॉचलिस्ट्स बनाने की सुविधा ताकि फेवरेट स्टॉक्स और कमॉडिटीज को ट्रैक कर सकें।

कोई एनुअल मेंटेनेंस चार्ज नहीं – यानी कम खर्च में ज्यादा फायदा।

बेस्ट फॉर : जिन ट्रेडर्स को इंट्राडे या स्विंग ट्रेडिंग करनी है और टेक्निकल एनालिसिस के टूल्स की ज़रूरत होती है, उनके लिए अपस्टॉक्स एक शानदार चॉइस है।

7. 5पैसा

5पैसा एक लोकप्रिय डिस्काउंट ब्रोकिंग प्लेटफॉर्म है जो 2016 में लॉन्च हुआ था और तब से अपने लो-कॉस्ट मॉडल और मल्टीपल इन्वेस्टमेंट ऑप्शन्स के ज़रिए यूज़र्स के बीच तेज़ी से पॉपुलर हुआ है। यह न केवल स्टॉक्स बल्कि म्यूचुअल फंड्स में भी डायरेक्ट इन्वेस्टमेंट की सुविधा देता है। इसके वेब और मोबाइल प्लेटफॉर्म को इस तरह डिज़ाइन किया गया है कि ट्रेडिंग हर यूज़र के लिए सिंपल और स्मूद लगे।

मुख्य फीचर्स:

आसान और यूज़र-फ्रेंडली इंटरफेस के साथ वेब और मोबाइल प्लेटफॉर्म।

डायरेक्ट म्यूचुअल फंड इन्वेस्टमेंट की सुविधा – वो भी बिना किसी एजेंट के।

F&O 360 प्लेटफॉर्म के ज़रिए एडवांस्ड एनालिसिस टूल्स की एक्सेस, जिससे डिसीज़न लेना हो जाए और भी बेहतर।

बेस्ट फॉर : जो इन्वेस्टर्स स्टॉक मार्किट की शुरुआत इंटरऐक्टिव लर्निंग और वर्कशॉप्स के ज़रिए करना चाहते हैं, उनके लिए 5पैसा एक समझदारी भरा ऑप्शन है।

8. शेयरखान

शेयरखान भारत की उन शुरुआती ब्रोकिंग कंपनियों में शामिल है जिसने 2000 में ऑनलाइन ट्रेडिंग को आम इन्वेस्टर्स तक पहुँचाया। देशभर में फैली अपनी फ्रैंचाइज़ी नेटवर्क की बदौलत इसने जल्दी ही एक मजबूत पहचान बना ली। 2016 में यह फ्रेंच इन्वेस्टमेंट बैंक BNP पारिबास का हिस्सा बना और फिर 2024 में मिराए एसेट फाइनेंशियल ग्रुप ने इसे अधिग्रहित कर लिया। शेयरखान सिर्फ ट्रेडिंग ही नहीं, बल्कि एडवांस लर्निंग के लिए भी जाना जाता है।

मुख्य फीचर्स:

मॉडर्न और स्मूद मोबाइल ऐप जिसमें एडवांस ट्रेडिंग टूल्स उपलब्ध हैं।

शेयरखान क्लासरूम’ के ज़रिए ऑनलाइन कोर्सेस और ट्रेनिंग प्रोग्राम्स।

प्रोफेशनल कस्टमर सपोर्ट जो यूज़र की हर परेशानी का तुरंत हल देता है।

बेस्ट फॉर : जिन्हें टेक्निकल या फंडामेंटल एनालिसिस सीखना है और ट्रेडिंग को गहराई से समझना है, उनके लिए शेयरखान एक बेहतरीन विकल्प है।

9. मोतिलाल ओसवाल

मोतिलाल ओसवाल की शुरुआत 1987 में हुई थी और तब से यह इंडियन ब्रोकिंग इंडस्ट्री में एक जाना-पहचाना नाम बन चुका है। 30+ सालों का अनुभव, दर्जनों अवॉर्ड्स और मजबूत रिसर्च बैकअप के साथ, यह कंपनी इन्वेस्टर्स को सिर्फ ट्रेडिंग ही नहीं बल्कि पर्सनलाइज्ड एडवाइजरी, पोर्टफोलियो मैनेजमेंट सर्विसेज और मल्टीपल एसेट क्लासेज में इन्वेस्टमेंट की सुविधा देती है। इनका RISE मोबाइल ऐप और वेबसाइट यूज़र्स को प्रो-लेवल रिसर्च रिपोर्ट्स और एडवांस एनालिसिस टूल्स तक एक्सेस देता है।

मुख्य फ़ीचर्स:

हर यूज़र की ज़रूरत के हिसाब से कस्टमाइज्ड फाइनेंशियल सॉल्यूशंस।

मोबाइल एप्लिकेशन यूज़र-फ्रेंडली इंटरफ़ेस के कारण इंडस्ट्री में सबसे बेहतरीन माना जाता है।

सिक्योरिटीज के अगेंस्ट लोन की सुविधा भी उपलब्ध है।

बेस्ट फॉर: ऐसे इन्वेस्टर्स जो एक ही प्लेटफॉर्म पर पोर्टफोलियो मैनेजमेंट से लेकर एडवांस रिसर्च और ट्रांजैक्शन फैसिलिटी तक सबकुछ चाहते हैं, उनके लिए मोतीलाल ओसवाल एक परफेक्ट चॉइस है।

10. एसबीआई सिक्योरिटीज

एसबीआई सिक्योरिटीज की स्थापना 2006 में हुई थी और यह भारत के सबसे बड़े पब्लिक सेक्टर बैंक, स्टेट बैंक ऑफ इंडिया (SBI) की फुली ओन्ड सब्सिडियरी है। पहले इसे SBICap Securities Limited के नाम से जाना जाता था। यह ब्रोकिंग फर्म अपने वाइड ब्रांच नेटवर्क और गवर्नमेंट-बैक्ड ट्रस्ट की वजह से इन्वेस्टर्स के बीच एक मजबूत और भरोसेमंद नाम बना हुआ है। एसबीआई सिक्योरिटीज आपको इक्विटी, कमॉडिटी ट्रेडिंग के साथ-साथ रिसर्च-बेस्ड एडवाइजरी और परसोनलाइज़्ड सर्विसेज भी ऑफर करता है।

मुख्य फ़ीचर्स:

हाई-नेट-वर्थ इन्वेस्टर्स के लिए डेडिकेटेड रिलेशनशिप मैनेजर्स की सुविधा।

मार्जिन ट्रेडिंग फैसिलिटी से इन्ट्राडे ट्रेडर्स को अतिरिक्त फंडिंग सपोर्ट मिलता है।

बेस्ट फॉर : जो इन्वेस्टर्स सरकारी बैंक से जुड़े प्लेटफॉर्म पर सिक्योर और वाइड-स्पेक्ट्रम ब्रोकिंग सर्विसेज चाहते हैं, उनके लिए एसबीआई सिक्योरिटीज एक विश्वसनीय ऑप्शन है। हाँ, इसका ब्रोकरेज चार्ज कुछ प्राइवेट ब्रोकर्स से ज्यादा हो सकता है, लेकिन सर्विस की क्वॉलिटी उस अंतर को कवर कर देती है।

11. एक्सिस डायरेक्ट

एक्सिस डायरेक्ट की शुरुआत 2011 में हुई थी और यह एक्सिस सिक्योरिटीज लिमिटेड का हिस्सा है, जो एक्सिस बैंक की सब्सिडियरी कंपनी है। इसने एडवांस टेक्नोलॉजी की मदद से एक पावरफुल ट्रेडिंग प्लेटफ़ॉर्म तैयार किया है जो इंडियन ब्रोकिंग इंडस्ट्री के टॉप प्लेटफ़ॉर्म्स में गिना जाता है। अगर आप एक्सिस बैंक के कस्टमर हैं, तो आप बड़ी आसानी से अपने बैंक अकाउंट को डिमैट और ट्रेडिंग अकाउंट से लिंक कर सकते हैं। मुंबई में इसका हेडक्वार्टर है और यह कंपनी अपने इन्वेस्टर्स को टेक्नोलॉजी, रिसर्च और सपोर्ट का बेहतरीन कॉम्बिनेशन देती है।

मुख्य फ़ीचर्स:

यूज़र्स को मिलता है एक एडवांस ट्रेडिंग और इन्वेस्टमेंट प्लेटफ़ॉर्म।

रेगुलर और डीप फंडामेंटल रिसर्च रिपोर्ट्स, जो स्टॉक्स, सेक्टर्स और कमॉडिटीज को कवर करती हैं।

मर्जिन फंडिंग फैसिलिटी से निवेशकों को मिलती है एक्स्ट्रा ट्रेडिंग पावर।

बेस्ट फॉर : जो निवेशक मर्जिन ट्रेडिंग फैसिलिटी का उपयोग करना चाहते हैं, उनके लिए यह एक अच्छा विकल्प है।

12. आईआईएफएल

आईआईएफएल (India Infoline) की शुरुआत 1985 में एक रिसर्च और एडवाइजरी फर्म के रूप में हुई थी। शुरुआत से ही इसका फोकस इन्वेस्टर्स को डीप रिसर्च और डेटा-बेस्ड इनसाइट्स देने पर रहा है। 2005 में कंपनी ने अपना नाम बदलकर IIFL किया और इंडियन स्टॉक एक्सचेंज में लिस्ट भी हुई। आज यह एक भरोसेमंद ब्रोकिंग हाउस है जो यूज़र्स को एडवांस ट्रेडिंग प्लेटफॉर्म, इन-डेप्थ रिसर्च रिपोर्ट्स और एजुकेशनल सेशंस जैसी सुविधाएं देता है, जिससे निवेशक बेहतर डिसीजन ले सकें।

मुख्य फ़ीचर्स:

इंडस्ट्री-लीडिंग रिसर्च और पर्सनलाइज़्ड एडवाइजरी सर्विसेज।

यूज़र-फ्रेंडली ट्रेडिंग प्लेटफॉर्म जो हर तरह के इन्वेस्टर्स के लिए उपयुक्त है।

फ्री एजुकेशनल सेशंस जो खासकर नए निवेशकों के लिए काफ़ी मददगार हैं।

बेस्ट फॉर : वो इन्वेस्टर्स जो रिसर्च और एक्सपर्ट एडवाइस के बेस पर स्मार्ट ट्रेडिंग करना चाहते हैं, उनके लिए आईआईएफएल एक शानदार चॉइस है।

13. एडेलवाइस

एडेलवाइस ग्रुप ने 2008 में ब्रोकिंग इंडस्ट्री में एंट्री ली और तब से यह निवेशकों को मल्टी-लेवल फाइनेंशियल सर्विसेज़ ऑफर कर रहा है। शुरुआत में कंपनी ने रिसर्च और एडवाइजरी पर ज़ोर दिया और फिर 2015 से म्युचुअल फंड्स, PMS (पोर्टफोलियो मैनेजमेंट सर्विसेज़), और एल्गो ट्रेडिंग जैसी सुविधाएं भी जोड़ लीं। इसका प्लेटफॉर्म खासकर उन निवेशकों के लिए डिज़ाइन किया गया है जो एक ही जगह पर टेक्नोलॉजी, रिसर्च और एडवाइस का पूरा पैकेज चाहते हैं।

मुख्य फ़ीचर्स :

एल्गोरिदमिक ट्रेडिंग की सुविधा जिससे ऑटोमेटेड डिसीजन लिए जा सकते हैं।

एक्टिवली मैनेज्ड फंड्स के सुझाव जो मार्केट कंडीशन्स के अनुसार बदलते रहते हैं।

डेली मार्केट अपडेट्स और रिसर्च एनालिसिस जो निवेशकों को अप-टू-डेट रखते हैं।

बेस्ट फॉर: ऐसे इन्वेस्टर्स जो एक ही प्लेटफॉर्म पर ट्रेडिंग, रिसर्च, और फाइनेंशियल एडवाइजरी जैसी सर्विसेज़ चाहते हैं, उनके लिए एडेलवाइस एक भरोसेमंद और प्रैक्टिकल विकल्प है।

14. ग्रो (Groww)

ग्रो (Groww) की शुरुआत 2016 में चार एक्स-फ्लिपकार्ट कर्मचारियों ने की थी, और कुछ ही सालों में यह युवाओं और नए इन्वेस्टर्स के बीच सुपर पॉपुलर हो गया। इसकी सबसे बड़ी खासियत है बेहद सिंपल और क्लीन यूज़र इंटरफेस, जिससे कोई भी बिना ज़्यादा टेक्निकल नॉलेज के भी आसानी से इन्वेस्ट करना शुरू कर सकता है। इस ऐप के ज़रिए यूज़र्स स्टॉक्स, म्युचुअल फंड्स, ETF जैसी कई इन्वेस्टमेंट ऑप्शन्स का फायदा उठा सकते हैं, वो भी मिनिमल चार्जेस के साथ।

मुख्य फ़ीचर्स :

स्टॉक्स, म्युचुअल फंड्स और ETF में आसान इन्वेस्टमेंट की सुविधा।

क्रेडिट, बिल पेमेंट और UPI जैसी बेसिक फाइनेंशियल सर्विसेज़ भी मौजूद।

न्यूनतम फीस स्ट्रक्चर – लॉन्ग टर्म इन्वेस्टर्स के लिए किफायती।

बेस्ट फॉर : जो निवेशक चाहते हैं कि उनका पूरा इन्वेस्टमेंट पोर्टफोलियो एक ही सिंपल ऐप में मैनेज हो सके, उनके लिए ग्रो (Groww) एक शानदार चॉइस है।

15. पेटीएम मनी

पेटीएम मनी की शुरुआत 2017 में डायरेक्ट म्युचुअल फंड इन्वेस्टमेंट प्लेटफ़ॉर्म के रूप में हुई थी, जिसे Paytm की पैरेंट कंपनी One97 Communications ने लॉन्च किया था। शुरुआती दौर में इसका मकसद था – हर किसी को म्युचुअल फंड्स में कम लागत पर इन्वेस्ट करने का मौका देना। फिर 2019 में कंपनी ने कम ब्रोकरेज के साथ स्टॉक ट्रेडिंग सर्विस भी शुरू की। आज यह ऐप एक सिंपल, किफायती और ऑल-इन-वन इन्वेस्टमेंट प्लेटफॉर्म बन चुका है।

मुख्य फ़ीचर्स:

यूज़र-फ्रेंडली ऐप जो नए यूज़र्स के लिए भी पूरी तरह सहज।

डायरेक्ट म्युचुअल फंड इन्वेस्टमेंट जिससे एक्स्ट्रा कमीशन नहीं देना पड़ता।

SIP और लंपसम इन्वेस्टमेंट के लिए स्मार्ट कैलकुलेटर्स की सुविधा।

बेस्ट फॉर : जो लोग म्युचुअल फंड्स और स्टॉक्स में कम खर्च में इन्वेस्ट करना चाहते हैं और एक सिंपल ऐप से सब कुछ मैनेज करना पसंद करते हैं, उनके लिए Paytm Money एक बढ़िया विकल्प है।

ट्रेडर्स के लिए 3 सर्वश्रेष्ठ ब्रोकर नीचे दिए गए हैं:

1. ज़ेरोधा : ज़ेरोधा भारत का सबसे बड़ा डिस्काउंट ब्रोकिंग प्लेटफॉर्म है, जो अपनी किफायती ब्रोकरेज फीस और भरोसेमंद सर्विस के लिए जाना जाता है। लाखों ट्रेडर्स इसे अपनी पहली पसंद मानते हैं। यहां आपको ट्रेडिंग के लिए कई एडवांस टूल्स मिलते हैं, जैसे Sensibull जो ऑप्शन ट्रेडिंग को आसान बनाता है, Streak जो आल्गोरिदमिक ट्रेडिंग की सुविधा देता है, और KITE जो एक पावरफुल वेब और मोबाइल ऐप है। साथ ही, इसकी एजुकेशनल साइट Varsity नए ट्रेडर्स के लिए सीखने का बेहतरीन माध्यम है।

2. पॉकेटफुल (Pocketful) : पॉकेटफुल एक नया लेकिन तेजी से लोकप्रिय हो रहा फिनटेक प्लेटफॉर्म है, जो बिना किसी इक्विटी डिलीवरी फीस के ट्रेडिंग का मौका देता है। इसे पेस फाइनेंशियल ग्रुप ने बनाया है, जिनका 30 से ज्यादा सालों का अनुभव इस प्लेटफॉर्म की विश्वसनीयता को बढ़ाता है। पॉकेटफुल का यूज़र-फ्रेंडली इंटरफेस और विविध निवेश विकल्प इसे नए और अनुभवी दोनों तरह के इन्वेस्टर्स के लिए आकर्षक बनाते हैं।

3. अपस्टॉक्स : अपस्टॉक्स भी किफायती ब्रोकरेज के साथ ट्रेडर्स को एक स्मूद और तेज़ ट्रेडिंग एक्सपीरियंस देता है। इसमें एडवांस चार्टिंग टूल्स के साथ Tick-by-Tick Engine नामक फीचर है, जो आपको लाइव मार्केट डेटा और ऑर्डर बुक की गहराई दिखाता है। यह सुविधा पहले सिर्फ बड़े संस्थागत निवेशकों के लिए थी, लेकिन अब हर रिटेल ट्रेडर इसका फायदा उठा सकता है।

इन्वेस्टर्स के लिए सबसे बढ़िया 3 विकल्प

इन्वेस्टर्स के लिए 3 सर्वश्रेष्ठ ब्रोकर नीचे दिए गए हैं:

1.पॉकेटफुल : अगर लॉन्ग-टर्म इन्वेस्टमेंट करना है तो पॉकेटफुल एकदम सही चॉइस है। ये मॉडर्न फिनटेक प्लेटफॉर्म है जिसमें ना कोई अकाउंट ओपनिंग फीस है, ना AMC (एनुअल मेंटेनेंस चार्ज) और ना ही डिलिवरी फीस। पॉकेटफुल की टेक्नोलॉजी बहुत एडवांस्ड है, जिसे 27+ साल के एक्सपीरियंस वाले एक्सपर्ट्स ने डेवलप किया है। यहाँ से आसानी से मल्टिपल एसेट क्लासेज़ में इन्वेस्टमेंट कर सकते हैं, जिससे यूजर एक्सपीरियंस स्मूद और बेहतर होता है।

2. मोतीलाल ओसवाल : मोतिलाल ओसवाल भारत के सबसे भरोसेमंद और अनुभवी ब्रोकर्स में से एक है। यहाँ आपको सिर्फ ट्रेडिंग ही नहीं, बल्कि पोर्टफोलियो मैनेजमेंट, एडवाइजरी सर्विसेज और गहरी रिसर्च रिपोर्ट्स भी मिलती हैं। इनकी सर्विस खासकर उन इन्वेस्टर्स के लिए सही है जो लंबी अवधि के लिए स्मार्ट और सूझ-बूझ से निवेश करना चाहते हैं। इनके मोबाइल ऐप और वेबसाइट दोनों पर यूज़र-फ्रेंडली इंटरफेस मिलता है, जिससे निवेश करना बेहद आसान हो जाता है।

3. आईआईएफएल (India Infoline Finance Limited) : आईआईएफएल उन इन्वेस्टर्स के लिए एक बढ़िया विकल्प है जो रिसर्च और एडवाइजरी को बहुत महत्व देते हैं। कंपनी उन्नत ट्रेडिंग प्लेटफॉर्म के साथ-साथ नियमित मार्केट अपडेट्स और मुफ्त एजुकेशनल सेशंस भी प्रदान करती है। ये खासकर उन लोगों के लिए परफेक्ट है जो मार्केट को समझकर, सूचनाओं के आधार पर अपने निवेश फैसले लेना चाहते हैं।

डीमैट अकाउंट के फायदे

डीमैट अकाउंट के फायदे नीचे दिए गए हैं:

तेजी से ट्रांजैक्शन: ट्रेडिंग के दौरान शेयरों की खरीद-फरोख्त तुरंत होती है, जिससे आप मार्केट के मौकों का लाभ बेहतर तरीके से उठा सकते हैं।

आसान निगरानी: सभी निवेश एक ही डिजिटल प्लेटफॉर्म पर नजर आते हैं, जिससे अपनी पोर्टफोलियो को मैनेज करना सरल होता है।

कम धोखाधड़ी का खतरा: इलेक्ट्रॉनिक रिकॉर्ड होने की वजह से स्टॉक्स चोरी या गुम होने की संभावना लगभग न के बराबर हो जाती है।

खर्चों में बचत: पेपर वर्क न होने के कारण लेन-देन से जुड़ी कई अतिरिक्त फीस बच जाती है।

डीमैट अकाउंट के बिना स्टॉक मार्केट में निवेश करना आज के जमाने में न केवल मुश्किल है, बल्कि जोखिम भी बढ़ जाता है। इसलिए एक भरोसेमंद और सुविधाजनक डीमैट अकाउंट निवेश की शुरुआत करने वालों के लिए सबसे जरूरी टूल है।

अपनी जरूरत के हिसाब से सबसे अच्छा डीमैट अकाउंट कैसे चुनें?

जब डीमैट अकाउंट खोलने की बात आती है, तो हर किसी की जरूरतें अलग होती हैं। इसलिए सही अकाउंट चुनना बहुत जरूरी होता है ताकि आपका निवेश सफर आसान और फायदेमंद रहे।

नीचे कुछ अहम बातों का ध्यान रखें जो आपकी पसंद को सही दिशा देंगे:

फीस और चार्जेस: अकाउंट खोलने और मेंटेन करने की फीस अलग-अलग ब्रोकर्स पर अलग हो सकती है। अपने बजट के हिसाब से ऐसा विकल्प चुनें जो ज्यादा महंगा न हो लेकिन अच्छी सेवा दे।

ट्रेडिंग और इन्वेस्टिंग की सुविधाएं: कुछ डीमैट अकाउंट सिर्फ ट्रेडिंग के लिए बेहतर होते हैं, तो कुछ में म्यूचुअल फंड्स और अन्य निवेश विकल्प भी शामिल होते हैं। अपने निवेश के प्रकार के अनुसार अकाउंट चुनें।

ग्राहक सेवा: जब भी आपको कोई सवाल या समस्या हो, तो ग्राहक सेवा की मदद जल्दी और असरदार मिलनी चाहिए। भरोसेमंद ब्रोकर्स का चुनाव करें जो समय पर सहायता देते हों।

ट्रेडिंग प्लेटफ़ॉर्म की आसानी: तकनीकी ज्ञान के बिना भी आपको अपनी निवेश गतिविधियां सहजता से करनी चाहिए। इसलिए ऐसा प्लेटफ़ॉर्म चुनें जो सरल और समझने में आसान हो।

रिसर्च और एडवाइजरी: अगर आप मार्केट की जानकारी लेकर ही निवेश करना पसंद करते हैं, तो ऐसे ब्रोकर्स चुनें जो अच्छे रिसर्च और सलाह देते हों।

इन बातों को ध्यान में रखकर आप अपनी ज़रूरतों और निवेश के तरीके के अनुसार सही डीमैट अकाउंट चुन सकते हैं, जो आपके लिए लंबी अवधि में फायदे का सौदा साबित होगा।

निष्कर्ष

इस ब्लॉग में हमने भारत के प्रमुख डीमैट अकाउंट्स और उनके खास फीचर्स पर विस्तार से चर्चा की है। सही डीमैट अकाउंट चुनना आपके निवेश सफर की सफलता के लिए बेहद जरूरी है। हर निवेशक की जरूरत और प्राथमिकताएं अलग होती हैं, इसलिए आपको अपने निवेश के तरीके, फीस स्ट्रक्चर, और उपलब्ध सेवाओं को ध्यान में रखकर निर्णय लेना चाहिए। टेक्नोलॉजी, ग्राहक सेवा, और रिसर्च सपोर्ट भी अकाउंट चुनते समय अहम रोल निभाते हैं। उम्मीद है यह जानकारी आपको समझदारी से अपने लिए सबसे उपयुक्त डीमैट अकाउंट चुनने में मदद करेगी और आपके निवेश को बेहतर बनाएगी।

डीमैट अकाउंट क्या होता है?

डीमैट अकाउंट एक डिजिटल अकाउंट होता है जिसमें आपके शेयर और सिक्योरिटीज इलेक्ट्रॉनिकली स्टोर होते हैं।

डीमैट अकाउंट खोलने के लिए क्या डॉक्युमेंट्स लगते हैं?

पैन कार्ड, आधार कार्ड, बैंक स्टेटमेंट और एक पासपोर्ट साइज फोटो की ज़रूरत होती है।

क्या डीमैट अकाउंट खोलना फ्री होता है?

कई ब्रोकर्स फ्री अकाउंट ओपनिंग ऑफर करते हैं, लेकिन कुछ में एएमसी (अकाउंट मेंटेनेंस चार्जेस) लग सकते हैं।

क्या एक व्यक्ति के पास मल्टीपल डीमैट अकाउंट्स हो सकते हैं?

हाँ, एक व्यक्ति अलग-अलग ब्रोकर्स के साथ मल्टीपल डीमैट अकाउंट्स रख सकता है।

बिगिनर्स के लिए बेस्ट डीमैट अकाउंट कौन सा है?

बिगिनर्स के लिए पॉकेटफुल, अपस्टॉक्स और ज़ेरोधा जैसे ईज़ी-टू-यूज़ प्लेटफॉर्म्स बेस्ट माने जाते हैं।

In today’s digital age, participation in the stock market has become extremely important for companies looking to increase their overall profitability. However, for a company to begin investing, a corporate demat account is a must.

Corporate demat account refers to an account in the name of the company where shares and securities are kept in electronic form. At the same time, companies can buy and sell shares through a corporate trading account.

In this blog, we will understand in detail what is a corporate demat account, what are its benefits, who can open it, what are the necessary documents and what is the process of opening it.

What is a Corporate Demat Account?

A Demat Account, or “dematerialized account”, is an account where your shares and other securities are kept in electronic form. Just like a Demat account is opened in the name of an individual, when a company opens an account to keep its investments and shares in digital form, it is called a corporate Demat account.

This account is specifically for registered companies such as Private Limited (Pvt. Ltd.) Companies, Public Limited Companies, LLPs (Limited Liability Partnerships), Trusts, etc.

The major difference between an individual Demat account and a company Demat account is that a company account can have multiple authorized signatories and it is opened in the name of the company, not in the name of any individual.

The main purpose of this account is to keep all the shares, bonds, mutual fund units and other securities of the company safely and systematically on a single digital platform.

Differences Between Individual Demat Account and Corporate Demat Account

Particulars

Individual Demat Account

Corporate (Company) Demat Account

Account Holder

An individual person

A registered company or institution

Purpose

For personal investments

For company investments, ESOPs, IPO participation, etc.

Authorized Signatory

Single person (account holder)

One or more authorized signatories as per board resolution

Document Requirements

Basic KYC documents

Statutory company documents + KYC + Board Resolution

Control & Management

Managed by the individual

Managed by company representatives

Nomination Facility

Available

Limited or controlled via board decision

Processing Time

Fast and simple process

Detailed verification, may take more time

Features of a Corporate Demat Account

A corporate demat account is a digital account for companies to store their shares, debentures, mutual funds, and other securities in electronic form. This account is designed not just to store investments but also to manage them smartly.

Digital Holding: All securities in this account are held in electronic form, eliminating the need for paperwork and physical storage.

Multiple Authorized Signatories: Companies can nominate multiple authorized signatories through their board resolutions who can operate this account.

Nomination and Power of Attorney: A nominee or power of attorney holder can also be appointed if required, making account operations more flexible.

Link to Corporate Trading Account: This account is directly linked to the corporate trading account, allowing companies to buy and sell shares easily.

Accessible Platforms: The account can be easily accessed from the Depository Participant (DP) website or mobile apps.