In case you have some extra money and want to invest for the short term with an objective to maintain liquidity and get some return. There are various options available in the debt category of mutual funds. Among them, the most preferred investment options to park idle money are overnight and liquid funds.

In today’s blog post, we will give you an overview of overnight funds and liquid funds, along with their key differences.

What are Overnight Funds?

Overnight funds are a category of debt mutual funds that primarily invest money in fixed-income instruments with a maturity of just one day. As investments are made in very short-term debt instruments, the investor considers them the safest option to park their money.

Features of Overnight Funds

The key features of overnight funds are as follows:

One-Day Maturity: The overnight fund invests its money in securities that mature within one day.

Low Return: The returns are low because the maturity of the instrument is extremely short i.e. 1 day only and the amount gets reinvested daily.

Low Interest Rate Risk: The interest rate risk in the overnight fund is very low, as the funds are least affected by changes in interest rates.

Very Low Credit Risk: Overnight funds generally invest in high-quality debt instruments, reducing the risk of default.

What are Liquid Funds?

A liquid fund is a debt mutual fund offered by an asset management company which invests the money collected from the investor in fixed-income securities having a maturity of up to 91 days. The objective of these funds is to provide liquidity along with returns. It invests the money in instruments such as commercial papers, treasury bills, certificates of deposits, etc. A liquid fund offers a slightly better return than a savings account.

Features of Liquid Fund

The key features of a liquid fund are as follows:

Liquidity: Investment in a liquid fund is highly liquid. One can easily redeem their money, and the amount is credited to their bank account within one working day.

Better Returns: Liquid funds often yield higher returns than savings accounts. This makes it attractive for investors who keep their money idle in their bank accounts.

No Lock-in: Liquid funds do not come with any lock-in period. It allows investors to withdraw their money at any time.

Professional Management: Investments in liquid funds are managed by the asset management companies’ professional, experienced fund managers.

The key difference between overnight and liquid funds is as follows:

Particulars

Overnight Funds

Liquid Funds

Duration of Investment

The overnight funds invest in securities having a maturity of 1 day.

A liquid fund invests the money in debt securities having a maturity of up to 91 days.

Risk

These funds have the lowest risk among all other debt mutual funds.

A liquid fund also carries lower risk, but has higher risk than overnight mutual funds.

Volatility due to Interest Rates

There are no or low risks related to changes in interest rates on overnight funds.

Liquid funds generally have slightly higher interest rate risk than overnight funds due to longer maturity.

Returns

Overnight funds have the lowest returns.

Liquid funds post higher returns than overnight funds.

Default Risk

These funds have almost zero default risk.

As the securities have a slightly higher maturity, they carry a higher default risk.

Ideal Investment Duration

The investment in overnight funds is suitable for 1 to 7 days.

Investment in a liquid fund is suggested for 3 to 6 months.

Suitability

Investment in overnight funds is suitable for big institutions.

Liquid funds are suitable for retail or individual investors to park their money.

Expense Ratio

Overnight funds have a lower expense ratio.

Liquid funds have a slightly higher expense ratio than overnight funds.

Portfolio Turnover Ratio

Overnight funds have a higher portfolio turnover ratio as the money is reinvested every day.

Liquid funds have a moderate portfolio turnover ratio as the securities in the portfolio are held for a few periods.

Where should you invest your money: Overnight or Liquid Fund

The decision of whether to invest in the Overnight Funds or Liquid Funds largely depends on how long you want to invest and your preference for risk. When you want to invest for a very short time, say a few days, and you want to have maximum safety with almost no interest rate risk, then overnight funds may be an appropriate choice since they invest in securities that mature after only a single day. Alternatively, when you are looking at a period of a few weeks or up to a few months and aiming at relatively higher returns, and the risk is also not that high, liquid funds can be a better option. Overnight funds are mostly suitable for overnight parking of money, in simple terms, whereas liquid funds are best for short-term investments and emergency funds.

On a concluding note, both overnight funds and liquid funds are suitable options for investors who want to park their money for the short term with an objective to earn a return with liquidity. These two funds are low risk and offer high liquidity, which typically means you can easily withdraw your money as needed. Overnight funds invest in securities that have a maturity of just one day, while liquid funds invest money in securities that have a maturity of up to 91 days. However, choosing among them depends on the investor’s risk profile and investment horizon; therefore, it is advisable to consult your investment advisor before making any investment decision.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Both liquid funds and overnight funds are safer investment options. But overnight funds are slightly safer than liquid funds as they invest in fixed income securities that have a maturity of one day.

Which offers higher returns among overnight funds and liquid funds?

Liquid funds offer slightly higher returns than overnight funds, because liquid funds invest in fixed income securities with longer maturity and higher coupons.

Do liquid funds have any lock-in period?

No, liquid funds do not have any lock-in period, but some liquid funds have an exit load.

Do overnight funds and liquid funds offer guaranteed returns?

No, neither overnight nor liquid funds offer guaranteed returns. As the returns of these funds are market-linked.

Can I start SIP in overnight and liquid funds?

Yes, you can easily start a SIP in overnight and liquid mutual funds.

There is a type of debt fund that invests your money in short-term instruments like treasury bills, commercial papers, and certificates of deposit. These securities usually mature within 91 days, making the interest rate risk low and helping the fund maintain a stable NAV (Net Asset Value). Because of this short maturity, liquid funds are designed to give you quick access to your money with limited volatility.

SEBI rules limit these investments to a maximum maturity of 91 days and also keep a check on expense ratios, which tend to be quite low for liquid funds. Exit loads are either zero or very small for a few initial days, so most of your capital stays intact even if you need the money on short notice. The main objective remains to protect your capital while earning comparatively better returns than a savings account.

In these funds the investment is done in high credit quality funds or generally funds that have AAA and A1+ rated securities to keep default risk low. In simpler terms, liquid mutual funds act like a smarter version of a savings account. Your Investment stays relatively safe, which can be accessed quickly while making you a decent amount of money in return.

Top 10 Liquid Mutual Funds in India 2026

Fund Name

AUM (Rs.Cr.)

Expense Ratio

Min. Investment (Rs.)

Axis Liquid Direct Growth

48,415

0.11%

100

HDFC Liquid Direct Growth

72,501

0.2%

100

Aditya Birla SL Liquid Direct

60,285

0.21%

100

Union Liquid Direct Growth

8,025

0.07%

5,000

Quant Liquid Direct Growth

1,327

0.22%

5,000

ICICI Prudential Liquid Direct Growth

60,474

0.2%

99

Nippon India Liquid Direct

33,500

0.2%

1,000

Kotak Liquid Direct Growth

43,974

0.2%

1,000

SBI Liquid Direct Growth

66,511

0.19%

500

UTI Liquid Direct Growth

31,333

0.15%

500

(Data as of 11 March 2026)

Overview of Top 10 Liquid Mutual Funds in India 2026

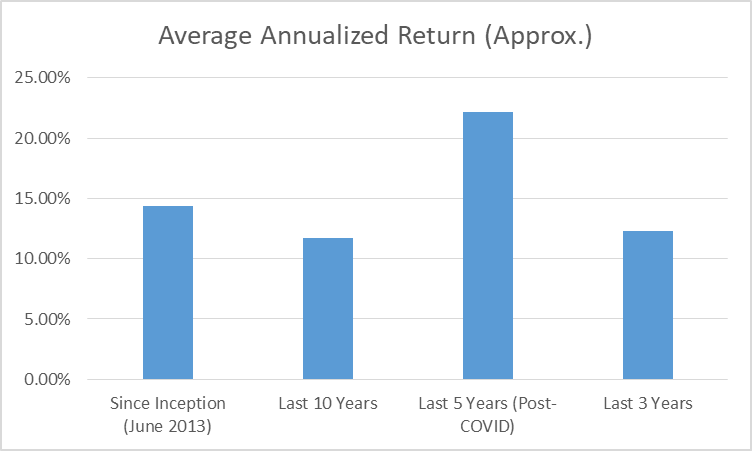

1. Axis Liquid Direct Growth

It is a very large and popular scheme where investment is mainly done in AAA-rated T-bills, CDs, and CPs, with an average maturity of around 45 days. Low expenses and a strong track record make it a common choice for emergency funds and short-term parking.

1 Year return

3 Year return

5 Year return

6.44%

7.05%

6.01%

(Data as of 11 March 2026)

2. HDFC Liquid Direct Growth

This is one of the largest liquid funds by AUM, with most of its portfolio in high-quality bank certificates of deposit and treasury bills. Its scale and cautious investment style make it attractive for investors who prioritise stability and strong liquidity.

1 Year return

3 Year return

5 Year return

6.39%

6.99%

5.95%

(Data as of 11 March 2026)

3. Aditya Birla Sun Life Liquid Direct

This fund gives investors a mix of T-bills, CDs, and CPs, with solid and sizable returns. The fund has shown steady performance over three and five years, often slightly outpacing the category average.

1 Year return

3 Year return

5 Year return

6.44%

7.07%

6.03%

(Data as of 11 March 2026)

4. Union Liquid Direct Growth

This is a mid-sized fund with funds allocated in PSU and government-backed papers, giving investors a comfort factor on credit quality. It works well for medium-ticket surplus amounts.

1 Year return

3 Year return

5 Year return

6.40%

7.04%

6.01%

(Data as of 11 March 2026)

5. Quant Liquid Direct Growth

This is a smaller but an active fund where there is a limited exposure to higher-yielding corporate CPs. In this fund returns are competitive, but it may suit investors who are comfortable with the active actions.

1 Year return

3 Year return

5 Year return

6.28%

6.92%

6.09%

(Data as of 11 March 2026)

6. ICICI Prudential Liquid Direct Growth

This is one of the largest and most established liquid funds that allows instant redemption up to a certain amount. The fund emphasises more on T-bills to prevent higher risk, making it beneficial for managing short-term cash needs.

1 Year return

3 Year return

5 Year return

6.36%

7.00%

5.96%

(Data as of 11 March 2026)

7. Nippon India Liquid Direct

If you are an investor that is looking for credit research and high-rated securities then this is the most suitable fund for you, as this fund results in a comparable stable portfolio. It’s preferred for new liquid investors who prefer a well-known brand.

1 Year return

3 Year return

5 Year return

6.41%

7.03%

6.00%

(Data as of 11 March 2026)

8. Kotak Liquid Direct Growth

This fund holds a significant portion in bank CDs and other top-rated securities, aiming to balance safety with slightly better yields. It has managed past periods of market stress without major issues.

1 Year return

3 Year return

5 Year return

6.38%

7.00%

5.97%

(Data as of 11 March 2026)

9. SBI Liquid Direct Growth

Backed by a PSU sponsor, this fund invests heavily in government securities and high-quality corporate debt. It also offers SIP, SWP, and STP options, which help investors who want to gradually shift money into other schemes.

1 Year return

3 Year return

5 Year return

6.31%

6.96%

5.94%

(Data as of 11 March 2026)

10. UTI Liquid Direct Growth

This is a veteran liquid fund where investments are done sensibly, as this fund emphasizes liquidity buffers like overnight repos. Here the focus is on steady, low-volatility returns instead of aggressively chasing higher yields.

Liquid funds do not invest in infrastructure companies or equities; they build a diversified basket of short-term debt instruments published by governments, banks, and large companies. The main instruments are:

Treasury Bills (T-Bills): Short-term government securities that mature within 91 days. They carry almost zero default risk and offer investors a yield around 6.3 – 6.5%.

Commercial Papers (CPs): Companies issue short-term debt with strong balance sheets. These usually offer slightly higher returns than T-bills and are often rated A1+ for safety.

Certificates of Deposit (CDs): The banks and a few other financial institutions issue the time deposits. Maturities range from a few weeks to 90 days and are backed by the strength of the banking system.

Repo and Reverse Repo: Overnight lending and borrowing arrangements with other institutions. These instruments add day-to-day liquidity to the portfolio and help meet redemption requests smoothly.

Generally, the best liquid mutual funds put 80% to 85% of their portfolio investments in financial sector debt like government securities, bank CDs, and high-quality corporate CPs. The remaining part usually goes into other AAA-rated instruments and overnight repos. This blend aims to deliver a balance of safety, liquidity, and reasonable yield.

Advantages of Investing in Liquid Funds

High Liquidity: Investors can instantly withdraw their savings up to a limited amount and the process generally takes T+1 day.

Better Returns: These funds give returns ranging from 6%-7% which is higher as compared to 3%-4% in savings accounts.

Low Volatility: Investments in short-term maturities with high-rated instruments result in minimal daily NAV fluctuations.

Useful for Emergency Funds: As investors can withdraw their savings instantly, these funds become very accessible.

Disadvantages of Investing in Liquid Funds

Lower Returns: These funds give lower returns as compared to equities and they are not designed for long-term wealth creation.

Credit and Interest Rate Risk: Although these are small, the risk associated is not exactly zero especially if a fund takes exposure to weaker issuers.

Taxed as Debt: As per the new rules the profit gained from these funds are taxed as per general income slab.

These types of funds are a perfect mix of savings accounts and longer term debt options. These are best suitable for investors if they are looking for:

Putting extra cash for a few weeks or months.

Building an emergency fund without locking your savings.

Keeping funds ready for future opportunities

In savings accounts people get a return of 3-4% but in top liquid schemes a return of 6.5% – 7% can be achieved, especially on large amounts. Unlike fixed deposits, you can take out the amount saved without any penalty and investors get daily returns instead of quarterly or annually.

This possesses a substantial portion in bank CDs and other top-rated securities. The goal is to balance safety with yields. It successfully navigated past market stress without major issues

Why Liquid Funds Matter in 2026

Repo rate in India is around 6.5%, which means short-term debt instruments are also offering considerable returns in 2026. As a result, many of the best liquid funds are delivering about 6.5 – 7% annual returns, while most savings accounts are still in the 3 – 4% range. That difference becomes meaningful if you’re putting your money aside for a few months or more.

Inflation is close to 5%, so leaving money in a low-yield savings account can slowly reduce your purchasing power. Liquid mutual funds help you keep pace with inflation better, without forcing you into high-risk assets like equities. There is no lock-in, and most funds allow redemption in T+1 working days; some even offer an “instant redemption” facility for a small limit.

As an investor, this makes liquid funds a practical tool for emergency funds, parking bonuses, or keeping money aside for short-term goals. You have the option to track these funds in real time, compare returns and risks, and move between schemes easily using platforms like the Pocketful app, which also offers zero brokerage on delivery trades and a simple interface for both beginners and experienced investors.

How to Choose the Best Liquid Fund in 2026

Investors shall look for the following thighs before selecting a liquid fund:

Past Performance: Look at the fund’s past performance by judging its last 5 year returns cycle.

AUM Size and Brand: Look for large and reputable fund houses in the market as they are reliable to invest your savings.

Portfolio Quality: High share of T-bills, top-rated CDs, and CPs should be your preference, and those with too much in a single issuer should be avoided.

Expense Ratio: Lower expense ratios of around 0.07% – 0.10% will give you more gross yield. So one shall prefer funds with low expense ratio.

Investors can easily compare all these factors on the Pocketful platform, where they can check out returns, AUM, expenses, and basic portfolio details side by side and then invest.

Liquid Mutual Funds act as a smart and reliable substitute for cash. The best mutual liquid funds like Axis, HDFC and Aditya Birla can give returns up to 6.5%-7% along with outstanding liquidity. These funds considerably exceed the performance of conventional savings accounts. Reflect on your investment duration and risk appetite.

These funds are best suitable for those looking to save for emergency savings, short-term investments or business operating capital. However these funds are not created for long term wealth creation but gives you purchasing power confidence as you have cash that is easily accessible.

For additional market updates and insights, download Pocketful, which offers users zero brokerage on delivery trades and an easy-to-use platform designed for both beginners and experienced investors.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

These are direct mutual funds where your savings are put in short-term financial instruments like T-bills, CDs, and CPs. Here the maturity is up to 91 days and these funds focus on giving high liquidity with minimal risk attached to it.

Best Liquid fund for beginners?

Axis Liquid Direct Growth and HDFC Liquid Direct Growth are a prominent market choice as they have large AUM, low expenses, and consistent performance.

Can I redeem my investment anytime?

Yes, usually there is no lock-in for liquid mutual funds and most funds allow T+1 redemptions and offer instant redemption with a limited amount per day.

Are liquid funds safer than other debt funds?

They generally carry lower interest rates and credit risk than longer-duration debt funds. This is because they hold very short-term, high-rated papers.

Are liquid funds better compared to savings accounts?

Liquid funds can be a more advantageous option as compared to savings accounts as they give higher returns.

Terms like “25 BPS increase” or “50 BPS cut” often appear in finance and banking news. While these terms may seem a bit technical to many, their meaning is quite simple to understand. Basis Point (BPS) is a standard way to express small changes in interest rates or percentages. Banks, investors, and central banks use this unit. In this article, we will explain the full form of BPS, its meaning, and its use in banking in simple language.

BPS Full Form

The full form of BPS is “Basis Point.” In finance and banking, it is a unit of measurement used to clearly express small percentage changes. When interest rates, bond yields, or investment returns increase or decrease slightly, they are expressed in Basis Points (BPS) rather than directly as percentages to more accurately describe the change.

Definition BPS

In finance, 1 Basis Point (BPS) equals 0.01%.

Similarly, 100 Basis Points = 1%.

This means that BPS is a standard way of measuring small percentage changes, which banks, investors and financial institutions use regularly.

BPS Formula

Percentage = BPS ÷ 100

How to Calculate BPS (Basis Point)

Formula : BPS = (New Rate – Old Rate) × 100

That is, the difference in percentage is multiplied by 100 to get the Basis Points.

Step-by-Step BPS Calculation

Step

Calculation Process

Example

Step 1

Identify the old interest rate and the new interest rate.

Old Rate = 7.50%

Step 2

Note the new rate

New Rate = 7.75%

Step 3

Find the difference between the two rates

7.75% − 7.50% = 0.25%

Step 4

Multiply this difference by 100.

0.25 × 100 = 25

Final Result

These are Basis Points.

Interest rate increase = 25 BPS

In this example, the bank’s interest rate increased from 7.50% to 7.75%, a total change of 0.25%. In financial terms, this is known as 25 Basis Points (25 BPS).

Percentage and BPS Conversion Table

Percentage Change

Basis Points

0.01%

1 BPS

0.10%

10 BPS

0.25%

25 BPS

0.50%

50 BPS

1%

100 BPS

What is BPS in Finance?

In the world of finance, the Basis Point (BPS) is used to measure small percentage changes. This is particularly useful in cases where rate changes are very small and require accurate representation.

BPS is commonly used in the following areas:

Changes in Interest Rates

Bond Yields

Mutual Fund Expense Ratios

Loan Interest Rates

Investment Returns

Even a change of 10–25 bps is considered significant in the financial market because it can have a significant impact. For example, loan costs, bond market yields, and corporate borrowing costs can be affected by these small changes.

For this reason, central banks often adjust their monetary policy by 25 bps or 50 bps in increments to balance economic activity and liquidity.

Why Financial Institutions Use Basis Points Instead of Percentages

To clearly display small changes : In finance and banking, interest rates often experience very small changes, such as 0.10% or 0.25%. Basis Points (BPS) are used to clearly communicate these small changes, making them easily understandable.

To avoid confusion : When expressing a percentage change, it is sometimes unclear whether the change is a percentage point or a percentage increase. Using BPS eliminates this confusion and allows the change to be communicated more directly and accurately.

To standardize financial communication : Banks, investment institutions, and central banks all use Basis Points to communicate rate changes in a uniform manner. This makes reports, policy updates, and market analysis easier to understand.

To accurately report policy rate changes : Central banks like the RBI often change their monetary policy by 25 bps or 50 bps. This provides the market with a clear picture of the exact change in interest rates.

For professional financial reporting : Accurate data is crucial in financial markets, bond yields, and investment analysis. Therefore, the use of Basis Points is considered a standard method in professional reporting and analysis.

Where Basis Points Are Commonly Used

Central Bank Policy : Central banks like the RBI often express interest rate changes in their monetary policy in Basis Points (BPS). For example, when a small change is made to the repo rate, it is announced as 25 BPS or 50 BPS, making it easier to understand the exact change in the rate.

Bond Market : In the bond market, BPS is used to represent small changes in bond yields. Investors and analysts often report how many BPS the yield on a government or corporate bond has increased or decreased.

Mutual Funds : In the mutual fund industry, small changes in expense ratios or returns are also expressed in Basis Points. This helps investors understand how small the change in fund costs or performance is.

Banking and Loan Rates : When banks change interest rates on loans or deposits, they are also reported in BPS. For example, banks may announce that home loan interest rates have been reduced by 20 BPS.

Financial Market Analysis : Basis points are also used in financial market reports and analysis to explain small changes in yield, interest rates, and returns, presenting the data in a professional and accurate manner.

Why Basis Points Matter for Investors

Help in Understanding Interest Rate Changes : Interest rate movements are very important for investors. When rate changes are expressed in bps, investors can easily understand how large or small the actual change is and how it may impact their investments.

Impact on Bond Investments : Even a small bps increase in yield in the bond market can affect bond prices. Generally, when bond yields rise, the prices of existing bonds fall. Therefore, investors investing in bonds closely monitor bps changes.

Debt Mutual Fund Performance : The returns of debt mutual funds also depend on interest rates. If market interest rates rise by a few bps, this changes bond prices and can directly impact the fund’s NAV.

Loan Cost and Borrowing Impact : Many investors also invest by taking out loans or have home loans or business loans. If banks raise interest rates by 20–50 bps, EMIs and borrowing costs may increase, impacting investment plans.

Market Trend and Policy Signals : When central banks change policy rates based on bps, it sends a signal to the entire market. Investors can make informed decisions about equity, bond, and fixed-income investments by observing these changes.

Common Mistakes People Make When Understanding BPS

Mistaking BPS for Percentages : Many people mistake Basis Points (BPS) for percentages. For example, some mistake 50 BPS for 50%, when in reality, 50 BPS = 0.50%. Therefore, it’s important to understand the difference between BPS and percentage points.

Confusion Between Percentage Change and Percentage Point : In finance, percentage change and percentage point change are different. BPS always represents a percentage point change. If an interest rate changes by 100 BPS, it means a direct change of 1% in the rate.

Ignoring Small Changes : Many investors and readers think that a change of 10–20 BPS is very small, but its impact on a large investment or loan amount can be significant. Therefore, even small BPS changes are considered significant in the financial markets.

Misunderstanding Financial News : When financial news reports that interest rates have increased or decreased by 25 bps, many people don’t understand it correctly. Understanding the correct meaning of BPS makes it easier to understand banking updates, policy decisions, and market reports.

Conclusion

The term Basis Point (BPS) is frequently encountered in finance and banking news. It’s a simple and accurate way to describe small changes in interest rates or returns. Once you understand the meaning of BPS, it’s much easier to understand banking updates, RBI policy announcements, and investment news. Therefore, understanding BPS is a useful tool when learning financial terms.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Infrastructure has always been the backbone of a nation’s economic growth, shaping how people move, work, and build businesses.

When you step outside, you’ll probably see the indications of India’s fast development: modern airports are growing all over the nation, metro networks are growing through cities, and new highways are stretching across states. One of the most talked-about investment themes in the market today is infrastructure development, which is occurring at a rate never seen before.

If you want to grow your wealth over the next decade, finding the best infrastructure fund might be on your mind. Many investors often look for the top 5 infrastructure mutual funds India has to offer right now. In this blog, we will learn and understand how to pick the best infrastructure mutual funds for your portfolio.

What Are Infrastructure Mutual Funds?

Infrastructure mutual funds are special types of equity mutual funds, where the main objective is to invest the money of investors in the shares of companies that help build the country. As per the rules, these funds must put at least 80 percent of their money into infrastructure related businesses.

When you invest in these funds, you are buying a small piece of many different companies. The types of infrastructure companies these funds invest in are quite varied. They include:

Construction and engineering companies that build roads and bridges.

Energy companies that generate power and manage oil refineries.

Material makers who produce cement and steel.

Transport companies that manage shipping and airports.

Telecom companies that set up mobile networks and data centers.

By investing in these funds, you are not just putting your funds in one company. You bet on the entire growth sector of India.

The fund’s main investment is in sectors related to construction, engineering, and power generation. Here the fund aims for high capital growth by dynamically changing its stock picks based on market trends. Major holdings of this fund includes Larsen & Toubro and Reliance Industries. Altogether this is a risky fund as the fund manager takes bold bets, which can lead to quick ups and downs in a short time span.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Quant Infrastructure Fund

8.46

18.41

23.58

2. Invesco India Infrastructure Fund

In this fund the focus is on companies that have a strong business model and also have a good cash flow. Unlike others, this fund puts nearly half of its money into mid and small companies. The fund focuses on capital goods and electrical equipment companies. As there are mostly mid and small cap companies included in this fund, the risk is very high. However, it has delivered excellent long term returns in the past.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Invesco India Infrastructure Fund

12.67

22.95

20.94

3. ICICI Prudential Infrastructure Fund

This is one of the biggest funds in the infrastructure mutual funds sector. It looks for solid companies available at a fair price. It mainly invests in large and famous companies like NTPC and Interglobe Aviation. Focus of this fund is on companies related to the energy and construction sector. It is less volatile than funds that buy small companies, but it still carries high sectoral risk.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

ICICI Prudential Infrastructure Fund

13.29

24.18

25.47

4. Bandhan Infrastructure Fund

This fund tries to find companies that will directly benefit from government spending in a specific infrastructure sector. This fund has a mix of both large and small companies in the market. Top sectors include capital goods and materials based companies. This fund comes under a very high risk profile. The fund looks for turnaround stories of companies which can take time to play out.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Bandhan Infrastructure Fund

9.40

23.43

20.37

5. Nippon India Power & Infra Fund

This fund revolves around the power sector. It wants to capture growth from electricity generation and traditional infrastructure companies. It invests deeply in the utilities and industries sector. Interestingly, this fund is a little stable and less fluctuating as compared to the general market. The fund has shown a great ability to balance risk and reward.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Nippon India Power & Infra Fund

18.12

25.56

23.27

6. Canara Robeco Infrastructure Fund

In this fund the investment is majorly made in market leading companies cumulatively. It looks for businesses with a unique advantage.About 61 percent of its money is put by the fund in large companies. The focus of this fund is on companies that deal in the power and heavy engineering sector. It is a high risk fund, but focusing on big companies helps protect your money when the market falls.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Canara Robeco Infrastructure Fund

21.33

26.18

24.30

7. DSP India T.I.G.E.R. Fund

TIGER stands for The Infrastructure Growth and Economic Reforms Fund. The fund focuses on companies that do structural changes in the country. The fund buys shares across all sizes of companies. It even invests in the healthcare and telecom sector, showing a modern view of infrastructure. It is a very high risk fund and wants the investors to stay invested for at least seven years to see the best results.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

DSP India T.I.G.E.R. Fund

22.07

26.22

23.85

8. Franklin Build India Fund

This fund looks for sustainable businesses and avoids companies that only do well in specific short cycles. The main focus of the fund is on the energy sector and also holds strong positions in transport and industrials. It is known for managing risk very well as it limits downside losses better than many of its peers.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Franklin Build India Fund

20.66

28.00

24.09

9. Kotak Infrastructure and Economic Reform Fund

It aims to grow wealth by investing in companies that benefit from India’s economic development. It heavily invests in construction, telecom, and auto parts. The fund carries a very high risk rating. It also tries to capture value across many parts of the economy.

Fund Name

1-Year Return (%)

3-Year Return (%)

5-Year Return (%)

Kotak Infrastructure & Economic Reform

20.01

20.51

21.89

10. SBI Infrastructure Fund

It aims to provide steady long term growth by picking a concentrated basket of infrastructure stocks. The fund places big bets on energy and construction giants like Shree Cement and Bharti Airtel. This fund has shown a balanced approach as it protects your capital well during bad market phases.

India’s Infrastructure Growth Story: India is a developing country and growing at a fast pace. For this developing country people require more houses, faster trains, and larger data centers. For example, India’s data center capacity is expected to grow massively by 2030 because of new technologies like Artificial Intelligence. This means companies building these digital and physical assets will have a lot of work for many years.

Government Initiatives and Budgetary Support: The government is the biggest customer for infrastructure companies. Recently, the government increased its budget for infrastructure to over Rs.11 lakh crore. They have also launched plans like PM Gati Shakti to make sure projects finish on time without delays. This gives companies a clear path to make profits.

Sector Multiplier Effect on Broader Economy: You must have heard about the multiplier effect, the Reserve Bank of India shows that for every 1 rupee the government spends on infrastructure, the overall economy grows by 2.5 to 3.5 rupees. Building a road & bridges creates jobs and people with jobs tend to buy more goods. This helps the whole country grow, making infrastructure companies very valuable.

Long-Term Wealth Creation Potential: Companies that build airports or power plants face very little competition as it is too expensive for a new player to enter this sector with very less experience. Because of this, existing companies enjoy steady business and predictable cash flows. If you stay invested for a long time, these steady profits compound and create massive wealth for you.

Advantages of Investing in Infrastructure Mutual Funds

Protection from Inflation: When prices of goods go up, infrastructure companies often increase their fees. For example, toll road prices go up with inflation. This protects your investment value.

Clear Earnings: Infrastructure based companies often have long contracts with the government, investors can easily guess their future profits.

Variety: Infrastructure based companies are not limited to cement companies. You are also investing in companies related to green energy, digital data centers, and telecom networks.

Disadvantages of Investing in Infrastructure Mutual Funds

Policy Delays: These projects need a lot of permissions and norms to be fulfilled If the government changes a rule or delays a permit, the company can lose money.

Economic Cycles: If the economy slows down and interest rates go up, new construction projects are halted, which can severely hurt your fund returns.

High Risk: Because the fund only invests in one theme, if the whole infrastructure sector performs poorly, your entire investment will drop in value.

How to Choose the Best Infrastructure Mutual Fund

Past Performance and Consistency: Investors shall always look for the fund’s past performance or how the fund performed over the last 3, 5, and 10 years. A good fund is one that consistently beats its benchmark index year after year.

Fund Size and Liquidity: Fund size is also called Assets Under Management or AUM. A very small fund might be risky for the investors and a very huge fund might struggle to buy and sell small company stocks quickly. A fund with a decent size that matches its strategy is the best choice.

Fund Manager Experience: Infrastructure is a complex sector which requires understanding of government policies and big bank loans. Choose a fund managed by someone who has been in the market for a long time and has seen the markets in depth.

Expense Ratio and Charges: This is the fee the mutual fund company charges you for managing your money. Even a small difference in fees can eat up your wealth over 10 years. Always try to pick funds with a lower expense ratio, also direct plans are cheaper than regular plans.

Investment Timeline: You cannot invest in infrastructure funds for just one or two years. These projects take years to complete. You should only invest in these funds if you have patience for at least 5 to 7 years.

Conclusion

To sum it up, the infrastructure sector in India offers a brilliant chance for long term investors. The country is developing and building its future, and the government is fully supporting this growth. By adding a good infrastructure mutual fund to your portfolio, you can be a part of this amazing journey.

For more market news and insights, download Pocketful – offering users zero brokerage on delivery trades and an easy to use platform designed for both beginners and experienced investors.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Are infrastructure mutual funds safe for beginners?

These funds carry a very high risk because they focus on only one sector so first understand the risk and then invest.

How much tax do I have to pay on my profits?

If you sell your investment before one year, you will pay a 20 percent tax on your profit. If you sell after one year, your profit up to Rs.1.25 lakh is tax free. Anything above that is taxed at 12.5 percent.

Do these funds only invest in building roads and bridges?

These funds invest in overall infrastructure alongwith telecom towers, green energy plants, airports, and digital data centers.

How long should I keep my money in these funds?

Infrastructure projects take a long time to finish and make profits. You should be ready to keep your money invested for at least 5 to 7 years to get good returns.

Can Non-Resident Indians (NRIs) invest in these funds?

Yes, NRIs can easily invest in Indian mutual funds. You just need to complete a simple KYC process and use an NRE or NRO bank account to start investing.

Gone were those days when one used to consider Gold and Silver as physical assets only. Now, there are various precious metal mutual funds to invest in India, through which one can invest in precious metals in a more professional, economical and convenient manner.

In today’s blog post, we will give you an overview of the best precious metal funds to invest in India.

What are Precious Metal Mutual Funds?

Precious metal mutual funds are the schemes offered by asset management companies that primarily give you exposure to precious metals or commonly known commodities such as Gold, Silver, etc. By investing in metal mutual funds, one can gain exposure to precious metals without the hassle of physical storage.

Features of Precious Metal Mutual Funds

The key features of precious metal mutual funds are as follows:

Affordability: One can easily invest in metal mutual funds with small amounts. And monthly investments through SIPs can also be made in it.

Liquidity: Unlike physical metals, mutual funds offer greater liquidity, as investors can invest and withdraw funds at any time.

Inflation Hedge: Metal mutual funds offer a hedge against inflation; hence, they can protect purchasing power during high-inflation regimes.

Transparency: Prices of metal mutual funds are linked to domestic gold prices and are influenced by global factors.

Top Precious Metal Mutual Funds to Invest in India

SBI Gold Fund

HDFC Gold ETF Fund of Fund

Nippon India Gold Savings Fund

Kotak Gold Fund

ICICI Prudential Gold ETF FoF

Nippon India Silver ETF FoF

HDFC Silver ETF FoF

SBI Silver ETF FoF

Axis Gold Fund

Edelweiss Gold and Silver ETF FoF

Funds

NAV (INR)

Net Assets (INR Cr)

Exit Load (%)

Expense Ratio (%)

SBI Gold Fund

47.56

15024

1.00 (15D)

0.24

HDFC Gold ETF Fund of Fund

48.56

11457

1.00 (15D)

0.18

Nippon India Gold Savings Fund

62.05

7160

1.00 (15D)

0.13

Kotak Gold Fund

62.83

6556

1.00 (15D)

0.16

ICICI Prudential Gold ETF FoF

49.83

6338

1.00 (15D)

0.09

Nippon India Silver ETF FoF

39.47

6099

1.00 (15D)

0.26

HDFC Silver ETF FoF

42.71

5811

1.00 (15D)

0.23

SBI Silver ETF FoF

27.59

4779

1.00 (15D)

0.30

Axis Gold Fund

49.04

2834

1.00 (15D)

0.17

Edelweiss Gold and Silver ETF FoF

36.68

3082

0.10 (15D)

0.23

(Data as of 12th Feb 2026)

Overview of the Best Precious Metal Mutual Fund

1. SBI Gold Fund

SBI Gold Fund is a recently-launched fund managed by SBI Funds Management Pvt. LTD., based in Mumbai, was launched in September 2011. Gold ETFs are the major investments in the fund as it tracks domestic gold prices, and they are a favourite investment option to provide protection against inflation, portfolio diversification, and disciplined investment in gold through SIPs.

2. HDFC Gold ETF Fund of Fund

This fund is offered by HDFC Asset Management Company Ltd., Mumbai, and was launched in November 2011. It invests in HDFC Gold ETFs to reflect the movements of the gold prices, and it is very popular in systematic investing, long-term wealth protection, and providing stability to the equity-intensive portfolios.

3. Nippon India Gold Savings Fund

This fund was started in March 2011 by Nippon Life India Asset Management Ltd, which is based in Mumbai and offers an exposure to gold using ETFs and other related instruments. It is characterised by effective cost management and is appropriate for investors interested in protecting against inflation and market volatility.

4. Kotak Gold Fund

This fund, managed by Kotak Mahindra Asset Management Company Ltd., Mumbai, and started in March 2011, tracks the movement of gold prices by investing in gold ETFs. It is the appropriate investment choice among investors who wish to have a consistent exposure to gold through SIPs with a highly rated and reputable AMC.

5. ICICI Prudential Gold ETF FoF

This gold Fund-of-Fund, launched in 2011 by ICICI Prudential Asset Management Company Ltd., Mumbai, invests in gold ETFs to track domestic gold prices. It is attractive to investors who are interested in having a good exposure to gold with the support of ICICI Prudential’s good fund management and distribution network.

6. Nippon India Silver ETF FoF

This fund was introduced in February 2022 by Nippon Life India Asset Management Ltd., Mumbai, and it offers exposure to the prices of silver in the form of silver ETFs. It fits well with the investors who want to diversify their holdings other than gold and enjoy the benefits of the industrial and investment demand for silver.

7. HDFC Silver ETF FoF

This fund is managed by HDFC Asset Management Company Ltd., Mumbai and was launched in 2022. It tracks silver prices by using silver ETFs. It provides an investor with an easy entry to the silver price movement, enjoying the convenience and transparency of the mutual fund path.

8. SBI Silver ETF FoF

This fund was launched in the year 2022 by SBI Mutual Fund. This fund tracks the performance of silver ETFs, and investors can take the exposure in it through SIPs and a lump sum.

9. Axis Gold Fund

This is a fund which follows and tracks the price of gold by investing in gold ETFs and was launched in October 2011 by the Axis Asset Management Company Ltd., Mumbai. It is characterised by fair prices and a stable monitoring system, and is appropriate for those investors who want to have a stable portfolio in the form of gold over time.

10. Edelweiss Gold and Silver ETF FoF

Launched by Edelweiss Asset Management Ltd., Mumbai, in August 2022, this is a unique fund that holds both gold and silver ETFs. It provides two precious-metal exposures within a scheme, which is perfect for investors who want more diversification in commodities.

Why One Should Invest in a Precious Metal Mutual Fund

One should invest in a precious metal mutual fund because it acts as a hedge against inflation and also provides stability in the portfolio, as it has low correlation with equity and bonds. In case of global uncertainty, geopolitical tensions, etc., investors considered precious metals as a safe haven to park funds. Hence, one can allocate a certain portion of their portfolio into precious metals.

Conclusion

On a concluding note, investment in a precious metal mutual fund is the most economical and efficient way of investing in gold, silver, etc. It offers a low-cost investment option to have an allocation in gold and silver. Most of the precious metal mutual fund tracks the performance of underlying gold and silver ETFs, reflecting the changes in domestic prices of precious metals. However, one should invest in these funds only after consulting their investment advisors.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What is the meaning of precious metal mutual funds?

Precious metal mutual funds are the funds offered by the asset management companies which primarily invest in metals like silver, gold, etc., generally through ETFs or Overseas funds.

Do I need a demat account to invest in metal mutual funds?

No, you do not require a demat and trading account to invest in metal mutual funds.

Are returns from precious metal mutual funds guaranteed?

No, the returns from precious metals are not guaranteed; their performance depends on various factors such as interest rates, inflation, global commodities prices, etc.

Can I invest in metal mutual funds through SIP?

Yes, one can easily invest in precious metal mutual funds through SIP (Systematic Investment Plan).

What are the factors to consider before investing in precious metal mutual funds?

There are various factors which an investor should consider before investing in precious metal mutual funds, which include AMC track records, past performance of the fund, tracking error, expense ratio, etc.

People in India want to grow their savings but they do not have the right knowledge and are even afraid of investing in the stock market. If you are one of these people, then a fund of fund strategy might be the right way to invest. It is a simple way where the experts manage your savings while you sit back and watch.

FOF full form is Fund of Funds and in the world of finance, the FOF meaning is quite easy to understand. It is a type of mutual fund that does not buy stocks or bonds directly. Instead, a FOF mutual fund takes the money it gets from investors and uses it to buy units of other mutual funds. Imagine it as a “collection of collections”. If a regular mutual fund is a basket of fruits, a fund of fund is a large box that contains many different fruit baskets.

So, what is FOF in mutual fund terms for the average Indian investor? It is a tool that offers double protection. A regular fund manager picks the best stocks, but an FOF manager picks the best fund managers. More than 5 crore Indians now invest in mutual funds, and FOFs are a growing part of this list.

What is a Fund of Funds?

A Fund of Funds (FOF) is a unique investment plan where one mutual fund scheme invests in other mutual fund schemes. This is different from a traditional mutual fund. In a traditional fund, the manager uses your money to buy assets like company shares or government bonds directly. In an FOF, the manager creates a portfolio using existing mutual funds as the building blocks.

There are two main ways these funds are structured. Some are called “fettered” funds. This means the FOF only invests in other funds managed by the same company. For example, an ICICI FOF might only buy other ICICI funds. Others are called “unfettered” funds. These have the freedom to buy funds from any company in the market, allowing the manager to pick the top performers from across the industry.

Feature

Traditional Mutual Funds

Funds of Funds (FOF)

What you can get

Direct stocks, bonds, or gold

Units of other mutual funds

Who manages it

One fund manager or team

A multi-manager approach

Risk level

Depends on the stocks or bonds chosen

Spread across many funds and styles

Number of managers

Single point of expertise

Benefits of several expert managers

How Does a Fund of Funds Work?

It starts with pooling investor money. Thousands of people like you contribute small amounts, which create a large pool of capital. The FOF manager then uses this large amount to buy units of different mutual funds. This creates a “multi-layered” portfolio.

The Role of the Fund Manager

In an FOF, the fund manager does not spend their time researching individual companies. Instead, they research other fund managers and their performance. They look at how consistent a fund has been over 3 years or 5 years. They check if a fund house follows its promises. The manager then decides how much money to put into each underlying fund.

Advantages of the Multi-Manager Approach

The multi-manager approach is like having a team of experts instead of just one. Every fund house has a different strength. One house might be great at picking small companies, while another is better at safe government bonds. An unfettered FOF can pick the best small-cap fund from one place and the best debt fund from another. This approach also reduces what we call “manager risk.”

There are many types of FOFs available in the Indian market today. Each type serves a different goal. Depending on whether you want high growth or safety, you can choose the one that fits you best.

1. Multi-Asset Fund of Funds

A multi-asset FOF invests in a mix of equity, debt, and gold funds. The goal is to give you a balanced portfolio with one single investment. Financial experts often use the “Thali” analogy for this.

2. ETF-Based FOFs

Exchange-Traded Funds (ETFs) are funds that follow a market index like the Nifty 50. An ETF-based FOF allows you to invest in a basket of ETFs through a regular mutual fund application.

3. International Fund of Funds

Many Indian investors want to own shares of famous global companies like Apple, Google, or Amazon. However, investing directly in the US or European markets is very hard but in International FOFs you give them money in Indian Rupees, and they invest it in international funds.

4. Gold Fund of Funds

A Gold FOF invests in Gold ETFs, which track the market price of 24-karat gold. You can start a Systematic Investment Plan (SIP) in gold for as little as Rs.500. It gives you the same returns as physical gold without any storage worries.

Comparison of Popular Gold Investment Methods

Feature

Physical Gold

Gold ETF

Gold FOF

Storage

Home or Locker (Risky/Fees)

Digital (Safe)

Digital (Safe)

Demat Account

Not Required

Required

Not Required

Making Charges

Yes (High making charges)

No

No

Liquidity

Medium (Jeweler)

High (Trade on exchange)

High (Redeem with AMC)

Small Investment

Not easy

Can be done

Very easy (via SIP)

Other types of FOFs

Sector specific FOFs: These funds focus here on specific sectors like technology or pharma, or specific countries.

Passive vs. Active FOFs: Passive FOFs rely on simply following an index to keep costs low. Active FOFs try to beat the market by making smart choices.

Hedge Fund FOFs: These are for very wealthy investors (HNIs). They use complex strategies to make money even when the market is falling. In India, these usually require a minimum investment of Rs.1 crore.

Excellent Diversification: The main advantage of FOFs is that the investors get access to a variety of mutual funds by doing just one investment. This layered diversification protects the investors from sudden market swings. If one company or even one fund house gives a bad result then your overall loss can be limited.

Professional Selection: There are thousands of schemes in India. An FOF manager uses institutional research to analyze performance, consistency, and risk. You get the benefit of this deep research without doing your own R&D.

Ease of Access: FOFs provide access to funds that might be hard for you to invest in directly. This includes niche sector funds or international funds from global partners like Franklin Templeton or DSP BlackRock. You can manage a global portfolio with one single NAV (Net Asset Value) to track.

Discipline and Rebalancing: When the market goes up, we want to buy more equity and as it goes down, we feel like selling. An FOF manager follows a strict plan, they even rebalance the portfolio based on market conditions, not emotions.

Disadvantages of Investing in FOFs

Higher Layered Fees: Since an FOF invests in other funds, there are two layers of fees. You pay a management fee for the FOF itself. The underlying funds also have their own expense ratios.

Diluted Returns: Diversification is a great option for safety, but too much of it can dilute your returns. If one fund in the FOF gives good returns, its impact might be reduced if the other four funds only give average returns.

Tax Complexity: In India, FOFs are often taxed like debt funds, even if they invest in equity funds. This is because they do not invest directly in the shares of Indian companies. If you are in the 30% tax bracket, the short-term tax on an FOF can be quite high.

How to Invest in a Fund of Funds

The process of investing in an FOF is straightforward. You can do it online from the comfort of your home.

1. Complete Your KYC

The first step is always KYC (Know Your Customer). You need to submit your PAN card, Aadhaar card, and address proof. Most modern apps allow you to complete this digitally in a few minutes. You may need to do a short video verification to prove you are the person in the documents.

2. Choose the Right Fund

Look for an FOF that matches your financial goals. If you want to grow wealth over ten years, look for an equity-heavy FOF. If you want safety for a goal two years away, look for one with more debt and gold exposure. Always check the expense ratio and the track record of the fund manager before choosing.

3. Pick Your Investment Mode

SIP (Systematic Investment Plan): This is one of the suitable and easy ways for most people.You invest a fixed amount like Rs.1,000 every month with discipline and help you buy more units when the market is low.

Lump Sum: If you have good savings, you can invest it all at once. This is best if you know that the market is at a good price.

4. Track and Review

Once you invest, you have to keep an eye on it and check your fund’s performance every few months. Compare it to other similar FOFs as most apps will give you a detailed report of your returns and the current value of your portfolio.

Pocketful is an excellent platform for both new and experienced investors in India. In this you get a user-friendly way to manage your mutual funds and FOFs.

Zero Brokerage: Pocketful provides zero brokerage on delivery trades, making it very affordable for the users.

Simple KYC: You can complete your digital KYC and start trading in just minutes.

One-Click Investing: They offer “Pockets,” which are curated baskets of investments based on themes like Green Energy or Digital India.

Tools for Success: The app includes a Portfolio Analyser where you can easily identify risks and you also get a dedicated customer support team for your doubt and queries.

Conclusion

Fund of Funds (FOF) are a powerful way to make your financial life very easy. In FOF the investors get a safety net as there is a multi-layer diversification and you can reduce your stress by not choosing the individual mutual funds. While your expenses are little due to fees and even a unique tax structure, the professional management and ease of access to global markets and gold often outweigh these negatives. Whether you are a beginner looking for a balanced “thali” or a seasoned investor looking for global exposure, FOFs provide a structured and disciplined path to wealth.

For more market news and insights, download Pocketful – offering users zero brokerage on delivery trades and an easy to use platform designed for both beginners and experienced investors.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Is a Fund of Funds safer than a regular mutual fund?

Generally yes as FOF is diversified across multiple funds and several fund managers, it is less likely to see extreme drops if one manager makes a mistake.

Can I invest in an FOF without a Demat account?

Most of the FOFs do not require a Demat account and you can easily buy them directly through an AMC or through apps like Pocketful just like regular mutual funds.

Why is the taxation of FOFs different?

In India, a fund is taxed as “Equity” only if it invests directly in Indian shares. Since FOFs invest in other funds, the law treats most of them as non-equity or debt funds for tax purposes.

Can I start an SIP with a small amount in an FOF?

Generally FOFs allow you to start an SIP with as little as Rs.500. This is one of the best ways for young professionals to start their investment journey.

Are the higher fees of FOFs worth it?

If you have the time and knowledge to pick and track five different funds yourself, you can save on the extra FOF fee. But if you want a “hands-off” experience and professional rebalancing, the small extra cost is often worth the convenience.

In today’s volatile stock market, investors are seeking options that offer both security and predictable returns. This is why corporate bonds are gaining attention in 2026. Bond yields have reached attractive levels in recent months, and the Reserve Bank of India’s policies have boosted confidence in this sector. As a result, many are now considering the best corporate bonds in India as a viable long-term investment option.

What Are Corporate Bonds and How Do They Work?

Corporate bonds are investment instruments through which companies raise money from investors and, in return, pay them a fixed rate of interest. They have a fixed maturity period, at the end of which the invested principal is repaid. The risk associated with these bonds depends on the financial health of the issuing company, and the returns are typically higher than those of government bonds.

Best Corporate Bonds Mutual Funds in India (2026)

HDFC Corporate Bond Fund

ICICI Prudential Corporate Bond Fund

SBI Corporate Bond Fund Direct Growth

Kotak Corporate Bond Fund Direct Growth

Bandhan Corporate Bond Fund Direct Growth

Nippon India Corporate Bond Fund Direct Growth

Axis Corporate Bond Fund Direct Growth

Tata Corporate Bond Fund Direct Growth

Franklin India Corporate Debt Fund

Baroda BNP Paribas Corporate Bond Fund Direct Growth

1. HDFC Corporate Bond Fund

The HDFC Corporate Bond Fund is managed by HDFC Mutual Fund, which was established in 1999. This fund primarily invests in high-quality corporate and government bonds, including those of well-known institutions such as State Bank of India, Bajaj Finance, and the Government of India. The fund focuses on generating stable income with controlled risk. Its performance has consistently been in line with its category over the long term, and its portfolio is diversified across various sectors.

Fund Details :

Details

Information

Current NAV

34.09

Fund Size

34,804.50

Expense Ratio

0.62%

Minimum Investment

₹100

Minimum SIP

₹100

Exit Load

Nil

Lock-in Period

NA

Fund Manager

Anupam Joshi

Fund Performance

Metric

Value

3-year return

7.39%

5-year return

6.12%

Alpha

0.03%

Beta

0.43

Sharpe Ratio

0.1996

Risk

7.39%

(Data as of 03 Feb 2026)

2. ICICI Prudential Corporate Bond Fund

ICICI Prudential Corporate Bond Fund is a debt fund that invests in high-quality corporate bonds and government securities. Its portfolio is diversified across various sectors, including LIC Housing Finance, government securities, and infrastructure-related companies. The fund is managed by Manish Banthia. Its performance over the past few years has been consistent with the category average, and its focus remains on maintaining a balanced risk profile with stable returns.

Fund Details :

Details

Information

Current NAV

32.71

Fund Size

33871.47

Expense Ratio

0.57%

Minimum Investment

₹100

Minimum SIP

₹100

Exit Load

Nil

Lock-in Period

NA

Fund Manager

Manish Banthia

Fund Performance

Metric

Value

3-year return

7.67%

5-year return

6.46%

Alpha

0.06%

Beta

0.28

Sharpe Ratio

0.3588

Risk

7.67%

(Data as of 03 Feb 2026)

3. SBI Corporate Bond Fund

The SBI Corporate Bond Fund is managed by SBI Mutual Fund, which was established in 1992 and is one of the oldest and largest fund houses in the country. This fund invests in corporate bonds and government securities, maintaining a balanced portfolio. Its major holdings include investments in entities such as Government of India Bonds, NABARD, Pipeline Infrastructure, and Bharti Telecom. The fund is managed by Rajeev Radhakrishnan, and its focus is on generating stable returns while managing risk.

Fund Details :

Details

Information

Current NAV

₹15.94

Fund Size

24.606.87

Expense Ratio

0.77%

Minimum Investment

₹5,000

Minimum SIP

₹500

Exit Load

NA

Lock-in Period

NA

Fund Manager

Rajeev Radhakrishnan

Fund Performance

Metric

Value

3-year return

7.17%

5-year return

5.82%

Alpha

0.02%

Beta

0.42

Sharpe Ratio

0.1606

Risk

7.17%

(Data as of 03 Feb 2026)

4. Kotak Corporate Bond Fund Direct Growth

The Kotak Corporate Bond Fund Direct Growth is managed by Kotak Mutual Fund and overseen by Deepak Agrawal. This fund primarily invests in high-quality corporate bonds and government securities, maintaining a balanced portfolio. Its major investments are in Government of India Bonds and institutions like NABARD, which demonstrate stability and a reliable credit profile. The fund’s structure focuses on generating stable returns over the long term while managing risk effectively.

Fund Details :

Details

Information

Current NAV

4063.35

Fund Size

18,840

Expense Ratio

0.69%

Minimum Investment

₹100

Minimum SIP

₹100

Exit Load

NA

Lock-in Period

NA

Fund Manager

Deepak Agrawal

Fund Performance

Metric

Value

3-year return

7.45%

5-year return

6.17%

Alpha

0.04%

Beta

0.40

Sharpe Ratio

0.2295

Risk

7.45%

(Data as of 03 Feb 2026)

5. Bandhan Corporate Bond Fund

The Bandhan Corporate Bond Fund is managed by Bandhan Mutual Fund, which was established in 1999. The fund is managed by Suyash Choudhary. Its portfolio primarily invests in government bonds and debt instruments of strong corporate companies. Its major holdings include Government of India Bonds, along with large corporate names such as Larsen & Toubro and Reliance Industries. It also includes a portion of Net Current Assets, ensuring a balanced and diversified investment structure for the fund.

Fund Details :

Details

Information

Current NAV

20.36

Fund Size

14,855.50

Expense Ratio

0.65%

Minimum Investment

₹1,000

Minimum SIP

₹100

Exit Load

NA

Lock-in Period

NA

Fund Manager

Suyash Choudhary

Fund Performance

Metric

Value

3-year return

7.08%

5-year return

5.79%

Alpha

0.01%

Beta

0.32

Sharpe Ratio

0.1565

Risk

7.08%

(Data as of 03 Feb 2026)

6. Nippon India Corporate Bond Fund

The Nippon India Corporate Bond Fund is managed by Nippon India Mutual Fund, which was established in 1995. The fund is managed by Vivek Sharma. Its portfolio primarily invests in government bonds and debt instruments of strong corporate entities. Its major holdings include Government of India Bonds, along with investments in companies such as NABARD, Aditya Birla Housing Finance, Siddhivinayak Securitisation Trust, and Shivshakti Securitisation Trust. It also maintains a portion in net current assets, ensuring a balanced and diversified investment structure.

Fund Details :

Details

Information

Current NAV

₹61.65

Fund Size

10,430.66

Expense Ratio

0.76%

Minimum Investment

₹1,000

Minimum SIP

₹100

Exit Load

NA

Lock-in Period

NA

Fund Manager

Vivek Sharma

Fund Performance

Metric

Value

3-year return

7.50%

5-year return

6.51%

Alpha

0.04%

Beta

0.46

Sharpe Ratio

0.2193

Risk

7.50%

(Data as of 03 Feb 2026)

7. Axis Corporate Bond Fund

The Axis Corporate Bond Fund is managed by Axis Mutual Fund, which was established in 2009. The fund is managed by Devang Shah. Its portfolio invests in government bonds and debt instruments issued by financial institutions. Its major holdings include Government of India Bonds, along with instruments from institutions such as NABARD, Clearing Corporation of India, and SIDBI. It also maintains a portion in Net Current Assets, ensuring a balanced and diversified investment structure for the fund.

Fund Details :

Details

Information

Current NAV

18.65

Fund Size

9,435.82

Expense Ratio

0.95%

Minimum Investment

₹100

Minimum SIP

₹1,000

Exit Load

NA

Lock-in Period

NA

Fund Manager

Devang Shah

Fund Performance

Metric

Value

3-year return

7.34%

5-year return

6.07%

Alpha

0.02%

Beta

0.41

Sharpe Ratio

0.1967

Risk

7.34%

(Data as of 03 Feb 2026)

8. Tata Corporate Bond Fund Direct Growth

The Tata Corporate Bond Fund Direct Growth is managed by Tata Mutual Fund, which was established in 1994 and is one of India’s oldest and most trusted fund houses. The fund is managed by Murthy Nagarajan. Its portfolio primarily invests in government bonds and corporate bonds issued by financial institutions. Its major holdings include instruments from institutions such as the Government of India, NABARD, National Housing Bank, and SIDBI, ensuring a balanced and diversified portfolio.

Fund Details :

Details

Information

Current NAV

12.68

Fund Size

4235

Expense Ratio

0.86%

Minimum Investment

₹5,000

Minimum SIP

₹150

Exit Load

NA

Lock-in Period

NA

Fund Manager

Murthy Nagarajan

Fund Performance

Metric

Value

3-year return

7.12%

5-year return

–

Alpha

0.01%

Beta

0.44

Sharpe Ratio

0.1502

Risk

7.12%

(Data as of 03 Feb 2026)

9. Franklin India Corporate Debt Fund

The Franklin India Corporate Debt Fund is managed by Franklin Templeton Mutual Fund, which was established in 1995. The fund is managed by Anuj Tagra. Its portfolio is diversified across government bonds and debt instruments of private companies. Its major holdings include Government of India Bonds, as well as investments in companies such as Poonawalla Fincorp, NABARD, RJ Corp, Sikka Ports & Terminals, REC, SIDBI, Embassy Office Parks REIT, and Jubilant Beverages, ensuring a balanced investment structure across diverse sectors.

Fund Details :

Details

Information

Current NAV

111.89

Fund Size

1,338.11

Expense Ratio

0.76%

Minimum Investment

₹10,000

Minimum SIP

NA

Exit Load

NA

Lock-in Period

NA

Fund Manager

Anuj Tagra

Fund Performance

Metric

Value

3-year return

7.67%

5-year return

–

Alpha

0.05%

Beta

0.32

Sharpe Ratio

0.2213

Risk

7.67%

(Data as of 03 Feb 2026)

10. Baroda BNP Paribas Corporate Bond Fund

The Baroda BNP Paribas Corporate Bond Fund is managed by Baroda BNP Paribas Mutual Fund, which was established in 2003. The fund is managed by Gurvinder Singh Wasan. Its portfolio invests in government bonds and debt instruments of large public and private sector companies. Its major holdings include NABARD, Indian Railway Finance Corporation (IRFC), REC, Export-Import Bank of India, NTPC, Bajaj Housing Finance, and Government of India Bonds. It also maintains a portion in Net Current Assets, ensuring a diversified and balanced investment structure.

Fund Details :

Details

Information

Current NAV

30.10

Fund Size

482.08

Expense Ratio

0.58%

Minimum Investment

₹5,000

Minimum SIP

₹500

Exit Load

NA

Lock-in Period

NA

Fund Manager

Gurvinder Singh Wasan

Fund Performance

Metric

Value

3-year return

7.61%

5-year return

5.57%

Alpha

0.04%

Beta

0.52

Sharpe Ratio

0.2141

Risk

7.61%

(Data as of 03 Feb 2026)

Risks Associated With Corporate Bond Funds

Deterioration of the company’s financial health : If the company in which the fund has invested experiences a decline in earnings, it may face difficulties in paying interest or repaying the principal. This impacts the fund’s value.

Impact of interest rate changes : When the RBI raises interest rates, the value of existing bonds decreases. This directly affects the fund’s Net Asset Value (NAV).

Difficulty in selling bonds quickly : Some bonds are not easily sold immediately. Selling them at a fair price when needed may take time.

Credit rating downgrade : If a company’s credit rating is downgraded, the value of its bonds may fall, affecting the fund’s returns.

Market uncertainty : Although these are considered safer than equity markets, economic conditions and government policies can influence their performance.

Conclusion

In conclusion, corporate bond funds are a balanced option for investors seeking regular and stable returns without taking on excessive risk. Choosing the right fund requires understanding not only the returns but also its holdings, fund manager, and expenses. With a little patience and the right information, corporate bond funds can bring stability to your portfolio.

Stay ahead with real-time market news and insights – download Pocketful today.

Enjoy zero brokerage on delivery & ETFs, plus advanced options trading tools on a fast, user-friendly platform.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

In India, mutual funds have gradually become a part of people’s everyday investment habits. Investing is no longer limited to large investors; even ordinary people are now participating in the market through SIPs (Systematic Investment Plans). The industry has grown rapidly, and along with it, investors’ mindsets have also changed. In this blog, we will understand the current state of the mutual fund industry and its future prospects in simple terms.

Current Size of the Mutual Fund Industry in India

Today, India’s mutual fund industry has become a strong pillar of the country’s financial system. By the end of December 2025, the industry’s total Assets Under Management (AUM) had exceeded ₹80 lakh crore, demonstrating the continuously growing confidence of investors.

AUM represents the total amount of money that mutual fund companies manage on behalf of investors across various schemes. Average AUM (AAUM), on the other hand, reflects the average assets under management over the entire month, providing insight into the stability of investment flows. The mutual fund industry has witnessed exceptional growth over the past ten years. While the total AUM was approximately ₹20 lakh crore in 2015, it has more than quadruple by 2025.

This rapid growth is primarily driven by the increasing popularity of SIP (Systematic Investment Plan) investments, easy access through digital platforms, and growing financial awareness among investors. Today, mutual funds are no longer limited to large investors; small and medium-sized investors are also participating regularly, further strengthening the industry’s foundation.

Year

Total AUM (₹ lakh crore)

2015

20.00 +

2020

30.00 +

2025

80.00 +

Category-wise Distribution of Mutual Fund Assets

Investment categories in the mutual fund industry

Equity Mutual Funds: Equity funds have become the largest segment of the mutual fund industry. Investors prefer them because of the potential for better returns from the stock market over the long term. Funds like Flexi-cap and multi-cap are seeing particular interest, as they can adjust their portfolios according to market conditions.

Debt Mutual Funds: Debt funds are suitable for investors who want to minimize risk and expect regular income. Because they invest in government and corporate bonds, they are also seen as an alternative to fixed deposits (FDs). Changes in interest rates directly impact these funds.

Hybrid Mutual Funds: Hybrid funds invest in both equity and debt. Their objective is to strike a balance between risk and return. They are considered a practical option for new investors and those with a moderate risk appetite.

Passive Funds and ETFs: Passive funds and ETFs have grown rapidly in popularity over the past few years. These funds have lower costs and track a specific index. Investors who want market-like returns at a lower cost are increasingly choosing them.

Gold and Commodity Funds: Gold and commodity-based funds are for investors who want to hedge against market uncertainty. Demand for these funds increases during times of inflation and global tension, as they are considered safe-haven investments.

Shifting Investor Preferences

Shift towards Equity and Passive Investing: Investors are now focusing not just on safe options, but on long-term wealth creation. This is why the share of equity and passive funds is increasing.

SIPs Connect with the Average Investor: SIPs (Systematic Investment Plans) have made investing easy and regular. It has become the most trusted method for investors in smaller cities and for new investors.

Focus on Cost and Transparency: Today, investors make decisions after understanding the expense ratio, fund strategy, and risk level. This is why low-cost and transparent products are being chosen more often.

Growth Drivers of Mutual Funds in India

Growing habit of SIP investments: SIPs have made investing easy and regular. People are able to invest small amounts every month, leading to a continuous increase in the number of investors over the long term.