Switzerland is renowned as a major global financial center, with Swiss banks famous for their strong privacy and strict confidentiality laws. These banks attract individuals and companies worldwide who value security and discretion for their wealth. But many people don’t know how to open a Swiss Bank Account.

In this blog, we will explain to you the procedure to open a Swiss Bank account.

What is a Swiss Bank Account?

A Swiss Bank is a financial institution situated in Switzerland, and is known for its privacy, strict laws, and secrecy. Accounts in these banks are generally opened by the person who seeks confidentiality and security. The Swiss Bank Law of 1934 states that it is a criminal offence for a bank to declare the details of a client to any other entity or person.

A Swiss bank is a global bank known for its exceptional security and secrecy. According to the Swiss Banking Law of 1934, it is illegal for a Swiss bank to reveal the identity of its account holders. However, Swiss banks did lose some transparency as a result of pressure from other countries. In addition to this, Swiss Bank complies with global banking and anti-money laundering laws. Hence, in the recent past, they are refusing to take on customers who are unable to show sufficient evidence of their wealth or income.

Types of Swiss Bank Accounts

The various types of Swiss Bank accounts are as follows:

Personal Account: This account is opened by an individual for their personal use and doing daily transactions. It generally includes savings and a current account. One can receive salary and other incomes in this account and make payments of bills, etc., using this account.

Business Account: This account is opened by companies and is generally used for holding investments or to conduct day to day transactions. This account offers a special kind of service, such as trade finance, treasury management, etc.

Numbered Account: In this type of account, the account holder’s name is replaced by a number to enhance privacy, and only a few senior bank officials know the true identity of the holder. However, Swiss law requires the bank to maintain proper identification records, and the holder’s details can be disclosed to authorities in cases involving tax treaties or legal investigations.

Custody Account: This account is generally opened by the individual to manage their investments, such as stocks, bonds, mutual funds, etc. They can either manage them directly or with the help of a wealth manager. This account is also known as an investment account.

Dormant Account: If this account remains inactive for more than 10 years, then the funds will be transferred to the Swiss state.

How to Open an Account in a Swiss Bank?

To open a Swiss Bank account, one can follow the steps mentioned below:

Type of Account: The first step is to identify the type of account which you want to open. As we have already mentioned, there are various types of accounts, like a personal account, a numbered account, etc.

Selecting the Bank: Various Swiss banks offer the service of opening a bank account, like UBS Group, Julius Baer, etc. One should choose a bank based on the services and charges of the bank.

Arranging Documents: Various types of documents are required to open a Swiss Bank account. The documents include a passport, address proof, source of funds, etc.

Application: Once the documents are arranged successfully, submit an application to open a Swiss bank account along with the supporting documents.

Verification: The Swiss bank officials review the documents and upon successful verification, your account is opened.

Deposit: Once the process is completed, the initial amount can be deposited into the bank account.

The key features of a Swiss Bank Account are as follows:

1. Privacy: An account in a Swiss Bank offers confidentiality and secrecy to its customers.

2. Stability: Switzerland has a history of political and economic stability and has a well-regulated banking system.

3. Investment Options: Swiss Bank offers its customers various investment options along with banking.

4. Minimum Deposit: An account in a Swiss Bank can be opened with a minimum deposit of a few thousand dollars; however, this amount varies across different banks and depends on the type of account you want to open.

There are significant advantages to opening a Swiss bank account:

Privacy: Having a bank account in a Swiss Bank provides a high level of security, as Swiss banks are famous for maintaining strict confidentiality.

Banking Services: Swiss Bank offers a wide range of services to its customers and are known for their personalised banking services.

International Reputation: Switzerland as a country is well known for its regulatory standards and has a well-regulated financial system.

Advisory Services: Swiss Bank also offers tailored investment advisory services, portfolio management services to its customers.

Disadvantages of a Swiss Bank Account

The various disadvantages of having a Swiss Bank account are as follows:

Minimum Balance: One is required to maintain a minimum balance in their Swiss Bank account, which can be between a few thousand dollars to a few million dollars, making it unsuitable for individuals with a low income.

Limited Privacy: Now, with the change in international treaties, the Swiss Banks’ privacy standards have been lowered over time.

Low Interest Rate: Swiss Bank offers a low interest rate on the deposits made by customers.

Annual Maintenance Fee: The bank charges high annual maintenance fees from its customers, whether they use banking facilities or not.

On a concluding note, Swiss Bank accounts offer a high level of privacy to their customers as no one can access the data of their customers. As per the law, it is a criminal offence for banks to disclose their customers’ information. But in the recent past, due to international treaties, the Swiss banks did share the details of the customer with the respective authorities. Hence, the privacy usually associated with having a bank account in a Swiss bank has decreased a little over the past few years. One must consult their tax advisor before opening a Swiss Bank account.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Yes, a Non-Resident Individual can open a Swiss Bank account.

Is it legal to open a Swiss Bank account?

Yes, it is legal to open a Swiss Bank Account; however, it is essential to follow all the regulatory guidelines laid down by the concerned authorities, such as the RBI, etc.

Do I need to travel to Switzerland to get the Swiss Bank account opened?

While initial applications may start online, almost all Swiss banks require in-person or video verification, and extensive documentation for source of funds.

What are the types of Swiss Bank accounts?

The various types of Swiss Bank accounts are as personal or current account, savings account, numbered account, etc.

Does the Swiss Bank pay interest?

Yes, the Swiss bank pays interest. However, the interest rate depends on the type of bank account.

What is the Swiss bank account opening minimum balance?

The Swiss Bank account opening minimum balance differs from bank to bank and it can vary from a few thousand dollars to millions of dollars.

You most likely picture opportunity, wealth, and perhaps even a little thrill when you think of the Indian stock market. While the market has indeed offered investors incredible growth opportunities over the decades, it also has a darker side, marked by major frauds driven by greed, flaws, and a lack of oversight.

This blog will examine five of the largest stock market scams in India, the kind that shook the country’s financial markets, destroyed savings, and significantly altered people’s perspective on investing.

Understanding Stock Market Scams

A stock market scam is an event when someone manipulates the system to make a significant profit, generally at the expense of common investors. It might involve manipulating the financial statements, driving up share prices and selling them off , or using insider information to get an advantage.

Let us move on to the next part: the largest stock market frauds that India has ever witnessed.

List of Major Stock Market Scams – Timeline

SCAM

TIMELINE

The Harshad Mehta Scam

1992

The Ketan Parekh Scam

2001

Satyam Scam

2009

NSEL Scam

2013

Karvy Scam

2019

Overview of Biggest Stock Market Scams

1. The Harshad Mehta Scam

Harshad Mehta was a stock market tycoon in the 1980s. Known as the “Big Bull,” he illegally obtained about ₹3,500 crore from banks using a network of fake bank receipts and fraudulent transactions, and then invested this money to manipulate stock prices. He made huge profits by driving up stock prices with the money, but everything fell apart in 1992.

The Sensex crashed when the scam was exposed, costing thousands of investors their hard-earned money. The shock was so profound that it forever changed the financial landscape of India. Regulations became stricter, and SEBI, the market regulator, gained more authority. You have most likely seen the well-known television show Scam 1992 if this story sounds familiar. Indeed, the series is based on real-life events.

A few years later, Ketan Parekh, a chartered accountant who later became a market manipulator, enters the picture. He was drawn to a variety of small-cap stocks, primarily in the media and technology sectors; these became known as “K-10 stocks.” To increase prices, Ketan borrowed large sums of money from banks and engaged in circular trading, which is the practice of buying and selling among friends to create demand. He made lots of money by selling his shares when prices were at their highest.

However, the bubble popped as usual at a time when India’s technological innovation boom was beginning to gain momentum. The scam, which was valued at over ₹40,000 crore, shook investor confidence and caused another market crash. One more example of how hype of investing in popular stocks that seems too good to be true can backfire.

3. The Satyam Scam

This one focused more on the implications of a company lying about its financial statements than it did on the stock market itself.

The well-known IT company Satyam Computers had been falsifying its financial statements for years. Ramalinga Raju, the founder, acknowledged inflating cash balances and profits by ₹7,000 crore.

The company showed fake numbers for years in an attempt to lure in investors while keeping a high stock price. It is one of the largest corporate scams India had ever witnessed, and once the truth was revealed Satyam’s share price collapsed.

In an instant move, the government brought in Tech Mahindra to take control and cleaned up the mess. India’s corporate governance regulations were also strengthened as a result of this controversy, making it more difficult, though not impossible, to repeat such behaviour.

The National Spot Exchange Limited (NSEL) scam included fraudulent commodity trades and questionable claims of large profits.

NSEL provided a trading platform for commodities such as grains, sugar, and so forth. However, it quickly became apparent that the trades were largely fraudulent and that no actual goods were being used to support them. The brokers misled investors by promising them fixed returns. When it came time for payouts, investors lost both their money and the underlying asset they had invested in.

A total of ₹5,600 crore was lost by about 13,000 investors. The fraud revealed major shortcomings in the regulations governing commodity markets. SEBI and other organisations were forced to intervene and implement more stringent regulations as a result.

5. The Karvy Scam

The reason this scam was so shocking was that Karvy was a well-known name in stock broking. Karvy was using client shares without authorization. They were pledging these shares to raise loans and make investments somewhere else, rather than simply transferring shares to the investor’s demat account. This violated both SEBI’s regulations and fundamental morality, which resulted in a loss of ₹2,000 crore to investors.

In a swift move, SEBI tightened rules on how brokers handle investor funds and shares and prohibited Karvy from onboarding new customers. This scam served as a warning to common investors that not all well-known companies can be blindly trusted.

Evolution of Regulatory Bodies

The evolution of the regulatory environment concerning stock market has been evaluated below:

1. Technology-Driven Monitoring System

These days, stock exchanges and regulators use advanced technology to keep an eye on market activity in real time. Automated systems are in place to identify suspicious trading patterns, such as unusual volumes or a sharp increase in the stock price. These warnings can immediately lead to additional investigations.

For instance, these systems quickly pick up on attempts to manipulate a stock through repeated buy-sell activity or circular trading. Additionally, it is now more difficult to create multiple or fraudulent accounts due to stricter KYC (Know Your Customer) regulations and PAN-based authentication.

2. The Role of Media and Whistleblowers

The media plays an important role in bringing shady practices to light. They helped in identifying warning signs before things got out of control, whether through newspapers, online news sources, or even social media accounts dedicated to financial transparency.

Whistleblowers are employees who disclose unethical activity. Over the years, scams have been exposed because insiders came forward. Now that SEBI has a formal whistleblower policy, informants are protected and more people are encouraged to come forward.

It’s crucial for investors to differentiate fact from fiction because the media occasionally exaggerates news, which can lead to panic or unnecessary speculation.

However, there are still some gaps in the system, even with stricter regulations and technological assistance, and scammers always come up with innovative ways to get around it.

For example:

There are still occasional stories of company officials engaging in insider trading.

It is unlawful for certain smaller, unregistered advisory firms to make promises of guaranteed returns.

Fake websites or fake trading apps imitate authentic ones in order to deceive investors of their money or personal information.

Additionally, there is an increase in services offering stock market tips from claimed experts who use false screenshots and success stories to confuse unaware retail investors.

Conclusion

Even though scams discussed above may appear to be something of the past, fresh versions continue to appear in various forms. The risks haven’t disappeared—they’ve simply changed, whether it’s through sceptical YouTube suggestions, anonymous Telegram groups, or social media hype.

Ultimately, successful investing requires common sense, research, and patience. If something appears unusual, it most likely is. The best course of action is to remain cautious, curious, and never stop learning. It is advised to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

If someone pushes you to “act fast,” hypes up penny stocks, or promises huge profits quickly, it can be considered a risky investment or even fraudulent tip.

How did SEBI respond to these significant frauds?

With more regulations, more intelligent tracking systems, and stricter control of advisors, firms, and brokers, SEBI became more stringent.

Can my demat account be tampered with by my broker?

There are regulations to prevent them from doing so. However, as demonstrated in the Karvy scam, it is still wise to monitor your portfolio on a regular basis.

What should I do if I suspect a scam?

Do not panic. You can speak with your broker’s compliance team or report it to SEBI via their SCORES portal.

We have all heard the saying, “Health is wealth.” However, the cost of medical treatments has risen rapidly in recent years. In such a situation, having a good health insurance plan acts as a financial safety net for families. Just having a policy is not enough — it is important to choose the right policy that truly helps at the time of need.

This blog compares the best health insurance policies in India, so that it is easy to understand which plan is the best among the existing options.

What is Health Insurance?

Health insurance is an insurance coverage that covers the costs associated with health treatment by the insurance company. It includes expenses such as hospitalization, operations, medicines, diagnostic tests, and sometimes even home care. The policyholder pays a fixed premium to keep the policy active and these expenses can be reimbursed through a claim if needed.

In today’s time when treatment of every disease can become a burden on the pocket, health insurance has become an essential safety net. Especially when many insurance companies are now also offering facilities like digital claim process, cashless treatment and customized plans. Along with this, the benefit of tax saving is also available, which makes it a practical and important investment.

Top 10 Best Health Insurance Plans in India (2025)

An overview of the best health insurance plans in India is given below:

1. HDFC ERGO Optima Restore

HDFC ERGO Optima Restore is a popular health insurance plan specially designed for individuals and family floater option. This plan is known for its “Restore Benefit” wherein if the sum insured is exhausted, it is automatically restored without any additional premium. Even in 2025, this plan is very popular among the customers due to its high claim settlement ratio and wide network of hospitals.

Key Features:

Sum Insured: ₹5 lakh to ₹50 lakh

100% restoration after first claim (once per year), with unlimited restore benefit available as optional add-on

Pre-Hospitalization: 60 days

Post-Hospitalization:180 days

No room rent limit (private single AC room covered)

Cashless treatment at 12,000+ hospitals

Lifelong renewability

Key Benefits :

Protection remains even after medical expenses are covered

Coverage for large families in a single policy

Long pre and post hospitalization cover

No room rent cap better treatment facility

Tax benefits available under section 80D

2. Niva Bupa Health Companion

Niva Bupa’s Health Companion plan is a simple yet effective health insurance policy, especially suitable for young couples and nuclear families. Its premium is affordable, and it has many features that make it a useful option for everyday health needs.

Key Features:

Sum Insured: ₹3 lakh to ₹1 crore

Waiting Period or Pre-Existing Disease (PED): 3 years

Pre-Hospitalization: 60 days

Post-Hospitalization: 180 days

No room rent capping

Cashless facility in 10,000+ network hospitals

Direct claim settlement – no TPA involved

Annual health check-up included

Key Benefits :

Complete coverage without any room rent limit

Fast and transparent claim process

Health check-up facility every year

Single policy for all family members

Tax exemption as well as peace of mind

3. Star Health Comprehensive Insurance :

Star Health’s Comprehensive Plan is specially designed for those who have long-term health problems or who are senior citizens. This policy has a low initial waiting period and many critical illnesses are covered from the first year itself. Its acceptance and claim settlement ratio in 2025 has been very strong in the market.

Key Features:

Sum Insured: ₹5 lakh to ₹1 crore

Pre-Hospitalization: 60 days

Post-Hospitalization: 90 days

PED Waiting Period 1 to 2 years (as per insured age)

Daycare treatments: 600+

No capping on disease-wise limits

Lifelong renewability

Free annual health check-up

Key Benefits :

Suitable for senior citizens and critically ill

Easy access to PED coverage

Coverage of multiple day-care treatments

Treatment without sub-limit

Fast and reliable claim settlement

4. Care Health Insurance

This plan from Care Health Insurance (formerly known as Religare) is perfect for those who want a high coverage, flexible and customizable policy for their entire family. This policy in 2025 is quite popular due to its comprehensive coverage and global health option. Add-ons like OPD, maternity and critical illness can also be added to it.

Key Features :

Sum Insured: ₹3 lakh to ₹6 crore

Pre-Hospitalization: 30 days

Post-Hospitalization: 60 days

PED Waiting Period: 4 years

Global treatment add-on available

No upper age limit for entry

21,100+ network hospitals

Annual health check-up included

Key Benefits:

Suitable for large families or those looking for high coverage

Global coverage for advanced treatment

Can buy policy at any age without any age limit

Highest number of network hospitals

Many options to customize as per your need

5. ICICI Lombard Health AdvantEdge

ICICI Lombard’s Health AdvantEdge Plan is a high-end health insurance policy suitable for those looking for global coverage, critical illness protection, and advanced medical facilities. This plan is quite popular in 2025 due to its unlimited sum restore, OPD coverage, and wellness benefits.

Key Features:

Sum Insured: ₹5 lakh to ₹50 lakh

Unlimited Sum Insured Restoration (multiple times/year)

Pre-Hospitalization: 60 days

Post-Hospitalization: 180 days

Global healthcare coverage (optional add-on)

OPD, wellness, mental health coverage included

PED Waiting Period: 2 years

Cashless access to 11,000+ hospitals

Key Benefits:

Perfect for critical illnesses or high-cost treatments

Sum restored even if you make multiple claims in a year

OPD and wellness features care for the whole family

Advanced coverage like mental health and global treatments

Fast and paperless claim process

6. Aditya Birla Activ Health Platinum

Aditya Birla’s Activ Health Platinum plan is a health insurance that is not just limited to treatment, but also promotes fitness and prevention. In 2025, this policy is a better option especially for those who are suffering from chronic conditions like diabetes, high BP or follow a healthy lifestyle and want to get rewards in return.

Key Features:

Sum Insured: ₹2 lakh to ₹2 crore

Chronic Management Program for diabetes, hypertension

HealthReturns reward points for fitness activities

Pre-Hospitalization: 60 days

Post-Hospitalization: 180 days

Daycare procedures: 586+

PED Waiting Period: 2–3 years

Annual health check-up for all members

Key Benefits:

Rewards and premium discounts for staying healthy

Chronic Disease Management Program prevention before treatment

Long pre and post hospitalization cover

A plan designed with both family protection and fitness incentives in mind.

Improvement in lifestyle health along with tax benefits

7. Tata AIG MediCare Premier

Tata AIG MediCare Premier is a comprehensive health insurance plan suitable for those who want treatment coverage not only in India but also abroad. The popularity of this policy in 2025 has increased because it also offers facilities like global coverage, organ donor cover, maternity benefits and air ambulance – that too without any room rent limit.

Key Features:

Sum Insured: ₹5 lakh to ₹3 crore

Global cover for 11 critical illnesses (selected plans)

Pre-Hospitalization: 60 days

Post-Hospitalization: 90 days

Maternity & newborn baby cover included

Organ donor expenses covered

No room rent restriction (private AC room)

PED Waiting Period: 3 years

Cashless facility in 7,200+ network hospitals

Key Benefits:

Treatment facility abroad for 11 critical illnesses

Coverage on pregnancy and childbirth too

No room rent limit no compromise in treatment

Premium facilities like air ambulance and donor cover

Suitable for high net worth individuals and travelers

8. Reliance Health Infinity

Reliance Health Infinity is a modern and advanced health insurance plan that offers all kinds of facilities from OPD to air ambulance and maternity. In 2025, this plan is being liked a lot among those users who want their insurance to be not just limited to hospitalization but also cover day-to-day health expenses.

Key Features:

Sum Insured: ₹5 lakh to ₹5 crore

OPD cover & unlimited doctor consultations (optional)

Air ambulance cover included

Pre-Hospitalization: 60 days

Post-Hospitalization: 90 days

PED Waiting Period: 3 years

Recharge of Sum Insured (up to 5 times/year)

Global emergency cover available (optional)

Wellness benefits & reward points

Key Benefits:

Daily health expenses like OPD and medicines also covered

Facility of Air Ambulance and Emergency Global Coverage

Facility of Sum Insured Recharge – Cover remains even after claim

Rewards on fitness and wellness activities

Ideal plan for high coverage and custom add-on options

9. Bajaj Allianz Health Guard

Bajaj Allianz Health Guard is a simple, affordable and reliable health insurance plan designed to provide financial protection in case of medical emergencies. The plan is available in both individual and family options and is known for its fast claim processing and customer support in 2025.

Key Features:

Sum Insured: ₹1.5 lakh to ₹50 lakh

Pre-Hospitalization: 60 days

Post-Hospitalization: 90 days

PED Waiting Period: 4 years

Daycare procedures: 500+

Free preventive health check-up every 3 years

Ambulance cover up to ₹20,000/year

Maternity and newborn cover (optional)

8,000+ network hospitals

Key Benefits:

Suitable for small families and mid-income group

Preventive health check-ups promote long-term health care.

Fast and paperless claim settlement

Option of good coverage while staying within budget

Optional maternity benefits ideal for those planning a family

10. ManipalCigna ProHealth Prime

ManipalCigna ProHealth Prime is a modern and innovative health insurance plan designed specifically for tech-savvy users and those who like custom features. This policy comes with a “Switch Off” feature, which allows you to save premiums for the period when you are abroad or when you do not need coverage. This plan in 2025 is in the news due to its flexibility and digital friendly features.

Key Features:

Sum Insured: ₹2.5 lakh to ₹1 crore

Switch Off feature can temporarily pause the policy

Unlimited Restoration of Sum Insured

Pre-Hospitalization: 60 days

Post-Hospitalization: 180 days

OPD & non-medical expenses covered (with add-on)

PED Waiting Period: 2 years

Preventive health check-ups included

Key Benefits:

Best option for tech-savvy and traveler customers

Can save premium by “switching off” the coverage when not needed

Provides coverage for OPD and certain non-medical expenses as well.

Unlimited Restoration coverage remains even on repeated claims

Key Factors to Consider Before Buying a Health Insurance Plan

Some of the key factors to consider before buying a Health Insurance plan are listed below:

What should be the sum insured : Considering the rising cost of treatment, coverage of ₹10 lakh or more has become a necessity today. A high sum insured plan is better for people living in big cities and private hospitals.

Cashless hospital network : It is more beneficial to choose a plan that has more network hospitals, especially in your city. This makes the claim process easier and faster.

Claim settlement ratio : The reliability of any health insurance depends on its claim settlement history. Choosing a health insurance plan with a claim settlement ratio of 95% or above is a safe option.

Pre-existing disease cover and waiting period : If you already have a pre-existing disease, check how long the plan requires you to wait before it covers it. A plan with a shorter waiting period is always better.

NCB, Room Rent Limit and Add-on Benefits : No Claim Bonus (NCB) increases the coverage every year. On the other hand, a plan without a room rent limit is more flexible. Also look for add-ons like maternity, OPD and health checkup.

How to Choose the Right Health Insurance Policy for You?

An individual should consider the below mentioned factors to choose the right health insurance policy:

Consider age and family size : If you are under 30 and don’t have any critical illness in your family history, you can start with a basic plan with lower premiums. But families with children or elderly should choose a floater policy with higher coverage and a shorter waiting period.

Use online comparison and IRDAI data: The IRDAI website provides claim settlement ratio and other information for policies. Also, online comparison tools make it easier to take a decision by looking at premiums, benefits and network hospitals together.

Understand add-ons as per your need: If OPD expenses are high, look for OPD cover. Advanced benefits like critical illness or global treatment also depend on the user’s needs.

Common Mistakes to Avoid While Buying Health Insurance

Some of the common mistakes to avoid while buying health insurance are given below:

Ignoring the waiting period : Most people forget that not all diseases are covered immediately after taking the policy. There is usually a waiting period of 2 to 4 years for pre-existing diseases, which is important to understand beforehand.

Buying a policy with low sum insured : Many times people buy policies with very low coverage to save premium. But today, a sum insured of at least ₹10 lakh has become a basic necessity.

Not paying attention to co-pay and sub-limits : In some policies, the policyholder has to pay a part of the hospital bill himself (co-payment). Similarly, there may be sub-limits on room rent or illness expenses, which become a problem later.

Buying only for tax saving : If health insurance is taken only for the tax benefit of Section 80D, then essential coverage and facilities may be missed. Always choose the policy as per your need and health history.

With medical expenses constantly rising, the right health insurance policy is not just a necessity but a wise decision. Every individual has different needs, some need a family floater, while others may need chronic disease cover. Therefore, it is important to keep in mind the features, claim history and add-on benefits while choosing a policy. The right plan not only takes care of the medical expenses but also gives peace of mind. It is wise to plan today so that any health emergency does not become a financial burden tomorrow.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Which is the best health insurance policy in India in 2025?

HDFC ERGO Optima Restore and Niva Bupa Health Companion are the top choices in 2025. However, the ideal plan ultimately depends on an individual’s specific needs and circumstances.

Which medical insurance is best for the family?

Care Health Insurance and Star Health Comprehensive plans are good for families.

What is a good sum insured amount in 2025?

A sum insured of ₹10 lakh or more is considered better in today’s times.

How long is the waiting period for pre-existing diseases?

Most plans have a waiting period of 2 to 4 years.

Can I buy health insurance online in India?

Yes, almost all major insurance companies offer the facility to buy health insurance online.

To choose the right stock in the share market, it is very important to understand the financial health of the company. Two important ratios ROE (Return on Equity) and ROCE (Return on Capital Employed) help a lot in this. Both these metrics show how profitably the company is using its capital.

It is important for today’s investors to know the true meaning of ROCE and ROE in the share market, how they are different and how to use them.

What is ROE?

ROE, i.e. Return on Equity, tells how much profit the company is making from its shareholders’ money. It is calculated using this formula:

Formula : ROE = Net Profit ÷ Shareholders Equity × 100

If a company has a high ROE, it means that it is using its investors’ capital well. Generally, an ROE of 15% or above is considered good. ROE matters more in sectors where capital requirement is less like technology and finance industry.

Example: Suppose a company has a net profit of ₹50 crore and shareholders equity is ₹250 crore,

Then, ROE = (50 ÷ 250) × 100 = 20%

This means the company is earning a profit of ₹20 on every ₹100 of capital invested by shareholders. So, ROE is an important metric, especially when it comes to long term investing.

What is ROCE?

ROCE stands for Return on Capital Employed. ROCE shows how much a company has earned using its total capital resources (i.e. equity + debt). This metric is especially important for capital intensive companies that rely on both debt and shareholder’s equity to earn profits.

Formula : ROCE = (EBIT ÷ Capital Employed) × 100

where, EBIT = Earnings Before Interest and Taxes.

Example : If a company has EBIT of ₹60 crores and total capital of ₹300 crores, then ROCE will be 20%.

ROCE = (60÷300) × 100 = 20%

Meaning, the company is earning ₹20 from every ₹100 of total capital, indicating its strong financial performance.

ROE vs ROCE : Key Differences

Parameter

ROE (Return on Equity)

ROCE (Return on Capital Employed)

Objective

Measures the return generated on shareholders’ equity

Measures the return generated on total capital employed (equity + debt)

Formula

Net Profit ÷ Shareholders’ Equity × 100

EBIT ÷ (Equity + Debt) × 100

Capital Considered

Only shareholders’ equity

Both shareholders’ equity and borrowed capital (debt)

What It Indicates

How efficiently a company generates profit using owners’ funds

How efficiently a company uses all available capital to generate operating profits

Impact of Debt

High debt can artificially inflate ROE

Debt is included, so it reflects a more accurate financial performance

Best for Sectors

Asset-light sectors like IT and Banking

Capital-intensive sectors like Manufacturing, Infrastructure, Oil & Gas

Reliability

Less reliable in highly leveraged companies

More transparent and reliable across different capital structures

Long-Term Perspective

Can sometimes show better short-term returns

Better suited for long-term performance evaluation, especially for companies with debt

Which Ratio Is Better for Investors?

Let us look at practical applications of these ratios.

1. When is ROE more useful?

ROE matters the most when the company has little or no debt, such as in IT or finance companies. In such cases, this ratio shows how well the company is earning returns on its shareholders’ capital.

2. When is ROCE more reliable?

If the company is in a capital-intensive sector, such as manufacturing, power or infrastructure, ROCE gives a more accurate picture. Because this ratio takes into account both debt and equity and tells how much profit the company is earning from the total capital.

3. Impact of debt on both ratios?

Sometimes ROE looks very good, but the reason for that might be the company’s high debt. ROCE clears this confusion because it also includes debt while calculating returns, which gives an idea of the real efficiency.

4. Why look at both together?

If you are thinking of long term investment, then both ROE and ROCE should be looked at together. ROE shows how much profit the shareholders are getting, while ROCE gives an understanding of how efficiently the company has used all its resources.

Practical Example : Comparing Two Companies

Example: Company A vs Company B – Comparison of ROE and ROCE

Financial Data (₹ in Crores)

Parameter

Company A

Company B

Shareholders’ Equity

₹80 Cr

₹140 Cr

Long-Term Debt

₹120 Cr

₹220 Cr

Capital Employed

₹200 Cr

₹360 Cr

Income Statement Highlights (₹ in Crores) :

Income Statement

Company A

Company B

EBIT

₹50 Cr

₹70 Cr

Interest Expense

₹12 Cr

₹30 Cr

PBT

₹38 Cr

₹40 Cr

Tax

₹8 Cr

₹10 Cr

Net Profit

₹30 Cr

₹30 Cr

ROE = (Net Profit ÷ Shareholders’ Equity ) X 100

Company A: ROE = (30 ÷ 80)X 100 = 37.5%

Company B: ROE = (30 ÷ 140) X 100 = 21.4%

ROCE = (EBIT ÷ Capital Employed ) X 100

Company A ROCE = (50 ÷ 200)X 100 = 25%

Company B ROCE = (70 ÷ 360) X 100 = 19.4%

Company A has a total capital of ₹200 crore (equity of ₹80 crore and loan of ₹120 crore). With this capital, the company earned a great return of 37.5% ROE and 25% ROCE.

Company B has a total capital of ₹360 crore, with equity of ₹140 crore and loan of ₹220 crore, but even then its ROE was only 21.4% and ROCE was 19.4%.

This comparison clearly shows that:

Company A earned more returns with less capital – meaning its business is more effective and capital-efficient.

Company B did not show the same efficiency even after investing more money, meaning the use of capital was not that effective.

Bottom line: Just having a lot of capital is not enough; what matters is how wisely that capital is used.

Common Mistakes to Avoid

Some of the common mistakes to avoid while analysing equities using ROCE and ROE are listed below:

Investing just by looking at high ROE : High ROE is not always a good sign. Many times companies take huge loans to show high ROE, which hides the real profitability. That is why it is important to look at ROCE and debt level along with ROE.

Ignoring ROCE, especially in capital-intensive sectors : In companies that invest heavily in assets (such as steel, infrastructure or manufacturing), ROCE matters more. Ignoring it means ignoring the actual efficiency of the company in generating profits.

Looking at data of only one year : Taking a decision by looking at only one year’s ROE or ROCE numbers can be a big mistake. One should always look at trends of 3–5 years to get an idea of consistency and sustainability.

Not comparing with industry average : Every company belongs to a specific industry with some unique characteristics. Technology companies are usually capital-light, while utilities or infrastructure firms require substantial investment. It is important to compare ROE and ROCE with the sector average.

Immediately considering low ROE as negative : Some mature and steady companies may have low ROE, but they give consistent dividends and stable cash flow. In such a situation, do not take investment decisions just by looking at the numbers, also look at the business model and long-term performance.

Conclusion

Both ROCE and ROE show the company’s earning capacity from different perspectives. ROE tells how much return the company is earning from shareholders’ capital, while ROCE shows the returns earned by utilization of the entire capital. It is not right to take a decision by looking at only one ratio. Smart investors identify the real strength of the company by looking at both together. It is essential to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Over the past few quarters, the inflation rate has been consistently declining, due to which there has definitely been relief for the general public, but salaries are stagnant and expenses on luxury items are constantly increasing. At such a time, it is not right to solely depend on one income. This is the reason why people are now looking for side income sources.

In this blog, we will tell you 20 effective and easy ways to earn extra income, which everyone can start along with their job or studies.

Top 20 Side Income Sources

Everyone’s financial objectives and skill sets are different, so here we have divided 20 income ideas into four different categories – so that you can choose the right option for you. Some side income ideas are entirely online, others cater to creative talents, a few involve financial investments, and several can be pursued on weekends or during your free time.

Detailed Breakdown: 20 Side Income Ideas You Can Start Today

A detailed breakdown of 20 side income ideas is given below:

1. Freelancing

In today’s digital era, freelancing is a great way to earn extra money from your skills. If you have any skill like writing, designing, coding or video editing, then you can make good money by working part-time for clients.

How to start: Create a profile on websites like Fiverr, Upwork, Freelancer, prepare a portfolio of past work, and start with small projects.

Who is best for: Students, job professionals, housewives and people who want to use extra time properly.

2. Online Tutoring or Selling Courses

If you have a strong hold on a subject like Maths, English, Coding or Finance then you can teach others online or create a self-paced course.

How to start: Take classes from Zoom or Google Meet, or create and upload your course on platforms like Udemy, Unacademy.

Who is better for: Teachers, students, working professionals and subject experts.

3. Blogging or YouTube Channel

If you like writing or making videos, then by starting a blog or YouTube channel can help you gradually earn income from brand collaborations, ads and affiliates.

How to start: Create blogs on WordPress or start making videos by choosing a niche on YouTube.

Who is better for: Creative thinkers, students, part-time contributors.

4. Affiliate Marketing

Affiliate marketing is a method in which you share the link of a product or service and if someone makes a purchase through your link, you get a commission.

How to start: Join affiliate programs of platforms like Amazon, Flipkart, Zerodha, and share links through blog or social media.

Who is it best for: Bloggers, YouTubers, content creators and digital marketers.

5. Digital Products

If you can create something like resume templates, budgeting sheets, planners or mini eBooks then you can earn passive income without repeated effort.

How to start: Create products with tools like Canva, Notion and upload them on platforms like Gumroad, Payhip.

Who is it best for: Designers, students, writers and creatives.

6. Stock Photography

If you have good photography skills, you can sell your photos on websites like Shutterstock, Adobe Stock and get royalty.

How can you earn: Depends on the quality of the photos and the number of downloads.

How to start: Choose your best quality photos and upload them on stock photo platforms.

Best for: Hobby photographers, travelers and visual content creators.

7. Handmade Crafts / Instagram Store

If you make things like candles, jewelry, art pieces or home decor, you can open your shop on Instagram.

How can you earn: Depends on the uniqueness, pricing and marketing of your products.

How to start: Create a professional page on Instagram, showcase products with good visuals and captions.

Best for: Housewives, artists, students with creative minds.

8. Voiceover or Podcasting

If you have a strong voice and can speak well, voiceover projects or podcasting can also make a strong side income.

How to start: Get a microphone and recording setup, and get started on freelancing sites or platforms like YouTube and Spotify.

Best for: Communicators, speakers, storytellers.

9. Art, Dance or Music Classes

If you are skilled in any art like singing, playing, painting or dancing – then you can generate extra income by taking classes on weekends.

How to start: Add students through word of mouth, local WhatsApp groups or Instagram.

Best for: Artists, hobbyists, homemakers.

10. Making Instagram Reels / YouTube Shorts

Short videos are quite popular these days. You can increase your followers by creating innovative content and can attract brand deals or sponsorships.

How to start: Create content on trending topics, post regularly, and use hashtags correctly.

Who is it best for: Gen-Z, creative people, students, and influencers.

11. Stock Market

Investing in good stocks can provide regular income in the form of dividends over time. Some people also make profits from short-term trading, but it requires proper knowledge and some practice.

Who is best for: Working professionals, students and people interested in finance.

12. Real Estate Rental Income

A stable income source can be created by renting out properties like flat, shop or office. This income can be quite good in metro cities.

How to start: List your house or shop on a platform like MagicBricks, 99acres to contact a good tenant.

Who is best for: Those who have property or space to rent out.

13. Mutual Funds / SIP

Investing a small amount every month through SIP can give good returns in the long term. This income is completely based on the market, but the risk is also balanced.

How to start: Create an account on apps like Groww, Paytm Money or Zerodha Coin and start SIP by selecting a fund.

Who is better for: Employed people, beginners in investing and financial planners.

14. REITs (Real Estate Investment Trusts)

Offers an opportunity to invest in real estate without buying property. By buying units in REITs, one can benefit from both rental income and growth.

How to start: One can invest in popular REITs like Embassy, Mindspace through the stock market.

Who is better for: Mid-term investors and people looking for stable income.

15. Peer-to-Peer Lending (P2P Lending)

One can earn side income by lending money to a needy person through the P2P platform and earning interest on it. This is an alternative investment option.

How to start: Start investing by creating an account on RBI registered platforms like Faircent, LenDenClub.

Who is better for: Investors with low risk tolerance and people looking for passive income.

16. Food Truck or Weekend Cafe Stall

Setting up a food truck or stall on a small scale on weekends can be a good source of income. There is always a demand for street food in metro cities, especially for new and unique food items.

How to start: Decide on a location, get an FSSAI license and start with a small menu.

Best for: Food lovers, chefs, etc.

17. Event Photography or Videography

Photography at events such as weddings, birthdays or corporate meetings is a popular side income source. With a creative vision and a little technical knowledge, this work can go a long way.

How to get started: Start with a camera and basic gear, build a client base through Instagram or local networking.

Best for: Photography enthusiasts, students, and creative people.

18. Renting out a car, room or equipment

Many times, there are resources lying around that are not being used like an extra room, bike or camera. You can rent them out to generate regular income.

How to start: List on sites like Zoomcar, Drivezy, Airbnb or Rentomojo.

Best for: Working professionals, travellers and those looking for passive income.

19. Becoming a delivery partner (Zomato, Swiggy, Dunzo)

A stable part-time income can be generated by taking out a few hours from your daily schedule for a delivery job. There is always a demand for food and package delivery in cities.

How to get started: Register on the app, submit bike photographs and documents and choose the shift.

Best for: Students, part-time workers and people with extra time.

20. Fitness trainer or yoga instructor

The passion for fitness is not just limited to health, it can also become a great source of income. Local classes, park sessions or online training can generate good income.

How to start: Start with local parks, societies or online classes.

Best for: Fitness lovers, health experts and certified instructors.

You can decide the right side income for yourself by considering the following points:

Calculate time carefully : Every work requires time, some ideas require a little time every day, like blogging, while some can be done even on weekends, like classes or setting up stalls.

Identify your skills and interests : The work you are comfortable with can turn into side income. Skills like designing, writing, video editing are useful in freelancing, while creative people can create content.

Understand the budget and risk : Some ideas require some investment to start, like the food business or stock market. On the other hand, online tutoring or work on social media can be started without money.

Start Small: Start on a small scale and gradually build a stable client base while learning.

Work continuously : Patience and consistency are what turns your extra efforts into success.

Conclusion

Apart from a full-time job, it is now both necessary and wise to adopt a way to earn side income. Amidst the changing economic situation, rising inflation and future uncertainty, an additional source of income not only provides financial security but also gives a feeling of self-reliance. In today’s era, every skill and every hobby has value – you just need to start in the right direction. Only those who use their time properly and constantly learn something new are able to gradually create a strong second income. Small steps, right thinking and a little patience together can bring about a big change.

Frequently Asked Questions (FAQs)

What is the best side income source in India?

Freelancing, online teaching and content creation are good options.

Can I earn extra income while doing a full-time job?

Yes, many ideas discussed above can be done on weekends or in free time.

Do I need money to start a side income?

Some of the ideas discussed above can be started without any investment.

How much time does a side income source take?

One can start by working 1–2 hours daily to earn a side income.

Is it legal to have side income in India?

Yes, as long as the income is earned in the right way and taxes are paid.

Rakesh Jhunjhunwala, one of India’s most successful and famous investors, is also known as the “Big Bull of India”. Coming from a simple family and starting with just ₹ 5,000, this chartered accountant made his mark in the stock market.

In this blog, we will know how Rakesh Jhunjhunwala made a fortune worth crores, interesting information related to his net worth, and educational background.

Rakesh Jhunjhunwala was born in a Marwari family, where the concepts of business and investment were part of everyday conversation since childhood. His father was an officer in the Income Tax Department and was himself interested in the stock market. From here, Rakesh ji’s interest also grew towards the market. From childhood, he used to hear his father talking about shares and gradually he started reading share prices and names of companies in newspapers.

He graduated in commerce from Sydenham College, Mumbai. After this, he started studying chartered accountancy and in 1985 he became a qualified CA. During his studies, he understood that he wanted to make a career in the stock market.

Soon after becoming a CA, he entered the stock market with a capital of ₹5,000. At that time he did not have any big resources, but he had confidence, knowledge of doing research and courage to take risks. This quality makes him different from millions of investors. He understood the market not just as a source of income but as an art and a science – and this thinking earned him the title of “Big Bull of India”.

Lets look at the journey of Rakesh Jhunjhnwala in the stock market over the years:

Started Investment Journey with just ₹5,000 : Rakesh Jhunjhunwala entered the stock market in 1985, when he started his investment with just ₹5,000. At that time, the BSE Sensex was only around 150. This was the time when common people considered the stock market as gambling, but Rakesh ji saw it as an opportunity.

Initial Loans from brother’s clients :His conviction and dedication impressed his brother’s clients, who trusted him with ₹2.5 lakh to invest. With this capital, he expanded his initial investment a little and focused on investing in some good stocks.

First big profit : His first notable profit came in 1986, not long after entering the market. At that time, he bought 5,000 shares of Tata Tea at a price of ₹43. In just a few months, this stock reached ₹ 143. That is, his investment grew to almost three times his initial stake. This success was a turning point for him, which convinced him that with research, patience and time, big money can be earned from the stock market.

Gradually built a strong portfolio : After Tata Tea, he identified good companies one after the other and invested in them for the long term. Companies like Sesa Goa, Lupin, Titan, Crisil became part of his portfolio. Rakesh Jhunjhunwala believed that if the fundamentals of the company are strong, then it is beneficial to invest in it for years.

Investment thinking : He did not just buy shares – he understood the company. He always believed in quality business and did not run after popular stocks. He held his investments for the long term, due to which his winners yielded multibagger returns over time.

He always believed in the principle: “Buy right, sit tight.” i.e., invest in the right company and then stay patient.

Rakesh Jhunjhunwala’s Net Worth Over Time

Net Worth Timeline

Year

Estimated Net Worth

Sources and descriptions

1985 (beginning)

₹5,000

Started investing with his own savings

1990

Approx. ₹25 lakhs

Early investment in stocks like Tata Tea, Sesa Goa yielded profits

2002

₹250 crores +

Stocks like Titan, Praj Industries gave tremendous returns

2013

$1.3 Billion (~₹9,000 Cr)

Forbes India Billionaires List

2018

$3 Billion (~₹21,000 Cr)

Growth of Multibagger Stocks

August 2022 (Death)

$5.8 Billion (~₹46,000 Cr)

His net worth before death according to Forbes and ET

January 2025

₹50,310 crore

Based on listed portfolio of RARE Enterprises

March 2025

₹64,552.8 crore

Trendlyne data Public holdings of 27 stocks

Rakesh Jhunjhunwala Per Day Income & Portfolio Strategy

Rakesh Jhunjhunwala’s net worth was around ₹46,000 crores at the time of his death in 2022, which has increased to more than ₹64,500 crores by 2025. The value of his portfolio changes drastically every day due to the market fluctuations. His income cannot be compared to a salary with a fixed amount, but it was completely based on the performance of his invested stocks and dividends received.

Features of Portfolio Strategy : His investment strategy was clear; he held strong companies for the long term and did not believe in frequent trades. He believed that the most effective way to earn profits was to identify quality companies and stay invested for the long term.

Key points of his strategy:

Investment in companies with strong fundamentals

Focus on the quality of management

Clear thinking of long-term growth

Limited portfolio rebalancing

Beyond Stock Market: Akasa Air & Private Ventures

Rakesh Jhunjhunwala wasn’t just a stock market investor he was also a visionary businessman who contributed to India’s economy.

Co‑Founder of Akasa Air : He joined Akasa Air in July 2021 and invested $35 million in the initial round, giving him a nearly 40% stake. He increased his investment to bring his total stake to 46%, making him Akasa Air’s largest stakeholder. Today, Akasa Air’s fleet has expanded to 27 aircraft and offers services across 28 destinations.

Boardrooms & Mentorship : He served on the boards of several companies: places like Aptech, Hungama Digital Media, Praj Industries, Nagarjuna Construction Company, Prime Focus and Geojit Financial Services, etc. Jhunjhunwala wasn’t just an investor; he was a guide to the people trying to establish their businesses.

India‑First Growth Vision : He believed that India’s growth story had just begun. Whether it was the aviation sector or technology, he looked at everything as an opportunity. Akasa Air exemplifies this vision as an airline that not only offers top-notch services but also wants to contribute to India’s economic growth.

Investment Philosophy & Life Lessons

Rakesh Jhunjhnwala’s investment philosophy and life lessons can be summarized in the following points:

Do thorough research and analysis : Rakesh Jhunjhunwala believed that no investment in the stock market should be made without research. He used to invest only after doing thorough research on the fundamentals, management quality and future growth of the company.

Diversification is essential: He always emphasized on diversifying portfolios. He considered it risky to invest all the money in a single sector or stock. He believed that investing in different sectors reduces the risk and ensures stability in the long term.

Buy Right, Sit Tight : His most famous thought was – “Buy Right, Sit Tight”. But this did not mean just buying shares and sitting tight. He used to say that the mark of a real investor is to identify a strong company and trust it for a long time.

Long term vision : Jhunjhunwala believed that the market is not always stable. There will be periods of significant fluctuations, but a wise investor is the one who does not panic at that time; rather trusts his rationale behind investments.

He did not consider investment as just a means of earning money. According to him, every loss is a lesson and every investment is a learning. His mantra was trust knowledge and analysis, not tips.

The news of the sudden demise of Rakesh Jhunjhunwala on 14 August 2022 left the entire nation stunned. On his demise, everyone from common investors to veteran business leaders paid tribute to him on social media.

After him, his wife Rekha Jhunjhunwala carried forward his investment legacy. The companies included in his portfolio are still standing strong, and the firm RARE Enterprises founded by him is active in the investment world.

Rakesh ji inspired millions to start their investment journey with his thoughts and experiences. Even today, his words “Be patient, keep learning, do research” guide the new generation of investors.

Conclusion

Rakesh Jhunjhunwala’s story tells us that to be successful in the stock market, it is not necessary to start with a huge amount- you just need to have knowledge and the courage to hold your investments during volatile market conditions. The knowledge he has left behind through his decisions remains an inspiration for every investor even today. His journey proves that with discipline, knowledge, and patience, even modest beginnings can lead to extraordinary success in the stock market.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

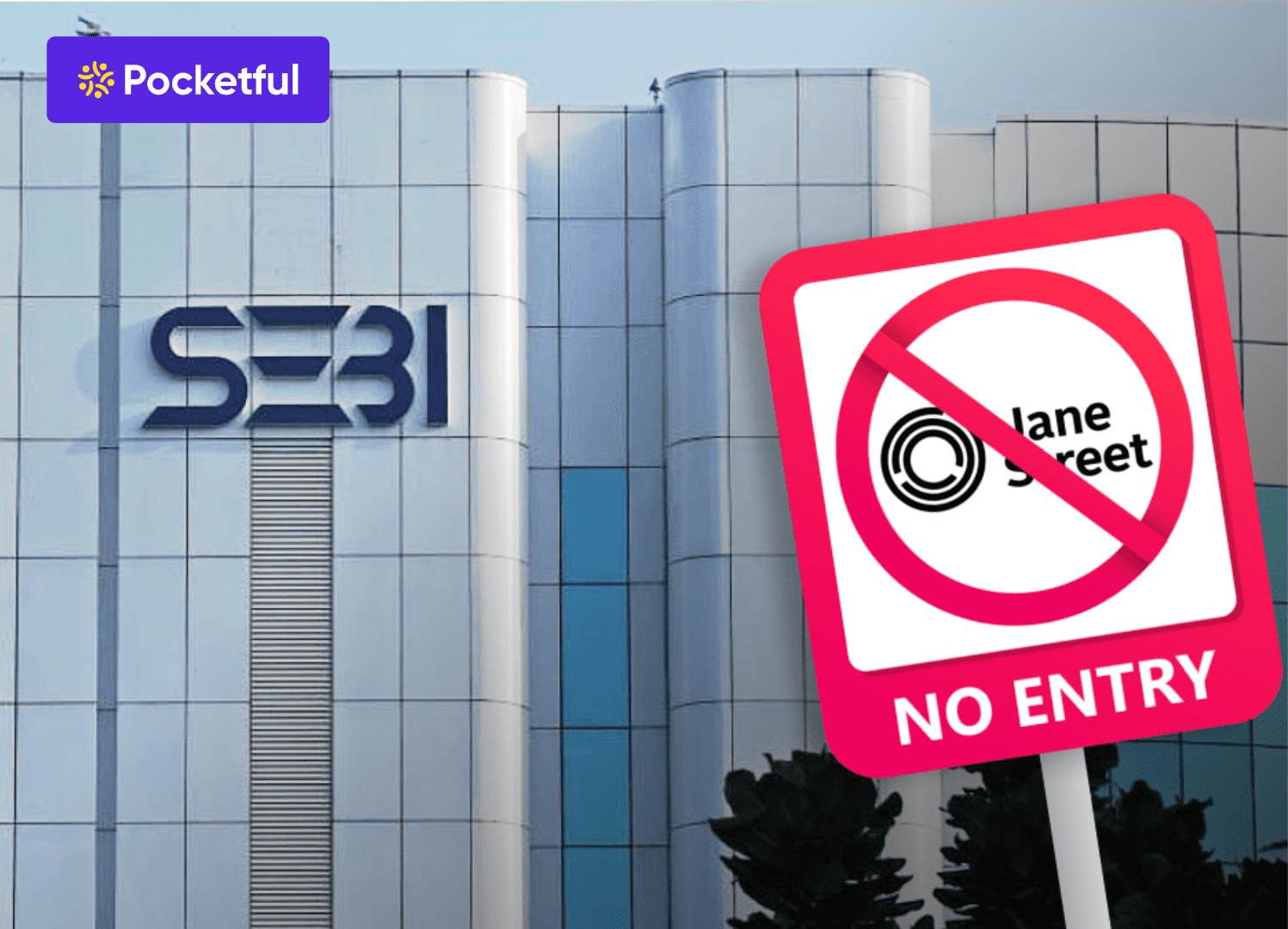

Market regulator SEBI has taken strict action against US trading firm Jane Street and banned it from the Indian securities market. Investigation revealed that the firm made unfair profits of about ₹4,843 crores by misusing algorithmic trading on the expiry-day of Nifty and Bank Nifty derivative contracts. This decision has sparked a serious debate on the transparency and credibility of algo trading and quant trading firms in India. This strict action by SEBI shows that bypassing the rules by using automated trading models will no longer be tolerated no matter how influential the firm is.

SEBI’s Charges Explained: Why Jane Street Was Barred?

SEBI has found Jane Street and its affiliates of violating rules of the Indian derivatives market due to deliberate manipulation of index prices. These activities were carried out continuously from 1 January 2023 to 31 March 2025, with additional violations noted in May 2025.

Allegation 1: Intra-Day Index Manipulation

Jane Street made heavy purchases in stocks like Bank Nifty in the morning on expiry days and sold them at the end of the day, creating volatility in the market. They benefited from this in option trading. On January 17, 2024, ₹4,370 crore worth of Bank Nifty futures and its constituent stocks were purchased in the morning, and by the end of the day, the Bank Nifty was brought down by heavy selling worth ₹5,372 crores, which earned them profits worth crores from their position in Bank Nifty index options.

Allegation 2: Marking the Close Strategy

According to SEBI, Jane Street artificially moved the index up and down in the last 30 minutes of the day on several occasions. The purpose of this was to influence the closing value of the index at the time of expiry, which directly benefited them in option trades.

What did the SEBI report say?

SEBI found in its investigation that these trading patterns had no economic basis. The report clearly stated:

“This entire strategy was pre-planned so that the Jane Street Group could make profits and mislead the market.”

For how long did all this last?

This suspicious trading was done from January 2023 to May 2025. SEBI has described it as a pre-planned and malicious scheme, in which crores of rupees were earned by ignoring the rules.

How Jane Street Made the Profits?

Jane Street and its affiliates followed certain trading patterns in Nifty and Bank Nifty index derivatives that were against market rules. According to SEBI’s investigation:

Repetitive Pattern :

SEBI tracked 15 expiry days in which Jane Street first bought Index Futures in large quantities in the morning.

At the end of the day, when the market was about to close, they sold the same futures — causing artificial volatility in the market.

Profit from Options :

By moving the index up or down around the market close on expiry day, they profited from their positions in call or put options.

The prices of these options change significantly at closing, giving Jane Street a huge profit.

SEBI Recovery:

SEBI said that Jane Street Group made an unfair profit of a total of ₹4,843 crore.

This amount is now being recovered and forfeited under the interim order.

What It Means for Jane Street in India?

SEBI has issued a provisional order against Jane Street India and its associated companies –

Ban on trading : SEBI has prohibited Jane Street India from trading, dealing or accessing the Indian securities market. That is, at present they cannot engage in any kind of stock market activity.

Account freezing : SEBI has directed Jane Street’s and its associates to deposit unlawful gains of ₹4,843 crore in an escrow account.

Opportunity to respond in 21 days : Jane Street has been given 21 days in which it can present its side or challenge SEBI’s order.

Final order possible : SEBI has clarified that this order is provisional, but after the investigation is completed, a heavy fine, permanent ban or other strict action is also possible in the final order.

What This Means for Indian Brokers and Traders?

SEBI’s action on Jane Street is now having ripple effects on India’s broking system and small investors, signalling tighter monitoring for the industry.

Rethinking Expiry-Day Trading Risks : Brokers will now have to re-look at high-volume and high-loss-probability trades that take place on the expiry day. This has become a sensitive area after SEBI’s investigation indicated expiry-day manipulation.

Risk Management rules will be more stringent : After this action by SEBI, brokerage houses will have to update their risk management policies. Especially advanced checks and controls will be necessary on trades that cause large price fluctuations.

Pressure will increase on Algo Trading Firms : The filters and trading rules used for algo trading need to be further refined. It will be necessary to ensure that such algorithms do not manipulate the market.

Disclosure required for high-volume clients : Brokers will have to give proper risk disclosures to clients who repeatedly make high-volume trades on expiry-day. SEBI is emphasizing transparency and client awareness.

Surveillance systems become more important : The time has come for all brokers to adopt advanced surveillance tools so that suspicious trading patterns can be caught in real-time. SEBI is now adopting a proactive approach in such cases.

How does it impact Indian markets?

SEBI’s decision to suspend Jane Street’s access is being seen as a strong regulatory action in the Indian stock market. This move makes it clear that the regulator will now keep a strict watch on the activities of algo and quant trading firms, especially when it comes to unfair or manipulative trading patterns.

Jane Street, which earned more than $2.3 billion in net revenue from Indian equity derivatives in 2024 alone, is now directly facing a major setback. Not only their participation in Indian financial markets but their credibility and long-built business network has also been affected.

Conclusion

SEBI’s recent action has made it clear that regulations regarding algorithmic and quant trading in the Indian market are going to become even stricter. The barring of a big global firm like Jane Street can not only shake the trading ecosystem, but can also force all foreign and domestic institutions to rethink compliance and legality of their trading activities. This step can prove to be a turning point for ensuring market transparency and fairness.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Most people in India use debit and credit cards these days, but very few know what the name written on their cards like RuPay or Visa means and how they are different from each other. Choosing the right card network is very important as it affects many aspects like security of transactions, convenience and international usage.

This blog explains in detail what is the difference between RuPay and Visa, which card is better for whom, keeping in mind the fees, benefits, acceptance, and global usage of both.

What is a RuPay Card?

RuPay card is India’s own payment card network, which was launched by NPCI (National Payments Corporation of India) in the year 2012. Its purpose was that India does not have to depend on foreign networks like Visa and MasterCard and people can get a cheap, safe and suitable option to make domestic transactions.

Fast and cheap in domestic transactions : Transactions made through RuPay card are processed in India itself, which makes the processing speed fast and the transaction charges are also very low. This is the reason why this card has become very popular especially in small towns and rural areas. Government banks and private banks issue it at a low cost, due to which it is used extensively in Jan Dhan accounts, PM Kisan, and other government schemes.

Types of RuPay Cards

There are many types of cards available under the RuPay network:

RuPay Debit Card : Money is debited directly from the bank account

RuPay Credit Card : For limit based spending

RuPay Prepaid Card : Use after preloading money

RuPay Global Card : For international use

Global expansion of RuPay : In recent years, RuPay has also expanded internationally. RuPay Global cards are accepted at over 42.4 million POS locations and over 1.90 million ATM locations in 185+ countries and territories worldwide. This means that now it is possible to do shopping, ATM withdrawal and online transactions abroad with a RuPay card.

Important role in government schemes : RuPay card is being used in many schemes of the Government of India such as:

Pradhan Mantri Jan Dhan Yojana

PM Kisan Samman Nidhi Yojana

E-Shram Card

Ayushman Bharat Yojana

In these schemes, money is sent directly to the accounts of the beneficiaries through Direct Benefit Transfer (DBT), and in most cases a RuPay card is given.

Visa card is the world’s largest and oldest international payment network, which started in America in 1958. Visa is not a card issued by any bank, but it is a network provider, which allows banks around the world to issue cards. It is used in the form of debit, credit and prepaid cards.

Globally accepted and user-friendly : The biggest strength of Visa card is its global acceptance. Cards on the Visa network are accepted in more than 200 countries, whether it is withdrawing cash from an ATM, shopping at a POS machine or making online payment from international websites. Apart from this, many Visa cards also offer premium features like lounge access, global offers, travel insurance and cashback.

Types of Visa Cards

Banks issue three types of cards on the Visa network:

Visa Debit Card: Directly linked to the bank account

Visa Credit Card : For limit based purchases

Visa Prepaid Card: Used by loading a fixed amount

Advanced in security and technology : Visa cards have security technology like EMV chip, 2-factor authentication, and fraud detection system, which makes transactions secure. Visa’s network called VisaNet is one of the fastest and secure payment processing systems in the world.

Key Differences Between RuPay and Visa Card

Parameters

RuPay Card

Visa Card

Origin

Launched in 2012 by NPCI, supported by the Government of India

Founded by US-based Visa Inc., started in 1958

Transaction Processing

All transactions processed within India, making it faster, cheaper, and more secure.

International processing involves currency conversion and cross-border fees, making it more expensive for foreign transactions

International Acceptance

Accepted in over 185 countries with over 42.4 million POS locations and over 1.90 million ATM locations.

Widely accepted in approximately 195 countries globally directly through Visa’s global network

Fees & Charges

Minimal charges for domestic use; slightly higher for international usage

Higher fees for international transactions due to currency conversion and network charges

Rewards & Benefits

Limited offers; government-issued cards typically don’t offer reward programs

Attractive rewards, cashback, travel benefits, and insurance on many cards

Usage in Government Schemes

Widely used in schemes like Jan Dhan, PM-Kisan, e-Shram, and other DBT programs

Not used directly in government schemes; popular among private users and international travelers

Usage Scope

Ideal for domestic payments, subsidies, ATM withdrawals, and local POS transactions

Suitable for both domestic and international payments

Card Issuance Cost

Low-cost issuance for banks minimal interchange and network fees

Expensive for banks as higher interchange and processing costs

The use of each card depends on the needs – some need the card only for local payments, while others need it for international shopping or travel. Both RuPay and Visa have their own benefits, only the way of using them is different.

Where you’re using it

Which card fits best

Daily expenses like ATM withdrawals or paying at local shops

RuPay

Receiving money from government schemes like Jan Dhan or PM-Kisan

RuPay

Making payments while travelling abroad at ATMs or swipe machines

Visa

Shopping on international websites or global online platforms

Visa

If you’re looking for extras rewards like travel benefits, insurance, or cashback

Visa

Want lower charges and faster domestic processing

RuPay

RuPay is a network that has been created in India, for the people of India. This card is generally better for local transactions, government payments and low charge transactions. Its biggest advantage is that its entire process takes place in India – which makes the transactions fast and secure.

On the other hand, the network of Visa cards is spread all over the world. If someone uses it more for making payments on international websites, or while traveling abroad, then Visa becomes a more suitable option. It also offers some advanced features, like airport lounge access or global insurance cover.

Pros and Cons of RuPay Card

Pros :

All transactions are processed in India, which leads to faster speeds and better data security.

Card issuance is cost effective for banks, which allows users to avail it at low or no charges.

Designed for domestic use easily accessible on ATMs, UPI and POS.

Acceptable and compatible with government schemes like Jan Dhan, DBT schemes etc.

Cons :

Limited acceptance for international transactions; not supported by all countries and websites.

Less or no extra features like rewards, cashback, travel benefits.

The international card variant (RuPay Global) still has a limited network.

Pros and Cons of Visa Card

Pros :

Visa is an international payment network that is accepted in 200+ countries across the world.

Works seamlessly with international websites and travel payments.

Most cards offer features like reward points, cashback, and discount offers.

Some premium Visa cards also come with advanced benefits like airport lounge access, travel insurance, and foreign transaction security.

Visa’s fraud detection technology and secure payment system works at international standards.

Cons :

International processing may lead to additional charges on transactions, such as foreign transaction fees.

For those who use their card only in India, a Visa card is not a must it may seem over featured or overserved.

Some basic Visa cards do not offer special offers or features, which may reduce value for money.

Choosing between Visa and RuPay depends on your needs. RuPay is ideal for affordable, fast, and secure domestic transactions. Its lower fees and strong integration with government schemes make it ideal for local use. Visa suits international travelers and online shoppers, offering wider acceptance and premium perks like rewards and insurance. Assess your spending habits and transaction locations to pick the card that best fits your lifestyle and financial goals.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Term insurance has become a necessity in 2025, especially in uncertain financial times where long-term security has become increasingly important. It is an insurance option that provides great financial security to the family’s future goals at a low cost. Today’s insurance companies are providing better claim processes, useful rider benefits and customized plans according to personal needs. This article includes 10 such trusted and popular best term insurance plans, which are becoming the first choice of people this year.

What is Term Insurance and Why is it Important?

Term insurance is a life insurance plan that provides coverage for a fixed period. During this period, if the insured person dies, the nominee gets the entire sum assured. But if the insured person survives till the completion of the policy term, then no amount is received. This is why it is called a “pure protection plan”.

In 2025, term insurance has become smarter and more personalized than before. Insurance companies are now also offering features like flexible plans, digital claim process and health-based premiums. This plan provides high coverage at a low premium, making it one of the most economical ways to ensure your family’s financial security.

Top 10 Best Term Insurance Plans in India

S.No

Term Insurance Plan

Claim Ratio (2023–24 Avg.)

Max Cover Age

Key Riders Available

1

LIC Tech Term Plan

98.5%

80 years

Accidental Death

2

HDFC Life Click 2 Protect Super

99.5%

85 years

Critical Illness, Accidental Death

3

Max Life Smart Secure Plus

99.5%

85 years

Critical Illness, Accidental Death, Waiver of Premium

4

ICICI Pru iProtect Smart

97.9%

85 years

Critical Illness, Accidental Death, Waiver of Premium

5

Tata AIA Sampoorna Raksha Supreme

99.0%

100 years

Accidental Death, Critical Illness

6

SBI Life eShield Next

97.6%

85 years

Critical Illness, Accidental Death

7

Bajaj Allianz Smart Protect Goal

99.1%

99 years

Critical Illness, Waiver of Premium

8

Aditya Birla DigiShield Plan

98.7%

85 years

Terminal Illness

9

PNB MetLife Mera Term Plan Plus

98.5%

99 years

Critical Illness, Accidental Death

10

Kotak Life e-Term Plan

98.6%

75 years

Accidental Death

Top 10 Best Term Insurance In India: Overview

An overview of the top 10 term insurance plans in India are mentioned below:

1. LIC Tech Term Plan

LIC Tech Term Plan is a pure protection plan which is available online only. It does not provide maturity benefit, but in case of death, the nominee is given the entire sum assured. Low premium, accidental rider option and the trust of LIC make it a reliable option.

Key Features

Plan can be purchased online only (no agent required)

Different premium rates for smokers and non-smokers

Guaranteed sum assured in case of death

Option to return policy within 30 days

Lower premium than other offline LIC plans

NRIs can also buy (medical test has to be done in India)

Benefits

Death Benefit: In case of death during the policy term, the nominee gets a fixed amount