Military personnel encounter specific financial challenges due to frequent deployments related to their service. Military members generally receive a stable income and benefits such as housing allowances, retirement plans, and education plans. With disciplined planning, these resources can help build significant wealth over time. Creating strong strategies for building and maintaining wealth leads to financial stability and long-term success.

In this blog, we will discuss the military wealth management techniques tailored to manage their specific investment needs.

Financial Planning: The First Step to Wealth Management

A strong financial plan is essential for managing wealth. Military personnel generally receive stable salaries, allowances and pensions. To make the most of these resources, they should focus on the following points:

1. Analyse Your Financial Goals: Evaluate your financial goals by identifying short-term and long-term objectives, such as buying a home, supporting your children’s education, or planning for retirement.

2. Budget Effectively: Monitor your income and regular spending habits for effective budgeting. Allocate funds for essential expenses, savings and investments.

3. Building Emergency Fund: Create an emergency fund by saving three to six months’ worth of living expenses to prepare for unexpected situations.

Using Government Benefits and Schemes

Indian military personnel can access several government schemes that provide financial benefits.

1. Defence Salary Package (DSP): It is a special salary account available for Indian Army, Navy, and Air Force Personnel, as well as members of Assam Rifles, Rashtriya Rifles, and GREF. These accounts are offered by banks like SBI and ICICI, with features of zero balance, higher withdrawal limits, and extra insurance coverage.

2. Agnipath Scheme: This scheme is an initiative by the Government that affects new recruits in the military. It is important to learn how this scheme affects their earnings and financial planning for the future. Under this scheme, recruits, called Agniveers, will receive a fixed salary for a four-year service period, with the income increasing gradually throughout their tenure, but an important point to consider is that only 25% of the Agniveers will be retained in the armed forces after the initial four years significantly affecting their long-term financial planning as they will need to find new employment opportunities post-service and use the accumulated service fund to secure their financial future.

3. Pension Plans: These plans are important aspects of financial planning for the future, so it is necessary to make sure that as a military personnel, you are well equipped with various components such as pension entitlements, gratuities, and provident funds. Understanding these elements will help you explore the different options available and ensure that you are adequately prepared for the post-retirement income. By doing this, you can create a stable financial foundation for the years after you stop working.

4. Insurance: Look into affordable group insurance offered by the Armed Forces, as it usually provides better coverage at a lower cost than individual policies. These group plans provide service members and their families with essential health benefits, life insurance and financial protection. You can achieve peace of mind without overspending. It is a practical way to focus on your well-being and that of your loved ones while meeting your commitments.

Wise investing is essential for increasing wealth over time. Below are some strategies designed for military personnel in India:

Public Provident Fund: PPF is a government-backed, risk-free savings option that provides tax benefits and returns.

National Pensions Scheme: The NPS is a great way to plan your retirement, offering market-linked returns and extra tax benefits.

Mutual Funds: For those willing to take calculated risks, mutual funds provide diversification and possibly higher returns than traditional savings methods. The investment method can be SIP, lumpsum, or both, whichever best suits the individual.

Real Estate: You can also explore the opportunity to invest in properties located in areas poised for growth, particularly during periods of market stability.

Gold: Though it is a traditional asset, gold continues to be a dependable investment for protecting against inflation and increasing portfolio diversification.

Tax Planning: Effective tax planning is essential for maximising your income. Military personnel can lower their tax obligations by taking advantage of the various exemptions and deductions available to them.

Deductions under various Sections

Section 80(c) – Investments: Deduction up to INR 1,50,000 per year in PPF, NSC, ELSS, LIC premium, and principal repayment.

Section 80(d) – Health Insurance: Deduction up to INR 25,000 for health insurance premiums (INR 50,000 for senior citizens). Armed Forces personnel can deduct private insurance costs if they do not use military healthcare facilities.

Section 80(G) – Donations: Donations to approved charitable organisations like the Prime Minister’s Relief Fund are tax-deductible.

Section 24(B) – Home Loan Interest: Interest on home loans is deductible up to INR 2,00,000 for self-occupied properties.

Tax-Free Gratuity: Gratuity received on retirement or resignation is exempt under section 10(10) up to the prescribed limit.

Suggestions for Optimised Tax Planning

Invest in tax-saving instruments like ELSS early for maximum benefits.

Keep proof of expenses to claim allowances and exemptions accurately.

Consult a tax advisor who specialises in military tax-saving techniques.

Insurance

Insurance Planning is crucial for Indian military personnel because of the high risks they face and the specific financial needs of their families. Here is a detailed analysis of an effective insurance plan for military personnel.

1. Life Insurance: Life Insurance offers financial protection to a family in the event of an unexpected death. Military personnel should consider the following points.

Armed Forces Insurance Plans: Army Group Insurance Fund (AGIF), Navy Group Insurance Scheme (NGIS), and Air Force Group Insurance Scheme (AFGIS) are government-backed schemes with low premiums. Benefits include coverage during service, savings, and post-retirement support. Coverage ranges from INR 50 lakh to INR 75 lakh or more, depending on the plan.

Term Insurance: Many private insurers, including LIC and others, provide cost-effective term insurance policies. Select policies that extend throughout the service period and beyond.

2. Health Insurance: While the military offers healthcare at its hospitals, extra coverage can help, especially for family members or after retirement.

3. Armed Forces Coverage: ECHS (Ex-Servicemen Contributory Health Scheme) provides post-retirement health coverage for retired personnel and their dependents.

Retirement Planning

Retirement planning is crucial for military personnel in India because their early retirement requires long-term financial stability. Below is a detailed analysis of effective retirement planning specially designed for armed forces personnel;

1. Pension: Retired Military Personnel receive regular monthly pensions based on rank and years of service, including inflation-linked adjustments via Dearness Relief (DR). Additionally, the military person can receive a lump sum advance of up to 50% of his pension amount, which will be deducted from his monthly pension payments over the next 15 years.

2. Gratuity: Retirement Gratuity and Death-cum Retirement Gratuity are available for eligible military personnel. An officer receives a pension of one-fourth of their monthly salary for each completed six-month qualifying service up to a maximum of 16.5 times their monthly salary.

3. Provident Fund: DSOPF or Defence Service Officers Provident Fund contributions accumulated during service are paid on retirement, and withdrawals are tax-free.

Furthermore, numerous investment options are also available for Post-retirement Income, such as the Senior Citizens Savings Scheme (SCSS), Pradhan Mantri Vaya Vandana Yojana, FDs, etc.

Conclusion

Wealth management for military personnel involves strategic planning, disciplined investments, and active asset management, not just saving money. Armed forces members can secure their financial future by using government benefits, investing wisely, planning for taxes and retirement and obtaining insurance. Furthermore, a financial advisor should be consulted before making investment decisions.

Frequently Asked Questions (FAQs)

Is the stock market a good option for military personnel?

Yes, it is a good option, but start with diversified mutual funds or index funds if you are a beginner and ensure investments align with your risk tolerance.

How can military personnel protect their assets during deployments?

Establish power of attorney for trusted individuals to ensure proper nominations and review insurance policies.

Are military allowances taxable?

Some allowances, such as field area and high altitude allowances, are exempt from tax under Section 10.

How frequently should military personnel review their wealth management plan?

Military personnel should review their finances at least annually or after major life events such as transfers, promotions or retirement.

What budgeting tips are useful for military families?

Track income and expenses, focus on emergency funds, and allocate allowances effectively using methods like the 50/30/20 rule, i.e., 50% for needs, 30% for wants and 20% for savings and investments.

Republic Day marks the commemoration of the day that India adopted its Constitution in 1950 and established itself as a sovereign, democratic republic. This day not only symbolizes India’s democratic spirit but also reflects the nation’s strides toward self-reliance and progress, especially in the field of defense. The Indian Republic Day is celebrated on January 26 every year, and it features the country’s defense capabilities and cultural diversity.

In this blog, we will give you information about the Republic Day of India, the growth of the Indian defense sector, major achievements and the future of the Indian defense sector.

Why is Republic Day Special?

January 26 is an important date in Indian history because on this day in 1930, the Indian National Congress declared Purna Swaraj or total independence from British rule, at its Lahore session. Two decades later, this date was chosen to enforce the Constitution of India that marked the establishment of a republic nation.

Republic Day reminds people of the sacrifices made by numerous people who fought for freedom and worked hard to build a strong and united nation. It also features events showcasing India’s cultural diversity along with the recent developments in the Indian defense sector.

Growth of India’s Defense Sector

Post-independence, India has made enormous progress in the defense sector. With the initial dependency on imports for military equipment, the country has moved far ahead on the path of self-reliance.

The establishment of the Defense Research and Development Organization (DRDO) in 1958 can be considered the beginning of India’s defense sector growth story. Since then, DRDO has played a huge role in developing the latest technologies and weapons systems. Year by year, India has been expanding its manufacturing capacities and slowly but surely reducing its dependence on defense imports.

The “Make in India” initiative was also one of the reasons for the rapid development of the defense manufacturing ecosystem since local firms were given incentives and technological support to produce defense systems. This initiative allowed the private sector to contribute significantly to the Indian defense sector and the GDP.

The allocation of a huge amount of money to its military is a reflection of India’s dedication to its security. In 2024, the defense expenditure of India surpassed ₹6 lakh crore and is currently among the highest in the world. India’s significant achievements in the defense sector are:

Indigenous Weapons and Technologies

In recent years, India has been focussing on manufacturing indigenous defense equipment and technologies such as:

Tejas Light Combat Aircraft, a symbol of India’s engineering excellence, proves India’s increasing self-reliance in manufacturing superior aircraft.

BrahMos is a missile manufactured by India in collaboration with Russia. It is the world’s fastest cruise missile.

INS Vikrant, India’s first Indigenous aircraft carrier, was commissioned in 2022. 76% of the ship’s parts were sourced indigenously, and nearly 500 Indian firms collaborated on this project.

Defense Exports

India is fast becoming a significant exporter in global defense markets. It has been exporting artillery equipment, radars, armored vehicles, etc., to over 100 countries. India’s defense exports have increased from ₹686 crores to ₹21,083 crores between 2014 and 2024. This is a result of steps undertaken to promote local manufacturing.

Government’s Role in Strengthening the Defense Sector

The Indian government has played a key role in the transformation of the defense sector.

The Defense Production and Export Promotion Policy (DPEPP) was introduced by the Government of India in 2020 to develop R&D facilities to reduce dependence on imports and strengthen India’s defense sector.

In 2020, the Foreign Direct Investment (FDI) limit in the defense sector was increased from 49% to 74% through the automatic route and up to 100% through the Government route. This has attracted foreign investors to invest in India and encouraged global companies to partner with Indian firms.

The government has also implemented the concept of a “negative import list,” which lists defense equipment or parts that must be purchased locally, which has resulted in a direct increase in revenues for domestic firms.

Republic Day Parade and Military Power

The Republic Day parade is one of the most-awaited events in India as it showcases the country’s cultural diversity and military power. The Government of India also honors military personnel with gallantry awards, such as Param Vir Chakra, Ashoka Chakra, etc., on this day. The event takes place every year at Rajpath (now Kartavya Path) in New Delhi and consists of a mind-blowing display of India’s defense capabilities.

In the recent past, the Republic Day parade featured Arjun and T-90 Bhishma tanks, Agni and Akash missiles, Rafale and Sukhoi Su-30MKI aircraft, etc., symbolizing the defense strength of the nation. Tejas fighter jets and BrahMos missiles were also popular additions to the Republic Day parade.

The defense sector of India is set to experience substantial growth in the future due to the following reasons:

1. Developing New Technologies

India is making efforts to develop and use the latest technologies, such as artificial intelligence, in cybersecurity, data processing, drones, etc. A Defense Artificial Intelligence Council was established in 2022 to provide necessary guidance and structural support for developing AI’s military applications. The council has identified 70 defense-specific AI projects, out of which 40 have already been completed by the DPSUs.

2. Private Sector Companies and Startups

The private sector companies are leading the transformation of the defense sector in India. Bharat Forge, Larsen & Toubro, and Tata Advanced Systems are the big names involved in the Indian defense sector. Newspace Research and Technologies, Tonbo Imaging, and ideaForge are some of the prominent startups developing drones, robotics, and unmanned systems.

3. Collaborations and Partnerships

Good diplomatic relations with countries such as the United States, Israel, France, etc., result in substantial knowledge transfer and joint development of high-tech systems.

Republic Day Offer By Pocketful

To honour those who serve the nation, Pocketful is offering lifetime free brokerage across all segments for Army, Navy, and Air Force personnel, including ex-servicemen and women. Now, you can start investing and trading in equities and commodities, which have the potential to generate high returns in the long run. This is an initiative by the company’s founders to thank the military personnel for their services to the country.

Republic Day is not just a celebration of India’s democratic spirit; it also describes the transition of a nation dependent on imports to a self-sufficient one. The Republic Day 2025 celebrates the sacrifices made by the military personnel for the nation as well as the breakthroughs in the defense industry that would ensure India’s security.

The Indian defense firms and policies developed by the Indian government have a strong emphasis on innovation, collaboration and indigenization. The progress seen in the defense industry is one such effort that leads to the realization of the objective of a robust and self-reliant India.

Military personnel are Indian citizens who serve in the armed forces, ensuring our freedom and safety. We feel safe and sleep peacefully at night because we know that military personnel are awake at the country’s border to protect us from enemies. Military personnel spend a lot of time ensuring our safety, which may result in them not getting a chance to manage their finances properly.

For such military personnel, here is our blog. Today’s blog post will give you 10 essential tips for financial planning for military families.

Importance of Financial Planning for Military Personnel

Sound financial planning ensures financial freedom and a secure future for the armed forces members and their families. Having a financial plan will also provide you peace of mind. Financial planning is a process that involves various steps, such as setting, managing, and tracking your financial goals based on your income. Through a comprehensive financial plan, one can achieve their financial goals.

Financial Planning Tips for Military Members

Various financial planning tips that military personnel can follow to have a safe and secure future are given below:

1. Budgeting

The first step toward proper financial planning is to create a budget and manage all the expenses according to the income. One needs to identify all the sources of income, whether regular or irregular. Generally, an individual should aim to save at least 20% of their monthly income to fulfill their future needs and make provision for emergencies.

2. Optimising Military Benefits

Military personnel are accommodated in cantonment areas, and some are allowed a house rent allowance (HRA). In India, military personnel’s children are also granted scholarships and fee concessions for education. Hence, this will help them save on costs and invest the saved amount.

3. Emergency Fund

An emergency fund acts as a financial buffer and is essential during financial emergencies. Setting aside funds for emergencies provides peace of mind and reduces stress during economic uncertainty. It also helps you maintain your current lifestyle and allows military personnel to handle emergencies without depending on anyone.

4. Debt Management

Debt management is essential for keeping finances in line. For this, they must make a list of all the debt, including the amount owed, interest rates, due dates, etc. After considering all the outstanding debt, you can reduce unnecessary expenses and free up more money to pay off debt. Military personnel should also ensure timely repayment of debt to avoid any late fees.

5. Retirement Planning

In India, the retirement age for military personnel ranges from 52 to 60 years, depending on rank and other criteria. They can plan their retirement by investing in equities, which can give high returns over the long term. After retirement, they can also start their businesses. For retirement planning, equity investments can be the most suitable option for long–term growth. One can consult a financial planner or financial advisor for advice.

6. Enhancing Knowledge

In the world of finance, there are various assets, and one needs to consider the correct investment vehicle that suits one’s risk profile and investment goals and understand its associated risk. To do this, they need to continuously work on enhancing their knowledge through various financial workshops and attend training sessions online.

7. Managing Large Expenses

To prepare for large expenses, one needs to have a well-defined plan and make provision for such costs beforehand. For example, if military personnel wish to purchase a house, they must save and invest in the early stages of their career.

8. Risk Planning

Proper risk planning is essential for military personnel because of the risks they face during their services. They must opt for a comprehensive life insurance policy to protect the future of their family members.

9. Tax Management

Managing the tax is a key tool for successful financial planning, as there are various options through which military personnel can save tax on their income by reducing their taxable income. As we all know, two tax regimes are available in India, and one must consider the most suitable regime. They must also keep themselves updated about the changes in tax laws and regulations and can consult a tax expert for further information.

10. Will

A will is a key document in financial or estate planning. This statement states how a person’s asset will be transferred to their legal heir or family members in case of death. In the absence of a proper will, conflicts might arise in the family. Having a will gives you peace of mind that your financial assets will be transferred according to your wish, helping you ensure a secure future for your family members.

Financial Planning for Military Personnel with Pocketful

To honour those who serve the nation, Pocketful is offering lifetime free brokerage across all segments for Army, Navy, and Air Force personnel, including ex-servicemen and women. Now, you can start investing and trading in equities and commodities, which have the potential to generate high returns in the long run. This is an initiative by the company’s founders to thank the military personnel for their services to the country.

Conclusion

On a concluding note, military personnel spend their lives protecting us from our enemies, and it is our duty to help them in every possible way. They also need a proper financial plan to secure their family’s financial future, and the 10 tips mentioned in the blog will certainly help them. However, once the financial planning is done, it must be reviewed regularly and adjusted according to the changing circumstances. However, it is advised to consult a financial advisor before investing in the stock market.

Frequently Asked Questions (FAQs)

Can military personnel invest in stocks?

Yes, military personnel can invest in stocks. They can open a demat account with Pocketful as they are offering lifetime free brokerage to all those who have served and are currently serving in the Indian Armed Forces.

How much should military personnel keep as an emergency fund?

Military personnel should keep at least 6 months of their salary in the form of an emergency fund to meet any unexpected liabilities.

Is there any special fund for armed forces personnel?

The National Defence Fund was set up by the Government of India in 1962 for the welfare of the members of the armed forces and their dependents.

Is the defence pension tax-free in India?

Yes, pensions received by the Indian Armed Forces personnel or their families are fully tax-exempt.

As a taxpayer with a PAN card, if you are wondering about the latest release of PAN 2.0 by the Income Tax Department and are concerned about whether your current PAN will still be valid or if you’ll need to apply for a new one, then this blog is for you.

In this blog, we will address your questions about whether you need to apply for a new PAN Card and will understand the features and benefits of PAN 2.0.

What is PAN 2.0?

The Income Tax Department has recently introduced PAN 2.0, to improve the process of issuing and managing Permanent Account Numbers (PAN). Under this PAN 2.0 initiative, applicants receive e-PAN cards with secure QR code, delivered directly to their registered email IDs at no cost. A minimal fee applies for those who prefer a physical PAN card.The goal of the Income Tax Department for this initiative is to modernize and speed up the process of issuing and managing Permanent Account Numbers (PAN) and Tax Deduction and Collection Account Numbers (TAN). Through technological innovations, processing, and consolidation, this procedure will enhance the user experience and improve taxpayer registration services. The Income tax department will combine all PAN allocation, correction, and update procedures under a single system.

PAN 2.0 Key Features and Benefits

The main features of PAN 2.0 are as follows-

There will be one portal for all kinds of services related to PAN and TAN.

It is an eco-friendly process and will reduce the paperwork.

A QR code will be added to the PAN card, further enhancing its security. The QR code contains encrypted personal details like your name, date of birth, and PAN number, which can only be accessed using special scanning tools, making it very difficult for anyone to fake or tamper with the card.

Under the PAN 2.0 initiative, applying for, updating, or reissuing a PAN card is completely online. This eliminates paperwork and makes it easier for people to submit and track their applications.

A dedicated help desk and the call centre will be there, which will resolve the queries and issues of the user.

Eligibility for PAN 2.0

To apply for a new PAN card, individuals need to fulfil some eligibility criteria, whether they are a new applicant or an existing cardholder.

Existing PAN card holder: If you are an existing PAN card holder, you are automatically eligible for the PAN 2.0 upgrade. You can request the new QR-enabled PAN without reapplying.

New applicants: New applicants need to fulfil some eligibility criteria by providing the following documents:

Proof of Identity: Adhar card, voter ID, Passport, or Driving license.

Proof of Address: Utility bills, Bank statement, or Rent Agreement

Proof of Date of Birth: Birth Certificate, School Leaving Certificate, or Passport.

PAN Card 2.0 Application Process – Step-by-Step Process

To apply for a new PAN card or to upgrade the existing PAN card to a QR-enabled version, here are the steps mentioned below:

Steps to Apply for PAN 2.0 via NSDL?

Now, an applicant can easily apply through the NSDL (Protean) Portal through the mentioned steps-

If an applicant wishes to apply for a new PAN card, they must visit the NSDL website.

Then, you must select the type of application, whether it is for Indian citizens, foreign citizens, or you wish to upgrade your existing PAN.

Then, you must select the category such as individual, association of person, body of individual, etc.

Then, you will be asked for details such as name, date of birth, email address, mobile number, etc.

After continuing with your application, you will be redirected to a new page where you will submit your digital e-KYC.

You have to mention whether you want a physical PAN card or not, and then you are required to enter the last four-digit aadhaar number.

Then, you are required to enter your details and contact details in the next part of the form.

By entering your area code AO type, you can proceed to the last part of the form, document submission and declaration.

To upgrade your existing PAN card, you need to enter your PAN and personal information and then submit the application.

You can select the e-KYC option to verify using aadhaar OTP.

Then, you will be redirected to a payment page where you have to submit the fees. After the successful payment, click on the continue button.

Then you are required to tick the declaration, select the authentication option and click on continue with e-KYC.

Enter the OTP received on your aadhaar registered mobile number and click on continue with E-sign.

After applying successfully, an acknowledgement in the PDF form will be generated.

Steps to Apply for PAN 2.0 via UTIITSL?

An applicant is required to visit the UTIITSL website and click on the PAN card application page under the PAN service section.

Then click on Apply for a new PAN card (Form 49A).

Then, you are required to choose between the physical mode of application and the digital mode of application.

You are required to fill in your details.

After verifying all the details, click the submit button.

Once the verification is completed, you will be redirected to the payment page.

Once the payment is made successfully, you will receive a payment confirmation. You can either save this or take a printout of it.

Then, you are required to affix your two passport-size photos on the printed form and put your signature on the space provided in the form.

Then you have to submit the form to your nearest UTIITSL office along with the attached copy of your identity, address and date of birth proof documents.

How is PAN 2.0 different from Existing PAN?

The significant differences between the existing PAN and PAN 2.0 are as follows-

Particulars

Existing PAN

PAN 2.0

Platforms

Right now, the services related to the PAN are available on three different platforms: e-Filing, Protean e-Gov portal and UTIITSL.

Under PAN 2.0, services related to PAN/TAN will be available on a single portal of the Income Tax Department.

Paperless Process

There is a difference between online and offline processes.

The process is completely online.

Security

It has a basic security feature.

The PAN 2.0 has QR codes that enhance the security with dynamic data for real-time verification.

Grievance

The grievance is time-consuming and takes more time.

It has a centralized and faster response mechanism.

Verification Process

The verification can be done manually or online through a status check.

It has an automated verification process, which can be done through a QR code.

User-Friendly

The process is complex and takes a lot of time.

It has a simplified and user-friendly process.

Submission of Documents

Earlier physical copies and scanned documents are required to be submitted.

The process is entirely online and has a process which is document-free.

Validity of Existing PAN Card

Since current legitimate PAN cards have no expiration dates, the PAN card issued by the income tax authorities will always be valid. Due to the government’s launch of PAN 2.0, new PANs will be provided to new applicants; however, this does not imply that existing PANs will no longer be valid. As a result, current PAN card holders are exempt from applying for new PANs; their current PANs remain valid.

Is PAN 2.0 Mandatory for Everyone?

The Indian government has made it clear that you do not need to apply for PAN 2.0 if you currently have a PAN card. However, you can apply for a new PAN 2.0 if you deliberately choose to upgrade your PAN with improved security features like a QR code. Since the current PAN cards are valid for life, the government has achieved a smooth transition, and they do not want reapplications; it is not required.

Conclusion

In conclusion, the government recently unveiled PAN 2.0, which centralizes the application procedure for new PAN cards and improves the security features of PAN. However, if you already have a PAN, you won’t need to apply for a new one; your current PAN will remain valid.

Frequently Asked Questions (FAQs)

I have a PAN card. Should I get a new ePAN for PAN 2.0?

No, as your current PAN issued by the income tax authorities will still be valid, you are not obliged to obtain a new e-PAN or PAN 2.0.

Is it important to replace the old PAN card with a new PAN card under PAN 2.0?

No, replacing your old PAN with the new PAN card under PAN 2.0 is not required; however, you can do so if you desire more security features.

Do I need to change my PAN card under the PAN 2.0?

No, you are not required to change your PAN card under PAN 2.0.

Do I need an Aadhaar Card to generate PAN 2.0?

Yes, if you are applying for a PAN card through NSDL, you will be required to have an Aadhaar card.

Can I reprint my PAN Card?

Yes, you can reprint your PAN card if you have misplaced it by submitting online fees on the provided platforms.

How to get a PAN Card with a QR Code?

If you apply for a PAN card under PAN 2.0, then you will receive your PAN card with a QR code.

How to get PAN 2.0 Online?

You can get a PAN card by applying online through the NSDL or UTIITSL portal.

The stock market is one of the quickest ways to create wealth and attracts thousands of investors and traders in India. Whether you are an amateur who wants to understand the very basic concepts or an experienced trader seeking to refine their strategies, YouTube has it all to offer. Thousands of YouTube channels in their field of stock market education provide tutorials on stock analysis, investment tips, and trading strategies.

In this article, we’ll be talking about the top 10 YouTube channels for the stock market in India that can help you take your stock market journey to the next level.

Top 10 Stock Market YouTube Channels

Trading Chanakya

Pranjal Kamra

Amit Kukreja

CA Rachana Phadke Ranade

Yadnya Investment Academy

The Financial Analyst

Elearnmarkets

Money Grower

Asset Yogi

Nitin Bhatia

Each of these YouTube channels has earned a name for sharing quality stock market information, making them the hotspots for stock market enthusiasts. Let’s head into the details of each of these channels, along with a few of their best-known playlists.

Trading Chanakya is one of the best YouTube channels to learn trading in India. The YouTube channel deep dives into investment strategies and risk management. The channel is recommended for both novices and advanced traders. The channel will help you understand the psychology behind the trading and will help you execute profitable trades in the stock market.

Popular Playlists on Trading Chanakya:

Basics of Stock Market: This playlist for beginners explains the basics of the stock market, including how to analyze stocks and market cycles, along with important financial metrics.

Options Trading: This is a deep dive into options trading strategies, teaching viewers how to use leverage options for profit and manage risks.

Stock Market Analysis: This playlist is for those who already have some knowledge of trading and teaches about technical analysis, chart patterns, and indicators.

Investing for Long Term: This playlist aims at long-term wealth creation through stock investments, where one focuses a lot on the importance of the fundamental analysis.

Why Follow? Great for novice and advanced traders seeking actionable insights.

2. Pranjal Kamra

Pranjal Kamra is one of the most popular YouTubers teaching about the stock market in India. He explains the most complex concepts in a very simple and easy-to-understand method through his tutorials on stock market investing, personal finance, and financial planning. He teaches the audience about the power of compounding and long-term investing.

Popular Playlists by Pranjal Kamra:

Stock Market for Beginners: A step-by-step guide to understanding the stock markets. This is the perfect playlist for all the new folks.

Investment Strategies: Advanced strategies, including value investing, growth investing and portfolio diversification.

Personal Finance: A comprehensive playlist encompassing financial planning, wealth creation, and retirement planning.

Mutual Funds: This playlist encompasses mutual fund investments, an excellent idea for those who wish to diversify their investments.

Why Follow? Pranjal’s practical advice and real-life examples make complex concepts easy to grasp.

3. Amit Kukreja

Amit Kukreja is another esteemed name in the category of personal finance and stock market education. His YouTube channel aims to educate people about specific investment strategies, financial planning, and market analysis. Given his detailed and easy-to-follow content, Amit Kukreja simplifies complex financial thoughts for beginners and provides more insight for experienced investors.

Trending Playlists on Amit Kukreja:

Stock Market Insights: In-depth reviews of stock market trends, the latest economic updates, and sector-specific reviews.

Investment Strategies: Tips and strategies for building a diversified portfolio aimed at meeting long-term financial goals.

Mutual Funds Masterclass: Reviewing mutual funds in detail with head-to-head comparisons to guide the audience toward making the right investment choices.

Wealth Planning Basics: Financial planning, retirement planning, and essentials about wealth management.

Why Follow? His channel provides a balanced mix of theoretical and practical financial knowledge.

4. CA Rachana Phadke Ranade

CA Rachana Phadke Ranade is one of the best stock market teachers on YouTube. With a background in finance, she is a trusted name for financial education. Her channel offers detailed lessons on all aspects of a stock market, be it trading strategy or financial literacy.

Top Playlists on CA Rachana Phadke Ranade:

Stock Market Course in Hindi: It is a complete stock market course for beginners, ranging from basic aspects of the market to advanced topics.

Technical Analysis: Offersdeep insights on technical analysis, chart patterns, and key indicators, which helps traders make informed trading decisions.

Fundamental Analysis: The playlist teaches how to analyze a company on the basis of its financial statements and determine intrinsic value.

Investing in Stocks: A playlist of long-term investments focusing on portfolio management and risk management, including diversifying investment portfolios.

Why Follow? Rachana’s structured courses are excellent for beginners and advanced learners alike.

5. Yadnya Investment Academy

Yadnya Investment Academy is one of the most well-respected channels that has always focused on delivering deep insights into financial planning, mutual funds, and the stock market. It is a platform that empowers retail investors with strategic investment opportunities for long-term wealth creation.

Popular Playlists on Yadnya Investment Academy:

Stock Market Insights: Analysis of the Indian stock market trends based on sectoral performance and macroeconomic conditions.

Mutual Funds Simplified: Guidelines on how to select the right mutual fund as per your financial goals, risk appetite, and specific performance metric.

Detailed Breakdown of listed companies, company fundamentals, and growth prospects for informed decision-making.

Why Follow? Perfect for those looking to build sustainable investment portfolios.

6. The Financial Analyst

The Financial Analyst is a popular YouTube channel that focuses on stock market analysis, investments, and personal finance. The playlists are meant to help people make better decisions regarding their money.

Most Popular Playlists on The Financial Analyst

Stock Market Analysis: It offers an overview of the current trends in the stock markets, technical analysis, and stock recommendations.

Investment Strategies: Several investment techniques are shared on how to build long-term wealth.

Stock Picks: This playlist features stocks that should be worth investing in, with a detailed analysis of their growth prospects.

Financial Planning: The playlist takes one through the entire personal finance spectrum, from budgeting to wealth management.

Why Follow? Offers quick, actionable tips for improving financial health.

7. Elearnmarkets

Elearnmarkets is a popular channel that aims to provide educational content to stock market enthusiasts. It is designed for those interested in learning trading and investing from scratch. The channel offers expert guidance with easy-to-understand tutorials, thus making complex financial concepts understandable to everyone.

Popular Playlists on Elearnmarkets:

Stock Market Basics: A playlist of beginner-friendly lessons to understand the basics of the stock market.

Technical Analysis: Comprehensive playlists on chart pattern recognition, indicators, and trading tools necessary for any successful trader.

Financial Planning: The playlist explainspersonal finance, wealth management, and financial planning.

Advanced Trading Strategies: Options trading, derivatives, and algorithmic trading are covered in this playlist.

Why Follow? An excellent resource for traders looking to advance their technical skills.

8. Money Grower

Money Grower is a YouTube channel that provides a combination of stock market analysis, trading techniques, and general financial knowledge. This interesting approach to teaching the viewers made Money Grower one of the top stock market YouTube channels.

Most Popular Playlists on Money Grower:

Stock Market for Beginners Series: This all-inclusive series covers the basics of the stock market.

Technical Analysis: Individuals can watch this playlist to learn how to use chart patterns for trading decisions.

Stock Picking: This playlist teaches you how to select individual stocks with long-term growth potential.

Investment Strategies: Learn how to make a very powerful investment portfolio.

Why Follow? Simplifies technical concepts into easily digestible lessons.

9. Asset Yogi

Asset Yogi is one of the popular channels providing informative content on stock market basics and investing strategies. The channel’s content caters to individuals with different experience levels, breaks down complex financial concepts, and provides actionable insights toward creating wealth. What makes Asset Yogi stand out is its ability to explain academic content through practical applications, which makes it useful for making the right financial decisions.

Trending Playlists on Asset Yogi:

Personal Finance Fundamentals: Beginners can watch this playlist to learn how to manage your personal finances.

Stock Market for Beginners: Learn how the stock market works and start your investing journey smoothly.

Real Estate Investment: A comprehensive guide on how to invest in property, the returns, and the general market trends.

Understanding Mutual Funds: In-depth studies of mutual fund types and returns and criteria that determine the best mutual fund for a particular investor.

Why Follow? The practical approach ensures relevance to real-life investment scenarios.

10. Nitin Bhatia

Nitin Bhatia is a popular YouTuber in the Indian stock market. He offers excellent content on stock trading, personal finance, and investment strategies. His channel is suitable for both beginners and advanced traders.

These YouTube channels provide some of the best educational content on stock markets in India. Be it learning the basics or advanced technical analysis, these channels will help you achieve your financial goals.

With the best stock market YouTube channel, you gain valuable insights, market updates, and upgrade your investing and trading approaches and strategies. Patience, discipline, and the pursuit of knowledge are key success factors in investing. However, it is advised to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Some of the best stock advisors on YouTube are Pranjal Kamra, Rachana Ranade, and Trading Chanakya.

Can I learn trading on YouTube?

It is possible to learn trading on YouTube because channels like Trading Chanakya, Elearnmarkets and Rachna Ranade offer quality educational content.

Who is the best stock market teacher?

The best YouTube stock market teacher is Rachana Ranade due to her clear explanations and easy-to-understand content.

Which of the following are the 5 best YouTube channels to learn about the Indian stock market?

The best 5 YouTube channels for the stock market in India are Pranjal Kamra, Rachana Ranade, Trading Chanakya, Elearnmarkets, and The Financial Analyst.

Can I trade based on the information provided by a YouTube channel?

It is advised to consult a financial advisor before making trading decisions.

While trading or investing in the stock market, one common term that market participants come across is LTP (Last Traded Price). LTP is the price at which a stock or security was last traded. Unlike opening or closing prices of a day, LTP continuously changes during the trading session. This provides insight for short-term traders.

In this blog, we will discuss what LTP means and its full form, how it is calculated, and how it is used in trading. We will also be discussing how LTP stacks up against other price metrics.

What is LTP?

LTP stands for Last Traded Price. It denotes the price at which the most recent transaction or trade involving a stock was executed. It is dynamic and varies throughout the trading day due to continuous buying and selling activity.

How is LTP Calculated in the Share Market?

LTP is determined directly from the transaction data recorded by the stock exchange. Here is a simplified breakdown.

Whenever a security is bought or sold, the exchange meticulously documents the transaction.

Every transaction record captures the exact price at which the trade was executed, along with a precise timestamp, ensuring comprehensive details for every transaction.

LTP of an asset represents the price at which the most recent transaction involving the asset has been completed. Furthermore, it is updated in real time as new transactions occur. For example, if the last transaction for a particular stock was executed at INR 500 at 3:15 PM, then the LTP at that instant would be INR 500.

LTP vs Other Key Price Metrics

Knowing the differences between LTP and other price metrics can improve your investment decisions and trading styles. Some of the key price metrics are:

Open Price – It marks the price at which the first trade of the day takes place, offering valuable insights into the market’s initial sentiment.

High Price – This represents the highest price achieved during a trading day. It reveals the highest price paid for that security on that day.

Closing Price – It is the weighted average price of the last thirty minutes of the trading day.

Average Price – This represents the mean price of all transactions conducted within a designated time frame. It offers a broader perspective on price fluctuations during the trading session.

Volume – It refers to the total number of shares exchanged during a specific timeframe. The volume shows the interest and activity levels in the security.

Uses of LTP in Stock Trading

LTP can be used in stock trading in the following ways:

Trend Analysis – Traders closely monitor the Last Traded Price (LTP) to discern market trends, helping them determine whether a stock is experiencing an upward or downward trajectory.

Momentum Trading – Traders seize opportunities in stocks that exhibit consistently increasing or decreasing LTPs, signaling a strong momentum.

Support & Resistance –The LTP is instrumental in recognizing important levels from where the price generally reverses, i.e. support and resistance levels.

Intraday trading – For short-term traders, the LTP is an essential tool for making buy or sell decisions based on minute-by-minute fluctuations.

Scalping – It is a dynamic trading strategy that focuses on executing rapid buy and sell transactions to capitalize on minor price movements. Traders frequently rely on LTP as a key indicator in this approach.

The LTP serves as a key element in technical analysis. It offers real-time insights to analysts, which helps them spot trends, patterns, and possible future price changes. Let us have a quick overview of how LTP can be used in technical analysis.

The ability to read charts is a key skill in technical analysis. LTP is illustrated on price charts to provide a visual depiction of a security’s price history.

Analysts use LTP to spot uptrends, downtrends, and sideways trends. LTP data also helps in analyzing historical support or resistance levels for an asset.

Technical indicators like moving averages, RSI, and Stochastic Oscillator use LTP data to generate signals.

LTP, when analyzed alongside volume, empowers traders to gauge whether price fluctuations are backed by substantial trading activity.

Factors Affecting LTP

Various factors affect the LTP of a stock, some of which are listed below:

Economic Indicators

Economic Indicators such as GDP, inflation rates, and employment data play a crucial role in shaping overall market sentiment and consequently influencing the LTP.

Supply & Demand

Supply refers to the total quantity of shares that can be offered for sale in the market. An increase in the number of sellers leads to a higher supply of stock, which can lower the last traded price.

Demand refers to the quantity of shares that can be bought in the market. Increased buyer interest raises demand, which pushes the stock’s last traded price up.

So, LTP represents a point at which supply and demand converge, signifying the price at which the buyer and seller reached an agreement to complete a transaction.

Corporate Announcements

Earnings Reports, whether positive or negative, can lead to substantial price fluctuations. Company events like mergers, acquisitions, product launches, or legal issues can also affect LTP. The performance of the industry in which a company operates also impacts its stock price. Dividend announcements can also attract investors and raise the stock price.

Bid-Ask Spread

The bid-ask spread is the difference between the bid price and the ask price. The bid price is the highest price a buyer will pay, and the ask price is the lowest price a seller will accept. The LTP usually falls within this range and adjusts as trades occur between the bid and ask prices.

A narrow bid-ask spread shows high liquidity and reduced volatility, whereas a wide bid-ask spread shows low liquidity, resulting in greater fluctuations in the LTPs.

Understanding the concept of LTP is essential for anyone engaged in trading or investing in the stock market. It stands for the last traded price of an asset, which is necessary for quick decision-making, especially for day traders and short-term investors. LTP changes with each transaction and is affected by supply and demand, market sentiment, corporate performance, and global events. Including LTP in your trading strategy can keep you updated on market trends, help identify important buying or selling opportunities, and improve trading performance. Remember, LTP is only one aspect of analysis; it is also essential to consider metrics like opening price, closing price, volume, etc. It is advised to consult a financial advisor before investing or trading.

Frequently Asked Questions

Is LTP the same as the closing price?

No, LTP reflects the price at which the most recent transaction was completed, while the closing price is the weighted average price of transactions during the final moments of the trading day.

How often does LTP change?

LTP changes every time a new transaction happens, making it a real-time indicator of stock price movements.

Is LTP useful for long-term investors?

While it is more useful for short-term traders, long-term investors might use it alongside other metrics to identify major support and resistance levels.

Why does LTP fluctuate during market hours?

LTP fluctuates because of ongoing trading activity, influenced by market dynamics and investor sentiment.

Can LTP be manipulated?

In highly liquid markets, it is difficult to manipulate LTP. However, in low-volume stocks, large block deals can cause large price swings.

The stock market has always been a captivating subject, full of drama, suspense, and high stakes. Hollywood and streaming platforms have turned the thrill of trading, investing, and corporate battles into some of the most engaging movies and web series. Stock markets are a place with a lot of interesting stories, which the entertainment industry has depicted in creative ways over the years. The entertainment industry has done an excellent job of simplifying complex financial events so that anyone can understand them. However, most of them are based on real-life incidents that caused the stock markets to plummet.

In this blog, we will provide an overview of the best movies and web series about the share market that are worth watching.

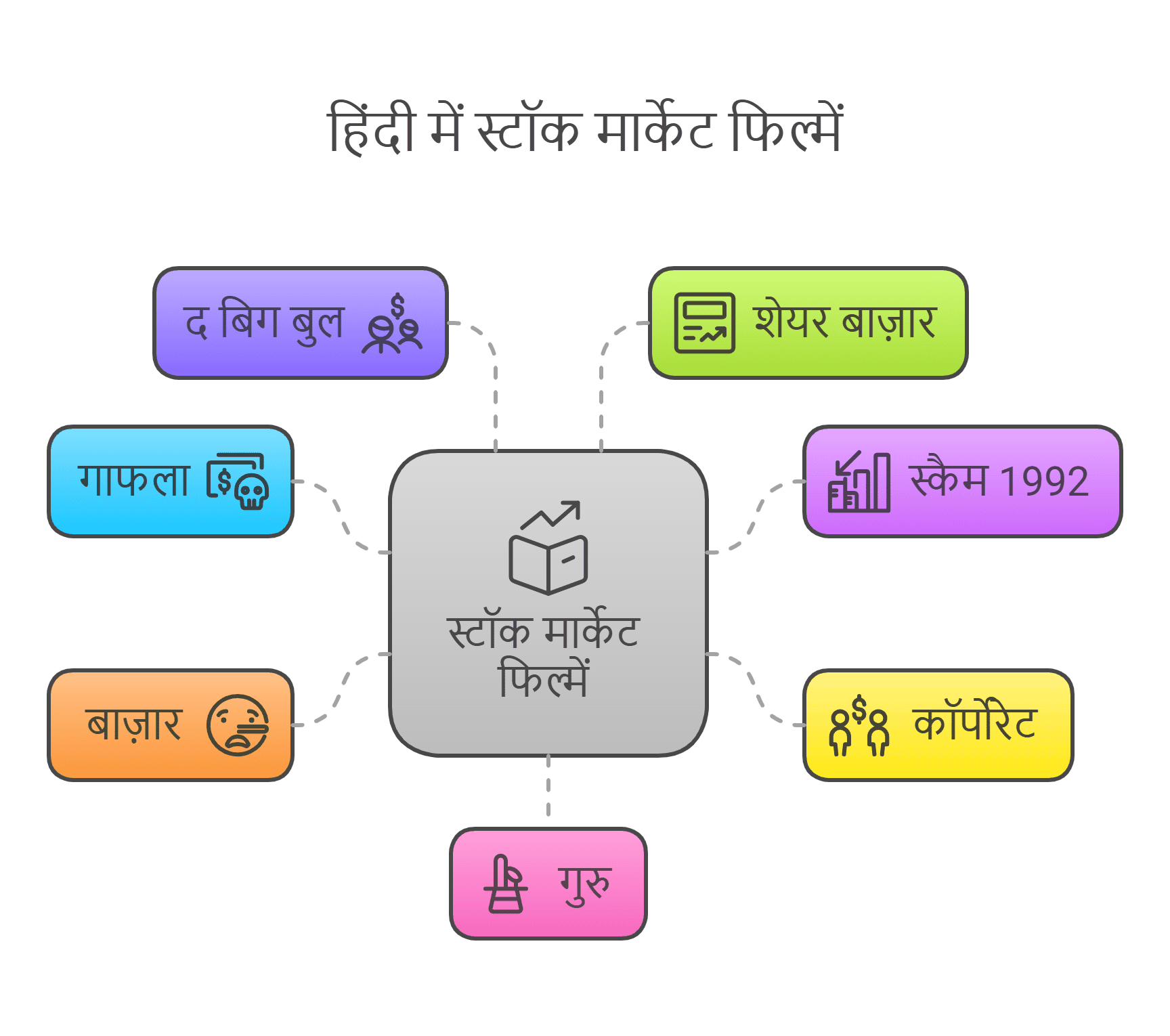

Performance Table: Best Stock Market Movies and Web Series

Here’s a table listing the best stock market-related movies in Hindi:

S.No.

Movie/Series

Year

Plot/Theme

Highlights

1

Gafla

2006

A young man enters the stock market and gets involved in scams.

Inspired by the Harshad Mehta scam.

2

Scam 1992: The Harshad Mehta Story

2020

Chronicles the rise and fall of Harshad Mehta in the stock market.

Realistic depiction of the stock market and its inner workings.

3

Corporate

2006

A drama about corporate rivalries and ethical dilemmas.

Explores power dynamics in business boardrooms.

4

Baazaar

2018

A young aspirant gets involved in the greed and deception of the financial world.

Slick portrayal of the stock market with standout performances.

5

The Big Bull

2021

A dramatized take on the Harshad Mehta-inspired stock market boom of the ’80s and ’90s.

Comparable to Scam 1992 but with a cinematic approach.

6

Share Bazaar

1997

Focuses on the ups and downs of the stock market.

One of the earliest Hindi films about the stock market.

7

Guru

2007

Loosely inspired by Dhirubhai Ambani’s life and rise as an industrial tycoon.

Explores ambition, business strategies, and financial risk-taking.

These movies and series provide a mix of drama, thrill, and education about the stock market and financial industries, making them engaging for audiences with an interest in this field.

Overview of the Best Share Market Movies and Web Series

The overview of the stock market movies and web series are:

1. The Wolf of Wall Street (2013)

The film, which was released in 2013, was based on the true story of Jordan Belfort, a stockbroker who operated a dishonest brokerage business. It is revealed in this film that Jordan co-founded Stratton Oakmont with a man by the name of Donnie and that the company participated in pump-and-dump stock price manipulation. As a result, Jordan has amassed an enormous fortune over time and subsequently becomes entangled in illicit operations, including drugs, women, and other things. Subsequently, they caught the interest of law authorities, notably the FBI. After an investigation, he lost all his wealth and faced serious repercussions. Leonardo DiCaprio portrayed Jordan in the film. The film was financially successful and made over $400 million.

Genre: Biography, Comedy, Crime

Director: Martin Scorsese

Starring: Leonardo DiCaprio, Jonah Hill, Margot Robbie

Key Takeaway: The dangers of unethical practices in the stock market.Language: English

Budget: ₹830 crore (approx.)

Earnings: ₹3,254 crore (approx.)

Available On: Netflix, Amazon Prime Video

2. Scam 1992: The Harshad Mehta Story (2020)

A book named “The Scam: Who Won, Who Lost, Who Got Away” was written by journalists Sucheta Dalal and Debashis Basu. The book’s contents served as the basis for the “Scam 1992: The Harshad Mehta Story”, which was released in 2020. The series narrates the tale of the largest financial fraud in India, which took place in the early 1990s. Pratik Gandhi played the role of Harshad Mehta. Mehta was well-known for his aggressive investment strategies and market manipulation methods. During his time, the Indian stock market soared to astronomical highs, due to which he was known as the “The Big Bull.” His prowess in manipulating the Indian Banking System and stock prices caught the attention of journalist Sucheta Dalal, portrayed by Shreya Dhanwanthary. She investigated the fraud and released her findings, which led to Harshad Mehta’s arrest, and ultimately, the Indian stock market crashed.

Key Takeaway: The importance of transparency and the potential consequences of exploiting financial loopholes.

Language: Hindi

Budget: Not publicly disclosed

Earnings: Not applicable (TV series)

Available On: SonyLIV

3. Margin Call (2011)

This American film narrates the actions performed by the employees at a large Wall Street investment bank for 24 hours during the financial crisis of 2007–2008. The movie’s title describes a scenario where an investor must increase the assets pledged as security for a loan after their value drops below a predetermined threshold. Eric Dale, the company’s head of risk management, developed a model that reveals a financial risk that could cause the firm to collapse. He alerted his bosses and other executives to the risk, but they initially ignored it. In an attempt to stay out of bankruptcy, companies strive to sell off their assets by the next day. This film illustrates how financial company mismanagement caused the global share market to crash.

Genre: Drama, Thriller

Director: J.C. Chandor

Starring: Kevin Spacey, Paul Bettany, Jeremy Irons

Key Takeaway: The risks involved in financial markets and how decisions made in crisis moments can impact the world.

Language: English

Budget: ₹29 crore (approx.)

Earnings: ₹161 crore (approx.)

Available On: Amazon Prime Video, Hulu, Peacock

4. Inside Job (2010)

The 2010 documentary Inside Job showcases the circumstances leading up to the financial crisis of 2007-2008. The documentary starts with an analysis of prevalent deregulations in the finance industry in the early 1980s. The dangerous aspects of these decisions are explained in the film, including mortgage-backed securities and credit default swaps. The film examines the economic bubble and how rising real estate prices encouraged banks to lend money without first determining the borrower’s creditworthiness. In 2007 and 2008, subprime loan defaults caused investment banks like Lehman Brothers and Bear Stearns to fail, while the government bailed out other institutions like AIG. The film illustrates how senior bank executives disregarded established guidelines, which caused the world stock market to collapse.

Genre: Documentary

Director: Charles Ferguson

Narrated by: Matt Damon

Key Takeaway: The far-reaching consequences of financial corruption and the need for transparency and regulation in the financial industry.

Language: English

Budget: ₹17 crore (approx.)

Earnings: ₹64 crore (approx.)

Available On: Netflix

5. Rogue Trader (1999)

Rogue Trader is a movie based on a true story about a reckless trader named Nick Leeson who made financial decisions that caused the UK-based Barings Bank to fail. The autobiography “Rogue Trader: How I Bought the Barings Bank and Shook the Financial World” served as the inspiration for the film. The film starts with the story of a young banker named Nick Lesson, portrayed by Ewan McGregor, who works for Barings Bank and is assigned to Singapore to oversee derivatives trading at the Singapore International Monetary Exchange. Through his aggressive trading, he generated significant profits right away. Afterwards, he started to lose money, but instead of disclosing it, he kept it hidden in a secret account and intended to use riskier wagers to win it back. After placing a large bet on the potential stability of the Japanese market, he lost a significant amount of money—roughly 827 million Euros—when the Japanese stock market experienced a correction in 1995 due to an earthquake in Japan. This event ultimately caused Barings Bank to fail.

Genre: Biography, Drama

Director: James Dearden

Starring: Ewan McGregor, Anna Friel

Key Takeaway: The dangers of unchecked power and the devastating impact one individual’s actions can have on the financial world.

Language: English

Budget: ₹105 crore (approx.)

Earnings: ₹13 crore (approx.)

Available On: Amazon Prime Video, Tubi

6. Wall Street

Wall Street is a film about the ins and outs of Wall Street and how people engage in insider trading. The film’s protagonist, Charlie Sheen, plays the role of Bud Fox, a young stockbroker with big goals in the financial world. Gordon Gekko is a smooth-talking, brash and ruthless corporate raider, portrayed by Michael Douglas. In search of success, Bud, a junior stockbroker, encountered Gordon Gekko, a wealthy and assertive stock market participant. Fox’s father, a maintenance worker’s union leader at an airline, provides him with some insider knowledge about a business, which Bud tells Gordon. For his performance in this film, actor Michael Douglas was awarded the Academy Award for Best Actor. The greed, power, ambition, and ethics of a person who is prepared to give up all for their achievement are all depicted in the film.

Genre: Drama

Director: Oliver Stone

Starring: Michael Douglas, Charlie Sheen

Key Takeaway: The consequences of corporate greed and ethical compromises.

Language: English

Budget: ₹124 crore (approx.)

Earnings: ₹362 crore (approx.)

Available On: Disney+, Amazon Prime Video

7. The Big Short

The Big Short, based on a non-fiction book by Michael Lewis, was released in 2015 and was regarded as a critically acclaimed film. Adam Mckay directed it. The events leading up to the 2008 financial crisis are explained in the movie. The film is about the people who foresaw the 2008 financial institution meltdown and placed bets against it, ultimately making substantial profits.

Christian Bale plays the role of Michael Burry, a hedge fund manager with a distinct perspective on the market. He studies the mortgage industry and concludes that the loans given out by financial institutions are risky and prone to fail. It draws attention to how subprime loans triggered the expansion and collapse of the US housing market. In addition to being a commercial success, this film won other accolades, including the Academy Award for Best Adapted Screenplay.

Genre: Biography, Comedy, Drama

Director: Adam McKay

Starring: Christian Bale, Steve Carell, Ryan Gosling

Key Takeaway: Understanding the risks and ethical implications of subprime mortgages.

Language: English

Budget: ₹231 crore (approx.)

Earnings: ₹1,102 crore (approx.)

Available On: Netflix, Amazon Prime Video

8. Boiler Room

The film Boiler Room, directed by Ben Younger, was released in 2000. The film is focused on the world of brokerage firms involved in questionable and frequently unlawful trading activities. Giovanni Ribisi played the role of Seth Davis, a young man who operates an unlicensed casino in his apartment after dropping out of college. He later worked for a brokerage company called J.T. Marlin, where he learned how to aggressively offer worthless penny stocks—to gullible customers and persuade them that they have a fantastic investment opportunity. He later learns about the negative aspects of JT Marlin’s company, including the pump and dump strategy, exploiting clients to make enormous profits. The film was made on a budget of $7 million and earned approximately $28 million at the box office.

Genre: Crime, Drama, Thriller

Director: Ben Younger

Starring: Giovanni Ribisi, Vin Diesel

Key Takeaway: The dangers of stock fraud and the impact of unethical trading.

Language: English

Budget: ₹58 crore (approx.)

Earnings: ₹232 crore (approx.)

Available On: Amazon Prime Video, Hulu

9. Too Big to Fail

The 2011 HBO film centers on the 2008 financial crisis and the responses of Federal Reserve Chairman Ben Bernake and Treasury Secretary Henry Paulson to the failure of Lehman Brothers. The film’s central theme is how the collapse of one organization might affect the collapse of the global financial system. Intense pressure and political scheming were also featured in the film as the Fed Chairman and New York Fed President attempted to stop the financial system from collapsing. Paul Giamatti played the role of Federal Reserve Chairman Ben Bernanke in the film, while James Woods portrayed Lehman Brothers CEO Dick Fuld. Critics praised the film for its narrative, directing, and acting, and it has been nominated for multiple awards, including the Screen Actors Guild and Golden Globes.

Genre: Drama

Director: Curtis Hanson

Starring: William Hurt, Paul Giamatti

Key Takeaway: The consequences of poor financial management and the efforts to prevent economic disaster.

Language: English

Budget: Not publicly disclosed

Earnings: Not applicable (TV film)

Available On: HBO Max

10. Enron: The Smartest Guys in the Room

The growth and fall of the Enron Corporation, one of the worst business scandals in the United States, is the subject of the 2005 documentary Enron, which Alex Gibney directed. Bethany Mclean and Peter Elkind’s book served as the basis for this documentary. Enron’s management committed a significant accounting scandal that ultimately caused the company to go bankrupt in 2001. The corporation manipulates accounting procedures and inflates its profits. Energy costs increase due to the company’s purposely induced power and energy constraints in California. In addition to receiving numerous honors and praise from critics, this documentary was nominated for an Academy Award for Best Documentary Feature.

Genre: Documentary

Director: Alex Gibney

Key Takeaway: The destructive effects of corporate fraud and the need for transparency.

Language: English

Budget: ₹5.8 crore (approx.)

Earnings: ₹39 crore (approx.)

Available On: Amazon Prime Video, Hulu

11. Billions

In 2016, this American television show made its debut. Personal rivalry, legal conflicts, and the fierce world of hedge funds were portrayed in the series. The show centers on two powerful individuals: Bobby Axelrod, played by Damian Lewis, who is the head of Axe Capital and a billionaire hedge fund manager, and Chuck Rhoades, played by Paul Giamatti, a US attorney who, despite his intelligence, has a vicious personality and is determined to bring Axelrod down. Later in the series, Mike Prince, a billionaire, appeared as Axe’s new rival. The script, directing, plot, acting, and other aspects of the Billions series have all won praise from critics.

Genre: Drama

Creator: Brian Koppelman, David Levien

Starring: Damian Lewis, Paul Giamatti

Key Takeaway: The personal and legal battles within the hedge fund industry.

Language: English

Budget: Not publicly disclosed

Earnings: Not applicable (TV series)

Available On: Showtime, Amazon Prime Video

12. Baazaar

Gauravv K. Chawla directed the 2018 Bollywood film Baazaar. Rohan Mehra portrayed the character of Rizwan Ahmad, an ambitious man from a tiny Indian town who wants to pursue a career in the stock market. Saif Ali Khan, a formidable and enigmatic businessman, portrayed Shakun Kothari. After meeting Shakun Kothari, Rizwan began managing his investments and used insider information to make profits. The negative aspects of the stock market are portrayed in this film. The film, which portrays greed, ambition, and moral compromise, draws inspiration from several Hollywood productions, including Wall Street and The Wolf of Wall Street.

Genre: Crime, Drama, ThrillerDirector: Gauravv K. Chawla

Starring: Saif Ali Khan, Rohan Mehra

Key Takeaway: The moral compromises people make to achieve financial success.

Language: Hindi

Budget: ₹34 crore (approx.)

Earnings: ₹40 crore (approx.)

Available On: Amazon Prime Video

13. Gafla

Gafla is a 2006 Bollywood film directed by Sameer Hanchate. The main focus of the film is to portray the details of Harshad Mehta’s stock market scam. The movie shows how a driven individual who aspires to succeed discovers loopholes in the Indian financial system and utilizes them to make huge profits. The story’s protagonist, Subhod Mehta, is a tiny businessman with an interest in the stock market. He quickly establishes his financial empire by using his high-risk trading methods to control stock prices, but he must finally confront the market’s negative aspects, too. He joined the stock market with huge ambitions but later turned to immoral behavior in an attempt to appease brokers and investors.

Genre: Drama, Thriller

Director: Sameer Hanchate

Starring: Vinod Sharawat

Key Takeaway: How ambition and manipulation can lead to massive consequences.

Language: Hindi

Budget: Not publicly disclosed

Earnings: Not widely released

Available On: YouTube

14. Black Monday

It’s a television show that ran from 2019 to 2021 and was produced by David Caspe alongside Jordan Cahan. The film is based on an event that occurred in 1987, when one of the biggest stock market crashes in history occurred on October 19. Don Cheadle plays the role of Maurice Monroe, the head of a successful brokerage firm named the Jammer Group. He was extremely ambitious yet ethically flexible. Andrew Rannells portrayed the character of Blair Pfaff, a crucial member of the firm and an unpredictable stockbroker. The show highlights the challenging situations protagonists face as Black Monday approaches.

Genre: Comedy, Drama

Creators: David Caspe, Jordan Cahan

Starring: Don Cheadle, Andrew Rannells

Key Takeaway: The impact of risky trades and unethical practices in volatile times.

Language: English

Budget: Not publicly disclosed

Earnings: Not applicable (TV series)

Available On: Showtime, Amazon Prime Video

15. Equity

The 2016 financial thriller Equity, directed by Meera Menon, centers on Naomi Bishop, a senior investment banker. The film covers the narrative of men’s domination in the finance industry and offers a distinctive viewpoint on the field. Anna Gunn, James Purefoy, and Alysia Renier were the film’s main actors. While working on an IPO for a tech company, Naomi encountered several challenges, including mistrust from their male coworkers and her complex relationship with a hedge fund manager. The film is notable because it depicts the realities faced by women in the finance industry.

Genre: Drama, Thriller

Director: Meera Menon

Starring: Anna Gunn, James Purefoy

Key Takeaway: The challenges and biases women face in finance.

Language: English

Budget: ₹29 crore (approx.)

Earnings: ₹13 crore (approx.)

Available On: Amazon Prime Video, Hulu

Here’s a list of some of the best stock market movies in Hindi or movies with a significant financial and stock market theme that may interest Bollywood enthusiasts:

Many films on the stock market have been made all over the world, but the majority of them are based on the financial crises that occurred in different nations. While some were based on the 2008 financial crisis, others were based on India’s 1992 stock market collapse or the 1995 Japanese market collapse. Every film imparts the wisdom that, despite possible short-term causes for market declines, investors should maintain faith in the stock market because, in the end, it will rise and surpass its prior peak.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Which is the best movie based on the stock market?

The stock market has been the subject of many films, such as Rogue Trader, Margin Call, The Wolf of Wall Street, etc.

Which Indian web series is based on the Indian Stock Market crash?

The 1992 Indian stock market crash is the subject of the web series Scam 1992, which is based on financial fraud committed by Harshad Mehta.

What was the reason for the stock market fall in the year 2008?

The collapse of US financial institutions like Lehman Brothers led to a decline in investor trust in banks, which in turn caused the 2008 stock market crisis.

Who played the role of Harshad Mehta in the Scam 1992 web series?

Pratik Gandhi played the role of Harshad Mehta in the Scam 1992 web series.

Who exposed the Scam of 1992?

The scam caused by Harshad Mehta was exposed by a journalist named Suchita Dalal.

On one fine day, sitting calmly in your chair, you hear the news regarding the due date for filing your income tax return, and the government may penalize you for not paying income tax by the due date. You must have thought about why you are paying a portion of your hard-earned money to the government. Is it necessary? How are you going to benefit from it?

In this blog, we are going to discuss how the government uses taxes for the benefit of the nation’s citizens. Moreover, we will give you some interesting, unpopular facts about the taxpayers in India. So, read on.

What is Tax?

Taxes are mandatory contributions made by corporations and individuals to the government. Governments use these funds to provide public services, such as police services and roads, to the public. The government also pays the salaries of civil servants. The public does not pay directly for these goods and services or for the time of public servants when they visit government offices; it pays indirectly through taxation. The government, therefore, regularly decides how much to spend, what to spend it on, and how to finance its expenditure.

There are different kinds of taxes levied on different assessees. However, these taxes are broadly classified into two major categories:

1. Direct Tax

Direct taxes are levied on individuals, corporations, and other entities. As the name suggests, direct taxes are the taxes that are paid by the taxpayers directly to the government. This tax is applicable to taxpayers earning income above some specific threshold, and it cannot be shifted to another taxpayer. That means not all individuals are liable to pay direct tax. Direct tax includes the following types of taxes:

Income Tax

Corporate Tax

Security Transaction Tax

Capital Gains Tax

Gift Tax

2. Indirect Tax

The indirect tax is not paid directly to the government but levied on the taxpayers at the time of purchase or consumption of goods and services, irrespective of the taxpayer’s income. The tax amount is included in the cost of goods or services, and the tax burden is passed on from the wholesalers to retailers, who pass it on to the customers. Examples of indirect tax are:

Goods and Services Tax

Custom Duty

Value Added Tax

How Does the Government Use Taxes?

Taxes are levied by the government and collected by tax authorities for the development of the nation. The tax collected by the government, which is the major source of revenue for the government, is used to fund various sectors in the country, such as:

Healthcare

Education

Infrastructure

Social Security

Defence

Environment Protection

International Relations

Emergency & Contingency Funds

Some Interesting Facts About Taxpayers in India

Here are some interesting facts about taxpayers in India:

A mere 5-6% of India’s population contributes to income tax, indicating a small number of taxpayers.

The new tax regime launched in FY 2020 features six slabs with rates from 0% to 30%, along with various exemptions under the previous regime.

As of 2023, 1.40 crore businesses are registered under the Goods and Services Tax (GST) system.

The largest group of individual tax filers falls within the ₹5-10 lakh annual income range.

Following demonetization, there was a 25% increase in income tax returns filed between FY 2016 and FY 2017.

Importance of Taxes in Making India a Developed Nation

Before we discuss how taxes are important in making India a developed nation, let’s talk about what makes a country developed. A country with a strong economy, a high quality of life, equal distribution of income among its citizens, low poverty and employment rates, access to quality health and education, and a diverse industrial sector is considered a developed nation. Below, we are listing a few key points of how taxes can help India achieve all those things and make it a developed economy:

The government uses taxes to build infrastructure, which is essential for any country’s economic growth.

The taxes received by the government are also used to fund social initiatives and welfare programs.

No country can become a developed country without education. Government-collected taxes are used to fund quality education in rural as well as urban areas, which includes school infrastructure, teacher’s salaries, etc.

The government bears the expenditure on health and medical R&D, hospital infrastructure, health insurance, and other services.

Taxes fund schemes to help people who are unemployed or have low levels of income.

Governments introduced progressive taxation in order to reduce income inequality by making people who earn more pay more taxes and build an equitable society.