In the dynamic world of trading, there are various tools available that can help you increase your return in the stock market. One such tool or facility is margin trading, which is becoming very popular among traders as it allows them to take a larger position without paying the full value upfront. However, before trading, understanding how to use margin trading wisely becomes essential.

In this blog, we will explain the top tips for successful margin trading.

What is Margin Trading?

Margin trading involves borrowing money from a broker to purchase or sell securities. Although margin trading involves a higher risk, it enables traders to take on larger positions than their actual capital and thus magnifies profits. Typically, the trader pays a margin upfront, which is set by the broker based on the entire trade value, and the broker pays the remaining sum on your behalf. You have to pay interest on the borrowed amount.

The important top tips for successful margin trading are as follows:

Understanding: Before initiating any trade using margin, one should become familiar with the concepts of leverage, initial margin required, etc.

Conservative Approach: Don’t use the maximum leverage that is permitted. To minimise risk, start by using less leverage until you are confident in your approach.

Stop Loss: To protect your capital, a stop-loss order allows you to automatically exit a trade at a set loss level. In margin trading, it is essential to use a stop-loss.

Monitoring: Especially in times of market volatility, it is essential to give particular attention to your open positions.

Diversification: Avoid allocating all your margin capital to a single stock or position. By spreading your investments across multiple stocks or sectors, you reduce risk and protect your portfolio from the impact of a single unfavorable trade.

Manage Your Emotions: Trading on margin can test your emotional discipline. Stay calm, stick to your plan, and avoid taking decisions based on greed or fear.

Stay Updated: One is required to keep oneself updated about the latest market updates and geopolitical events so that, in case of any negative news, one can exit their position promptly.

Liquid Stocks: It is always suggested that liquid stocks be used for margin trading, as liquid stocks can be easily bought and sold.

Interest Rates: Brokers charge interest on the margins; therefore, comparing the interest rates charged by different brokers is recommended to get a better deal.

Avoid Margin Calls: When the stock price you have purchased falls, your broker will notify you to pay an extra margin. Therefore, one should constantly monitor their trading positions.

The important features of margin trading are as follows:

Leverage: This margin trading feature lets you trade with more money than you have.

Initial Margin: The initial margin, which is a set percentage of the entire trade value, must be deposited before you can start margin trading.

Interest Rate: Until the position is closed, you will be liable for paying interest on the money you borrow from the broker.

Short Term: In order to profit from market volatility, margin trading is commonly used for short-term trades, particularly intraday or swing trading.

Restricted Shares: Not all stocks are permitted for margin trading. Brokers usually only allow this facility for liquid stocks.

Benefits of Using Margin Trading

The significant benefits of margin trading are as follows:

Higher Returns: Large positions can be taken on by traders with limited funds. However, it also comes with a higher risk as margin trading increases the buying power of the trader.

Short Selling: Using margin trading, one can initiate short positions in the futures by paying a limited margin, which allows traders to profit from bearish markets.

Frequent Trades: In Intraday Trading margin trading is particularly helpful because it enables traders to take multiple positions in a single day and profit from short-term price changes without using up all of their capital.

Diversification: Margin Trading allows you to spread risk by investing in a number of stocks or industries instead of putting all of your money into one.

On a concluding note, margin trading is a very effective tool enabling an investor to enhance their return with limited capital. One can increase their purchasing power multifold. However, margin trading comes with various risks; therefore, it requires a disciplined approach, effective risk management, etc. Therefore, it is advisable to first learn about margin trading and consult your investment advisor before initiating any trade in order to avoid losses.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Can I use margin trading in the derivative segment?

Most brokers do not offer margin trading facilities for trading in futures and options.

What will happen if I am unable to fulfil a margin call?

If you are unable to fulfil your margin call, then your broker will automatically square off your position.

What is the full form of MTF in the stock market?

MTF refers to “Margin Trading Facility”. It allows a trader to execute a trade without paying the full value of the trade; only a fixed percentage of the trade value is to be paid by the trader upfront.

Does every broker offer margin trading?

No, not every broker offers margin trading. Therefore, you need to check with your broker whether they offer this facility or not. Pocketful offers its users a margin trading facility.

How long can I hold a trading position made via margin trading?

The holding period depends on your broker policy, so compare the margin trading facility rules of various brokers before selecting a broker.

In today’s world, silver is not only a precious metal but also a critical material used in various industries such as solar, electric vehicles, electronics, etc. Therefore, as an investor, you must be thinking about how to invest in silver-related stocks for better returns.

In this blog, we will give you an overview of top silver stocks along with the benefits of investing in them and key performance indicators.

What are Silver Stocks?

Silver stocks are shares of companies primarily engaged in exploration, mining, production, and selling silver. Silver and its related products are a major source of revenue for these companies. Their profit is dependent on production costs and operational efficiency. Investing in these shares can give one indirect exposure to the silver industry.

An overview of the best silver stocks in India is given below:

1. Hindustan Zinc Limited

Hindustan Zinc Limited was established in 1966 by Metal Corporation of India. Initially, it was a public sector undertaking established to fulfil the demand for zinc in India. In 1980, after realising the increasing demand for silver, the company invested in refinery technologies to extract silver. In 2002, the government decided to divest this company and sold the majority stake to Sterlite Opportunities Limited, a subsidiary of Vedanta Limited. However, the government retains nearly 29.54% with itself. Today, the company is India’s largest integrated silver producer and sells silver as 30 kg bars, 1 kg bars and in powder form. The company’s headquarters are situated in Rajasthan.

Vedanta Limited was founded in 1986 under the name Sterlite Industries (India) Limited and was initially focused on producing wires and cables for the telecommunication sector. In 1992, the company decided to enter into the refinery business and started smelting copper. The company formed a parent company in the United Kingdom known as Vedanta Resources Limited, and this company was listed on the London Stock Exchange. The company is a prominent player in the Indian mining industry. The company purchased Sesa Goa Limited in 2007. It also acquired the business of Carine India, which was a prominent player in the gas industry. Vedanta Limited holds a 64.9% stake in Hindustan Zinc Limited (HZL), which ranks as the world’s 5th largest silver producer. In FY2023, HZL reported an impressive annual silver production of approximately 714 tonnes. The company also owns mines in South Africa. The company’s headquarters are situated in Mumbai.

Founded in 1993 by T.S. Kalyanaraman, Kalyan Jewellers India Ltd. is a prominent name in the jewelry industry, offering an extensive range of gold, silver, and precious stone jewelry. The company operates on a customer-centric business model focused on transparency, quality, and variety. One of its key differentiators is the wide selection of designs backed by unmatched warranties. To strengthen its presence in smaller towns, Kalyan Jewellers has launched the unique “My Kalyan” program, which operates through over 750 centers across India. This initiative significantly enhances customer outreach and plays a major role in expanding the brand’s market footprint.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

36.34%

311.20%

573.02%

(As of 05th January 2026)

4. Goldiam International Limited

The company was founded in 1986 as Goldiam (International) Private Limited. Initially, the company began its work as an exporter of cut and polished diamonds and jewellery. It received Export Performance Awards in 1991. They regularly pay dividends and bonuses to their shareholders. However, because of lower margins, the company exited its wholesale business in Hong Kong and India. During 2023-24, the company announced its venture into the retail sector. The company has its headquarters in Mumbai.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-15.53%

166.12%

687.28%

(As of 05th January 2026)

5. Thangamayil Jewellery Limited

The company was established in 1947 and was initially known as Balu Jewellery. It was founded by the Late Shri. N. Balusamy Chettiar. In 1979, the business was handed over to the son, Mr. Balarama Govinda Das, Mr. Ba. Ramesh and Mr. N.B. Kumar. The company formally began its operation in 2000 when it was incorporated as Thangamayil Jewellery Private Limited. The company launched its IPO in 2007 and became a publicly traded company. The company’s headquarters are situated in Tamil Nadu.

The significant benefits of investing in silver stocks are as follows:

Portfolio Diversification: One can diversify their portfolio by investing in silver stocks.

Increasing Demand: The demand for silver is increasing due to its industrial applications and precious metal status. Therefore, investing in these companies can be considered a good investment opportunity.

No Physical Storage: One is not required to buy and store physical silver and can get the benefit of the appreciation in the price of silver.

Regular Income: Some companies discussed above regularly declare dividends, which can be a source of passive income for investors.

Factors to Consider Before Investing in Silver Stocks

The factors which need to be considered before investing in silver stocks are as follows:

Company Financials: Before making any investment in silver stock, one needs to evaluate the financials of the company, such as revenue growth, profit margins, debt levels, etc.

Geopolitical Risk: The prices of silver are highly volatile as geopolitical events impact the share prices of silver companies.

Demand from Industrial Sectors: Silver is widely used in industries such as solar energy, electronics, and electric vehicles. Monitoring the demand trends in these sectors can help you assess future growth potential for silver-related companies.

Government Policies and Import/Export Regulations: Changes in government policies, import/export duties, or environmental regulations can significantly impact silver production and profitability of these companies.

The future of silver stocks is very promising in India because the demand for silver is increasing day by day, due to its industrial applications, especially in the green energy sector. With the rise in the use of electric vehicles, the demand for silver will increase because electric vehicles use silver. Along with this, the government is also pushing clean energy adoption, in which silver plays an important role. Therefore, one can invest in silver stocks for the longer horizon.

Conclusion

On a concluding note, investment in silver stocks provides you with an opportunity to earn profit from the increasing price of silver. Investment in silver stocks offers a mix of capital appreciation, inflation hedging, and participation in the renewable energy sector. However, the performance of silver companies depends on the global prices of silver, which can be very volatile because of various factors such as geopolitical events, demand for silver, etc. Therefore, it is advisable to consult your investment advisor before making any investment in silver stocks.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Which stocks are associated with silver in the Indian stock market?

Some commonly traded silver stocks in India are Hindustan Zinc Limited, Vedanta Limited, Kalyan Jewellers India Ltd., Goldiam International Limited, and Thangamayil Jewellery Limited.

Do silver stocks pay dividends?

Yes, some silver stocks pay dividends. However, one needs to check the dividend yield of the company before making any investment. Dividend-paying silver stocks are suitable for investors who are looking for a passive income.

What are the major risks of investing in silver stocks?

The major risks related to investing in silver stocks are volatility in the global price of silver, geopolitical risk, environmental regulations, etc.

How can I invest in silver stocks in India?

One can easily invest in silver stocks by opening a demat and trading account. You can easily open a demat account with Pocketful, and you also don’t need to pay any brokerage on equity delivery trades.

What is a good time to invest in silver stocks?

You can invest in silver stocks at any time as it offers diversification; however, certain factors need to be considered before investing in silver stocks, such as silver price trends, macroeconomic factors, etc.

Earlier, whenever you went out for shopping or dinner, you probably carried physical cash to make payments. However, with the launch of UPI or Unified Payment System by NPCI (National Payments Corporation of India) in 2016, things have changed drastically. Now, you can make all kinds of payments through your UPI mobile application. But sometimes the payment gets stuck. In that case, the user must know how to file a UPI complaint.

In this blog, we will explain to you how to register a UPI complaint and what details are required to raise a complaint.

What is UPI Payment?

UPI or Unified Payment Interface allows a user to make payments on a real-time basis. This system was developed by the National Payments Corporation of India (NPCI) in 2016. NPCI is regulated by the Reserve Bank of India. This system has changed the landscape of the Indian payment system. One can easily transfer the funds using their mobile 24*7, UPI even works on holidays.

Features of UPI Payment

The key features of UPI are as follows:

Immediate Transfer: One can easily transfer money in real time, which makes UPI a preferred way of making payments today.

Convenient: An individual doesn’t need to worry about carrying physical cash or going through the hassle of finding change, as UPI allows you to transfer the exact amount easily.

Link Multiple Bank Accounts: One can easily link their multiple bank accounts to a single UPI ID.

QR Code: Using UPI allows one to easily transfer money without sharing any bank details. Scanning a QR code, one can instantly transfer the money.

Cost-efficient: UPI transactions are free for most users, especially those involving direct bank-to-bank transfers. However, a 1.1% interchange fee may apply to transactions over ₹2,000 made using Prepaid Payment Instruments (PPIs) such as digital wallets. This fee is paid by the merchant, not the customer.

Secure: The use of two-factor authentication allows you to securely transfer money to other users.

The common issues with the UPI payments are as follows:

Failed Transaction: In a failed transaction, the amount is deducted from the bank of the payer, but it does not get credited to the bank of the receiver. It generally happens because of network errors or server issues.

Payment Decline by Bank: Your payment can be declined by the bank because of several reasons, such as invalid UPI PIN, insufficient balance, etc.

Failed UPI Registration: There are some cases when the user is not able to register themselves on the UPI application, due to inactive SIM, etc.

Daily Limit: UPI generally has a daily transaction limit. If the limit has been exceeded by the user, then further payments cannot be made.

Bank Server: Sometimes the bank server does not respond or faces some issue; during such times, the payments cannot be made.

How to Register a UPI Complaint?

One can easily raise a UPI complaint following the mentioned steps:

UPI Application: The UPI application, which you were using, allows you to file a complaint and report fraud through the in-app complaint or help section.

NPCI Website: Alternatively, you can visit the website of NPCI, and go to the “Dispute Redressal Mechanism” section and file your complaint.

Customer Care: One can reach out to the customer support department of the company offering UPI services via the helpline provided on their website or application.

Bank: The user can also contact their banks regarding the rejection of UPI payment and can file a complaint for the same.

There are a few details that one should keep handy while registering a UPI complaint.

Registered Mobile Number.

Transaction ID or UTR (Unique Transaction Number).

Date and Time of Transaction.

Amount of Transaction.

Details of the beneficiary account to which you were making the payment.

Error message or screenshot.

Having these details handy can make filing a UPI complaint much easier.

Checking Status of UPI Complaint

One can easily track the status of their UPI complaint online by following the steps mentioned below:

NPCI Website: To check the status of a complaint made on the NPCI website, one can click on the tab “Click here to check the complaint status” and choose their product type, bank and enter CRN number.

UPI Application: If the complaint has been made through the UPI application, then one can track the status of their complaint on the help and support section of the UPI application.

Bank: If you have filed a complaint through the bank, then you can visit the branch or call their customer support number and ask them about the status of your complaint.

On a concluding note, UPI, or Unified Payment Interface, has transformed the way people make payments and shop in India. Now you do not need to carry physical cash while travelling; you can just pay or transfer an amount using the UPI application installed on your mobile phone. However, sometimes the users also face minor difficulties, such as payment being deducted but not credited to the receiver’s account, etc. In this case, you do not need to worry and can easily file a complaint through various modes and get a resolution. However, it is advisable to carefully select a reliable UPI application to avoid any fraud.

Frequently Asked Questions (FAQs)

What is the full form of UPI?

UPI refers to Unified Payment Interface, which NPCI launched to digitise the payment ecosystem.

What type of UPI complaint can I raise?

One can raise complaints about money debited from one’s bank account but not credited to the receiver’s account, a failed transaction, a payment made to the wrong person, or an unauthorized transaction.

Where can I file a complaint about UPI payments?

One can file a complaint on the official website of NPCI, the UPI application, and with your bank.

Where can you check the status of a UPI complaint?

The status of the UPI complaint can be checked on the official website of NPCI or the UPI application

Where to escalate the UPI complaint?

The UPI complaint can be escalated to your bank grievance portal, NPCI portal, or the banking ombudsman.

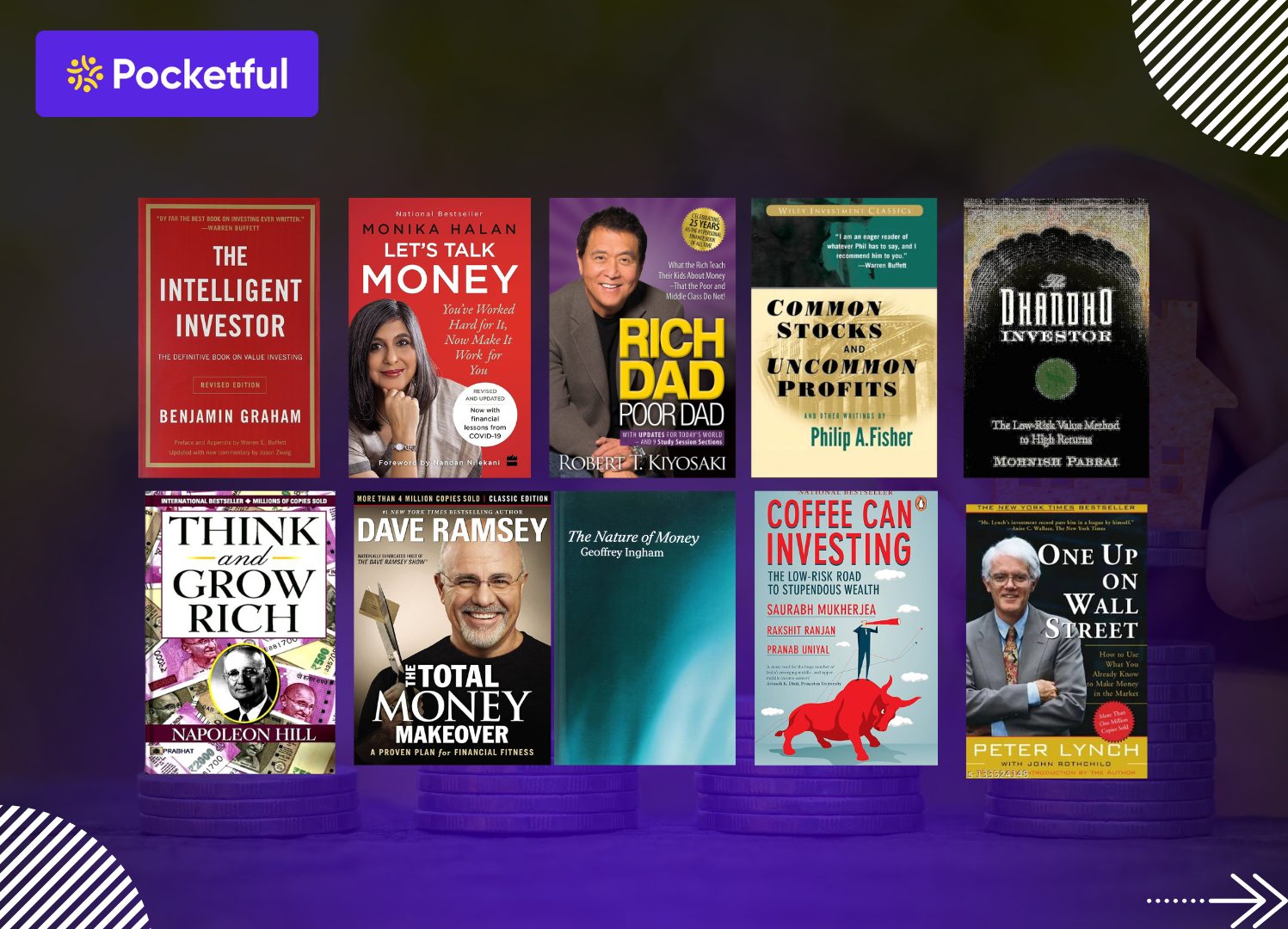

Mastering personal finance is key to building wealth, avoiding debt, and achieving financial freedom. The right books can transform your mindset and guide you toward smarter money decisions. Here, we’ve handpicked the 10 best personal finance books that offer timeless strategies and practical insights to help you take charge of your financial future.

In this blog, we will give you an overview of the top 10 personal finance books.

Top 10 Personal Finance Books

S.No.

Book Name

Year

Author

Rating (Goodreads)

1

The Intelligent Investor

1949

Benjamin Graham

4.3

2

Let’s Talk Money

2018

Monika Halan

4.3

3

Rich Dad Poor Dad

1997

Robert T. Kiyosaki

4.1

4

Common Stocks and Uncommon Profits

1958

Philip A. Fisher

4.2

5

The Dhandho Investor

2007

Mohnish Pabrai

4.3

6

The Nature of Money

2011

Geoffrey Ingham

3.9

7

One Up on Wall Street

1989

Peter Lynch

4.3

8

Think and Grow Rich

1937

Napoleon Hill

4.2

9

Coffee Can Investing

2018

Saurabh Mukherjea

4.2

10

The Total Money Makeover

2003

Dave Ramsey

4.3

Overview of the Top Personal Finance Books

1. The Intelligent Investor

This book was written by Benjamin Graham and was published in 1949. Benjamin Graham is known as the father of value investing. In this book, he explains key characteristics of an investor that separates them from a speculator. The book emphasises long-term investing and suggests that an intelligent investor ignores the mood of the market and only trades when there are favourable prices. He said investing is not a get-rich-quick scheme but a serious business. Considered a must-read by many, The Intelligent Investor remains one of the most influential finance books ever written.

2. Let’s Talk Money

The book was written by Monika Halan, who is a renowned financial journalist. The book is divided into three parts: building the foundation of a financially sound life, creating wealth, and getting wealthy. This book is written in an easy to understand language that can help an individual make informed decisions related to different stages of life. She covers essential topics such as budgeting, emergency funds, insurance, retirement planning, and choosing the right investment products suited to individual goals and risk profiles.

3. Rich Dad Poor Dad

This book was written by Robert T. Kiyosaki and was published in 1997. In this book, the author has explained his life experience of the difference in mindset between his biological father, who was poor and the father of his best friend, who was very rich. Through their contrasting approaches to money, he highlights the difference in mindset between working for money and making money work for you. Kiyosaki encourages readers to break free from the traditional cycle of earning, spending, and saving, and instead focus on building assets that generate passive income. This book emphasises how financial literacy and self-belief help you in creating wealth.

4. Common Stocks and Uncommon Profits

The book was first published in 1958 and was written by Philip A. Fisher. In this book, Fisher focuses on a growth-oriented approach to investing, which was based on qualitative analysis, i.e., analysing company’s management, its capacity for innovation, competitive advantages, and long-term vision. It remains a must-read for anyone interested in growth investing and learning how to identify outstanding companies before they become widely recognized.

5. The Dhandho Investor

The book was written by Mohnish Pabrai, who was the founder of Pabrai Investment Fund. The book was published in 2007. The writer introduces the “Dhandho” approach of investing, which means investing in simple, predictable businesses. According to the book, one should not invest in futuristic ideas; instead, invest in businesses which have a proven track record. The principles of investing discussed in this book are similar to those used by Benjamin Graham and Warren Buffett.

6. The Nature of Money

Written by Geoffrey Ingham and published in 2004, this book offers a unique and thought-provoking perspective on what money truly is. Ingham challenges the traditional economic view of money as merely a neutral medium of exchange. Instead, he explores money as a social construct, emphasizing its role in shaping relationships of credit and debt within society. This book dives deep into the sociology and politics behind money, providing readers with a richer, more nuanced understanding of how modern financial systems operate. It’s an essential read for anyone interested in exploring the foundations of money beyond conventional economic theories.

7. One Up on Wall Street

This book was written by Peter Lynch and published in 1989. Peter Lynch is a successful mutual fund manager. He managed various Fidelity Magellan Funds from 1977 to 1990, and achieved an annualised return of 29%. In this book, he emphasises the importance of daily observation of individual investors, which they can use to find common and promising investment opportunities. Focusing on the principle of “Invest in what you know”, the author believes that anyone can discover great stocks before they’re widely recognized by analysts.

8. Think and Grow Rich

This book was published in 1937 and was written by Napoleon Hill. Based on decades of studying the habits and mindsets of highly successful people, the book is much more than a guide to earning money; it’s a blueprint for achieving success in any area of life. Napoleon interviewed several successful people and found some common characteristics, which are mentioned in the book. Once you finish reading this book, you will get to learn the psychology of creating wealth.

9. Coffee Can Investing

The book was written by Saurabh Mukherjea, Rakshit Ranjan, and Pranab Uniyal, and it was published in 2018. In this book, the authors discusses a long-term approach to wealth creation, especially tailored for Indian investors. The authors introduce the concept of “Coffee Can Investing,” inspired by an old American practice where people would stash valuable possessions in a coffee can and forget about them for years. In investing terms, this means identifying high-quality, fundamentally strong stocks and holding them untouched for at least 10 years.

10. The Total Money Makeover

The book was first published in 2003 and was written by Dave Ramsey. The book provides steps to get out of debt and build wealth. Ramsey emphasizes that successful money management is 80% behavior and the remaining 20% consists of knowledge. The author discusses a “Debt Snowball” method of repaying their smallest debts first, building momentum towards saving and investing, allowing you to eliminate debt and achieve financial freedom.

Why should one read Personal Finance Books?

There are various reasons why one should read a personal finance book, a few of which are mentioned below:

Avoiding Debt Traps: Reading books allows you to manage your debt efficiently. These books can help you reduce debt, create realistic budgets and build a more secure financial future.

Long Term Wealth Creation: Reading books helps you create wealth over a while by teaching you the importance of disciplined investing.

Change in Mindset: Many people avoid investing early in life, missing out on substantial gains from the power of compounding. Books help them in understanding the concept of compounding.

Financial Freedom: Reading books regularly allows you to attain financial freedom at an early stage and provides you with peace of mind.

Conclusion

While earning money is challenging, managing it wisely requires even greater skill and discipline. Many seasoned investors have shared their experiences through books, offering valuable insights on navigating the market and aligning your investments with your financial goals and risk tolerance. However, it’s important to remember that these books provide general guidance and should not be seen as direct investment advice. Always consult a qualified financial advisor before making any investment decisions.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

There are various books available through which one can learn the art of investing; however, one can start with “The Intelligent Investor” written by Benjamin Graham.

Is there any book that can help me get out of debt?

Yes, books like “The Total Money Makeover” focus on budgeting and managing your debt.

Do I need to have a financial background to read personal finance books?

No, you do not need to have a financial background to understand the concepts discussed in the personal finance books, as they are written in simple language and explain the concept through real-world examples.

Where can I purchase personal finance books?

One can purchase personal finance books on online platforms such as Amazon, Audible, and Google Play Books.

Is there any personal finance book specifically for the Indian audience?

Yes, there are various books written by various authors that can help an Indian investor in understanding the concepts of personal finance. Examples of such books are “Coffee Can Investing”, “Think and Grow Rich”, etc.

Artificial Intelligence (AI) is rapidly changing the world of investment in India. By 2025, spending on AI in India is estimated to reach around ₹ 14,300 crore, showing a growth of more than 31% year-on-year (IDC report). At the same time, individual investors are now also using data analytics and machine learning to better understand market trends.

In this blog, we will explain to you in simple language how you can make your investments even smarter, faster and more accurate by using AI.

AI in Investing

AI (Artificial Intelligence) means programming machines with the ability to think and make decisions like humans. ML (Machine Learning), a subset of AI, learns from data provided. Deep Learning is an advanced form of ML that uses artificial neural networks and tries to work a little like our brains.

1). How is AI different from traditional tools?

Earlier, screeners and algorithms picked stocks based only on predefined financial rules (such as the P/E ratio).

But now, AI-powered tools understand sentiment, scan news, technical and fundamental data in real-time, and create strategies on their own and moreover, they can also identify market patterns. This reduces the scope of human error and emotional decisions.

2). AI: Real-World Applications

Robo-advisors: These are AI-based advisors that understand your risk appetite, goals, and financial habits and guide you in investing.

Sentiment Analysis: AI analyzes investor sentiment from Twitter, news, Reddit—for example, when the Adani-Hindenburg controversy happened, AI-based sentiment tools were able to detect sentiment changes and predict price fluctuations quickly.

Portfolio Optimization: AI can easily balance portfolios, manage risks, and detect frauds with ML and predictive analytics.

Today’s investor is not limited to just charts and ratios. AI is now playing a broader role making decision-making at every stage faster, personalized, and more data-driven. Let us evaluate the role of AI in the investment process based on different metrics mentioned below:

1). How is AI changing the Research Process?

The traditional research process was time-consuming and subject to personal bias. AI is making this process automatic, neutral, and much more in-depth. Many of today’s AI tools can scan everything from financial documents to CEO statements.

For example, NLP-based systems can analyze management discussion and analysis (MD&A) sections in the annual reports and guess whether their tone is bullish or bearish.

2) How does AI make Portfolio Management easier?

Every investor’s financial goal, risk-taking capacity, and holding period are different. AI can create tailored portfolios based on investor’s individual preferences.

Through data analytics, AI decides how much should be invested in which asset class — equity, debt, gold or international funds.

Mutual Fund houses like Nippon India are now integrating AI into their smart asset allocators, which reallocate portfolios as per market changes.

Also, smart-beta ETFs and factor-based investment plans are growing rapidly in India, which are based on indicators such as volatility, quality, and momentum selected by AI.

3). How is AI making Risk Management more accurate?

Financial frauds, extreme volatility, and behavioral biases all of these can impact an investor’s portfolio. AI provides real-time solutions to all of these.

Many SEBI-registered fintech platforms in India are now using AI to track transaction patterns and report any unusual behaviour immediately.

In the banking sector, credit card companies are now using AI-based behavioral scoring to assess a person’s repayment capacity taking into account real-time spending behavior, not just income or CIBIL score.

NBFCs and digital lending apps are also now using neural networks and decision trees instead of traditional ratio models for risk estimation.

4). How does AI read News and Market Sentiment?

Markets today are not just driven by numbers; emotions, Twitter trends, media coverage and global events also influence investment decisions.

Sentiment analysis tools like FinBERT can now analyze social media and news data to determine public sentiment about a company or sector.

These tools not only provide scores, but also suggest which sectors are seeing a sudden surge in interest or a decline.

For example, when the report concerning the Adani Group was published in 2023, many sentiment trackers had already indicated a negative trend, allowing proactive decisions to be taken.

Let us look at the AI based investment platforms that are popular in India:

Smallcase : Smallcase is a unique platform where you can invest directly in stock portfolios created by InvestorAi, Wright Research, etc. These smallcase fund managers create investment portfolios based on suggestions from AI-powered robo-advisors scanning real market data.

Jarvis Invest : Jarvis is an advanced robo-advisory platform that suggests smart stock recommendations based on your risk profile, age, and financial goals. The platform dynamically manages the portfolio by processing real-time data.

ET Money Genius : ET Money Genius is a new AI-powered feature that suggests a customized portfolio strategy based on the user’s financial goals and risk profile. It offers weekly rebalancing, downside protection and smart asset allocation.

Limitations, risks and ethical concerns in AI investments

Some of the risks, limitations and ethical concerns regarding use of AI in making investments is given below:

Incomplete and Biased Data : AI models are often trained on historical data. If this data is biased or incomplete, the model may incorrectly predict future trends. This can lead to wrong investment decisions, increasing the likelihood of losses.

False Signals due to Noise : There is a lot of noise in short-term price movements in the stock market. Sometimes AI interprets this noise as a meaningful signal, which can lead to incorrect buy/sell suggestions especially in high-frequency trading.

Blind Reliance Without Human Judgment : AI-based tools are powerful, but relying on them blindly can be dangerous. AI cannot understand financial statements, news context or geopolitical events as well as humans do currently. Therefore, the investor should also do some analysis and check AI recommendations before investing.

Lack of Regulatory Clarity (in India) : SEBI has not yet fully implemented any dedicated framework governing AI trading or robo-advisory.

Ethical Concerns: Users often do not understand how AI algorithms work. If a wrong decision is made, the resulting trades can contribute to market volatility or unintended price movements.

Data Privacy & Cybersecurity Risks : AI platforms get sensitive information from users such as financial data, income information and investment habits. If this data is not encrypted or protected properly, hackers can misuse it. Apart from this, investor accounts may also be at risk of cyber-attacks.

Now let us evaluate the future of AI in Indian stock market:

SEBI’s AI-ML Guidelines : In June 2025, SEBI released a consultation paper for AI/ML use, focusing on five key aspects: Model Governance, Mandatory Disclosure, Continuous Testing, Bias Control, and Data Security. These rules are a step towards making areas like investment advice, robo-advisory, algo-trading transparent, fair and secure.

Opening the door for retail investors to algo trading : Another proposal from SEBI came in April 2025—in which there was a discussion on allowing retail investors to do algorithmic trading. Now, even retail investors can connect their AI based stock recommendation algos with their broker APIs and do algorithmic trading.

SEBI implements AI Accountability for Regulated Intermediaries : The new SEBI regulations of February 2025 holds market infrastructure institutions and intermediaries (such as advisory firms, brokerages) accountable for any consequences arising from AI use—this includes responsibility for ensuring data security and outputs resulting from operations and client services. This means, if an AI model executing trade causes high volatility in stock prices, then the platform will be held responsible.

RBI’s AI-Ethics and Security Framework (‘FREE-AI’) : In December 2024, RBI formed its ‘FREE-AI’ committee which will ensure ethical and responsible use of AI in the financial sector , This will also impact banking and payment platforms, creating a strong AI-governance ecosystem.

AI is slowly becoming the most powerful ally of investors for various applications such as data analysis, personal financial planning, or forecasting trends. But with this growing influence of technology comes the need for prudence, regulation, and data security. As much as investors embrace AI, it is equally important to choose the right platform, understand data privacy, and avoid misconceptions. In the times to come, AI will not only make investing easier but also more responsible and secure. It is advised to consult a financial advisor before making any investment decision based on AI recommendations given by platforms.

Frequently Asked Questions (FAQs)

Can I use AI tools for investing even if I’m a beginner?

Yes, many AI-based platforms such as robo-advisors are created for beginners, which give stock suggestions and data analysis.

Is AI-based investing 100% safe?

No, every AI stock recommendation tool carries some risk as incorrect data or biased models can cause losses.

Does SEBI allow AI-based trading in India?

Yes, SEBI has made some rules for AI and algo trading and now this path is opening for retail investors as well.

How does AI help in portfolio management?

AI analyzes your investment patterns, risk profile and market data to give smart portfolio suggestions.

Is my financial data safe with AI platforms?

Reliable platforms take care of encryption and data safety, but you should definitely read the privacy policy and check whether the platform is SEBI-registered or not.

If you’re looking to gain exposure to the sugar industry in India, investing in sugar penny stocks can be an intriguing option. These low-priced stocks often come with high growth potential but they also carry significant risk. Investors generally get confused about what factors they should consider before investing in penny stocks.

In this blog, we will give you an overview of the best sugar penny stocks in India, along with the factors to consider before investing in them.

What are Sugar Penny Stocks?

Sugar penny stocks are stocks of companies primarily engaged in producing and distributing sugar, sweeteners and other related products. They are known as penny stocks because their share prices are generally below a hundred rupees. They also sell ethanol as a by-product of sugar processing. These stocks carry high risk and are preferred by the investor who wishes to take high risk for high returns. Sugar production contributes a significant portion to the country’s GDP.

S.No.

List of Sugar Penny Stocks

1

Dwarikesh Sugar Industries Limited

2

Shree Renuka Sugars Limited

3

Bajaj Hindusthan Sugar Limited

4

Ugar Sugar Works Limited

5

The Andhra Sugars Limited

6

Rajshree Sugars & Chemicals Limited

Market Information of Sugar Penny Stocks

Company

Current Market Price (in INR)

Market Capitalisation (in INR crores)

52-Week High (in INR)

52-Week Low (in INR)

Shree Renuka Sugars Limited

24.9

5,296

24.9

22.8

Bajaj Hindusthan Sugar Limited

16.3

2,087

29.6

15.6

The Andhra Sugars Limited

73.2

993

91.5

63.3

Dwarikesh Sugar Industries Limited

34.2

633

52.6

32.1

Ugar Sugar Works Limited

37.3

420

53.5

35.8

Rajshree Sugars & Chemicals Limited

29.6

97.9

54.4

28.8

(Data as of 05 February 2026)

Best Sugar Penny Stocks – An Overview

An overview of the best sugar penny stocks is given below:

1. Shree Renuka Sugars Limited

In 1995, Narendra Murkumbi and his mother, Vidya Murkumbi, founded Shree Renuka Sugars Limited. The manufacturers refine sugar and also engage in the production of ethanol and power generation. The company is also engaged in sugar, coal, and molasses trading. Owns and distributes a popular sugar brand known as Madhur. In 2006, the company signed an MoU with a Brazilian sugar company and emerged as the largest sugar exporter from India. It has its headquarters in Mumbai.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-32.92%

-46.69%

147.54%

(Data as of 05 February 2026)

2. Bajaj Hindusthan Sugar Limited

Bajaj Hindusthan Sugar Limited was founded by a freedom fighter turned businessman named Shri Jamnalal Bajaj on 24 November 1931. The company opened its first plant at Gola Gokaran Nath in Lakhimpur Kheri. Initially, the company’s cane crushing capacity was 400 tonnes per day; later it was increased to 1,36,000 tonnes per day. The company has four production plants situated in Pratappur, Rudauli, Kundarkhi, and Utraula in Uttar Pradesh. The company headquarter is situated in Maharashtra.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-39.85%

15.96%

144.03%

(Data as of 05 February 2026)

3. The Andhra Sugars Limited

Andhra Sugars Limited was incorporated in August 1947 by Dr. Mullapudi Harishchandra Prasad. The company commenced its first sugar factory at Tanuku with a crushing capacity of 600 tonnes of sugarcane. The diversified its business into the chemicals sector. The company commissioned another plant in 1997 as the Taduvai Sugar Plant. The company’s headquarters are situated in Andhra Pradesh.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-18.33%

-42.96%

14.84%

(Data as of 05 February 2026)

4. Dwarikesh Sugar Industries Limited

Dwarikesh Sugar Industries Limited was incorporated in 1993. They got their first sugar plant commissioned in 1995 at Dwarikesh Nagar. The founder of the company is Mr. Gautam R. Moraka. The company primarily focuses on sugar and ethanol production. The company launched its IPO in 2005 and raised capital to increase its production capacity. The company had two plants, which began supplying surplus power to the state grid. The company’s headquarters are situated in Maharashtra.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-30.83%

-61.71%

21.81%

(Data as of 05 February 2026)

5. Ugar Sugar Works Limited

Ugar Sugar Works Limited was founded in 1939 and is one of India’s oldest sugar companies, founded by Shri V.S. Shirgaokar. In 1940, the Shirgaokar Brothers took the management into their own hands and took the company to new heights. The company established its first plant in Karnataka, and later diversified into distilleries and power generation. The company produces white crystal sugar of various grades such as M-30, S-30, and SS-30. The company has its headquarters in Karnataka.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-28.24%

-57.65%

128.31%

(Data as of 05 February 2026)

6. Rajshree Sugars & Chemicals Limited

Rajshree Sugars & Chemicals Limited was incorporated in 1985 by G. Varadaraj. The company has four refineries in Tamil Nadu. The company primarily focuses on the manufacturing of sugar and its by-products. The company recently acquired Trident Sugars. The company has its headquarters in Tamil Nadu.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-44.95%

-35.11%

88.10%

(Data as of 05 February 2026)

Key Performance Indicators (KPIs)

The key performance metrics of penny sugar stocks are as follows:

The significant benefits of investing in penny stocks are as follows:

Global Demand: Sugar tends to have consistent demand, as it is less sensitive to economic fluctuations compared to other commodities. Therefore, these companies have a stable revenue.

Raw Material: Sugar is used as a raw material for the food and beverage industry. Additionally, with the growing cafe culture and processed food demand, the sector is poised for further growth.

By-products: The by-product of the sugar industry includes ethanol and power, which can also be an alternate source of income for the company.

Government Incentive: The Government introduces various incentives for ethanol blending, which can be beneficial for the sugar companies.

Factors to be considered before investing in penny sugar stocks

There are various factors to be considered before investing in sugar penny stocks, such as:

Financial Health: The company’s financial health must be checked before making any investment. Company’s revenues and profit margin play an important role in determining the company’s financial position.

Raw Material: The sugar industry’s performance depends on the sugarcane production and the monsoon.

Management: Check whether the company has a strong management team and a proven track record before making any investment.

Future of Penny Sugar Stocks

The government has implemented various initiatives to increase ethanol production, due to which the sugar companies will be direct beneficiaries. The government has announced a goal of 20% ethanol blending by 2030. Along with this, the food and beverage (F&B) industry uses sugar as a raw material, and with the expansion of the F&B industry, the sugar companies will continue to grow. Hence, we can say sugar penny stock will have a bright future.

On a concluding note, the sugar industry provides an opportunity to participate in the growing economy of the country, as India is the second-largest producer of sugar in the world. Sugar penny stocks are companies which are primarily engaged in the production of sugar and their by-products, including ethanol and power. However, investment in penny stocks comes with greater risk as they tend to be highly volatile and generally lack financial stability. Therefore, it is advisable to consult your investment advisor before making any investment decision.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

The sugar penny stocks carry high risks because they have low market capitalization or low liquidity, dependent on the weather, and are highly volatile.

Why are sugar penny stocks considered a good investment option?

India is the second-largest exporter of sugar in the world, and with the rise of the food and beverage industry, this sector will continue to grow in the future, as sugar is used as a raw material for this industry.

What are some of the sugar penny stocks in India?

Some commonly traded sugar penny stocks are Dwarka Sugar Industries Limited, Shree Renuka Sugars Limited, Bajaj Hindusthan Sugar Limited, Ugar Sugar Works Limited, The Andhra Sugars Limited, and Rajshree Sugars & Chemicals Limited.

Do sugar penny stocks pay dividends?

Generally, penny stocks do not give dividends as they generally reinvest the profits in the business to expand it. Investing in penny sugar stocks offers returns, if any, in the form of capital appreciation.

What are the factors to be considered while investing in penny sugar stocks?

Various factors need to be considered before investing in penny sugar stocks, such as their financial performance, revenues, business model, debt level, key performance ratios, etc.

Ever wonder how the Indian economy keeps growing, even if traditional banks aren’t able to reach every corner of the country? The answer lies within a vibrant segment of the Indian economy called the Non-Banking Financial Companies or NBFC sector. These are the silent champions bridging the financial gaps, empowering small and medium enterprises, and aiding millions of Indians in getting access to credit, loans, and other crucial financial services that were previously beyond their reach.

So, what are the NBFCs, and what makes their shares so attractive to investors? Let us explore the exciting world of NBFCs and understand their contribution toward India’s financial growth story.

What are NBFC Companies?

Non-Banking Financial Companies, or NBFCs are considered to be financial institutions which are registered under the Companies Act and governed by the Reserve Bank of India (RBI). For more context, unlike conventional banks, NBFCs do not possess a banking license and thus, cannot accept demand deposits from the general public. Regardless, they are crucial in the Indian economic landscape for issuing loans, advances, asset financing, hire-purchase, leasing, and even secondary market investment in securities.

Known for their innovation and flexibility in developing financial products, NBFCs tap into underserved markets catering to small businesses in rural regions and people with limited access to credit. Their growth has been rapid, NBFCs are accounting for more than a quarter of India’s total credit as compared to one sixth a decade earlier. NBFCs have become key drivers of economic growth and financial inclusion in the country in recent years.

Top 10 NBFC Sector Stocks List in India

Company Name

Current Market Price (₹)

Market Capitalization (in ₹ Crores)

52 Week High (in ₹)

52 Week Low (in ₹)

Bajaj Finance

947

5,88,275

979

642

Jio Financial ServicesLtd.

332

2,11,120

363

199

Indian Railway Finance Corporation Ltd.

138

1,80,149

229

108

Power Finance Corporation Ltd.

427

1,40,848

580

357

Cholamandalam Investment and Finance Corporation Ltd

1,561

1,31,278

1,684

1,168

Shriram Finance

682

1,28,175

730

493

REC Limited

396

1,04,144

654

357

Bajaj Housing Finance

122

1,01,446

188

103

Muthoot Finance

2,641

1,06,026

2,692

1,665

Sundaram Finance Ltd.

5,010

55,660

5,536

3,733

(Data as of 10 July 2025)

Overview of the Top 10 NBFC Stocks in India

An overview of the top 10 NBFC sector stocks in India is given below:

1. Bajaj Finance

It is one of the leading non-banking financial companies of India, it has over 101 million customers spread over 3800 towns. The company provides easy consumer, home, personal, gold, and auto loans to small businesses and rural consumers. Widely known for its quick loan approvals and strong digital presence, Bajaj Finance reported a valuation of 4.16 lakh crore in assets under management (AUM) and a 19% year-on-year increase in net profit for FY25 as of March 2025.

Along with generous dividends, the company distributed bonus shares as a reward to its investors. By prioritizing technology and customer relations, Bajaj Finance continues to grow and remains a favorite in the NBFC sector.

It is one of the rapidly growing NBFC in India, it provides services like loans, insurance, and wealth management for customers. It is a part of the Reliance Group and headquartered in Mumbai. Using new age technology, Jio Financial Services ensures seamless service delivery and customer support from any part of India. People have easy access to finance because of Jio Financial Services’s easy to use products and strong digital platforms. The company reported a net profit of Rs. 3.2 billion, marking strong growth for the FY25, alongside declaring its first-ever dividend. Jio Financial Services is rapidly gaining traction as an instant financial service provider for those looking for credit.

IRFC Ltd is one of the leading public sector companies in the country and is dedicated to providing financial assistance to various departments of the Indian Railways. IRFC was established in 1986, situated in New Delhi and is mostly owned by the Government of India. It is one of the public sector companies which announced the commencement of services for raising funds within the capital markets and financial institutions to aid in the procurement of railway projects, acquisition of rolling stock, and developing infrastructure. Through leasing and financing activities, IRFC remains a vital player in India’s railway sector. IRFC was granted Navratna status in March 2025, portraying the significance of the company’s performance. The company is trusted by people and has stability and reliability which draws in investors to get exposure to invest in the growing NBFC space.

It is one of the leading public sector financial institutions in India. It provides financing for projects in the power sector, including electricity generation, transmission, and distribution. It is based out of New Delhi and was set up in 1986. PFC is a major energy infrastructure development NBFC and is under the Ministry of Power.

The company has shown strong financial performance, low NPAs, and prominent participation in project financing for public and private sector borrowers. As of early 2025, PFC has reported a market cap of over ₹1.4 lakh crore along with a good dividend yield. Due to its strong presence and consistent track record in the power sector, it is a preferred investment for those seeking growth and stability.

One of India’s most prominent Non-Banking Financial Companies (NBFCs) that delivers comprehensive services like automobile loans, home loans, property loans, and financing for SMEs. It is associated with the Murugappa Group, headquartered in Chennai. The company has over 1,600 branches across the country and manages assets above ₹2 lakh crore.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

9.56%

145.47%

644.66%

(Data as of 10 July 2025)

6. Shriram Finance

It is the one of the largest retail Non-Banking Financial Company (NBFC) in India. It provides loans for commercial vehicles, two-wheeler and car purchases, housing, gold, and small business loans. Founded in 1979 and based in Chennai, the company has more than 3,200 branches and assets of ₹2.63 lakh crore under management. Shriram Finance serves millions of customers, even in rural and unbanked areas. It is the preferred choice for most investors in the NBFC sector due to its strong customer base and profitability.

It is one of the most prominent public sector financial companies in India, focusing on the financing power projects for generation, transmission, and distribution of electricity across India. Based in New Delhi, REC is instrumental in the development of electricity infrastructure in India and actively works with the government and private sector companies on energy projects. The company aims to provide ₹2.5 trillion for renewable energy projects till 2030.

The company also gives dividends, making it popular among investors seeking passive income . Investors looking to finance infrastructure in India will appreciate REC Limited for its strong history and strategically important position in India’s energy landscape.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-35.39%

305.87%

395.11%

(Data as of 10 July 2025)

8. Bajaj Housing Finance

A prominent lender in India’s housing finance sector providing home loans, loans against property, and lease rental discounting. It is a part of the Bajaj Finserv group and based in Pune. The firm is known for providing fast and reliable loan approval procedures due to its technology.

In FY25, Bajaj Housing Finance reported strong growth with net profit increasing by 25% to ₹2,163 crore and a year-over-year 26% growth of over ₹1.14 lakh crore in assets under management. The company’s gross NPAs stood at an impressive low of 0.29% as of March 2025, further it has operational efficiency and robust asset quality. Bajaj Housing Finance remains a good choice for investors looking for good returns and home buyers seeking reliable lenders.

It is India’s biggest gold loan Non-banking Financial Company, with its corporate office in Kochi and more than 4,800 branches in parts of the country. In addition to gold loans, Muthoot Finance has diversified its portfolio to include personal loans, business loans, money transfer services, insurance distribution, microfinance, and housing finance. Its business model focuses on quick disbursal, minimal documentation, and customer-friendly policies, making it a preferred choice among lower and middle-income households.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

45.27%

154.23%

142.13%

(Data as of 10 July 2025)

10. Sundaram Finance Ltd.

It is among the top rated NBFC in India and is located in Chennai, Tamil Nadu. Sundaram Finance deals strongly in vehicle and equipment loans, home loans, and also manages assets for both retail and corporate customers. It was started in 1954 and is well known for its strong management, robust asset quality, and regular dividend payouts.

Even though the NBFC sector faces challenges, Sundaram Finance maintained a healthy growth in asset under management, strong asset quality and high capital adequacy ratio. It is termed to be a stable company making it attractive for the investors in the financial sector of India.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

10.86%

169.73%

283.97%

(Data as of 10 July 2025)

Key Performance Indicators

Company Name

Basic EPS (₹)

Net Profit Margin (%)

ROE (%)

ROCE (%)

Bajaj Finance

268.94

24.05

17.20

46.79

JIO Financial ServicesLtd.

2.54

59.70

1.30

1.20

Indian Railway Finance Corp Ltd.

4.98

23.94

12.34

49.98

Power Finance Corp Ltd.

69.67

28.65

19.52

65.86

Cholamandalam Investment and FIn Corp Ltd

50.72

16.48

18.00

75.97

Shriram Finance

50.82

22.86

16.91

17.30

REC Limited

60.20

28.18

20.26

68.85

Bajaj Housing Finance

2.67

22.58

10.84

43.60

Muthoot Finance

132.84

26.47

18.15

47.55

Sundaram Finance Ltd.

170.53

21.36

14.24

49.87

(Data as of March 2025)

Advantages of Investing in NBFC Stocks

The advantages of investing in NBFC stocks is given below:

Ability To Reach Untapped Areas : NBFCs grant credit and give financial assistance to people as well as small businesses that are often neglected by traditional banks and this promotes NABARD’s financial inclusion policies, thus propelling the economy.

Better Interest Margins : NBFCs have the opportunity to charge higher loan rates relative to banks, which means greater net interest income and profits.

Varied Services : They provide a variety of services such as personal loans, motor vehicle loans, microfinance, and so on, which is beneficial since risks are diversified.

Less Rigid Operations and Quicker Expansion : Due to less stringent regulatory laws compared to banks, NBFCs are able to grow their operations and sell innovative financial products.

Significant Growth Opportunities : Investments in NBFCs is a lucrative opportunity for investors seeking stocks with growth potential as they are expanding rapidly and often outperform banks in profitability and asset growth.

Disadvantages of Investing in NBFC Stocks

The disadvantages of investing in NBFC stocks is given below:

Regulatory Risks : The NBFC sector faces the regulatory risk due to frequent changes made by the RBI, which can affect profit margins and affect business models.

Interest Rate Sensitivity : The stock value of NBFC is very sensitive to changes in interest rates. Increased interest rates would result in greater borrowing costs which, in turn, would hurt profits.

Credit Risk and Asset Quality : NBFCs are likely to incur higher defaults compared to banks.

Market Fluctuations and Liquidity Issues : NBFC stocks tend to be quite volatile, and their prices may plummet during market downturns or periods of liquidity pinch.

Conclusion

Investments in NBFC stocks help diversify portfolios as well as grow your wealth owing to new and innovative financial products provided by them. These stocks can be adversely affected by regulatory risks, changes in interest rates, credit risks, and more. One should analyze their advantages and disadvantages to capture the long-term potential of these stocks and can be a part of the expanding NBFC sector.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

An NBFC or a Non-Banking Financial Company is a company that operates like a bank that offers services of granting loans and other financial services but does not have a banking license and does not accept deposits from the public.

Who regulates NBFCs in India?

Majority of the NBFCs in India are governed by the Reserve Bank of India (RBI), which controls their registration, activities, and compliance with regulations governing them.

Why should one consider accumulating NBFC stocks?

NBFC stocks offer strong returns through exposure to high-growth sectors, diverse loan portfolios, and underserved markets, with flexible operations enabling faster expansion and better profitability than traditional banks.

What are some notable risks for investing in NBFC stocks?

The main risks would be regulatory changes, interest rate changes, potential credit losses from defaults, etc., exposing them to greater risk during recessionary periods.

How to identify the best NBFC stock in India?

Identify the NBFC stock that has strong business fundamentals, robust risk management systems and good track record.

The Indian securities market has witnessed several cases of large-scale manipulation over the years, and one of the most notorious among them is the K-10 scam, masterminded by stockbroker Ketan Parekh. This scam not only shook investor confidence but also wiped out an estimated ₹30,000 to ₹40,000 crore in investor wealth.

In this blog, we will give you an overview of who Ketan Parekh is and how he conducted scams in the Indian Market, leading to massive losses for Indian investors.

Who was Ketan Parekh and What was the K-10 scam?

Ketan Parekh was a stockbroker and was associated with NH Securities. He was also an associate of Harshad Mehta, who was a key figure behind the 1992 securities market scam. He was involved in a scam, which was also known as the “K-10 Stocks Scam”. In this scam, he identified 10 stocks that generally have low liquidity and manipulated their prices. He borrowed funds from Madhavpura Mercantile Cooperative Bank, created artificial demand, and generated hype in the media regarding these 10 stocks. He also conducted circular trading in which the buying and selling of stocks is conducted between related parties.

The stocks which were selected by Ketan were related to the IT and media sectors. In the pump and dump strategy adopted by Ketan Parekh, the prices of those 10 stocks were inflated artificially, and when the retail investor purchased those stocks, they were dumped by him.

How was the Ketan Parekh Scam Exposed?

The scam was exposed when the Securities and Exchange Board of India noticed some unusual price movements in a few selected stock prices. When the case was investigated by the SEBI, it was found that Parekh had taken a huge loan from the Madhavpura Mercantile Cooperative Bank. SEBI traced the circular trading between the Parekh firm and linked brokers.

Impact on the Securities market after the Ketan Parekh Scam

The stock market crashed after the 2001 Union Budget because the K-10 stocks crashed. Around 30 to 40 thousand crore of investor wealth was wiped out during such a correction. Retail investors faced a huge setback and lost faith in the market.

Another Scam by Ketan Parekh

After the 2001 K-10 scam, Ketan Parekh was barred from participating in the securities market. But despite this, he was involved in another front-running scam. A front-running scam is an illegal practice in which someone with insider information executes trades, through which they earn profit from the anticipated price movement a large order will cause.

Let’s understand the front running with an example: when a large buyer is about to execute a large trade, the front runners purchase the stock at a lower price and then sell it once the order is placed by the big buyer; thereby selling at a higher price and realizing quick profits. From this whole process, Ketan Parekh gained around ₹65.7 crore between 2021 and June 2023.

How was this Scam Exposed?

In early 2025, SEBI uncovered a sophisticated front-running operation led by Ketan Parekh, netting him approximately ₹65.7 crore. Parekh leveraged insider information, leaked by a Singapore-based intermediary about large institutional trades. Acting on real-time intelligence, his network placed strategic early trades ahead of these orders. As the institutional transactions hit the market and prices shifted, Parekh’s team swiftly profited. The investigation revealed a complex scheme involving multi-tiered trading structures, covert communications (via burner phones and WhatsApp), and even informal cash settlements.

SEBI tracked over 10 mobile numbers, which were saved under various names, including Jack, Boss, John, and Bhai, among others. By analyzing these calls and hotel check-ins, SEBI traced Ketan Parekh’s trading activities. SEBI’s fast, multi-location raids resulted in interim trading bans on Ketan Parekh and 10 other entities and ₹65.7 crore in liability against Parekh.

SEBI banned Ketan Parekh and 2 others from accessing the securities market and froze their trading accounts.

Lesson for Investors

There are certain lessons that an investor should learn from the scam of Ketan Parekh. A few such lessons are as follows:

Do not follow the trend: Generally, investors follow stocks that are hyped because of their constant rise in prices.

Stocks Trading at Upper Circuits: As an investor, it is advised to avoid stocks that constantly trade at upper circuits.

Low Liquidity: Generally, stocks that have low volume are easy to manipulate; therefore, one should avoid investing in stocks that have low liquidity.

Company Financials: Before investing in any stock, through research should be conducted, including an analysis of the company’s revenue, profits, debt, and other key financial metrics.

Conclusion

On a concluding note, we all know that investment in shares or equity helps us create wealth in the long run, but due to certain scams, such as the K-10 scam, investors lose confidence in the financial markets. Investors must stay vigilant, focus on strong fundamentals, and avoid shortcuts that promise quick gains. Always remember: informed, disciplined investing is the key to success. Therefore, it is advised to consult your investment advisor before making any investment decision.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Ketan Parekh is a former trader and investor who initially worked as a stockbroker in the Indian stock market. He was involved in two scams, the first one known as the K-10 Stocks Scam, and the second was a front-running case.

What is front-running?

Front-running is an illegal practice in which a trader buys specific securities before a large order is placed in those securities based on insider information. When the big orders are placed, the investor sells those securities at a higher price and makes illegal profits from it.

What are the major actions taken by SEBI against Ketan Parekh?

SEBI has barred Ketan Parekh from accessing the securities market and instructed him to return ₹65.7 crore earned illegally.

How can investors protect themselves from scams like Ketan Parekh’s?

Investors should research thoroughly, avoid hype-driven or low-liquidity stocks, focus on strong fundamentals, diversify investments, and consult a trusted advisor to reduce the risk of falling for scams.

Is Ketan Parekh still alive?

Yes, Ketan Parekh is still alive, and he is being investigated by SEBI in a new front running case.

Where is Ketan Parekh now?

Ketan Parekh is alive, recently arrested in 2025 for a ₹130 crore fraud. He is banned from the stock market, with his accounts frozen, and is currently in legal custody.

Imagine on a Sunday evening you’ve decided to cook a special dinner for your family. You have started preparing the meal, the pan is on the stove, the oil is sizzling, only to find that you’ve run out of few key ingredients required. The nearest kirana store is a 15 minute walk away, and you just don’t have the time.

Just a few years ago, this would have been a frustrating situation but today, you pull out your phone, tap a few buttons, and in less than 10 minutes, a delivery person is at your door with everything you require. In this blog, we will compare Blinkit and Zepto, the two major players in the Indian Quick Commerce segment.

Introduction to Quick Commerce

Think of it as e-commerce, but at a super-fast forward pace. It’s the business of delivering things you need, like groceries, medicines, and even electronics, to your doorstep in minutes, not hours or days.

And in India, it’s not just a new trend, it’s a revolution. The market has exploded from just $300 million in 2022 to a projected $7.1 billion by the end of 2025. That’s a 24-fold increase, and by 2030, experts believe it could be worth a massive $35 billion industry.

But why is this happening so fast, especially in India? There are a few simple reasons:

Fast Paced Life : In big cities like Mumbai, Bengaluru, and Delhi, life is fast. Juggling work, family, and traffic makes a quick trip to the store feel like a huge task. Quick commerce saves us precious time.

Young Population : Almost half of India’s population is under the age of 30. This young, tech-savvy generation grew up with smartphones and expects everything instantly.

Digital Power : With so many people using smartphones and UPI, ordering and paying for things online has become second nature. These digital facilities make quick commerce possible.

The COVID-19 Push : The pandemic changed our habits, many of us tried online grocery shopping for the first time. We got used to the convenience, and the habit stuck around even after lockdowns ended.

This isn’t just about getting your groceries faster. This massive shift shows that as a country, we are starting to value our time just as much as our money. The demand for instant services is a sign of a modern, developing economy, and it’s attracting investors from all over the world who see India’s potential.

At the heart of this revolution are two companies that have become household names : Blinkit and Zepto.

About Blinkit

Its story didn’t start with a 10-minute delivery app. In fact, it started way back in 2013 under a different name that you might remember as Grofers.

Founded by Albinder Dhindsa and Saurabh Kumar, Grofers was built for planned monthly grocery shopping. You’d make a list, place a big order, and get it delivered in a day or two. But as the market changed, Grofers didn’t have a choice other than to adapt to the changing market or become irrelevant.

In 2021, they made a bold move. They completely changed their business, rebranded to Blinkit, and made a new promise : delivery “in the blink of an eye”. This wasn’t just a new name. It was a complete transformation to fight in the new 10-minute delivery market. Then came the masterstroke, in 2022, the food delivery giant Zomato bought Blinkit for $568 million. This was a game changer as Zomato’s deep pockets and massive delivery army gave Blinkit the firepower it needed to scale up and dominate the market.

If Blinkit is the experienced veteran, Zepto is the young, fiery challenger who changed the game. It was founded in 2021 by Aadit Palicha and Kaivalya Vohra, two 19-year-old friends who dropped out of a prestigious computer science program at Stanford University to build their company in India.

Their big idea came from their own frustration during the COVID-19 lockdown. They saw that even online grocery orders were taking days to arrive. They realized that people really wanted groceries instantly.

So, they built a company around one simple, powerful promise : delivery in 10 minutes. They pioneered the “dark store” model in India, setting up a network of mini warehouses in dense neighborhoods to make these super fast deliveries possible.

Their idea was so powerful that it became an instant sensation. In less than two years, Zepto became a “unicorn,” a startup valued at over $1 billion. They didn’t just build a successful company, they set a new standard that forced established players like Blinkit to completely reinvent themselves.

So, when you’re hungry and need something fast, which app should you open? Let’s break it down.

The Core Battleground: Service, Speed, and Selection

Here is a quick look at how the two services compare on the things that matter most to you.

Features

Blinkit

Zepto

Delivery Time

Promises 10-15 minute delivery. Average time can be slightly longer but still quick.

Famous for its 10-minute promise and is very consistent in hitting this target in its service areas.

Product Range

Very wide range. Groceries, fresh produce, electronics, beauty products, and even stationery.

More focused on high demand daily essentials like groceries, snacks, and drinks. The range is growing but is more curated.

Delivery Charges

Has variable delivery fees, surge pricing during peak hours, and other handling charges.

Was the first to introduce a small platform fee. Also has delivery fees and late-night charges.

App Experience

Feature rich app with a powerful, AI-driven search.

Praised for its clean, simple, and very fast app. It’s built for one thing : ordering quickly.

Blinkit is currently the market leader in the country. It covers about 40-46% of the quick commerce market. Although Zepto is a strong competitor with about 21-29% market share.

Let’s dive into the strategies followed by both the giants as market share itself doesn’t tell us the whole story.

Blinkit’s Strategy : Backed by Zomato, Blinkit is focused on rapid expansion. It operates in over 30 cities, including many Tier-2 cities. It is also expanding its product range aggressively.

Zepto’s Strategy : Zepto is more focused on tier 1 cities. It operates mainly in the top 10 metro cities like Mumbai, Delhi, Bengaluru, and Chennai. Its goal is to dominate these high-demand, profitable areas by offering the best possible experience before expanding further to tier 2 cities.

They compete with each other through “dark stores,” the small warehouses that are the heart of this business. Blinkit is on a mission to expand its network to over 2,000 stores by 2026, while Zepto is strategically growing its 650+ stores in the cities it serves.

Blinkit: SWOT Analysis

Strengths

Fundamentals : Strong financial backing and access to a huge delivery network makes it a strong player.

Market Dominance : It has the largest market share and a huge customer base across the country.

Array of Products : Sells everything from groceries to electronics.

Weakness

Expenses : The 10-minute model is very expensive to run, making profitability a big challenge.

Quality issues : Some users report issues with service quality and longer delivery times.

Delivery Partner Issues : It has faced strikes and protests from its delivery partners, making the task of achieving profitability challenging.

Opportunities

New Offerings : It can add more high-margin items like fashion, home decor, and more.

Tier-2/3 Cities : Huge potential for growth in smaller Indian cities where competition is lower as compared to tier 1 cities.

Threats