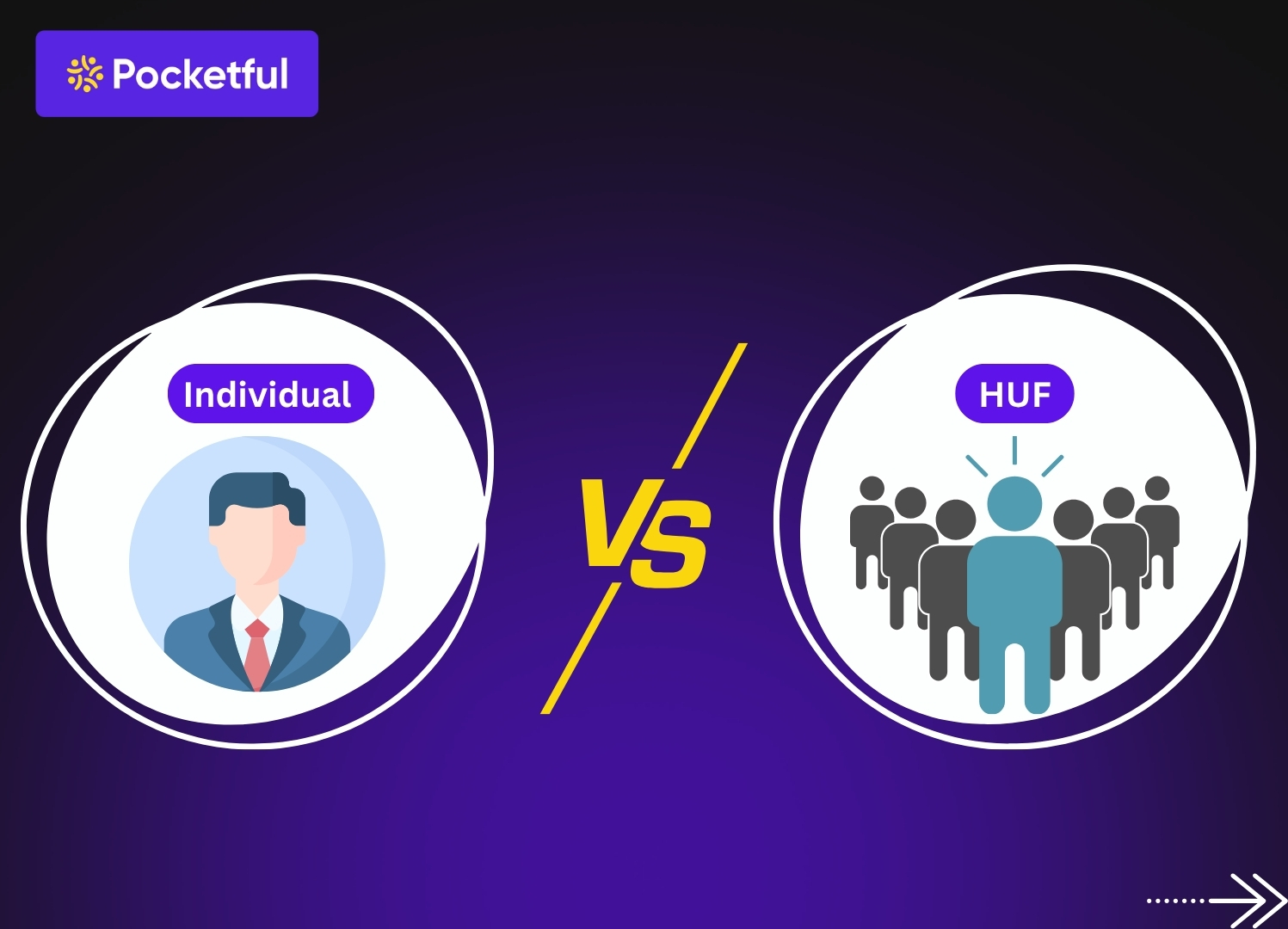

You must have an individual demat account in which you can hold securities to create long-term wealth. But most of you are not aware of the HUF demat account in which you can manage the investment as the head of your family, known as “Karta”. Using this account, you can create wealth for your family.

In today’s blog post, we will give you an overview of an individual and an HUF demat account, along with the differences.

What is an Individual Demat Account?

An individual demat account is a personal demat account opened by an individual to hold, buy and sell securities, including shares, bonds, etc., in electronic form. Only the account holder in whose name the demat account is opened can operate it. An individual bank account can be linked with this demat account.

Key Features of an Individual Demat Account

The key features of an individual demat account are as follows:

Nominee: The individual demat account holder can nominate various individuals in their demat account so that in case of the death of the account holder, the securities can be easily transferred to the near ones.

Multiple Accounts: One can open multiple demat accounts with different stock brokers, using the same PAN Card.

Taxation: All the gains earned from this demat account are taxed as per the norms of individual capital gain.

Unique ID: As an individual can open multiple demat accounts, all the demat accounts have a separate user ID and identification number.

When a Hindu Undivided Family is considered a legal entity registered under the Hindu Law, opening a demat account to invest in shares, mutual funds, bonds, etc, is known as an HUF Demat Account. However, the account is opened in the name of HUF, but the Karta of the family operates it. All gains earned from investments in the name of an HUF are taxed as a separate entity.

Key Features of HUF Demat Account

The key features of an HUF demat account are as follows:

HUF Name: The HUF account is opened only in the name of the HUF and PAN, and not opened in the name of an individual.

Separate Entity: An HUF is considered a separate legal entity, and all the income is taxable as an independent entity.

Eligible Investment: An HUF can invest in almost all kinds of investments, such as shares, mutual funds, bonds, etc.

One Demat Account: An HUF can open only one demat account against its PAN, but individual members can still have their own separate demat accounts using their personal PANs.

Difference Between an Individual and an HUF Demat Account

The key differences between an individual and an HUF demat account are as follows:

Particular

Individual Demat Account

HUF Demat Account

Owned By

An individual account can be owned by an individual.

This account can be owned by a Hindu Undivided Family.

PAN Card

An individual’s PAN Card is linked to it.

HUF Pan Card is used in it.

Operation By

This account is solely operated by an individual.

A HUF demat account can only be operated by the head of the family, known as “Karta”.

Taxation

All the incomes generated from this account are taxed in the hands of the individual.

All investment income is taxed separately in the hands of HUF.

Number of Demat Accounts

An individual can open multiple demat accounts using the same PAN Card with different brokers.

Only one demat account is allowed to be opened using an HUF Pan Card.

Transmission

In case of the death of the account holder, the securities are transferred to the nominee.

In case of Karta’s death, a new Karta is appointed instead of transferring units.

Objective

The objective of an individual demat account is to create an individual’s wealth.

A HUF demat account is generally used to create wealth for the family.

Document’s

Only the document of the individual is required.

Along with the document of the HUF Karta’s documents are also required.

If you are looking to create wealth for your family or create a legacy for them, then you can consider opening an HUF demat account and operate it as the Karta of the family. However, if you are looking to create wealth for yourself, then you can open an individual demat account and manage your investment accordingly.

Conclusion

In conclusion, both the individual and the HUF demat account facilitate the holding of securities, such as shares, bonds, and ETFs, in electronic form. However, both of these accounts differ in terms of ownership and operation. Having an individual demat account helps in creating wealth for an individual, whereas an HUF demat account builds wealth for a Hindu Undivided Family, and it is operated by the Karta, who will be the head of the family. Choosing among these demat accounts totally depends on the objective of creating wealth.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Is there any difference between an individual and an HUF demat account?

An individual demat account can be opened and operated by only an individual, whereas the HUF demat account can only be operated by the head of the Hindu Undivided Family, known as Karta.

Can a person who is a Karta open a separate individual account?

Have you ever heard of a stock market that does not have any screens, apps, or even a stock exchange? Dabba trading is exactly what it sounds like: a secret, off-the-record way for people to try to make money in the markets. No taxes, no fees, and no digital trail. But here is the problem: it is against the law and very risky. In this blog, we will talk about dabba trading, what it is, how it works, and why you should stay away from it.

What is Dabba Trading

Dabba trading is like an unregulated stock market that happens outside of official exchanges like the NSE or BSE. People do not use an authentic broker or the exchange’s system; instead, they write down trades in a “dabba,” which means “box” or “notebook” in English.

A dabba operator, who is not a registered broker, takes buy and sell orders from people. But the trades never make it to the stock market. Everything is paid in cash, which is why people who do this do not have to pay brokerage fees, GST, STT (securities transaction tax), SEBI fees, or stamp duty. It seems cheaper and easier on the surface.

But here is the catch: it is against the law and very dangerous. Also, if you get caught, you could face big fines and even imprisonment under Indian securities law.

In short, dabba trading is a way for some people to avoid paying fees, but it is stressful. It might look good, but it is not worth the risk.

Dabba trading is not a new thing; it has been in existence for several years. It took off in the 1980s and 1990s, when the stock market was not well-regulated as it is now. A lot of small traders and brokers did not have easy access to official exchanges back then, so they executed trade deals that were not recorded.

The word “dabba” comes from how trades were written. Instead of using the stock exchange, operators would write trades in notebooks or “boxes.” In fact, people were not buying shares; they were betting on share prices with the operator acting as a middleman.

Before the internet and discount brokers, dabba operators were very popular in small towns. It was fast, cheap, and easy compared to the official process, which was full of paperwork.

Tables turned in the 2000s when SEBI entered the picture and became a strict regulator, demat accounts became standard, and digital trading platforms evolved to make trading much easier and legal. That caused dabba trading to become extinct, but it never completely stopped.

Even though the government regularly cracks down and raids dabba traders, you can still find them in small groups all over India. The “no fees, no taxes” lures people in, but the risks have continued to grow worse over time.

How does Dabba Trading Work?

Here is how this trading works

There is usually an operator, which is someone who acts like a broker but does not hold a licence or registration.

Traders tell this operator what they want to “buy” or “sell.” But instead of going to the NSE or BSE, the order is just written down in a notebook, ledger, or even a computer file. The “dabba” is that record.

There are no digital trails here. Cash is used to settle everything. That is how they avoid paying broking fees, GST, STT, and all the other costs that come with real trading.

People figure out how much money they made and lost at the end of the day or week. The operator gives you cash if you “gain.” You have to pay if you lose.

There is no paper trail, no receipts, and no safety net for these trades because they never make it to the official stock exchanges. Your money is gone if the operator deceives you.

Why do People indulge in Dabba Trading?

To avoid fees – There are no brokerage, GST, STT, or other charges. It seems less expensive than normal trading.

Cash transactions – Everything is paid for in cash, so there is no paperwork or digital trail.

Looks simple and quick – traders think they can make money faster because there are no rules or regulations.

The thrilling factor – For some, it feels like gambling on the stock market, which makes it fun.

Legal Status of Dabba Trading in India

It is against the law, and SEBI and the stock exchanges do not recognise it. You are outside the system if you trade through a dabba operator.

The Securities Contracts (Regulation) Act, 1956, makes these off-the-record trades illegal in India. If you get caught, you could face big fines or even jail time.

There is no safety net. You cannot go to SEBI or the courts if something goes wrong with these trades because they are not on the official exchange. You are all alone.

Dabba trading can get you into legal issues for tax evasion.

At first, dabba trading might seem like a good idea because there are no taxes, no paperwork, and no middleman. But all you are getting is a lack of protection, an increased probability of losing money, and a risk of getting into legal trouble. We suggest you stay on the regulated track if you want to build sustainable, long-lasting wealth. It is the safest, smartest, and only way to make sure your money works for you.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

While investing in the stock market we might have often heard about ETFs or exchange traded funds. A standard ETF, like one that tracks the Nifty 50, which is like a basket of stocks where the biggest companies get the biggest share. This is simple, but it means you end up putting more money into stocks that are already large and popular.

But what if you can invest in more smarter ways and build a smarter basket. This is where the smart beta ETF is for, instead of just focusing on a company’s size, a smart beta ETF picks and weighs stocks based on other specific traits or “factors”, like whether a stock is undervalued, has stable earnings, or pays good dividends. It’s a strategic approach that blends the low-cost, rule-based nature of a passive ETF with the intelligent stock-picking ideas of active investing.

What is an ETFs?

Exchange Traded Funds, or ETFs are a basket of stocks where instead of buying one share of one company, you buy one unit of an ETF that has small pieces of many companies at once, making your investments diversified and not concentrated in just one or two stocks. It’s a simple way to get diversification and usually comes with lower fees.

Generally, ETFs that track the Nifty 50 choose companies based on their size, or market capitalization. Market cap is calculated by multiplying a company’s share price by the total number of shares it has. This method is called “market-cap weighting.” In such ETFs, bigger companies get a larger share of the basket. That’s why a large company like Reliance Industries affects the Nifty 50’s performance much more than smaller companies in the index.

What are Smart Beta ETFs?

Smart ETFs are an investment product that fall in between purely investing in Nifty 50 ETF and fully active investing in selected stocks. Index is used for benchmarking in Smart Beta ETF. A smart beta fund tracks an index, just like a regular ETF, but the main focus is not only on the market cap, it is built using a transparent, rules-based system that focuses on specific characteristics or factors, which is the main idea behind Smart Beta ETFs.

The rules used for these Smart Beta are pre-defined that are followed automatically. For example, a rule might be, “From the Nifty 100 stocks, only select companies that have low debt and stable earnings.” This makes the process transparent and removes emotional decision-making.

Smart Beta ETF is now becoming popular amongst the investors and the options for these alternatives in India are growing as smart beta takes the proven ideas that expensive active fund managers have used for years and puts them into an automated, low-cost, and transparent ETF format.

Value: The goal here is to find out a high-quality brand that is at a low P/E ratio as in this strategy the focus of buying the stocks is to get stocks that seem cheap compared to their actual business worth.

Quality: Here the strategy for an investor is to opt for the stock of companies that have strong management, well managed working with stable earnings, low debts, and strong financials.

Low Volatility: This strategy focuses on stocks with smoother price moves as this helps in reducing overall portfolio risk and standard deviation.

Momentum: This strategy helps in investing in such stocks that have a positive upward trend with a hope that the trend will continue to move upwards.

Dividend Yield: The strategy focuses on regular dividend yielding, which becomes a popular choice for investors looking to earn a regular income from their investments.

Equal Weight: In this strategy every stock gets the equal share rather than giving preference to the bigger companies only, equal-weight share improves diversification and reduces the risk of dependence only on big companies and their performance.

Risk-Adjusted Returns: With smart beta, it is not just about higher returns, but fulfilling better returns for the risk taken. These ETFs focus on factors that have performed well historically in an attempt to outperform traditional market cap funds over a long time.

Enhanced Diversification: As we explained, a Nifty 50 ETF is often overweighted to the top 5 or 10 stocks. Smart beta strategies that focus on equal weighting invest more evenly across a greater number of stocks. This diversification helps to mitigate the risk of one or two large stocks underperforming and the impact of those stocks dragging down the whole portfolio.

Rule-Based Approach: These rules, or rather strategies, have distinct advantages which are often overlooked. Pre-defined rules help to overcome emotional biases and behavioral mistakes which can negatively impact the portfolio. Smart beta ETFs have rules which are set so that there is no room for emotional decision making. For instance, a value ETF is programmed to sell stocks which are deemed expensive and purchase stocks which it considers to be cheap, is an example of forcing you to operate in a buy low, sell high mentality.

Cost-Effectiveness: Though Smart Beta ETFs can be a little expensive than most of the passive ETFs, they are generally much cheaper than actively managed mutual funds pursuing similar factor strategies.

Of course, no investment is without risk. It’s important to have a balanced view and understand the potential downsides.

Factors Can Underperform: Out of all the risks, this is the most important to understand. Every factor has losing streaks. There can also be long periods of years when a value strategy lags behind the market, whereas a momentum strategy fails during a sudden market crash.

Limitation of Backtesting: A lot of smart beta strategies “work” in “back-tests” or simulation-based on past data strategy. But as every investor knows, past performance is no guarantee of future results. A strategy that worked every decade doesn’t seem plausible to work for the next decade.

Higher Costs and Complexity: Smart Beta ETFs, owing to their complex nature in both design and management, charge a conditionally higher expense ratio as compared to the plain and simple INDEX ETFs. Although the difference may be small, it is still evident.

Lower Liquidity: Out of the newer or more niche smart beta ETFs in India, some might have comparatively lower liquidity, or volume of participants to buy and sell parts of the ETF on a daily basis. It may not be a major concern for most small investors, but it may pose a challenge for those looking to trade a considerably large volume of the ETF in a short time.

The Psychological Challenge: Smart beta ETFs are designed to perform differently from the main market. This difference is called “tracking error.” While this is intentional, it can be mentally tough. Imagine the Nifty 50 is up 20% in a year, but your low volatility ETF is up only 8%. It’s easy to feel like you’re missing out and be tempted to sell at the wrong time. Sticking with the strategy requires conviction.

Why Do Investors Choose Smart Beta ETFs?

Smart beta ETFs are selected by the investors because they look for more strategic investments rather than just buying randomly from the market and also investors don’t want to pay the high fees or rely on the judgment of an active fund manager. They offer a middle ground that is rules-based, transparent, and cost-effective.

It is for investors who want to buy quality companies stock or undervalued stocks for the long-term as Smart Beta ETF allows the investors to make the investments simpler and in a disciplined way.

Smart beta ETFs are not just simple ETFs but they are new powerful and innovative tools that are designed for modern investors like you. Though you need to keep in mind that they do not provide guaranteed high returns but they provide a strategic investment plan to build your portfolio.

The strategy to invest in Smart beta ETFs depends upon your investment goals, as understanding the right strategy with patience can help you excel your financial goal.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

No, the returns in smart beta ETFs are not guaranteed but they are designed with a potential to give better risk-adjusted returns in the long run, but the chances of their performance is greater than Nifty 50 ETFs in the long term.

Are smart beta ETFs actively managed?

No, smart beta ETFs are not actively managed. They are best described as a hybrid. The strategy behind Smart Beta Indices is active (e.g., choosing focus, value, etc.), but the fund itself is managed passively. A human fund manager is not making daily buy or sell decisions.

Difference between a smart beta ETF and a normal Nifty 50 ETF?

In a Nifty 50 ETF the focus is more on the bigger companies based on the market capitalization. On the other hand, smart beta ETF deals differently by giving weightage to companies based on factors like low price, financial health or low volatile company.

Are smart beta ETFs expensive?

Smart beta EFTs are expensive compared to the traditional index ETFs, but they are less expensive than actively managed mutual funds.

Are smart beta funds suitable for beginners?

They can be, but it’s important for a beginner to first understand the basic concept of an index ETF. If you are willing to learn about the specific factor (like value or quality) and understand that the fund will behave differently from the main market, it can be a good addition to your portfolio.

Have you ever thought of making money in a single day by trading? This is what you can do in Intraday Trading, by investing your money in the stock market and you buy stocks and sell them on the same day, hoping to profit from the small price changes that happen throughout the day.

Let’s say you see a stock at Rs.100, you believe it will go up to Rs.103, on that day and you buy it, and if it moves to a desired price, you sell it and earn Rs.3 profit per share giving you the profits before the market closes.

But for quick decision making you need to have an Intraday trading app, a good app needs to be fast, easy to use, and reliable. But the market has so many intraday trading apps and finding the best app for intraday trading in India can feel overwhelming.

In this blog we will get to know the top intraday trading apps in India and learn their features and uses.

Top 10 Intraday Trading Apps in India

1. Upstox

It is a financial stock broking app that is backed by people like Ratan Tata, Upstox is a powerhouse app built for speedy stock services. It is best suitable for people who frequently trade during the day.

It offers charting tools from both TradingView and ChartIQ. You can also place ‘basket orders’ to buy or sell up to 20 different stocks at once with a single click.

With so many features, it can feel a little complicated for a total newbie. Active traders who need a fast and powerful platform.

2. Groww

Groww is incredibly popular with beginners because it is very easy to use. If you’re new to the market, this is a great place to start, learn and invest.

The app’s design is clean and easy to understand. It also offers ‘OCO’ orders, where you can set your target price and your safety-net stop-loss at the same time.

It is made for all the young population that can do hassle free trading without studying and investing too much time on learning but the advanced traders might miss some of the deeper analytical tools found on other platforms.

3. Pocketful

Pocketful is a new-age platform built for traders who like technology and information at one place. Pocketful provides powerful tools like algo-trading and options strategy making trading simpler for everyone. It offers a complete trading platform paired with easy-to-understand educational content, helping users learn and invest in one place without feeling overloaded.

It makes powerful tools like algo-trading and options strategy simple for everyone.Pocketful GPT helps you achieve Smart AI that analyzes portfolios, researches markets, and designs strategies.

Angel One is one of the pioneers in the stock broking field, and it is a mix of long legacy and modern tech.

The app also offers ‘Smart Orders’ to help you trade automatically and an AI engine called ARQ Prime that gives you stock market ideas. They also provide a good margin facility if you want to trade with more capital than you want to invest.

The app is packed with features and is best suited for anyone who wants a good mix of modern tools and expert research.

5. Zerodha Kite

Zerodha is one of the leading stockbrokers of India, and their app, Kite, is famous for super fast user experience and clean user interface. It is one of the most relied on apps among the experienced traders for Intraday trading and much more.

Kite has detailed stock charts and financial information with over 100 tools to help you analyze your preferred stocks. You can also set ‘Alert Triggers Orders (ATO)’ which automatically places a linked basket of orders on the exchange when a Kite alert is triggered. In ATO, market orders are placed with market price protection.Alert Triggers Orders (ATO) is a feature that automatically places a linked basket of orders on the exchange when a Kite alert is triggered. In ATO, market orders are placed with market price protection.

Zerodha gives you the stock analysis and the holistic company information, but it does not give you stock investment tips. Traders who are comfortable with charts and numbers can use the information, making their own decisions.

6. ICICI Direct

ICICI is one of India’s biggest banks, ICICI Direct is one of its segments for trading in the financial market which comes with a super convenient 3-in-1 account that links your bank, trading, and demat accounts together.

Moving money in and out is instant and seamless because your bank account is already linked to your trading account. The app also has great charts and special tools for scalping, which helps them in instant decision making.

The cost for trading was more expensive, but with new players in the market the price has also become competitive. It is best suited for ICICI Bank customers who need everything at one place.

7. Fyers

Fyers is a platform built by traders, for traders which has become a huge hit among people who like charts and numbers. It offers one of the best TradingView experiences, letting you trade directly from the charts, which is a huge time-saver. It also has a special ‘Options Scalper’ tool for quick options trades.

Fyers is designed for technical traders, so it might be a little complicated for the beginners who need guidance throughout. It is best suited for traders who can understand and use technical data and available tools.

8. 5paisa

5paisa is a great choice if you’re looking for a low-cost app that is packed with advanced features. It’s perfect for budget-conscious traders as you can subscribe to different plans that lowers your brokerage fees and even more.

5paisa has powerful TradingView charts and a stock screener to help you find good trading opportunities during your intraday trades. Although the best research features are locked behind their paid plans.

9. IIFL Markets

IIFL is another experienced broker which provides a solid trading app. Their biggest strength is the high-quality research and stock tips they provide to their clients. Traders get access to expert research reports, which is great if you need ideas on what to trade.

The app also has a ‘Buzz’ feature that keeps you updated with the latest market news so that you can make the right move during your Intraday trade.

It’s a full-service broker, and so it’s a little costlier and does not have a flat-fee as other discount brokers. Traders who like to have expert opinions to back up their intraday decisions can rely on IIFL Markets.

10. Paytm Money

Paytm money is the trading segment from the makers of Paytm, the app is all about making trading simple and accessible for the mass audience. The platform has user friendly tools making it easier to start trading.

The app’s clean and quick design helps in making the intraday trades smooth and quick. It also supports important tools like GTT orders and Bracket orders to help you manage your risk.

It currently focuses on stocks and F&O only, commodities so you can’t trade commodities or currencies on it. It is best suitable for Beginners and Paytm users who want a simple, no-fuss trading app.

3-in-1 account (bank + trading), advanced charts, special order types

Fyers

Charting experts & technical traders

Flat ₹20 or 0.03% (whichever is lower)

Top-tier TradingView experience, special tool for options scalping

5paisa

Budget-friendly trading

Flat ₹20 per executed order

Good charts, stock finding tools, low-cost subscription plans

IIFL Markets

People who like expert advice

Flat ₹20 per executed orde

In-depth research reports, stock tips, market news feed

Paytm Money

Simplicity and ease of use

Flat ₹20 or 0.05% (whichever is lower)

Very clean design, GTT orders, essential risk management tools

Intraday Trading Basics

Let’s have a look at the simple rules of intraday trading you should know.

Fixed Time: Traders need to make sure that they close all their positions before the market closure or before 3:30 PM in intraday trading to avoid fees or losses.

No Ownership: Since you buy and sell the stocks on the same day, they never actually enter your demat account, providing no ownership. In intraday you just trade on the price movement.

Leverage/Margin: This is like a small loan from your broker for the day to buy more shares than you can with your own capital, resulting in more profits, but it can also magnify your losses as well.

Short Selling: You can sell a stock first at a high price (even if you don’t own it) and buy it back later when the price drops and the difference you get is the profit.

Advantages and Disadvantages of Intraday Trading

Advantages

Daily Gains: You can make money fast and skip the weeks or months of money invested as in intraday trading you can make profits (or losses), same day.

No overnight stress: As the stock is traded on the same day so you know your net loss and profit giving you a clear picture without the risk of market fluctuations due to overnight news.

Power of Leverage: Leverage allows you to take bigger positions than your capital would normally allow.

Profiting from short selling: You can make profits even when the market is down, a falling market can become an opportunity.

Disadvantages

High Risks: Most people who try intraday trading lose money so it is not easy, as there is constant market fluctuations.

Stressful: Watching the market go up and down can lead to an emotional decision, leading to bad decisions.

Full-time job: You can’t just check in once or twice during the day as successful day trading requires you to watch the market constantly.

Added costs: You pay small fees on every trade you make on that day and if you trade a lot, fees can eat your profits.

There is no single best intraday trading app that fits everyone. The right choice is personal. If you love charts, Zerodha or Fyers can be opted. If you’re a beginner, start with something simple like Pocketful as you can also experiment with automated trading. Pocketful has some really advanced, user-friendly tools. And if you prefer getting expert advice, Angel One or IIFL Markets are great options. And remember the best advice is to start small, learn every day, and always trade responsibly.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What if I forget to sell my stocks before market closure?

The broker automatically sells it known as “auto square-off”, usually this is chargeable and a penalty is levied typically around Rs.50 + gst per trade.

Can day trading be started from Rs.1000?

Technically, yes but it’s very hard to get profit out of it and if there is some small profit then the fees can evade your gains. You can learn using such a small amount and know how the market works.

When is the best time of day to trade?

Many traders find the most action happens in the first hour (9:15 AM – 10:15 AM) when the market opens, and the last hour (2:30 PM – 3:30 PM) before it closes. The market tends to move the most during these times.

How are intraday trading profits taxed?

They are treated as ‘speculative business income’, which means the profit is added to your total income and taxed based on your income tax slab.

What is a ‘stop-loss’ in simple terms?

A stop-loss is your safety net where you can sell the stock at the desired price automatically if it starts to fall, as a falling stock can erode your initial investments.

Imagine you are now a settled individual and thinking about the next big goal of your life like buying a house, funding your child’s education or maybe starting a new venture. To make this happen you might need a financial partner to meet your goals, today we are going to know about a company that is built on this very idea.

Overview of Tata Capital

Tata Capital’s journey from a new player in 2007 to a financial leader is a tale of steady and smart growth.

The company set up its main businesses by launching a special division for home loans, Tata Capital Housing Finance, in 2008 and Tata Capital expanded quickly, offering all kinds of loans for homes, cars, businesses, and personal needs. Seeing that the future was online, the company focused on its website and apps. This made getting a loan faster and easier for everyone, even in smaller towns.

The company’s total lending crossed Rs.1 lakh crore and then doubled to over Rs.2 lakh crore in just a few years. In 2025, it took the big step of launching its IPO to be listed on the stock market. Led by CEO & MD Rajiv Sabharwal, the company is guided by the strong ethical principles of the Tata Group. This means it is run with honesty and transparency, which is a big reason why people trust it. The company has a simple promise ‘We only do what’s right for you’ (‘Karein wahi jo aapke liye sahi’), this isn’t just a slogan; it shows their vision to be a “Responsible Financial Partner fulfilling India’s Aspirations”. The company has five core values: Integrity, Responsibility, Excellence, Pioneering, and Unity.

Products and Services of TATA Capital

For Individual or Families:

Personal Loans: This is for personal use like weddings, a holiday, or a medical emergency.

Home Loans: For customers that want to buy, build, or even fix up your dream home.

Vehicle Loans: For customers who are looking for new and used cars, and also for bikes and scooters.

Other Loans: Here you can also get loans by using your property or investments (like shares) as security.

Credit Cards & Insurance: These products are also available for its users.

For Businesses:

Business Loans: Here small and medium businesses can get loans to grow, buy new machines, or manage their daily costs.

Commercial Finance: High capital loans for large companies and big projects like roads and bridges.

Cleantech Finance: TATA Cleantech Capital is a company that provides loans for green projects like solar and wind projects.

Wealth Management and Digital Tools:

Wealth Services: If you are looking for expert advice for your financial future and want to manage your investments, TATA group will also help with this.

Moneyfy App: This is the mobile app used for investing, in this you can start investing in mutual funds with just Rs.500, which helps more people join the financial system.

Market Presence and Reach

Geographic Coverage: TATA capital has over 1,500 branches in more than 1,100 towns and cities, giving customers easy access.

Customer Segments: They help a wide variety of people and businesses from retail everyday people like you and me, small and medium-sized businesses, which are the engine of our economy and Corporate like big, well-known companies.

Digital Footprint: TATA capital has advanced websites and financial apps like TATA capital and Moneyfy. Users can easily apply for loans, invest and even keep an eye on their account. With its strong physical and online presence it caters to both tech savvy and technologically obsolete people.

There are two main streams of income of TATA Capital. First is the Interest on Loans which is their biggest earner and second is the fees for services like the processing fees for loans or loans or commissions for selling insurance and mutual funds.

Value Proposition

Reliable Brand: The “Tata” name means safety, honesty, and good service.

All in One: You can get all your financial needs met here, from loans to investments. It’s convenient.

Easy Availability: With branches and apps, they are easy to reach, no matter where you live in India.

Diversified product and services: They have a solution for almost every financial goal, which means they can help a lot of different people.

Key Partnerships and Channels

TATA capital has aligned with other TATA group companies, for example they partner with TATA Motors to offer affordable car loans directly from the outlets and it has also collaborated with TATA Housing from home loans. This helps in getting customers from multiple sources which is a major problem for other companies.

Marketing Strategy of Tata Capital

Brand Positioning

The brand is portrayed like a partner who helps in achieving your dreams, their ads give you the opportunities that you are looking for like buying a car or buying a new house or even if you require funds for your next business project, the brand has a tagline “Count on us” ensuring trust and reliability for customers.

Target Audience

They look for people that are looking to make change for themselves or their families like a young person who wants to have a new house for his family and a car for their use or someone who is looking to start a new venture. Also to amplify their brand they have chosen Shubman Gill as their brand ambassador to connect with a younger, ambitious audience that values trust.

Advertising Campaigns

‘Mitaye Faasle’ (Bridge the Distances): In this campaign the users are shown how problems related to money can create emotional distancing among the families and how TATA capital can solve all these problems.

‘Apne Mann ki Karo’: This campaign used humour to talk about their flexible loans, connecting with people in a fun, light-hearted way.

Digital Presence: They are very active on social media like Facebook and Instagram, sharing useful tips and information for their followers.

Customer Engagement & CSR

The company is connecting with the mass audience by sponsoring big events like IPL (Indian Premier League), making the brand very prominent and visible to the audience. The company also does social work (CSR) in various sectors like health, education and the environment, which helps companies to strengthen their image which shows that the company cares about their targeted audience.

Total Income: Tata Capital profit had a 56% jump from the previous year as the company earned about Rs. 28,370 crore.

Profit: The profit earned was Rs. 3,655 crore after all the taxes and expenses.

Total Loans (AUM): Tata Capital lent out the massive amount of Rs.2.33 lakh crore by June 2025.

The company is growing but the most important thing for a company is to get back the loans issued to the customers so one should keep an eye on the Non-Performing Assets because this is the loan percentage that is under risk. As of June 2025, Tata Capital’s Gross NPA was 2.1% and its Net NPA was 1%, which is considered healthy.

The company even launched its IPO in October 2025 which showed a steady response. The company has a focused and a stable approach which was also seen in its IPO where the IPO was priced fairly to attract people that are looking for long term growth rather than making quick profits.

SWOT Analysis of Tata Capital

A SWOT analysis is a simple way to see a company’s Strengths, Weaknesses, Opportunities, and Threats.

STRENGTHS

WEAKNESSES

The Trusted Tata Brand: Their biggest advantage. People trust the name.

Lower Profit Margins: They earn a bit less profit on each loan compared to some top competitors like Bajaj Finance.

Many Different Products: This reduces risk. If one area is slow, others can do well.

Complex to Manage: Running such a large and diverse business can be difficult and costly.

Strong ‘Phygital’ Network: They are present everywhere, both with branches and online.

Depends on Parent Group: While a strength, any trouble for the main Tata Group could affect them.

Good at Managing Risk: They have a good record of keeping bad loans (NPAs) low.

OPPORTUNITIES

THREATS

Lending to Small Businesses & in Villages: There’s a huge opportunity to provide loans to small businesses and people in rural India.

Tough Competition: They face strong competition from big banks, other NBFCs, and new fintech startups.

Growth of Digital Services: More people are using smartphones, creating a chance to offer more digital-only products.

Stricter Rules: The RBI is making rules for big NBFCs stricter, which could affect their business.

Boom in Green Energy: India’s focus on clean energy is a big opportunity for their special green finance division.

Economic Slowdowns: If the economy slows down, more people might struggle to repay loans.

Helping More People Get Loans: A chance to give financial services to millions of Indians for the first time.

Issues at the Top: Any problem at the very top of the Tata Group could harm the brand’s reputation.

The story of Tata Capital shows how to build a financial powerhouse on a foundation of trust. The success of the company was dependent on their use of both the branches and technology which can serve everyone. The success totally depends on their wide range of products and by smartly using their network in a balanced way.

Tata Capital’s future looks bright as they have big opportunities like lending money to small businesses as they grow their digital offerings.The company also faces many challenges through new rules and regulations and their arch rivals. Tata Capital’s had grown themselves through a steady and responsible way. It’s not about quick growth and risky bets. The company has stuck to their core values, and set themselves to remain as a trusted financial partner for their mass audience and years to come.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Tata Capital is a large financial services company that majorly provides loans like home loans, car loans, and business loans to people and companies. It also helps people invest their money and offers insurance.

Why is the Tata brand so important for Tata Capital?

In the world of money, trust is everything. The “Tata” name immediately makes people feel that their money is safe and the company is honest. This is a huge advantage over its competitors.

What is the ‘Tata Capital Business Model’ in simple terms?

Their business model is “diversified.” Think of it as not putting all your eggs in one basket. They offer many different types of loans and services, so if one area isn’t doing well, the others can support the business. This makes them very stable.

Why wasn’t the Tata Capital IPO a blockbuster hit on day one?

The IPO was priced for long-term investors who believe in the company’s steady growth, not for traders looking to make a quick profit. Analysts believe it’s a good investment for the long run.

What is a simple SWOT analysis of Tata Capital?

Its biggest strength is the trusted Tata brand. Its main weakness is that it makes a little less profit on its loans compared to some rivals. A big opportunity is to give more loans to small businesses in India. The biggest threat is the tough competition from banks and new online finance companies.

Pharma mutual funds and healthcare mutual funds are emerging as a great option for investors in 2025. Increasing healthcare needs, government schemes and increasing expenditure on research are strengthening this sector. In such a situation, the pharma sector mutual fund is useful for those who want stable and safe returns over a long period of time. In this blog, we will know which are the best pharma mutual funds India 2025, and how they can make your portfolio balanced and profitable.

What Are Pharma Sector Mutual Funds?

Pharma sector mutual funds are mutual funds that invest primarily in companies in the pharmaceutical, healthcare services, diagnostics, medical devices and biotechnology sectors. As per SEBI regulations, any sector fund is required to invest at least 80% in the same sector.

Investment focus : Pharma mutual funds in India focus specifically on healthcare innovation, diagnostics, medical equipment and drug manufacturing. This way, investors can directly connect to the growth story of that sector.

Difference from diversified funds : While diversified mutual funds spread investments across many different sectors (such as IT, banking, consumer goods), pharma sector mutual funds focus only on the healthcare and pharma industry. This is why the potential returns may be higher, but the risk is also higher.

Best Pharma Sector Mutual Funds 2026

Fund Name

Current Nav

AUM

3 years return

5 year Return

Nippon India Pharma Fund

₹512.99

₹8113.59Cr

22.21%

16.99%

SBI Healthcare Opportunities Fund

₹433.98

₹3933.26Cr

25.77%

18.86%

Tata India Pharma & Healthcare Fund

₹30.75

₹1295.83Cr

22.87%

17.27%

UTI Healthcare Fund

₹292.65

₹1096.95Cr

25.10%

17.28%

ICICI Prudential Pharma Healthcare & Diagnostics Fund

₹40.42

₹6226.82Cr

28.40%

20.07%

DSP Healthcare Fund

₹39.12

₹3106.92Cr

23.00%

16.96%

LIC MF Healthcare Fund

₹29.88

₹85.19Cr

20.52%

13.77%

Mirae Asset Healthcare Fund

₹39.02

₹2761.64Cr

21.63%

17.17%

Aditya Birla Sun Life Pharma & Healthcare

₹31.21

₹829.63Cr

22.14%

15.27%

ITI Pharma and Healthcare Fund

₹16.40

₹226.5Cr

20.47%

–

(Data as on 14-10-2025)

1. Nippon India Pharma Fund

Nippon India Pharma Fund has a minimum SIP of ₹100 and is managed by Sailesh Raj Bhan. The fund invests in leading companies like Sun Pharma, Divi’s Labs, Lupin, Cipla, Dr. Reddy’s and Apollo Hospitals. The portfolio also includes companies like Medplus, Vijaya Diagnostic, GSK Pharma and Gland Pharma.

2. SBI Healthcare Opportunities Fund

SBI Healthcare Opportunities Fund has a minimum SIP of ₹500 and is managed by fund manager Tanmaya Desai. It invests in Sun Pharma, Divi’s Labs, Max Healthcare, Cipla, Lonza Group and Lupin and is suitable for long-term investors in the healthcare sector.

3. Tata India Pharma & Healthcare Fund

The minimum SIP of Tata India Pharma Fund is ₹100 and it is managed by Rajat Srivastava. The portfolio includes Sun Pharma, Cipla, Apollo Hospitals, Lupin, Repo Instruments, Healthcare Global, Torrent Pharma, Aster DM, Fortis and Alkem Laboratories.

4. UTI Healthcare Fund

The minimum investment in UTI Healthcare Fund is ₹500. Led by Fund Manager Kamal Gada, it invests in companies like Sun Pharma, Cipla, Ajanta Pharma, Lupin, Procter & Gamble Health and Dr. Reddy’s.

5. ICICI Prudential Pharma Healthcare & Diagnostics Fund

The minimum investment of ICICI Prudential Pharma Fund is ₹100. It is managed by Fund Manager Dharmesh Kakkad and the portfolio includes Sun Pharma, Dr. Reddy’s, Divi’s Labs, Cipla, Aurobindo Pharma, Lupin, Mankind Pharma, Alkem, Biocon and Tri-Party Repo.

6. DSP Healthcare Fund

DSP Healthcare Fund has a minimum investment of ₹100 and is managed by Chirag Dagli. The portfolio includes Cipla, Sun Pharma, Ipca Labs, Cohance Lifesciences, Laurus Labs and Gland Pharma.

7. LIC MF Healthcare Fund

LIC MF Healthcare Fund has a minimum SIP of ₹200. Led by Fund Manager Karan Doshi, it invests in Sun Pharma, Apollo Hospitals, Torrent Pharma, Cipla, Tri-Party Repo and Divi’s Labs.

8. Aditya Birla Sun Life Pharma & Healthcare Fund

Aditya Birla Sun Life Fund has a minimum SIP of ₹100. Fund Manager Dhaval Shah manages it and the portfolio includes Sun Pharma, Apollo Hospitals, Cipla, Fortis Healthcare, Abbott India and Torrent Pharma.

9. Mirae Asset Healthcare Fund

Mirae Asset Healthcare Fund has a minimum SIP of ₹99. Fund Manager Vrijesh Kasera manages it and the portfolio includes Sun Pharma, Divi’s Labs, Glenmark Pharma, Aurobindo Pharma, Cipla, Apollo Hospitals, Lupin, Dr. Reddy’s, Krishna Institute and Cohance Lifesciences.

10. ITI Pharma and Healthcare Fund

ITI Pharma Fund has a minimum SIP of ₹500 and is managed by Rohan Korde. The portfolio includes Sun Pharma, Divi’s Labs, Max Healthcare, Apollo Hospitals, Cohance Lifesciences and Torrent Pharma.

The demand for healthcare and medicines has increased rapidly after the COVID-19 pandemic. This has made “Pharma Mutual Funds” an attractive option for investors as they offer stability along with good returns.

2. Export boom and India’s global role

India’s pharma exports reached $27.9 billion in FY 2023-24, which is about 9.3% higher than the previous year. This growth was almost double the global average.

India is now called the “Pharmacy of the World” as it supplies more than half of the world’s generic medicines. India alone meets 40% of the US and 25% of the UK’s generic drug needs.

3. Government initiatives

The PLI (Production-Linked Incentive) scheme of the Government of India has given new impetus to the pharma sector. Investment and production capacity in projects related to drugs and medical devices have increased rapidly. These initiatives have made pharma mutual funds even more attractive for investors.

4.Strong domestic demand base

Increasing diseases, lifestyle challenges and ageing population in India are continuously increasing the demand for healthcare services. Also, the coverage of health insurance is also expanding rapidly, giving an additional boost to the pharma sector.

5. India on the global supply chain

India’s drug manufacturing capacity and quality standards (such as US-FDA and WHO-GMP) have continuously improved. Due to this, it has become a reliable part of the global supply chain and India’s role in the pharma industry has become stronger.

Key Things to Check Before Investing in Pharma Sector Mutual Funds

Performance record of the fund : Before investing in a pharma sector mutual fund, make sure to look at the CAGR (Compound Annual Growth Rate) of the last 3 years and 5 years. Funds that consistently perform well are considered reliable.

Expense ratio : Sector funds often have a slightly higher expense ratio. Funds with a lower expense ratio can give better returns for investors in the long run.

Expertise of the fund manager : Since pharma is a niche sector, it is very important to have an experienced fund manager. Their research and selection capabilities directly impact the returns.

Volatility : Pharma funds are defensive in nature but during a bull run, they can give lower returns than sectors like IT or banking. Investors should be prepared for this volatility.

Investment period : These funds are better suited for those with an investment horizon of 5 years or more. It is not right to expect them to last for a short period of time.

Who should avoid : Pharma funds are not suitable for investors who are looking for short-term gains or have very low risk.

Sector Dependency : Pharma mutual funds invest primarily in pharma and healthcare companies. This means that if there is a downturn in the sector, the fund’s performance can be directly affected. For example, the success or failure of a new drug, competition and changes in demand in the market can directly impact the NAV.

Regulatory Risk : The healthcare sector is heavily regulated. FDA approvals, new drug policies, changes in drug prices or new government regulations can impact the fund’s performance. Sudden changes in regulations can lead to fluctuations in the fund’s returns.

Volatility : The pharma sector is sometimes very volatile. Events such as the success of new drugs, expiry of patents, mergers or global health crises such as COVID-19 can impact the sector, leading to rapid changes in the fund’s NAV.

Liquidity Risk : Some healthcare funds may have low liquidity. This means that if the investor wants to withdraw money immediately, it may take time. So invest only the amount that you can keep for a long period.

Portfolio Diversification : Investment in these funds is limited to only one sector, so the risk can be high. Therefore, experts recommend that the portfolio should also be invested in other sectors and asset classes so that the overall risk is reduced and the investment remains safe.

If you want to invest in the health sector, Pharma mutual funds are a practical option. These funds can give good returns in the long term and also provide an opportunity to be a part of the growing demand of the health sector. Yes, sometimes returns can be affected due to fluctuations in the sector or new regulations. So do not rush, do some research and invest only after balancing your money. If you invest money wisely, these funds can become a safe and profitable source for you.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Canara HSBC Life Insurance Company Limited, a leading private life insurer jointly promoted by Canara Bank and HSBC Insurance (Asia-Pacific) Holdings Limited, has launched its ₹2,517.50 crore Initial Public Offering (IPO), entirely as an Offer for Sale (OFS) (i.e., no fresh capital is being raised). The IPO opened for subscription on October 10, 2025, with a price band set between ₹100 and ₹106 per share. The subscription window will close on October 14, 2025, and the shares are scheduled to be listed on both the BSE and NSE on October 17, 2025.

Canara HSBC Life Insurance IPO Day 3 Subscription Status

On Day 3, the Canara HSBC Life Insurance Company IPO received a moderate response from investors, closing with an overall subscription of 2.05 times. The Qualified Institutional Buyers (QIB) category led the demand with a subscription of 7.05 times, indicating strong interest from institutional investors. The Non-Institutional Investors (NII) segment recorded a subscription of 0.33 times, showing limited participation from high-net-worth investors. Within this segment, the bNII (above ₹10 lakh) portion was subscribed 0.28 times, while the sNII (less than ₹10 lakh) portion saw a subscription of 0.44 times. The Retail Individual Investors (RII) category recorded a subscription of 0.42 times, reflecting a modest response from retail participants.

Investor Category

Subscription (x)

Qualified Institutional Buyers (QIB)

7.05

Non-Institutional Investors (NII)

0.33

bNII (above ₹10 lakh)

0.28

sNII (less than ₹10 lakh)

0.44

Retail Individual Investors (RII)

0.42

Total Subscriptions

2.05

Total Applications: 1,74,847

Total Bid Amount (₹ Crores): 4,055

How to Check Canara HSBC Life Insurance Co.Ltd IPO Allotment Status

Canara HSBC Life Insurance allotment can be easily checked online in two ways: from the Registrar’s website and from the BSE or NSE website. This IPO will be listed on both the exchanges – BSE and NSE, so the allotment status will be available to all investors on both platforms.

Select “Canara HSBC Life Insurance ” from the IPO list

Enter PAN number and Application number

Click on Search

Objective of the Canara HSBC Life Insurance

Canara HSBC Life Insurance will not receive any proceeds from the Offer. All funds raised through the Offer will go entirely to the Selling Shareholder, after deduction of Offer-related expenses and applicable taxes, which will be borne solely by the Selling Shareholder.

Canara HSBC Life Insurance GMP – Day 3 Update

The grey market premium (GMP) of Canara HSBC Life Insurance Company Limited IPO stood at ₹0 as of 5:00 PM on October 14, 2025 (Day 3). Considering the upper end of the price band at ₹106, the estimated listing price is around ₹106, indicating no gain (0%) per share.

Date

GMP

Est. Listing Price

Gain

14-10-2025 (Day 3)

₹

₹106

0%

Disclaimer: The above GMP (Grey Market Premium) is just unofficial market information, which is not officially confirmed. These figures are shared for informational purposes only and investment decisions based on these should be based on the investor’s own research and discretion. We do not conduct, recommend or support any kind of transaction in the grey market.

Canara HSBC Life Insurance – Key Details

Particulars

Details

IPO Opening Date

October 10, 2025

IPO Closing Date

October 14, 2025

Issue Price Band

₹100 to ₹106 per share

Total Issue Size

23,75,00,000 shares(aggregating up to ₹2,517.50 Cr)

Important Dates for Canara HSBC Life Insurance Allotment

Event

Date

Tentative Allotment

October 15, 2025

Refunds Initiation

October 16, 2025

Credit of Shares to Demat

October 16, 2025

Listing Date

October 17, 2025

Canara HSBC Life Insurance Overview

Canara HSBC Life Insurance, established in 2007, is a leading private life insurer in India jointly promoted by Canara Bank, the country’s fourth-largest public sector bank, and HSBC Insurance (Asia-Pacific) Holdings Limited. According to the CRISIL Report, the company ranks third among public sector bank-led life insurers in terms of lives covered and recorded the third-highest weighted premium income growth among bank-led insurers between Fiscal 2022 and 2025.

As of June 30, 2025, it managed assets of ₹61,107.40 million and maintained a strong solvency ratio of 200.42%, exceeding the 150% regulatory requirement. Profit after tax grew at a CAGR of 13.26%, reaching ₹1,169.81 million in Fiscal 2025. The company’s extensive bancassurance network, including Canara Bank, HSBC India, and regional rural banks, contributed over 90% of new business premiums in Fiscal 2025.

Canara HSBC Life offers 20 individual and 7 group products across savings, protection, retirement, and ULIP categories. Emphasizing digital transformation, 99.7% of applications were processed digitally, improving persistency and customer satisfaction. Recognized for innovation, it has received industry awards for technology and data analytics excellence. With strong promoters, sound financials, and customer-centric digital initiatives, the company continues to strengthen its leadership in India’s life insurance sector.

Frequently Asked Questions (FAQs)

What is the opening and closing date of Canara HSBC Life Insurance?

Canara HSBC Life Insurance is open on 10 October 2025 and will close on 14 October 2025.

What is the price band of the Canara HSBC Life Insurance?

Its price band is fixed from ₹100 to ₹106 per share.

What is the GMP (Grey Market Premium) of Canara HSBC Life Insurance today?

The GMP on 14 October 2025 is ₹0, which leads to a possible listing price of ₹106.

What is the total issue size of Canara HSBC Life Insurance?

The total issue size of the Canara HSBC Life Insurance is ₹2517.50 crore, entirely as an “Offer for Sale”.

What is the expected listing date of Canara HSBC Life Insurance ?

This IPO is expected to be listed on BSE and NSE on 17 October 2025.

The mutual fund market in India is growing by the day. Today, thematic mutual funds in India offer a new opportunity for investors who invest not just in companies but in larger trends, such as Digital India, the energy transition, or the defense industry. They are on the verge of becoming the top-ranked mutual funds in India by 2026. In this blog, we’ll explore how thematic funds work, where they rank among mutual funds in India, and how you can choose your own top-rated mutual fund schemes/SIPs.

What are Thematic Mutual Funds?

Thematic mutual funds are funds that invest based on a specific theme or idea. This theme can encompass more than one sector. For example, a “Digital India” theme might include IT, telecom, and fintech companies.

How do they work?

These funds typically employ a top-down investment approach. The fund manager first determines which themes (such as defense, energy transition, electric vehicles) will be strong over the long term. Then, investments are made in various sectors and companies aligned with that theme. This way, investors become participants in the entire trend, not just a single sector.

List of Best Thematic Mutual Funds in India 2026

S.No

Fund Name

AUM (Rs Cr)

3 / 5 Years Return (%)

3 / 5 Years Category Average

Current NAV

1

ICICI Prudential Technology Fund

₹14,734Cr

14.85% / 18.55%

19.55% / 22.326%

₹190.58

2

Mirae Asset Great Consumer Fund

₹4,552Cr

17.13% / 21.80%

19.55% / 22.32%

₹94.97

3

ICICI Prudential Manufacturing Fund

₹6,490Cr

26.82 % / 28.84%

19.29 % / 22.23%

₹35.26

4

Sundaram Services Fund

₹4,333Cr

18.36% / 24.21%

19.71% / 23.99%

₹34.46

5

UTI-Transportation and Logistics Fund

₹3,741Cr

24.59% / 26.84%

19.29% / 23.28%

₹290.60

6

SBI Consumption Opportunities Fund

₹3,175Cr

14.59% / 24.31%

19.17% / 22.47%

₹306.53

7

HDFC Housing Opportunities Fund

₹1,285Cr

19.73% / 23.80%

19.29% / 23.28%

₹22.03

8

Aditya Birla Sun Life Manufacturing Equity Fund

₹1043Cr

18.65% / 18.32%

19.29% / 23.28%

₹32.05

9

Edelweiss Recently Listed IPO Fund

₹924Cr

15.61% / 19.77%

18.29% / 22.28%

₹27.14

10

SBI Comma Fund

₹702Cr

16.47% / 20.44%

19.29% / 22.44%

₹104.28

(Data as of 26 Sep 2025)

A brief overview of the Best Thematic Mutual Funds in India 2026 are given below:

1. ICICI Prudential Technology Fund

This fund is managed by ICICI Prudential AMC and primarily invests in IT sector and technology-related stocks. It was launched on June 22, 1993, and today is considered one of India’s leading technology-focused mutual funds. The fund’s objective is to provide investors with long-term exposure to the growth of the technology sector. It is currently managed by Vaibhav Dusad. The fund’s portfolio is concentrated in large IT giants such as Infosys, TCS, Wipro, and Tech Mahindra, providing it with strong stability and sector-specific exposure.

Fund details :

Min SIP

Min Investment

Fund Manager

₹100

₹5,000

Vaibhav Dusad

2. Mirae Asset Great Consumer Fund

Mirae Asset Great Consumer Fund is a thematic equity fund managed by Mirae Asset Mutual Fund. It aims to enable investors to participate in India’s consumption growth story. As the middle class and income levels in the country are growing, demand for consumer-based companies is also steadily increasing. The fund focuses on industries such as FMCG, automobile, telecom, and retail. The portfolio consists of a mix of large and reliable companies. ITC, Hindustan Unilever, and Asian Paints represent FMCG and branded consumer goods. Mahindra & Mahindra and Maruti Suzuki provide exposure to the automobile segment. Bharti Airtel captures the growth of the telecom sector, while Trent and Avenue Supermarts focus on retail and consumer services. Eicher Motors and Eternal Ltd. further diversify the portfolio.

Fund details :

Min SIP

Min Investment

Fund Manager

₹1000

₹5,000

Siddhant Chhabria

3. ICICI Prudential Manufacturing Fund

This fund is managed by ICICI Prudential AMC and focuses on India’s manufacturing sector. It aims to invest in companies that are directly linked to the country’s industrial progress and the “Make in India” initiative. The fund is currently managed by Antariksh Banerjee and is designed to capture the benefits of long-term manufacturing growth.

Its portfolio includes large and strong industries. Giants like Ultratech Cement and Ambuja Cements represent India’s manufacturing sector. Mahindra & Mahindra and Hindustan Aeronautics capture the growth story of automobiles and aerospace. Names like Cummins India and JSW Steel reflect the strength of the industrial machinery and metals sectors.

Fund details :

Min SIP

Min Investment

Fund Manager

₹100

₹5,000

Antariksha Banerjee

4. Sundaram Services Fund

Sundaram Services Fund is a thematic mutual fund managed by Sundaram Mutual Fund. Its objective is to invest in Indian services-based companies, as the service sector continues to grow in India’s economy. The fund was launched on February 26, 1996, and is currently managed by Rohit Seksaria. The fund’s portfolio focuses on leading service-based companies. Major companies like Bharti Airtel and Reliance Industries represent telecom and consumer services, while HDFC Bank and Axis Bank represent financial services strengths. Additionally, exposure to Tri-Party Repo (TREPS) helps manage liquidity. This mix provides a balanced and diversified perspective on the services sector.

Fund details :

Min SIP

Min Investment

Fund Manager

₹100

₹100

Rohit Seksaria

5. UTI-Transportation and Logistics Fund

UTI-Transportation and Logistics Fund is a sector-specific thematic fund managed by UTI Mutual Fund. The fund was launched on November 14, 2002, and is currently managed by Sachin Trivedi. Its objective is to benefit investors from the growth of India’s automobile, logistics, and transportation sectors. The portfolio includes key companies representing the auto and transportation sectors. Mahindra & Mahindra and Maruti Suzuki cover India’s passenger and utility vehicle segments. Eicher Motors and Bajaj Auto demonstrate strength in two-wheelers and commercial vehicles. Interglobe Aviation (IndiGo) provides air traffic exposure, while Eternal Ltd. further diversifies the portfolio.

Fund details :

Min SIP

Min Investment

Fund Manager

₹500

₹5,000

Sachin Trivedi

6. SBI Consumption Opportunities Fund

SBI Consumption Opportunities Fund is a thematic equity fund managed by SBI Mutual Fund. It was launched on February 7, 1992, and is currently managed by Ashit Desai. The fund aims to capture the story of India’s growing consumption sector. As income levels and consumer demand rise, the prospects for consumption-based companies are also brightening. Its portfolio includes leading consumption companies. Bharti Airtel represents telecom consumption, while Jubilant FoodWorks and Britannia Industries cover the Indian food and FMCG segments. Major companies like Hindustan Unilever and Asian Paints represent premium consumer brands. Mahindra & Mahindra provides strong exposure to automobile consumption.

Fund details :

Min SIP

Min Investment

Fund Manager

₹500

₹5,000

Ashit Desai

7. HDFC Housing Opportunities Fund

HDFC Housing Opportunities Fund is a thematic equity fund managed by HDFC Mutual Fund. Launched on December 10, 1999, the fund is currently managed by Srinivasan Ramamurthy. Its objective is to capture opportunities in India’s housing and infrastructure sectors. Given the country’s urbanization and growing housing demand, this theme is considered relevant for the long term. The fund’s portfolio focuses on large financial institutions and infrastructure companies. These include major financial institutions like HDFC Bank and ICICI Bank, which are involved in housing finance and retail loan growth. Larsen & Toubro and Ambuja Cements represent the strength of the construction and cement sectors. NTPC, the backbone of energy supply, and State Bank of India, as the country’s largest bank, provide further balance to this theme.

Fund details :

Min SIP

Min Investment

Fund Manager

₹100

₹100

Srinivasan Ramamurthy

8. Aditya Birla Sun Life Manufacturing Equity Fund

Aditya Birla Sun Life Manufacturing Equity Fund is a thematic fund managed by Aditya Birla Sun Life AMC. It was launched on September 5, 1994, and is currently managed by Harsh Krishnan. The fund focuses on opportunities in India’s manufacturing sector and invests in companies directly involved in industrial production, automobiles, engineering, and basic industries. The fund’s portfolio includes several prominent and trusted names. Reliance Industries is a leading player in diversified manufacturing and energy. Hindalco Industries is a leader in metals and aluminum manufacturing. Maruti Suzuki and Mahindra & Mahindra demonstrate strong presence in automobile manufacturing. Cummins India provides exposure to industrial machinery and engineering, while United Breweries contributes to consumer and beverage manufacturing.

Fund details :

Min SIP

Min Investment

Fund Manager

₹1000

₹1,000

Harsh Krishnan

9. Edelweiss Recently Listed IPO Fund

The Edelweiss Recently Listed IPO Fund is a unique thematic fund managed by Edelweiss Mutual Fund. It was launched on August 23, 2007, and is currently managed by Bhavesh Jain. The fund invests in companies that have recently listed through an IPO (Initial Public Offering). Its objective is to enable investors to participate in the early growth story of newly listed businesses. The fund’s portfolio focuses on new and emerging businesses across diverse sectors. It includes consumer and automobile brands such as Hyundai Motor India and Vishal Mega Mart. Swiggy reflects the strength of the digital consumption and food delivery sectors. Bajaj Housing Finance provides exposure to financial services, and Sai Life Sciences and Sagility Ltd. represent growth in the healthcare and research sectors.

Fund details :

Min SIP

Min Investment

Fund Manager

₹500

₹5000

Bhavesh Jain

10. SBI Comma Fund

SBI Comma Fund is a thematic equity fund managed by SBI Mutual Fund. It was launched on February 7, 1992, and is currently managed by Dinesh Balachandran. The fund primarily invests in the commodities, materials, and energy sectors. These sectors, linked to India’s industrial and energy needs, have long been considered the backbone of economic growth, and this is the fund’s primary focus. The portfolio includes leading commodity and energy companies. Tata Steel and Vedanta provide exposure to metals and mining. Reliance Industries represents the energy and petrochemical sectors. Ultratech Cement covers construction and infrastructure growth, while ONGC is a major player in oil and gas production. CESC Ltd. also provides stability to the power supply and utilities sectors.

Policy Support : The Indian government has paid special attention to sectors such as defense, infrastructure, energy transition, and the digital economy in recent years. Policy support in these sectors can provide thematic funds with the opportunity for long-term, stable growth.

Benefiting from Changing Economic Trends : Trends such as digital transactions, electric vehicles, healthcare, and renewable energy will strengthen in the coming years. Thematic mutual funds offer investors the opportunity to participate in these changes from an early stage.

Potential for Additional Returns : When the chosen theme remains relevant over the long term, thematic funds have the potential to deliver better returns than traditional diversified equity funds. However, this is not always guaranteed and involves higher risk.

A Different Approach from Sectoral Funds : Sectoral funds focus on a single industry, while thematic funds invest in multiple industries within a larger story. This helps spread the risk somewhat.

Growing Investor Interest : Investor interest in thematic funds has increased over the past few years. This is because investors prefer to invest in sectors and trends that have strong future potential.

Potential to Outperform Indices : Over some periods, thematic funds have outperformed broad indices. However, their performance depends on trends and market conditions, so investors should have realistic expectations.

Strategic Role in Portfolios : These funds are best held as satellite allocations rather than as part of a core portfolio. This allows investors to take advantage of emerging trends while maintaining portfolio diversification.

Emerging Investment Themes in India 2026

Defense and Aerospace : The country is moving towards becoming self-reliant in defense equipment. Continued large orders and export opportunities are strengthening this theme.

Infrastructure and PSUs : Government spending on roads, railways, and power is steadily increasing. This is benefiting not only infrastructure companies but also many public sector undertakings.

Energy Transition : In keeping with climate goals, there is a significant emphasis on renewable energy. Solar, wind, and battery technology are at the center of this transition.

Electric Vehicles and Electronics : EV adoption is increasing, and domestic electronics manufacturing is also strengthening. Battery and charging networks are driving this trend.

Digital and Fintech : Digital payments and online services have become a daily necessity. Investment in data security and cloud services will also increase in the coming years.

Healthcare and Pharma : Growing demand for healthcare and the discovery of new medicines are continuously strengthening this sector.

Premium Consumption : As incomes rise, people are increasingly investing in premium and branded products. This theme is expected to deepen in the coming years.

Thematic mutual funds are attractive, but they carry some significant risks that should not be overlooked.

Relying solely on the theme : People often invest under the influence of a story or trend. However, not every theme succeeds. The true strength comes from the companies’ earnings and business models.

Limited Diversification : Like sectoral funds, thematic funds operate within a limited range. If the theme weakens, the entire portfolio can be affected.

Liquidity Issues : Some themes are based on small stocks. These stocks cannot be easily sold during difficult times, which can increase losses.

The Importance of Timing : Timely entry and exit are crucial in these funds. Late entry or hasty exit can impact returns.

Investor Behavior : FOMO in a bull market and panic in a bear market – this is the biggest mistake. Repeated decisions like this can weaken actual returns.

Taxation of Thematic Funds in India (2026 Update)

Equity-oriented Thematic Funds Tax Rates

Short-Term Capital Gains (STCG) : If you sell equity-invested units within 12 months or less, the STCG tax rate will be 20%.

Long-Term Capital Gains (LTCG) : If the holding period is more than 12 months, the LTCG tax rate will be 12.5%.

Exemption : The first LTCG up to ₹1.25 lakh is tax-free. That is, if your LTCG is less than ₹1.25 lakh, no tax will be payable.

Thematic mutual funds offer investors the opportunity to participate in India’s rapidly changing economy and emerging trends. Whether it’s manufacturing, consumption, infrastructure, or technology, each theme offers long-term potential. However, it’s also true that they carry relatively higher risks. Therefore, it’s always wise to include them in your portfolio with a limited allocation and a long-term view.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Let’s look at a different aspect of the financial market except from buying and selling shares, this is mutual funds and dividends. So, have you ever wondered if you get extra cash back from your mutual fund investments? Many people think of this as a ‘dividend’ just like a small bonus for investing.

But have you ever wondered, do mutual funds pay dividends? The answer is yes, but it’s not exactly what you might think. It’s not really “extra” money that you get, so understanding what happens to dividends in mutual funds is one of the most important things for an investor.

In this blog we will look upon how mutual funds pay dividends to the investors.

What’s a Mutual Fund Dividend?

A mutual fund is like a big investment basket managed by a registered & professional fund manager. This basket makes money in a few ways:

Company Profits: If your fund owns shares of a company like TCS, and TCS decides to share its profits, your fund gets a piece of that.

Interest Earnings: If your fund has lent money (by buying bonds), it earns interest, just like a bank FD.

Smart Selling: When the fund manager sells an investment for more than they paid, the fund makes a profit.

All this money gets collected in the fund. After paying its running costs, the leftover profit can be shared with you.

Here’s something every investor in India needs to know. In 2021, the market regulator and watchdog SEBI changed the name of the “Dividend Option” to IDCW which stands for Income Distribution cum Capital Withdrawal.

SEBI wanted to be crystal clear and protect the investors from being misled. The old name, “dividend,” made it sound like you were getting extra bonus money from your investments but this was not the whole story.

Income Distribution: This is the part that comes from the fund’s actual earnings.

cum Capital Withdrawal: It means some of the money you’re getting is your own invested money being handed back to you.

By this you can understand that IDWC isn’t a bonus just like a dividend. It’s the fund giving you a mix of its profits and a little bit of your own money back.

How do mutual funds pay dividends?

The fund gathers up all the profits it has made.

The fund manager looks at the pile of profits and decides if there’s enough to share.

If it’s a “yes,” the money is sent straight to your bank account. By law, it has to get to you within seven working days.

IDCW Payout: Investors can get their cash directly and it lands in your linked bank account. This is best suitable for people who need a regular stream of money, like retirees.

IDCW Reinvestment: Instead of cash, the money is used to buy you more units in the fund. Here the investor does not cash out the profits rather get more funds in it.

Growth Option: This is the most popular choice as, no money is paid out, all the profits are ploughed back into the fund to help it grow bigger and faster making it more profitable and valuable over time.

Feature

IDCW (Dividend) Plan

Growth Plan

Profits

You either get cash or more units.

Money is put back into the fund to grow.

Price

Price of the units drop after the payout

Price of unit grows over time

Units

Stays the same or gets reinvested

Stays the same

Best suitable for

Someone who needs cash in hand regularly.

Someone who wants money to grow over the years.

Taxation

You pay tax on it in the year you receive it.

You only pay tax when you decide to sell your units

How are Dividend Pay Decided?

The dividends in mutual funds are not 100% guaranteed, it’s not like a fixed deposit where you know exactly what returns you will be getting.

The fund manager is the one who takes the decision after considering the following:

Profit Generated: A fund can only be distributed if there is enough profit generated.