In today’s fast-paced world, understanding personal finance is more important than ever. Managing personal finances is the key to achieving financial stability, ensuring security, and maintaining peace of mind. But what is personal finance exactly? At its core, personal finance covers all the financial decisions related to income, spending, savings, and investing. Having a firm grasp of personal finance basics can significantly impact your financial future, helping you achieve long-term goals and avoid common financial pitfalls.

This article will delve deep into personal financial management, explaining its importance and offering practical insights into how you can take control of your financial future.

Understanding Personal Finance

Personal finance encompasses a wide range of financial activities that an individual or household engages in to manage money effectively.

Personal Finance Definition

Personal finance refers to the process of planning, managing, and handling one’s financial resources to achieve personal financial goals. It covers essential aspects such as budgeting, saving, investing, and debt management to ensure financial stability and growth.

Core Areas of Personal Finance

- Income Management – Tracking earnings from salaries, businesses, or passive income sources.

- Expense Planning – Understanding and controlling where you spend your money.

- Savings Strategy – Setting aside money for future needs and emergencies.

- Investment Planning – Growing wealth through investing in assets like stocks, bonds, and mutual funds.

- Risk Management and Insurance – Protecting financial assets through insurance and contingency planning.

By focusing on these key areas, individuals can take control of their finances and work towards a secure financial future.

Why Is Personal Finance Important?

Many people overlook the importance of personal financial management until they face financial difficulties. Managing personal finances efficiently can lead to numerous benefits:

1. Preparation for Emergencies

Life is unpredictable, and financial emergencies can arise anytime. Whether it’s a sudden job loss, a medical emergency, or an unexpected expense, having a solid financial plan can help you navigate through tough times without resorting to debt.

2. Achieving Financial Goals

Proper personal finance management allows individuals to set realistic financial goals, such as buying a house, funding education, or planning for retirement. By managing money wisely, one can reach these goals without financial stress.

3. Ensuring a Comfortable Retirement

Retirement planning is an essential part of personal finance. Through consistent saving and investing, individuals can secure a financially stable future and enjoy a comfortable lifestyle even after they stop working.

4. Reducing Financial Stress

Financial stress can negatively impact mental and physical health. By maintaining a well-organized financial plan, individuals can avoid unnecessary financial burdens and improve their overall well-being.

Key Components of Personal Finance Management

The key components of personal finance management are:

1. Budgeting

A budget is a financial plan that helps track income and expenses. Creating a budget involves:

- Listing all sources of income.

- Categorizing fixed and variable expenses.

- Setting spending limits for discretionary expenses.

- Adjusting the budget to align with financial goals.

2. Saving

Savings is crucial to achieve financial security. Strategies for effective saving include:

- Establishing an emergency fund (3-6 months of living expenses).

- Setting aside a percentage of income for long-term goals.

- Utilizing high-yield savings accounts.

3. Investing

Investing helps grow wealth over time. Key investment options include:

- Stocks – Ownership in companies that can generate returns in the form of dividends and capital appreciation.

- Bonds – Low-risk securities offering fixed income in the form of coupon payments.

- Mutual Funds – Pooled investments managed by professionals.

- Real Estate – Investing in residential and commercial properties that can appreciate over time.

4. Debt Management

Avoiding excessive debt is critical for financial stability. Effective debt management strategies include:

- Paying off high-interest debts first.

- Making pre-payments to reduce outstanding loans.

- Avoiding unnecessary loans and impulse purchases.

5. Insurance and Protection

Financial protection against unexpected events is an essential part of personal finance basics. Important types of insurance include:

- Health Insurance – Covers medical expenses and emergencies.

- Life Insurance – Provides financial security to dependents.

- Property Insurance – Protects assets like homes and vehicles.

Personal Finance Management Strategies

1. Setting Financial Goals

Clear financial goals help create a roadmap for financial success. Steps to setting goals include:

- Identifying short-term goals (Example: paying off credit card debt, saving for a vacation).

- Establishing long-term goals (Example: buying a house, retirement planning).

- Creating action plans to achieve these goals within their respective timeframes.

2. Developing a Financial Plan

A solid financial plan should include:

- A detailed budget and expense tracker.

- A well-structured savings and investment plan.

- A risk management strategy with appropriate insurance coverage.

- Track progress towards financial goals and adjust the plan as needed.

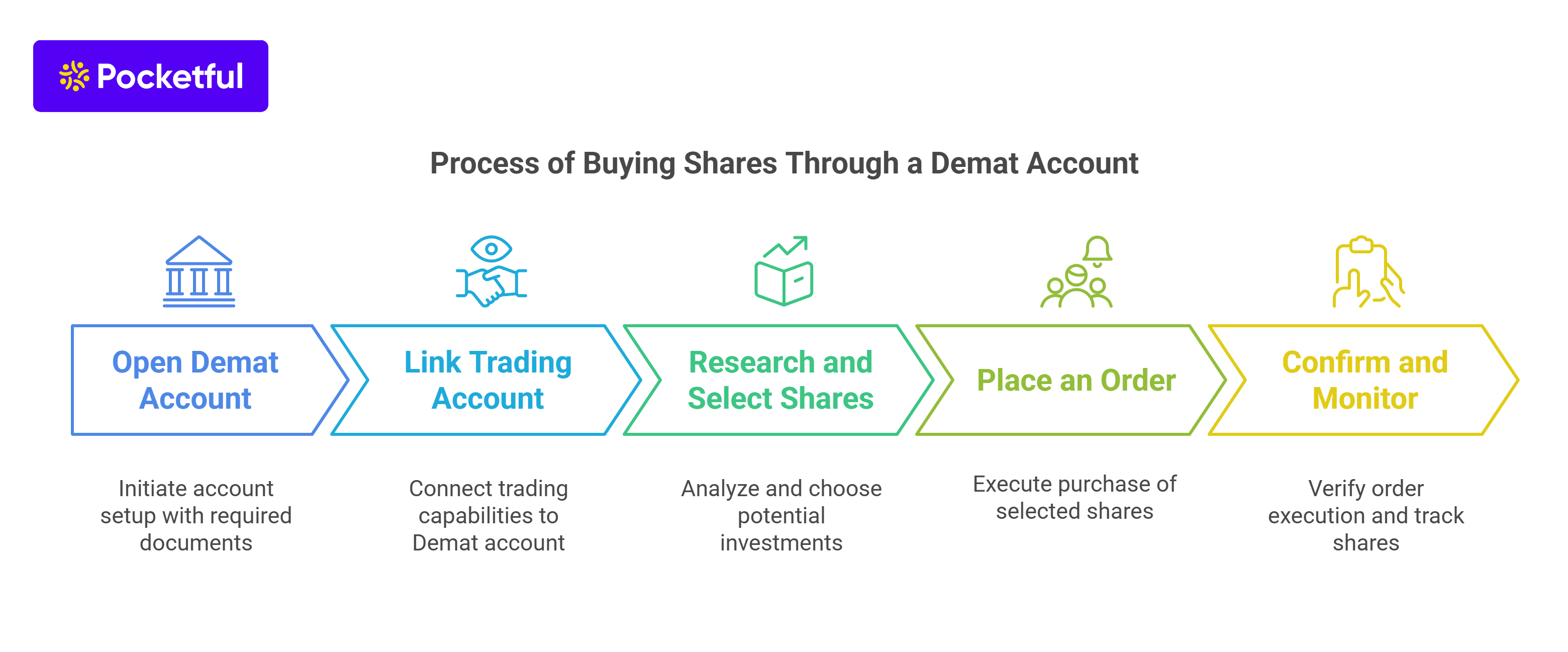

3. Utilizing Financial Tools and Resources

Several tools can simplify financial management, such as:

- News Apps – Economic Times, Mint, Finshots, etc.

- Investment Platforms – Pocketful, Zerodha, etc.

- Financial Literacy Resources – Books, podcasts, and online courses.

Personal Experience and Lessons Learned

Learning about personal financial management has been a game-changer in my life. A few years ago, I struggled with uncontrolled spending, mounting debt, and zero savings. It was only when I started tracking my finances, setting realistic goals, and investing wisely that I saw a transformation.

One of the best decisions I made was setting aside funds for saving and investments before spending on discretionary items. Gradually, I built an emergency fund and started investing in stocks and mutual funds. The discipline of sticking to a budget also helped me eliminate unnecessary expenses and focus on my financial goals.

Key lessons I’ve learned:

- Start early – The sooner you learn to manage your finances, the better your financial future.

- Avoid frequent lifestyle upgrades– Increased earnings shouldn’t mean unnecessary spending.

- Be patient – Wealth accumulation takes time; consistent efforts pay off.

By applying these principles, I have achieved financial stability and peace of mind. I encourage everyone to take control of their finances and make informed financial decisions.

Conclusion

Personal finance is a critical aspect of life that influences financial security, stress levels, and overall well-being of an individual. Understanding and implementing personal finance basics—budgeting, saving, investing, and managing debt—can lead to a financially stable future.

By taking proactive steps toward personal financial management, setting clear financial goals, and utilizing the right resources, anyone can achieve financial independence. Whether you’re just starting or looking to improve your financial habits, remember that small, consistent steps can make a big difference in shaping your financial future.

Frequently Asked Questions (FAQs)

Why is personal finance important?

It helps prevent financial stress, prepares you for emergencies, secures your retirement, and supports goal achievement.

How can I start managing my finances?

Create a budget, track expenses, save consistently, invest wisely, and avoid unnecessary debt.

What is the 50/30/20 rule?

Allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

How can I reduce debt effectively?

Prioritize high-interest debt, make extra payments, and avoid unnecessary loans.