Commodity trading is the process of buying and selling of commodities such as gold, crude oil, copper, etc., in spot markets or derivative markets. Commodity trading has numerous advantages as it helps market participants diversify their portfolios, speculate on future price movements, etc.

However, commodity trading can result in significant losses as prices can change suddenly due to certain factors such as weather, global demand, political events, etc. This makes it difficult to predict how much profit or loss a trader might make.

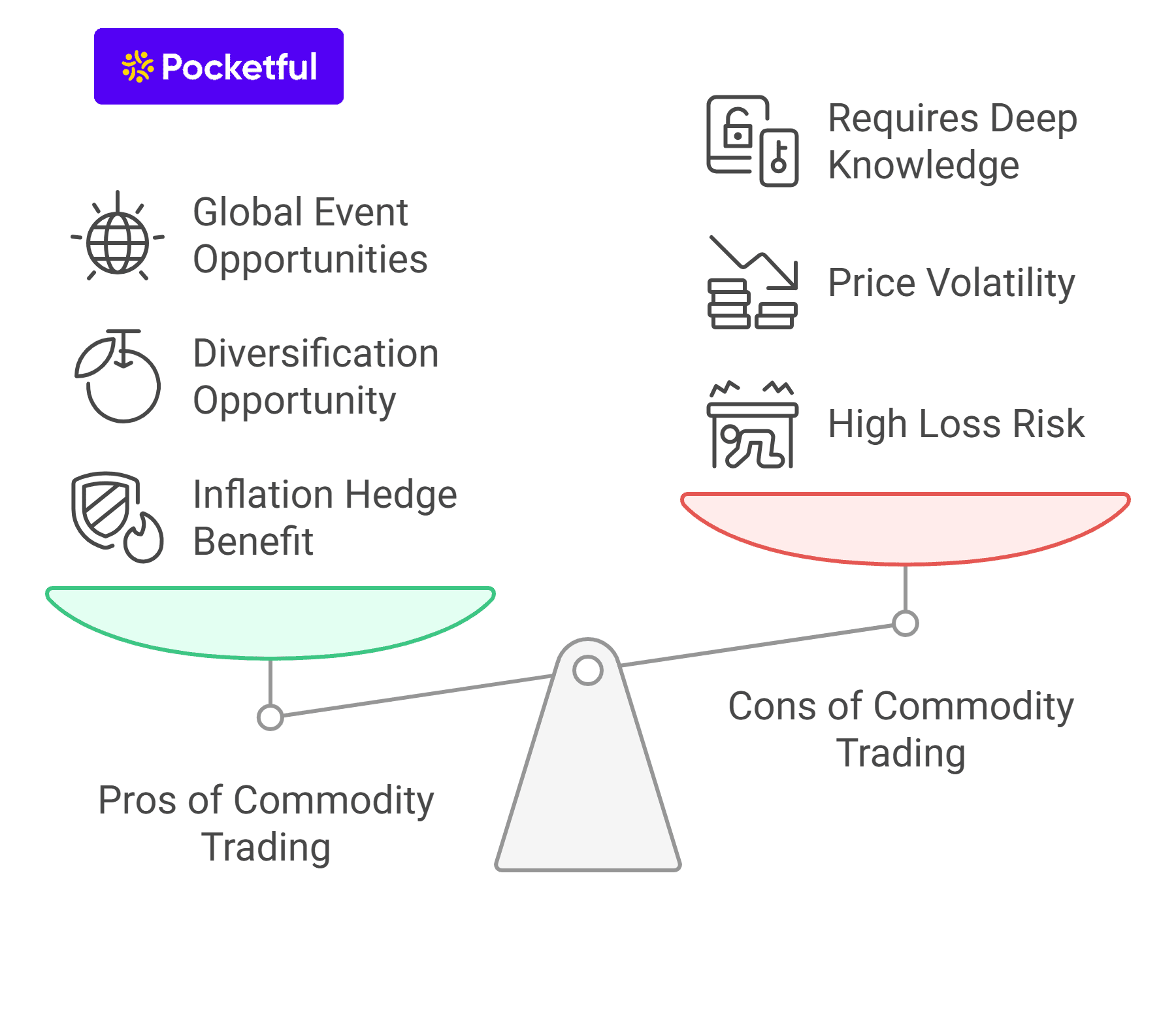

In this blog, we will discuss the pros and cons of commodity trading, which will help you make smarter trading decisions.

Pros of Commodity Trading

The pros of commodity trading are:

1. Protection Against Inflation

Commodity trading provides a powerful hedge against inflation. Market participants can use derivative contracts to protect their portfolios against inflation. Furthermore, futures contracts allow traders to lock in the price of a commodity for a transaction at a future date. This helps them fix the cost of raw materials and mitigate the impact of rising inflation.

When inflation rises, the price of raw goods rises, and these can specifically include goods like oil, metals, and agricultural items. For example, for a business reliant on raw materials for its manufacturing activities, it is essential to control the input costs. If inflation is expected to rise, the company can buy the futures contracts of the specific raw material and basically fix their buying price for a transaction at a future date.

2. Portfolio Diversification

Commodities are usually traded through futures and options on platforms like MCX. These contracts are not strongly correlated with traditional assets, such as equities and bonds. For example, commodities like gold or oil often perform well when stock markets are underperforming, thus decreasing your portfolio’s overall risk.

3. Opportunity During Global Events

Global events can cause significant price movements in commodities. Trading on exchanges like MCX provides the opportunity to profit from such volatility, as global crises frequently impact commodities prices.

4. Higher Returns

Commodity trading offers margin trading, which means traders can hold a large position with a small capital. If prices move favorably, the profits are significant. However, leverage is also associated with increased risk, as if prices move in the opposite direction, losses can be significant.

5. Transparent and Fair Pricing

Commodity trading often occurs on regulated exchanges such as MCX, ensuring transparent pricing and no price manipulation. All trading takes place on electronic commodity trading platforms, which helps prevent price manipulation. This increases the market participant’s confidence and makes the market more transparent and trustworthy.

Check Out – Free Commodities Screener

Cons of Commodity Trading

The cons of commodity trading are:

1. High Risk of Loss

Commodity trading involving futures and options can be risky. This is primarily because of the leverage involved, which is why even small price movements can result in big losses.

2. Price Volatility

Commodity prices can fluctuate rapidly. This can be due to a variety of factors, such as weather, regulatory changes and world events. Just for instance, a natural calamity can harm crops or halt oil production, which can increase prices.

Similarly, a reduced demand for a specific commodity can cause price declines. These unexpected price swings are difficult to forecast. Even experienced traders sometimes struggle with these unpredictable price changes, making commodity trading dangerous and complex to manage.

3. Requires Deep Knowledge

Successful commodity trading requires a thorough grasp of market trends, supply and demand dynamics, etc. This helps you make wise trading decisions, particularly when trading in futures and options.

For example, price swings can be induced by political upheaval in OPEC nations. Because of the turmoil, oil prices may rise or fall significantly, making wise trading decisions extremely tough.

Things to Keep in Mind Before Trading in Commodities

You should remember the following points before trading in commodities:

- A higher trading volume in a specific commodity means more market participants are actively buying and selling, which can lead to bigger price changes. It also results in more trading opportunities.

- Know how much risk you’re willing to take. High-risk trades can give you more profit, but they also carry a higher chance of losing money.

- Keep a close watch on the price trends of commodities. Prices of some commodities can go up fast and drop just as quickly, which makes them risky.

- Don’t put all your money into one commodity. Spreading your trading positions across commodities reduces risk and increases your chances for profit.

Read Also: How to Trade in the Commodity Market?

Conclusion

Commodity trading on platforms such as MCX can provide lucrative trading opportunities. However, trading in commodities also involves risks as commodity prices can be extremely volatile. This is due to variables such as weather, politics, and global demand, which make these markets unpredictable.

Understanding how prices change is critical for success in commodities trading helps you stay on top of market trends. Knowing your financial objectives and the amount of risk you’re prepared to accept is critical.

Choose which commodities to trade and look for strategies on how to take advantage of price fluctuations effectively. Understanding your risk tolerance is crucial. Diversifying your trading positions across many commodities reduces risk.

Stay updated, monitor market movements, and alter your trading plan when necessary. With the appropriate strategy, you can make well-informed trading decisions, helping you achieve your financial goals.

| S.NO. | Check Out These Interesting Posts You Might Enjoy! |

|---|---|

| 1 | Understanding Commodity Market Analysis |

| 2 | What is the Timing for Commodity Market Trading? |

| 3 | Risks in Commodity Trading and How to Manage Them |

| 4 | 5 Tips for Successful Commodity Trading |

| 5 | Stock Market vs Commodity Market |

Frequently Asked Questions (FAQs)

What is commodity trading?

Commodity trading is the buying and selling of raw materials like gold, oil, and agricultural products in spot or derivative markets to profit from price fluctuations and hedge against risk.

What are the key advantages of commodity trading?

Commodity trading offers protection from inflation, portfolio diversification, and potential high returns. Futures contracts can be used to lock in prices, and market volatility during global events creates additional trading opportunities.

What risks are involved in commodity trading?

Commodity trading carries high risk due to leverage and unpredictable price volatility. Market price changes due to weather, global demand shifts, or political events can result in significant financial losses.

How does commodity trading act as a hedge against inflation?

Commodity trading, particularly through futures contracts, enables traders to lock in prices. This strategy protects against rising raw material costs during inflationary periods.

What should traders consider before engaging in commodity trading?

Traders should assess risk tolerance, monitor market trends, diversify positions, and gain deep market knowledge. Understanding supply and demand dynamics is crucial for making informed trading decisions.