Opening a Demat account online is a simple and most convenient way to manage your investments in stocks, bonds and other securities. With a Demat account, you can store all your financial assets in electronic form, which makes it easier to buy, sell and monitor your portfolio.

In this blog, we will walk you through the steps of opening a Demat account online, from choosing a reliable depository participant (DP) to completing the necessary documentation. Whether you’re a beginner or an experienced investor, this process ensures uninterrupted access to the stock market from the comfort of your home.

What is a Demat account and how does it work?

The full form of a Demat account is a “Dematerialized account”. It is an electronic account used to store and manage your financial securities such as stocks, bonds, and mutual funds in digital form. It eliminates the need for physical certificates, ensuring the safe and convenient handling of investments. With a Demat account, you can buy, sell, and transfer securities easily, making it an essential tool for participation in the stock market.

A Demat account works like a bank account, but instead of holding the money, it holds your securities. When you buy shares, they are credited to your Demat account, and when you sell them, they are debited. The account ensures that all transactions are secure and updated in real-time.

To begin your investing journey, you need both a Demat account and a trading account. The trading account is used to buy and sell securities in the stock market, and the Demat account is used to store securities. Both accounts are linked for seamless investing experience.

How to Open the Demat Account?

Wondering how to open a Demat account or how to open a Demat account online? This process is very simple. Choose a Depository Participant (DP) such as a bank or brokerage firm and follow these steps:

- Visit the DP’s website and select the option to open a “Demat Account online.”

- Fill out the application form and upload the necessary documentation, like PAN card, Aadhaar, and bank details.

- Complete the in-person verification process online or offline.

- Once verified, then your Demat account will be activated.

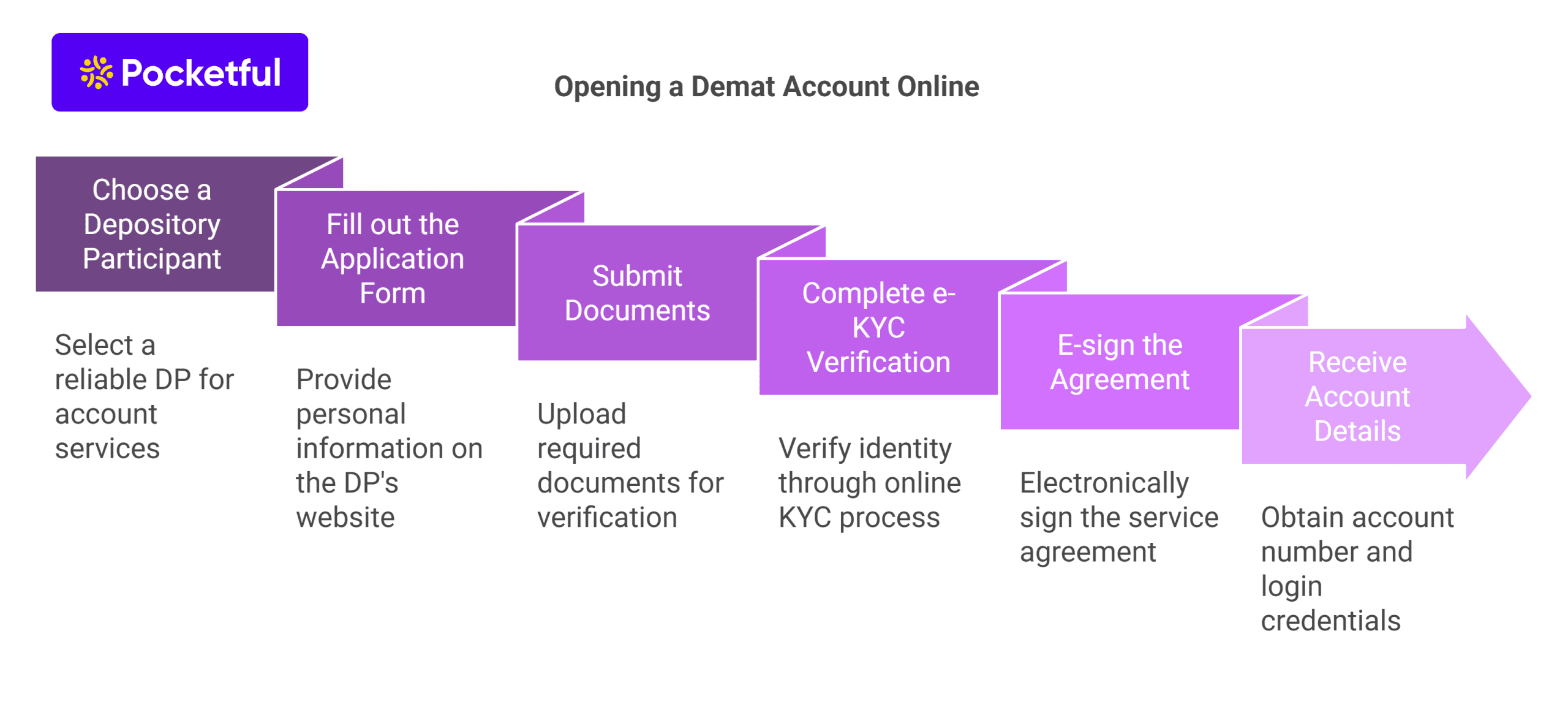

Steps for Opening A Demat Account Online

Opening a Demat account online is a simple process as it allows you to manage your investments efficiently. Follow these simple steps to open a Demat account and start trading online:

1. Choose a Depository Participant (DP)

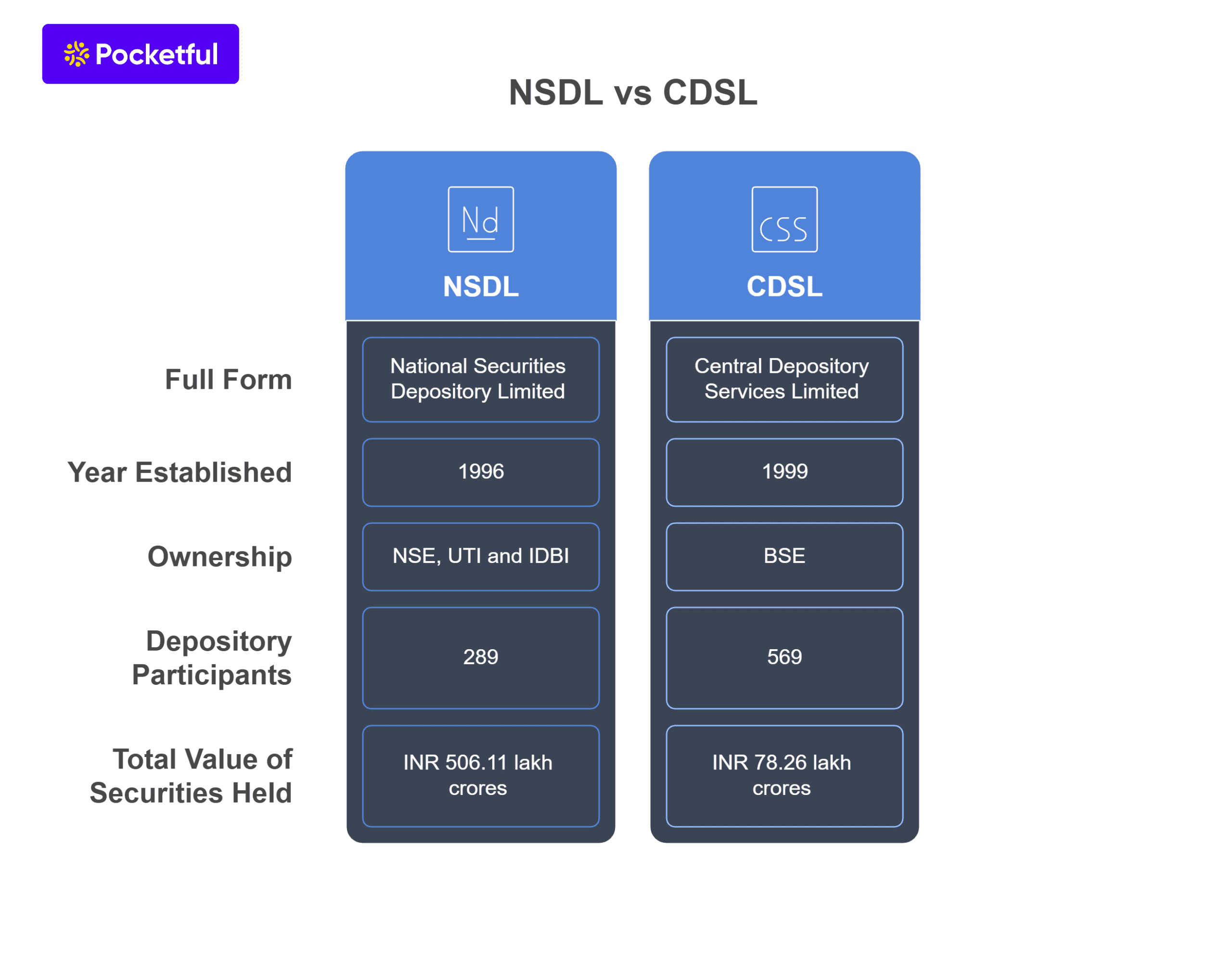

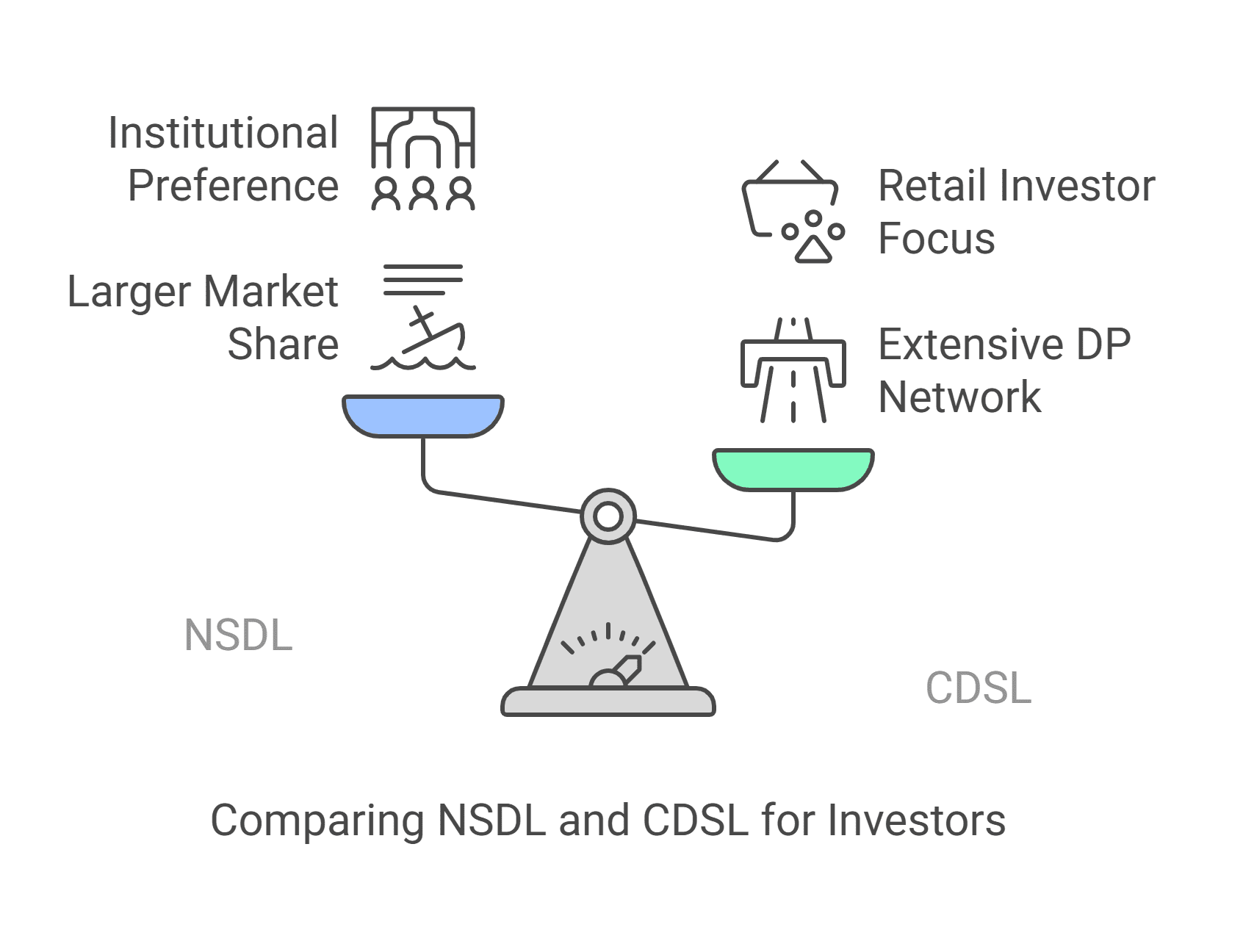

Before opening a Demat account online, select a reliable depository participant (DP) such as a bank, financial institution or brokerage firm. These entities are authorized by depositories like NSDL or CDSL to offer Demat account services.

2. Fill out the Application Form

Visit the DP’s website and select the option to open a “Demat Account online.” You will need to fill out an application form that asks for basic personal information such as name, address, date of birth, and contact details.

3. Submit Documents

Upload the required documents, such as your PAN card, Aadhaar card, passport-size photographs and bank details. These documents serve as identity proof and address verification.

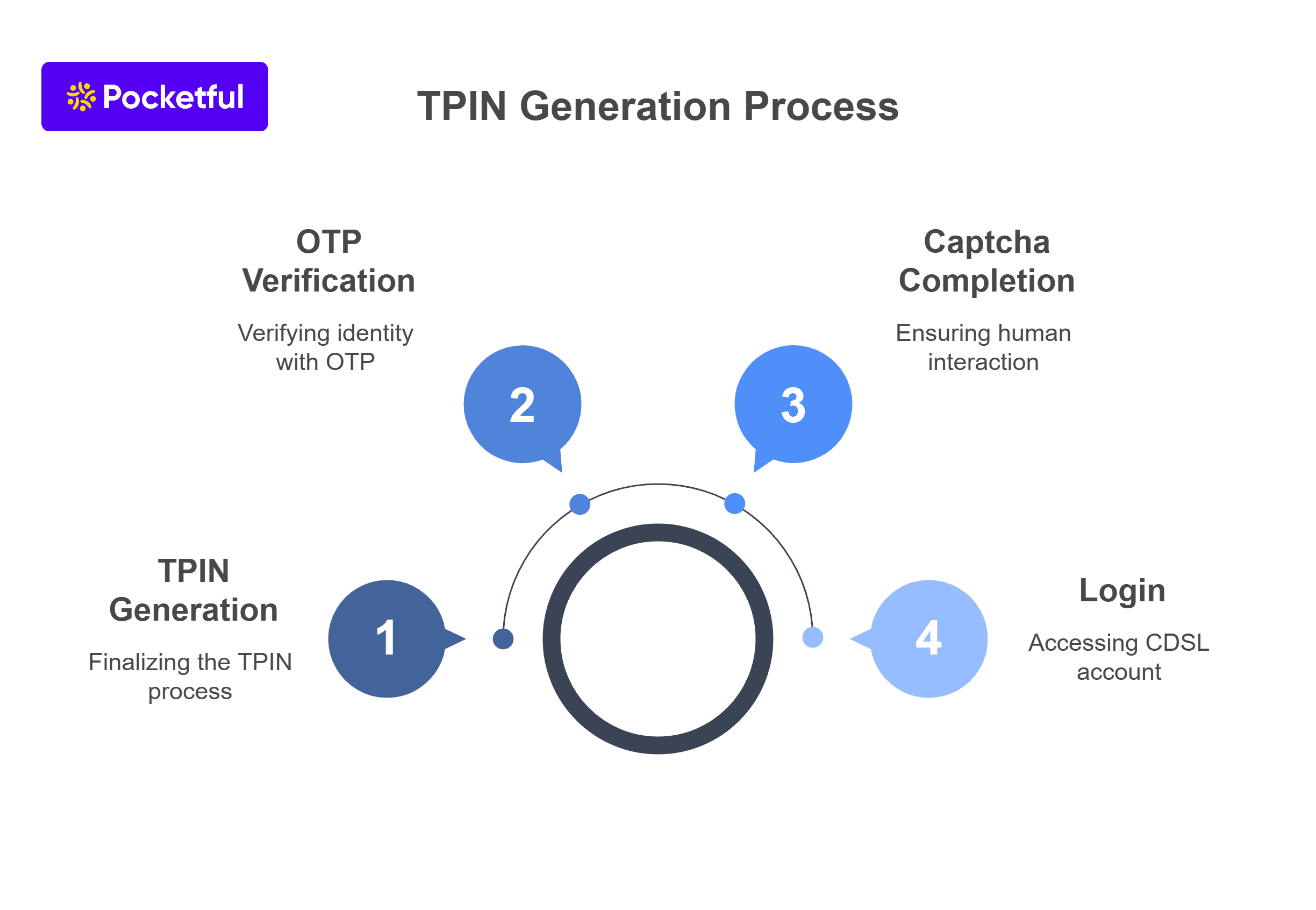

4. Complete e-KYC Verification

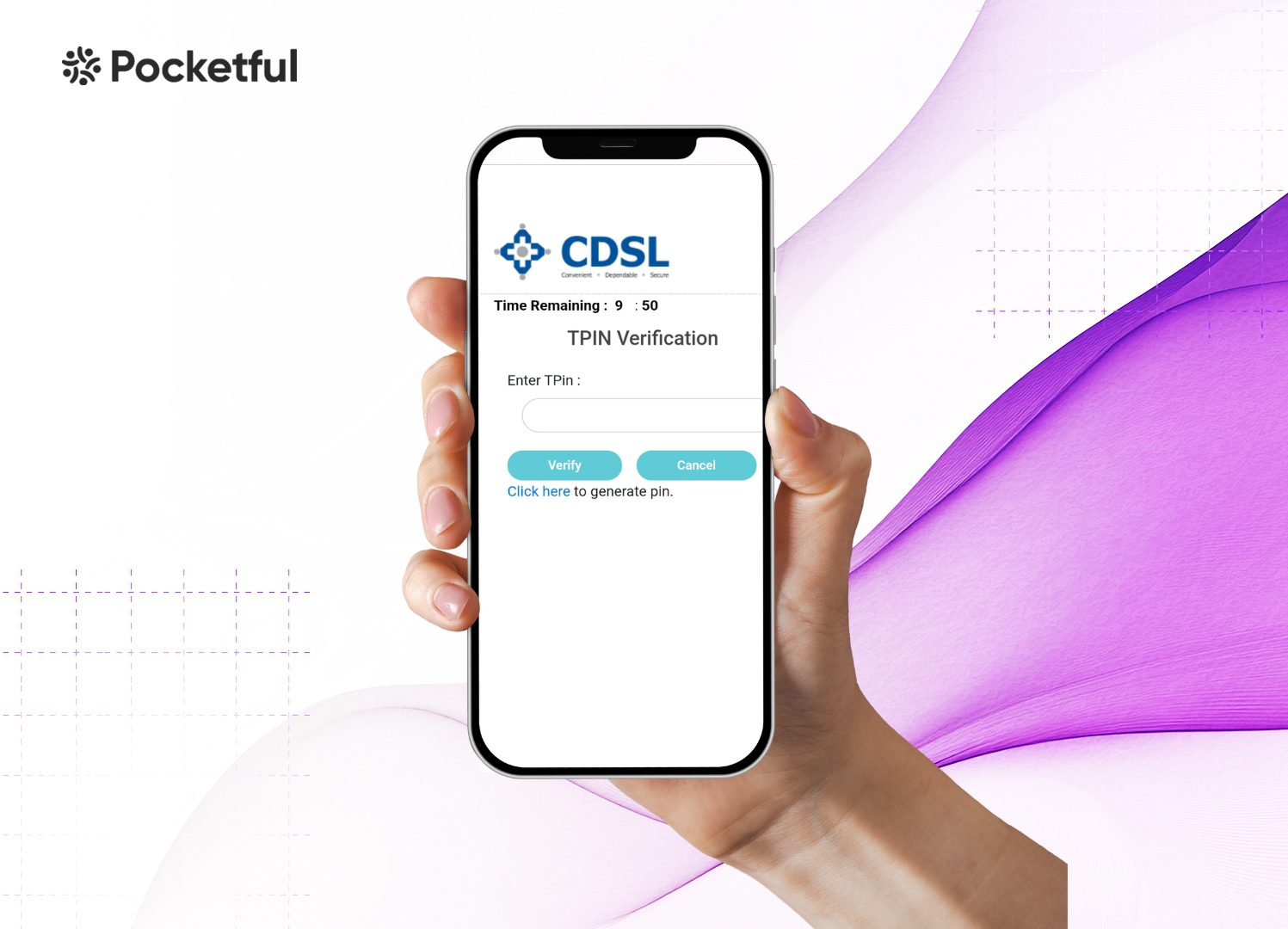

Complete the Know Your Customer (KYC) process online. You can verify your identity using the Aadhaar based e-KYC or video verification. Some DPs may also require in person verification (IPV) through video calls.

5. E-sign the Agreement

E-sign an agreement with the DP that outlines your rights, obligations and the DP’s terms of service. This is usually done electronically.

6. Receive Account Details

Once your documents and details are verified by the depository participant (DP), your Demat account will be activated. You will receive your Demat account number (also known as Beneficiary Owner ID) and login credentials via email. You may also open a trading account alongside the Demat account and do transactions.

Following these steps to open a Demat account and a trading account ensures you are ready to start investing.

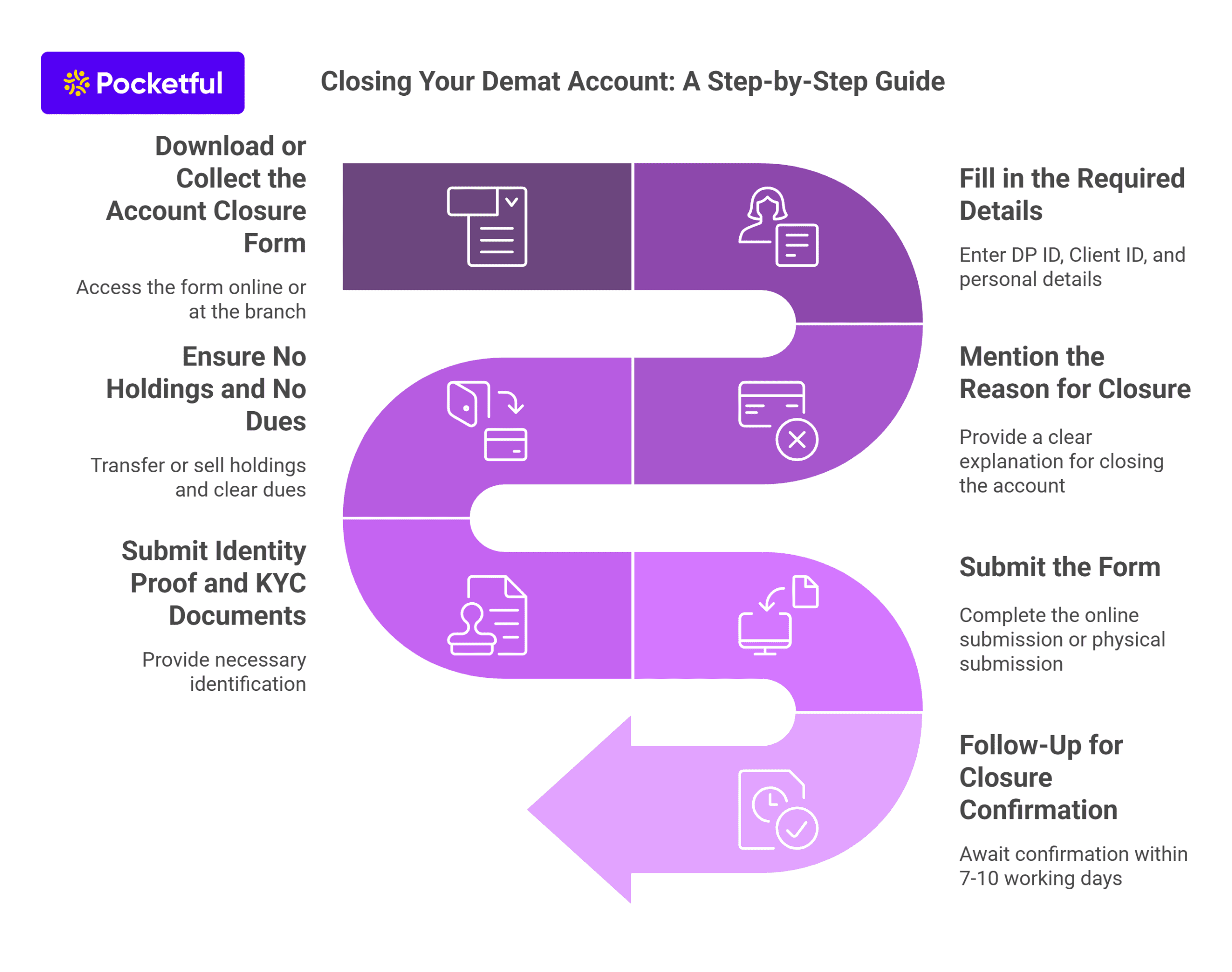

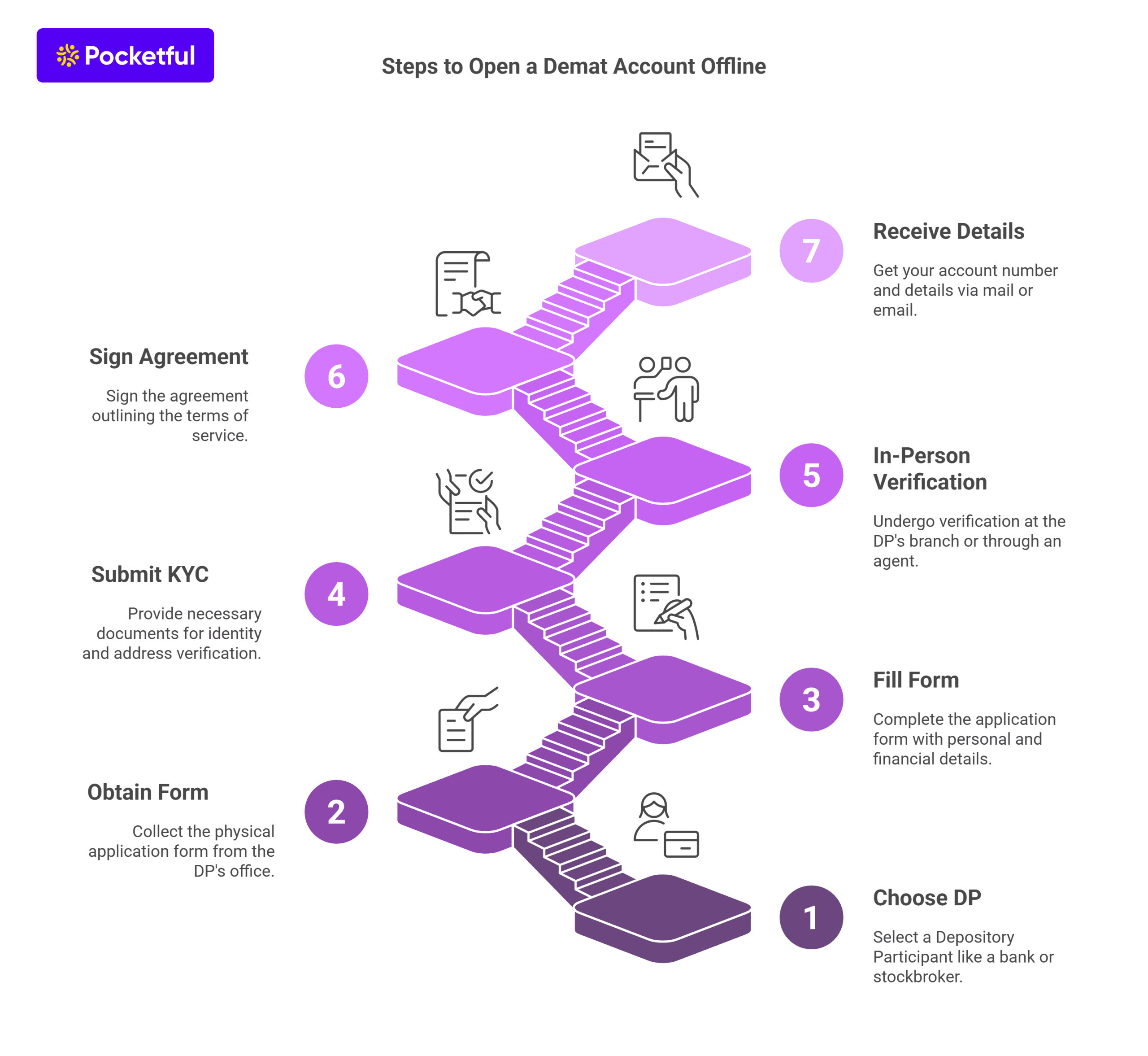

How to Open a Demat Account Offline

Opening a Demat account offline is a traditional method for those who prefer in person interactions or may not have access to the internet for online applications. Here’s a step-by-step guide on how to open a Demat account offline:

1. Choose a Depository Participant (DP)

The first step is selecting a Depository Participant (DP) such as a bank, stockbroker or financial institution. These DPs are authorized by depositories lіke NSDL or CDSL.

2. Obtain the Application Form

Visit the DP’s office or branch to collect the physical Demat account application form. You can also download this form from their website.

3. Fill Out the Application Form

Fill the application form with your personal details including the name, address, PAN number, and bank account details. The form has sections for both the Demat and trading accounts, which can be opened together.

4. Submit KYC documents

Submit the documents required for the Know Your Customer (KYC) process. These include:

- PAN Card

- Aadhaar Card or another valid address proof

- Passport sized photographs

- A canceled cheque for linking your bank account

5. In Person Verification

Once the documents are submitted, an in-person verification (IPV) will be conducted at the DP’s branch or through an agent visiting your address.

6. Sign the Agreement

Sign an agreement with the DP outlining the terms of service and your rights as an account holder.

7. Receive Account Details

After verification, your Demat account is activated, and you will receive your account number and other details by mail or email.

For those who prefer the online processes, opening a Demat Account online is more convenient and quick.

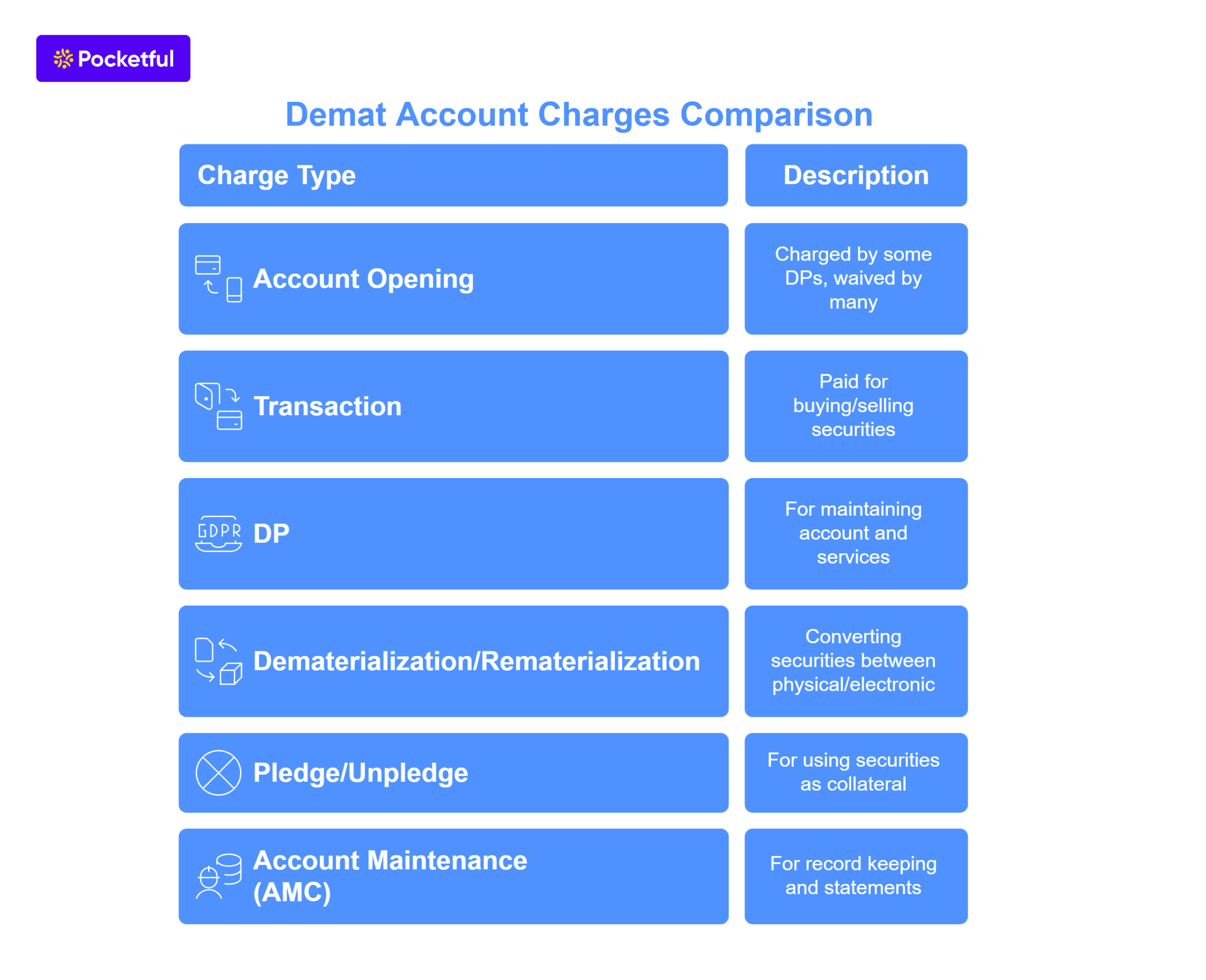

Types of charges associated with Opening a Demat account

Now that you have decided to open a Demat account, understanding the associated charges is crucial. Various fees come with the maintenance and operation of a Demat account. Below is a list of charges you may incur when you create a Demat account:

1. Account Opening Charges

Some Depository Participants (DPs) charge a оne-tіme fee for opening a Demat account. However, many DPs offer a Demat account free of cost. However, it is essential to check with your DP regarding any one-time fees.

2. Annual Maintenance Charges (AMC)

Annual Maintenance Charges (AMC) are recurring fees to be paid by the account holder for maintaining their Demat account. The amount varies depending on the DP. Some may waive the AMC for the first year.

3. Transaction Charges

Whenever you buy or sell the securities, a transaction charge is levied. The DP may charge a fee per transaction or based on transaction volume. These fees accumulate over time based on trading frequency.

4. Dematerialization Charges

If you hold physical shares and wish to convert them to electronic form, then the DP may charge a dematerialization fee.

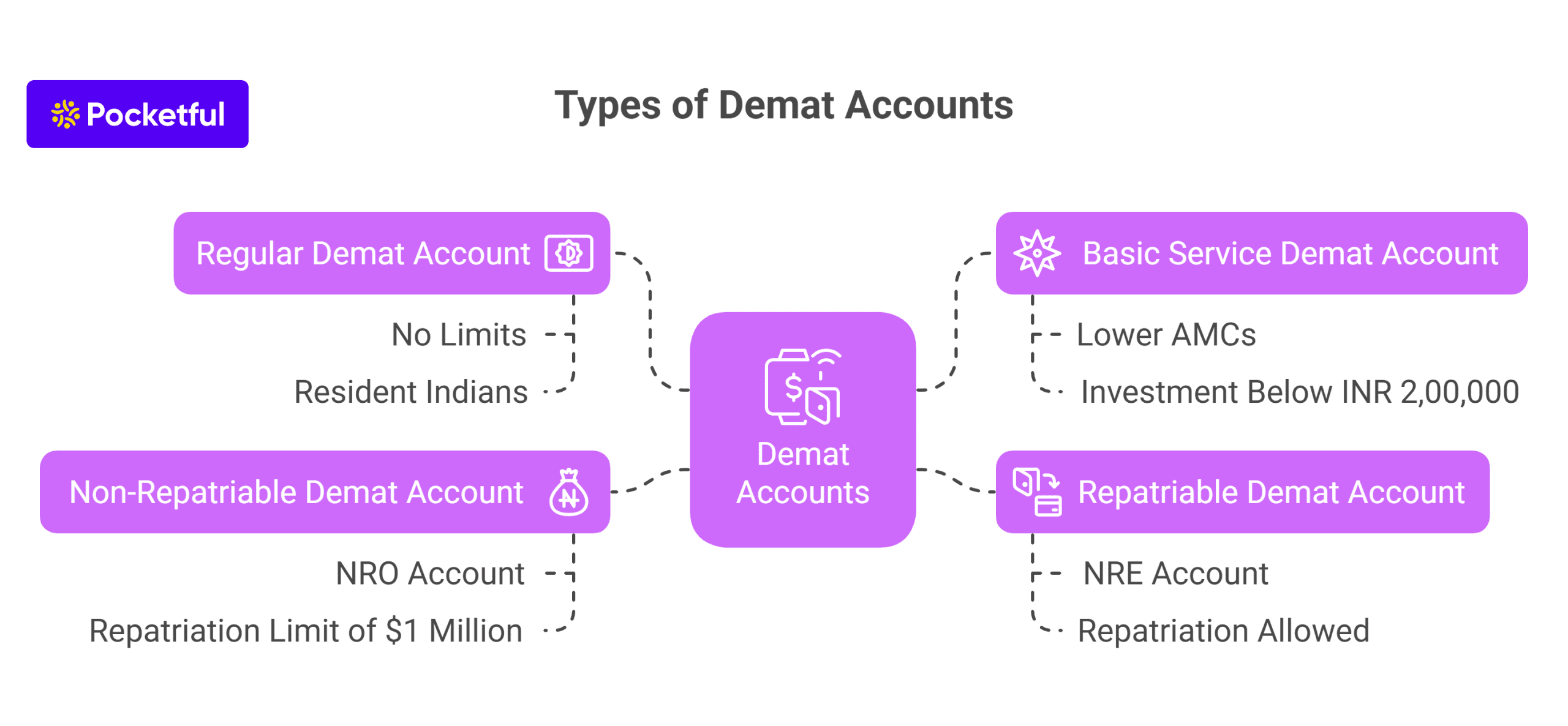

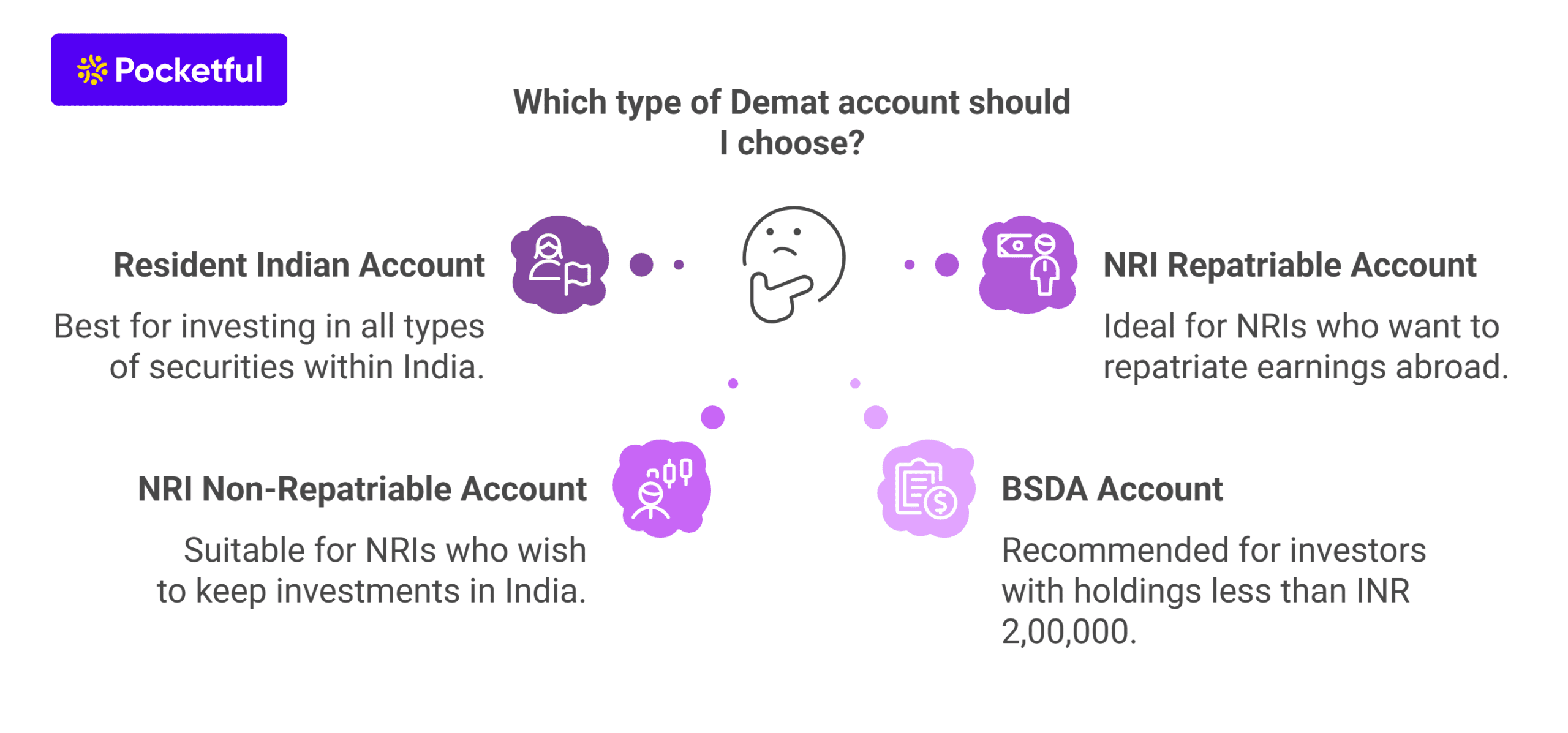

Read Also: Types of Demat Accounts in India

Things to remember while opening a demat account

When considering to open a Demat account, there аre severаl important factors to keep in mind. These considerations will help ensure that you choose the right Depository Participant (DP) and avoid unnecessary complications.

- Choose the Right DP: Before opening a Demat account, research and compare the services offered by different Depository Participants. Look for a DP that offers the transparent pricing and reliable customer service with easy integration with the trading platforms. Most DPs, such as banks or brokerage firms, offer the option to create a Demat account along with a trading account for seamless transactions.

- Understand the Charges: Familiarize yourself with the various charges associated with maintaining a Demat account. These include account opening fees, annual maintenance charges (AMC), transaction fees, and dematerialization charges. Some DPs may waive the certain fees as part of promotional offers, so it is crucial to compare the costs before opening a Demat account.

- KYC Compliance: Ensure you have the necessary documents ready for KYC verification. This includes PAN, Aadhaar, bank details, etc. Accurate and complete information is a must for successful verification.

By remembering these points, you can confidently navigate how to open a Demat account and start your trading journey smoothly.

Conclusion

In conclusion, opening a Demat account, whether online or offline, requires careful consideration of various factors such as choosing the right Depository Participant (DP) and understanding the associated charges and ensuring the KYC compliance. Linking the correct bank account and opting for DPs with additional services can enhance your trading experience.

Frequently Asked Questions (FAQs)

What is a Demat account?

A Demat account holds your financial securities like stocks, bonds, and mutual funds in the digital form, eliminating the need for physical certificates.

How to open a Demat account online?

To open a Demat account online, choose a Depository Participant (DP), fill out the online application form, upload the necessary documents (PAN and Aadhaar), complete the e-KYC verification and sign the agreement digitally. Once verified, your account will be activated in one or two business days.

What documents are required to open a Demat account online?

To open a Demat account, you will need a PAN card, an Aadhaar card, a bank account statement, a cancelled cheque and a passport-sized photograph.

How long does it take to open a Demat account online?

The online process for opening a Demat account is usually quick and takes anywhere from a few hours to 1-2 business days, depending on the DP.

Can I open a Demat and trading account together online?

Yes, most DPs offer the option to open both Demat and trading accounts simultaneously online. This allows you to store and trade securities efficiently through a single integrated platform.