A Demat account is essential for holding shares and other securities in electronic format and eliminates the need for physical share certificates. To buy shares through a Demat account, you first need to open the account with a depository participant, usually a bank or financial institution. Once set up, you can link your Demat account with a trading account to trade in stocks, mutual funds, and other securities directly from your smartphone or computer.

In this blog, we will explain the steps involved in purchasing the shares through a Demat account, the eligibility and documents required, and the benefits of a Demat account.

What is a Demat account?

A Demat account, short for a Dematerialized account, is a digital account that allows investors to hold and manage their securities, such as shares and bonds, in an electronic format. After opening a Demat account, you can easily buy and sell the shares online without the hassle of physical certificates. This modern approach helps simplify the investment process, making it more convenient for both new and experienced investors.

To invest using a Demat account, you need to link it with a trading account, which enables you to execute buy and sell orders. Once your accounts are set up, you can begin purchasing the shares online. If you are wondering where to buy shares online in India, many brokers provide user-friendly interfaces for trading.

To buy a share, you simply log into your trading account, search for the desired stock, and place a buy order. The shares are credited to your Demat account after “T+1” days, where “T” is the transaction date. Learning how to buy shares online opens up a world of investment opportunities and allows you to grow your wealth efficiently. Whether you are just starting or looking to diversify your portfolio, a Demat account is an essential tool in the modern financial markets.

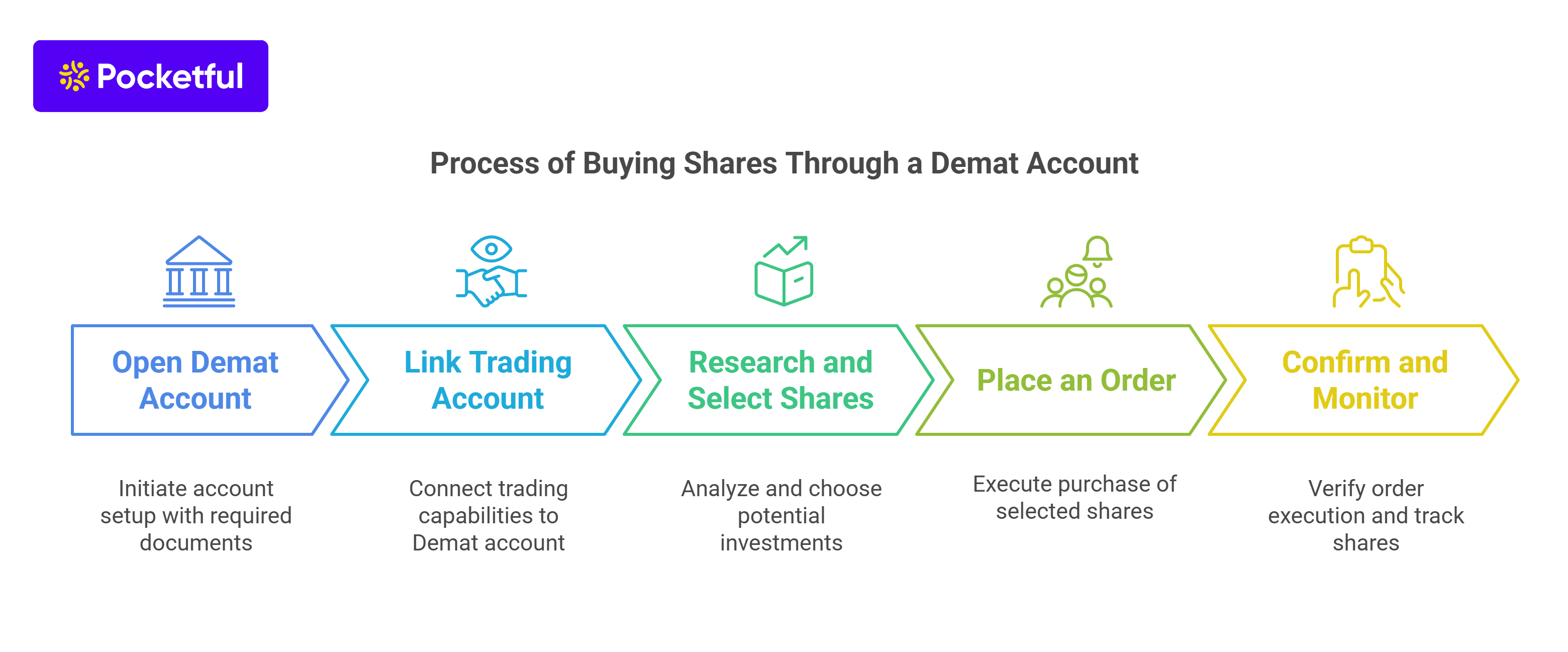

How to Buy Shares Through a Demat Account?

Buying shares through a Demat account is a straightforward process, making the investment process simple and more efficient. Here are the essential steps you need to follow:

Open a Demat Account: The first step is to open a Demat account with a depository participant such as a bank or brokerage firm. You will need to provide identity verification documents and fill out the required forms. After successful verification, DP opens a Demat account for you.

Link a Trading Account: After opening your Demat account, you should link it with a trading account, allowing you to seamlessly buy and sell shares online. However, many DPs open a Demat and a trading account simultaneously.

Research and select Shares: Before investing, conduct a thorough financial analysis of various companies and identify the shares you wish to purchase. There are numerous resources available online to help you analyze potential investments.

Place an Order: Once your accounts are set up and funded, log in to your trading account to buy a share. Search for the stock using its ticker symbol, select the quantity and place an order (market or limit).

Confirm and Monitor: Confirm whether the order is executed. Once executed, the shares will be credited to your Demat account, where you can track your investments.

Best Strategies to Buy Shares

Investing in shares requires a strategic approach to maximize returns and minimize risks. Here are some of the best strategies to buy shares effectively:

Conduct Thorough Research: Analyze a company’s financial health, market position, and growth potential. Understanding the fundamentals will guide you in making informed investment decisions.

Use a Trading Plan: Develop a systematic trading plan that outlines your buying and selling criteria. This plan will help you stay disciplined and avoid emotional trading.

Monitor Market Trends: Keep an eye on market trends and economic indicators. Understanding the market sentiment will assist you in timing your investments effectively.

Start Small: If you’re new to investing, consider starting with smaller amounts. This helps you to learn how to buy shares online without exposing yourself to significant losses.

Utilize Technical Analysis: Familiarize yourself with technical analysis tools to identify buying opportunities. These tools can help you determine the best entry and exit points for your investments.

Eligibility and Documents required to open a Demat Account

To open a Demat account, certain eligibility criteria and documents are required. Understanding these prerequisites is essential for a hassle-free demat account opening process.

Identity Proof: Government-issued ID such as an Aadhar card, passport, or voter ID.

Address Proof: Utility bills, rental agreements, etc., that confirm your residential address.

PAN Card: A Permanent Account Number (PAN) is mandatory for tax purposes.

Photographs: Recent passport-sized photographs may be required.

Bank Details: A canceled cheque or bank statement for linking your bank account.

Once you gather these documents, you can approach a depository participant (DP) to complete the application process. Understanding these requirements ensures you are well-prepared to start your investment journey.

Open a Free Demat Account with Pocketful to Buy Shares Seamlessly

Opening a Demat account with Pocketful is free of cost and is an excellent way to manage your investments. Pocketful provides a user-friendly platform that simplifies the entire investment process for both beginners and investors.

To get started, simply download the Pocketful mobile application or visit their website. The account opening process is quick and straightforward. You will need to provide basic details, such as your identity proof, address proof, and a PAN card. Once your documents are verified, you can open your Demat account at no cost.

With your Demat account and trading account set up, you can easily buy shares online. Pocketful offers a comprehensive list of features and enables you to explore various investment opportunities. The platform’s intuitive interface allows you to track market trends, execute trades effortlessly, and manage your portfolio efficiently. Moreover, Pocketful ensures secure transactions, giving you peace of mind as an investor.

Benefits of a Demat Account

A Demat account offers several benefits mentioned below:

Convenience: A Demat account eliminates the need for physical share certificates and makes it easier to buy, sell, and manage securities electronically. This digital approach streamlines the entire trading process.

Reduced Risk of Loss: Physical share certificates can be lost, stolen or damaged. With a Demat account, your shares are stored securely in an electronic format, reducing the risk of loss.

Quick Settlement: Settlement of transactions is quicker through a Demat account than traditional methods.

Stores Multiple Securities Types: A Demat account allows you to hold the various securities including stocks, bonds, mutual funds, and exchange-traded funds (ETFs), all in one place which simplifies portfolio management.

Easier Record Keeping: Your Demat account provides a clear and comprehensive record of all your transactions and holdings, making it easier to track your investments and manage your portfolio effectively.

Automatic Updates: Corporate actions such as dividends, bonus shares, and stock splits are automatically reflected in your demat account.

Conclusion

Buying or selling shares with the help of a trading account linked with a Demat account significantly enhances security and efficiency as compared to traditional methods. With the elimination of physical share certificates, investors can buy and sell securities quickly and securely. Moreover, a Demat account can store different types of securities and automatically adjust holdings for any corporate actions.

Frequently Asked Questions (FAQs)

What is a Demat account, and why do I need one to buy shares?

A Demat account is a digital account that holds your securities in electronic form. Investors can buy shares through a trading account but need a Demat account to store them.

How do I open a Demat account?

To open a Demat account, choose a depository participant (DP), such as a bank or brokerage firm. Fill out the demat account opening form and provide the required documents like identity proof, address proof, PAN card, etc. Once verified, your account will be activated.

How do I buy shares through my Demat account?

Investors can buy shares by opening a Demat account and linking it to a trading account. To buy shares, log in to your trading platform, search for the desired stock, and place an order. The shares will be credited to your Demat account upon successful transaction.

Are there any fees associated with a Demat account?

While opening a Demat account is usually free, there may be annual maintenance charges associated with it. Additionally, brokerage fees apply when buying the shares. It is advisable to review the fee structure of your chosen DP.

Can I sell shares directly from my Demat account?

Yes, you can sell shares directly from your Demat account by using your linked trading account. After logging in to your trading account, you can place a sell order for the shares you wish to sell, and the proceeds will be credited to your trading account after the transaction is completed.

A Permanent Account Number (PAN) is a crucial document for opening a Demat account in India. However, for individuals without a PAN card, there are alternative ways to open a Demat account, as there are some exemptions. Want to know if you fit the criteria? Read on.

This blog provides a comprehensive look at who can open a Demat account without a PAN card and its benefits. Moreover, we will discuss the process and documents required to open a Demat account.

What is a Demat Account?

A Demat account stands for “Dematerialized account”. It is an electronic storage account used to hold financial securities like stocks, bonds, and exchange-traded funds (ETFs). By digitizing securities, a Demat account eliminates the need for physical certificates, streamlining and securing the trading and investment process.

Opening a Demat account requires essential documents, particularly a PAN (Permanent Account Number) card, which helps investors during tax filing and track transactions. However, for individuals looking to invest or trade who do not possess a PAN card but are eligible for an exemption, it is possible to open a Demat account without a PAN card. The exemptions are discussed later in the blog.

Documents Required for Opening a Demat Account

To open a Demat account, certain essential documents are generally required to verify identity, address, and bank details. These documents ensure compliance with financial regulations. Key documentation includes:

Identity Proof: Commonly accepted identity proofs are the Permanent Account Number (PAN) card, Aadhaar card, passport, or Voter ID. A PAN card is a mandatory document for opening a Demat account as it is used for tax filing purposes and tracking transactions.

Address Proof: Documents like the Aadhaar card, passport, and driving license or utility bills (e.g. and electricity or telephone bill) are commonly accepted for verifying your address.

Bank Details: Providing a canceled cheque or a bank statement with your name, account number, and IFSC code is crucial. This is needed to link your Demat account to your bank.

Income Proof (Optional): Income proof is required for trading in the futures and options segment. A recent salary slip, ITR or six-month bank statement may be needed.

Opening An Online Demat Account

Opening an online Demat account is a quick and convenient process that allows you to manage and store your securities digitally. A Demat account or dematerialized account will securely hold assets like stocks, bonds, and ETFs, also eliminating the need for physical certificates. To open a Demat account online, start by choosing a reliable brokerage or financial institution that offers superior services and user friendly platforms.

The process typically begins by completing an online application form, where you must provide personal details such as your name, address, etc. Uploading essential documents like PAN card, Aadhaar card, bank statement and recent passport-sized photographs is part of the verification process. Some brokers may also require a digital copy of your signature. Upon submission, these documents undergo a Know Your Customer (KYC) verification, which is often completed within a day or couple of days. Once the DP verifies and approves your application, you receive your Demat account details and can begin trading through the broker’s application or website.

Is a PAN Card A Must For A Demat Account?

According to the Securities and Exchange Board of India (SEBI), a PAN card is a mandatory requirement for engaging in securities transactions in India, which makes it essential to open a Demat account. It serves as an identification proof and helps investors and authorities keep track of transactions occurring in a Demat account. Moreover, the PAN card helps regulators track transactions and prevent tax evasion.

However, if you are still wondering “Can I open a Demat account without a PAN card?”, the answer is yes. Investors can open a Demat account without a PAN card, but the applicant must fulfill certain criteria to take advantage of this exemption. Let’s look at the exemptions specified by the SEBI.

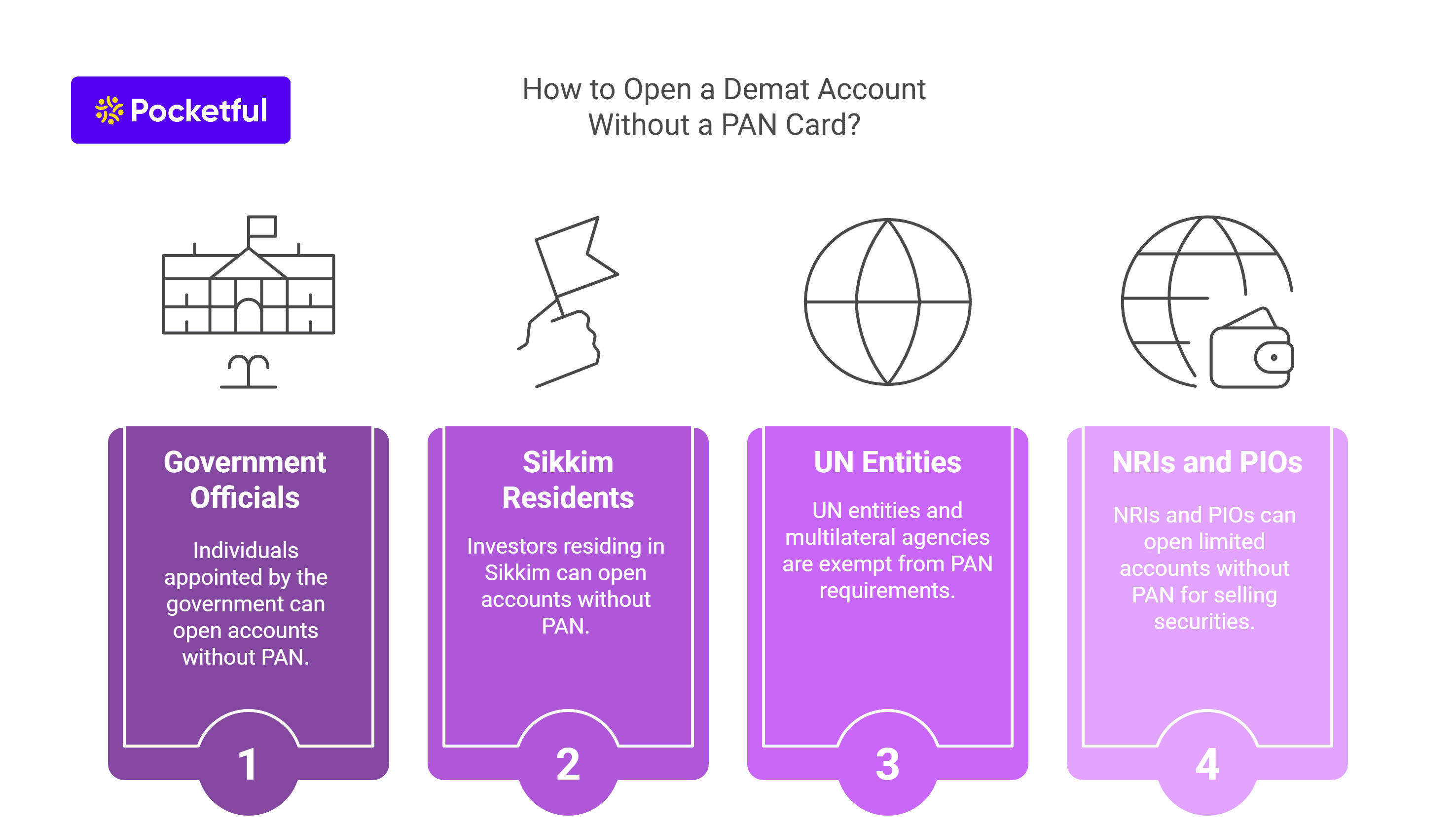

How to Open a Demat Account Without a PAN Card?

According to SEBI regulations, some individuals and entities can open Demat accounts without a PAN card. The exemptions are listed below:

Officials appointed by Government: A PAN card is not required for transactions conducted by individuals appointed by the Central Government or State Governments. These individuals can be official liquidators, court receivers, etc.

Investors in Sikkim: Investors residing in Sikkim can open a Demat account without a PAN card. DPs must verify the proof of address thoroughly to confirm that the investor is a resident of Sikkim.

UN entities & Multilateral Agencies: These entities are not required to furnish a PAN card to open a Demat account if they are exempt from paying taxes or filing tax returns.

NRIs or PIOs: Non-resident Indians (NRIs) or Persons of Indian Origin (PIO) are allowed to open a “limited purpose BO account” without a PAN card to sell any securities they currently own in the form of physical form. These accounts are suspended for credit from IPOs, off-market transactions or secondary market transactions. However, the investor continues to receive benefits arising out of corporate actions. Such accounts are valid for a period of 6 months, after which the investor must provide a PAN card to convert the limited-purpose BO account into a normal BO account.

Benefits of Having a PAN Card

A PAN (Permanent Account Number) card is an important financial document in India as it offers a range of benefits. Some of the benefits are listed below:

Simplified Tax Filing: A PAN card serves as a unique identifier for all financial transactions and simplifies the process of filing income tax returns. It helps the government track taxable activities, reduce fraud, and maintain transparency in the financial system.

Avoid Tax Deduction at higher rates: While making payments to NRIs or Indian residents, it is essential for the recipient to furnish their PAN card. If the recipient does not have a PAN card, then the sender must deduct TDS at a higher rate of 20% according to Section 206AA of the Income Tax Act.

Easy Loan Approvals: A PAN card makes it easier to get a loan as it provides a reliable financial history.

Demat Account: A PAN card is mandatory to open a Demat account, which helps investors manage investments easily.

Identity Proof: The PAN card is also widely accepted as proof of identity.

Conclusion

A PAN card is essential for opening a Demat account in India. However, SEBI has specified certain exemptions under which some individuals or entities are not required to provide a PAN card to open a Demat account.

A PAN card tracks an individual’s financial history, helps enhance an individual’s credibility in financial institutions, and simplifies processes like loan applications and credit card approvals. Moreover, the PAN card serves as an ID across various domains. Overall, possessing a PAN card is invaluable for investors to track their transactions and simplify the tax filing process.

Frequently Asked Questions (FAQs)

Can I open a Demat account without a PAN card?

Investors can open a Demat account without a PAN card if they fulfill the criteria listed by the SEBI.

Which documents can be used as identity proof for opening a Demat account?

Identity proof documents include an Aadhaar card, Voter ID, passport, or driver’s license.

Which individuals and entities are not required to provide a PAN card to open a Demat account?

Individuals residing in Sikkim, UN agencies, multilateral agencies, officials appointed by the government, NRIs, and PIOs are not required to provide a PAN card when opening a Demat account.

What is a limited-purpose BO account?

A limited-purpose BO account is a type of Demat account that can be opened without a PAN card and remains active for a period of 6 months. NRIs and PIOs use this account to sell any securities held in the physical form. The account is restricted from receiving credits and requires investors to furnish a PAN card after 6 months to convert it into a regular demat account.

India’s financial market has witnessed a bull run in the past few years, which is why many NRIs are trying to invest in the Indian stock market. An NRI needs a Demat account and a trading account to participate in the Indian stock market. Opening an NRI (Non Resident Indian) trading and Demat account is a straightforward process that helps the NRIs to invest in the Indian stock market. Whether you are looking to trade in equities, mutual funds, or bonds, having the right demat account is essential.

In this blog, we will talk about the steps to open the NRI trading and Demat account and also explain the documents you will need, and clarify the different types of accounts available including the NRE and NRO accounts.

Who is an NRI?

A Non-Resident Indian (NRI) is an Indian citizen who resides outside India for various reasons such as employment, business, or education and does not stay in India for more than 182 days in a financial year. NRIs are allowed to invest in Indian financial markets which is facilitated through NRI Demat and Trading account. The NRI Demat account holds shares and securities in electronic form and makes it easier to manage investments from abroad.

For NRIs, there are different types of accounts, including the NRE Demat account and NRO Demat account, which are used to store securities, and the NRI trading account that allows trading in securities in India. Understanding the features of these accounts is essential for NRIs looking to participate in the Indian stock market and maximize investment opportunities effectively.

What is an NRI Demat Account?

An NRI Demat account is a specialized account that allows the Non-Resident Indians (NRIs) to hold and manage their securities in electronic form. It is essential for NRIs who want to invest in the Indian stock market as it will simplify the process of buying, selling, and transferring shares. There are two main types of Demat accounts for NRIs:

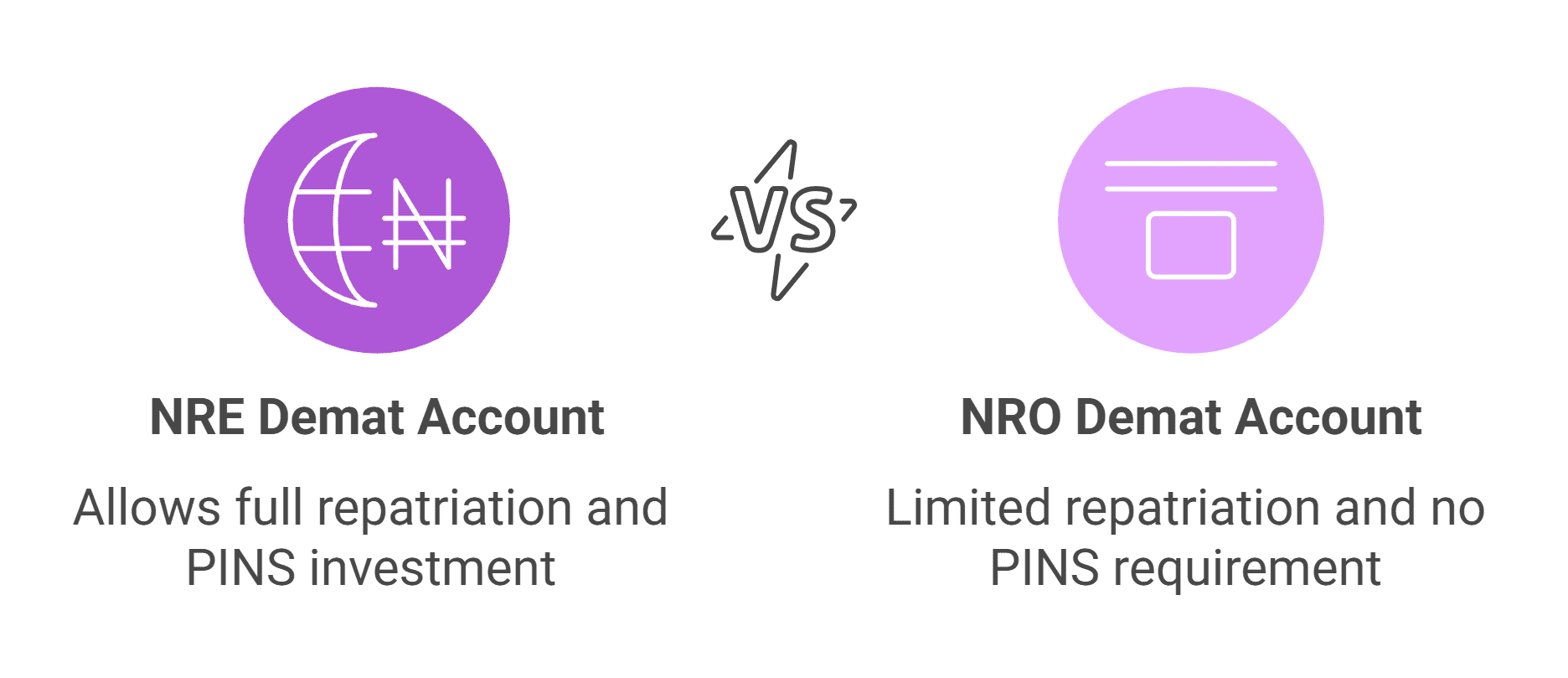

NRE Demat account: NRE or Non-Residential External Demat account allows NRIs to invest in Indian financial markets such as stocks, bonds, etc. Investors use this account to take advantage of the Portfolio Investment NRI scheme (PINS). The NRE demat account is linked with the NRE bank account. The advantage of using an NRE demat account is that both investments and profits earned on them can be repatriated to the NRI’s bank account in their country of residence.

NRO Demat account: NRO or Non-Resident Ordinary Demat account also allows NRIs to invest in Indian securities. It is different from an NRE demat account as it doesn’t require NRIs to invest through the PINS route, and the NRIs can repatriate only up to $1 million of investment to their country of residence.

Can an NRI open a Demat Account in India?

Yes, a Non-Resident Indian (NRI) can open a Demat account in India as it enables them to invest in the Indian stock market. NRIs have the option to choose between an NRE Demat account and an NRO Demat account depending on your investment goals. An NRE Demat account is suitable for those who have a majority of earning sources abroad and want the advantage of repatriating funds freely. On the other hand, if an NRI has income sources in India and wants to claim exemptions on the interest earned, then a NRO demat account is more suitable.

What is the NRI Demat Account Opening Process?

The NRI Demat account opening process involves several key steps to ensure NRIs can effectively invest in the Indian stock market.

Applicants need to select a reputable Depository Participant (DP) that offers NRI demat account services. They can choose between an NRE Demat account or an NRO Demat account based on their income sources.

Get the NRI account opening form from DP’s website or nearest branch.

Mention all the relevant details and attach all the required documents, such as proof of identity and proof of address. Documents required include a copy of passport, proof of overseas address, copy of PAN card, etc. Communicate with the DP to get a complete list of the documents required.

Sign the agreement with the DP. The agreement lists the responsibilities of both the investor and DP.

DP verifies the information, and upon successful verification, an NRI Demat account is opened, and the DP sends the credentials to your registered email ID.

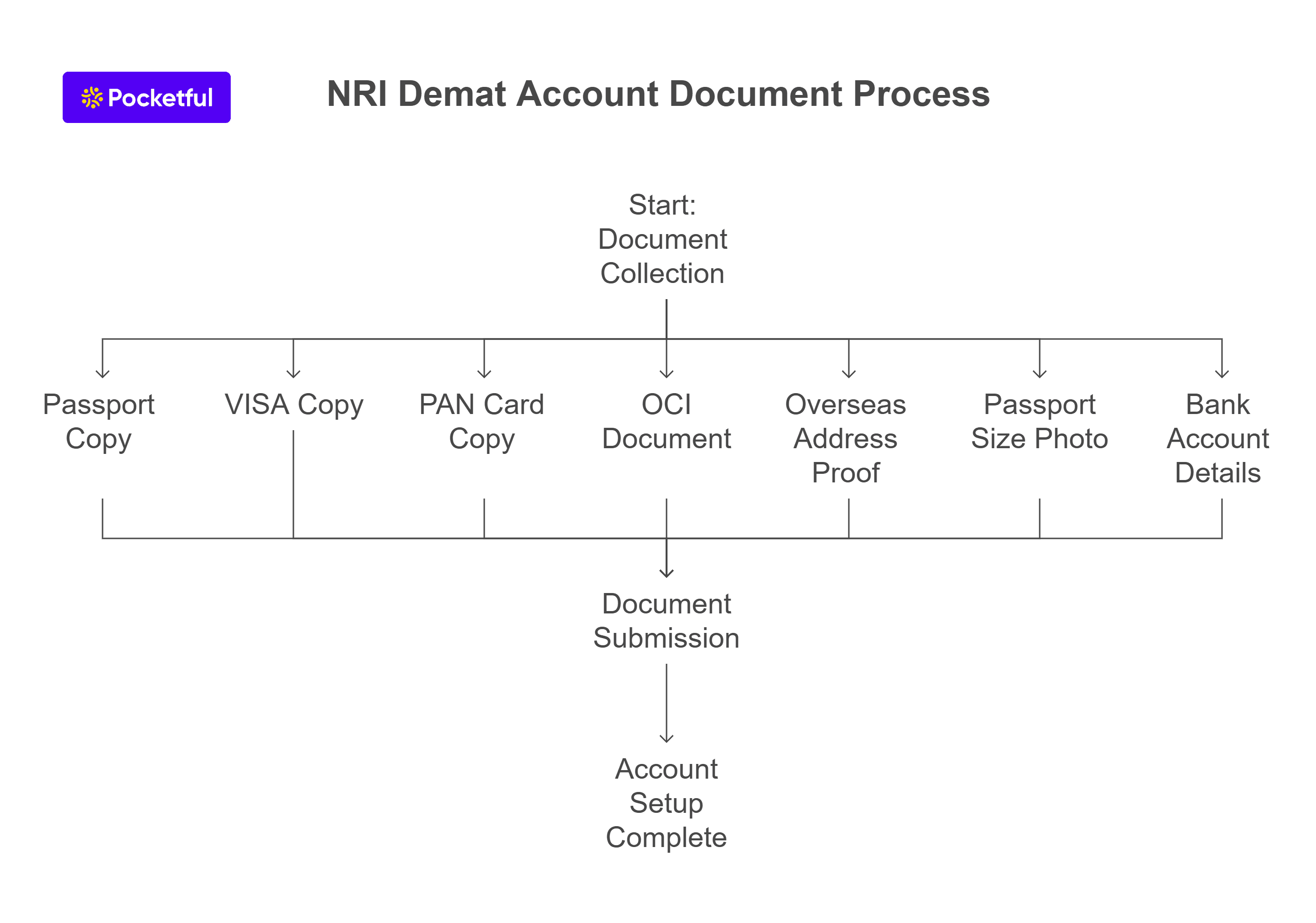

Documents Required for NRI Demat Accounts

Specific documents are required to comply with regulatory norms and ensure a smooth account opening process. The documents required for a NRI demat account are:

Copy of passport as proof of identity

Copy of valid VISA

Copy of PAN card

OCI (Overseas Citizenship of India)

Overseas Address Proof

Passport size photograph

Bank Account Details

These documents ensure that the NRI trading account in India is set up correctly and facilitating efficient trading and investment management while adhering to legal requirements. Proper documentation helps streamline the process of opening a Demat account for NRIs.

NRI Demat Accounts: The Benefits

NRI Demat accounts offer several benefits that empower Non Resident Indians (NRIs) to invest in the Indian stock market.

NRI demat account allows NRIs to hold securities in electronic form and simplifies the management of investments. With an NRI Demat account, transactions are quicker and more efficient, and the need for physical paperwork is eliminated.

NRE demat account offers the investors the option to repatriate funds.

NRO Demat account allows NRIs to manage the income generated in India while complying with tax regulations.

Conclusion

In conclusion, Demat accounts for NRI serve as essential tools for Non-Resident Indians looking to invest in the Indian stock market. With benefits like electronic storage of securities, seamless transactions, and compliance with tax regulations, these accounts simplify the investment process. However, investors must choose between the NRE and NRO demat accounts based on their investment goals and sources of income.

Frequently Asked Questions (FAQs)

What documents are required to open an NRI trading and Demat account?

To open an NRI trading and Demat account, you need to provide a copy of your valid passport, VISA, PAN card, OCI, proof of overseas address and a recent passport sized photograph.

Can I open both NRE Demat and NRO Demat accounts?

Yes, you can open both NRE and NRO accounts simultaneously.

Is it mandatory to have an NRI trading account to open a Demat account?

Yes, it is mandatory to have an NRI trading account linked to your Demat account. This trading account enables you to execute buy and sell transactions in the Indian stock market.

How long does it take to open an NRI trading and Demat account?

An NRI trading and demat account can be opened within a couple of days.

Can I manage my NRI trading and Demat account online?

Yes, most financial institutions, and brokerages offer online platforms for managing your NRI trading and demat accounts. You can access real-time market data, execute trades, and monitor your portfolio conveniently from anywhere in the world.

A Demat account is an absolute must-have for holding shares and securities traded in the financial markets. Research shows that in 2024, there were 46 million more demat accounts.

In addition to this, people are now opting for a joint demat account. This allows multiple individuals to jointly hold and manage investments stored in a single demat account.

You can open a Demat account online. This reduces the ownership structure’s complexity and opens up more possibilities for families, business partners, or spouses wanting to pool together their investments.

What is a Joint Demat Account?

A joint demat account can be defined as an account that allows two or more individuals to jointly hold and manage securities. A joint bank account functions similarly by giving the account ownership of shares to several holders.

A joint Demat account can have up to three account holders. This includes one primary and two joint holders. The primary account holder is responsible for the account. Although the primary account holder is responsible for the account, all demat account joint holders have equal rights in managing the investments.

Prominent Features and Benefits of a Joint Demat Account

Some of the most common features and benefits of a joint demat account include:

1. Pooling Resources

Joint account holders can pool their funds and make shared investments with a joint demat account. This helps increase the overall investment amount, allowing joint holders to invest more effectively.

2. Reduced Maintenance Fees

A joint demat account allows everyone to split the maintenance costs. This reduces overall fees. This makes it an economical choice for those looking to manage investments together. Sharing these expenditures is much cheaper than keeping separate accounts for each member.

3. Smooth Estate Transfer

If one of the demat account joint holders dies, the surviving holder(s) will immediately take over the account. This simplifies and expedites the process of transferring assets. It eliminates the need for complex legal formalities.

Who Can Open a Joint Demat Account?

Joint demat accounts can be opened for anyone fulfilling depository participant (DP) criteria. Joint demat accounts can be opened by the following individuals:

Residents of India above 18 years of age.

NRIs that comply with applicable regulations.

The holders can be unrelated to each other: business partners, friends, family members, etc., can co-own a joint demat account. However, all holders must conform to KYC norms.

Documents Required for Opening a Joint Demat Account

When you open joint demat account online, it requires the following documents:

PAN Card: A copy of the PAN card for each account holder.

Photographs: Recent passport-size photos of all account holders.

Proof of Identity: Documents like an Aadhaar card, Voter ID, passport, or driver’s license.

Proof of Address: Documents such as an Aadhaar card, utility bill, or passport to verify the address.

Bank Account Proof: A cancelled cheque or a recent bank statement of the primary account holder.

Income Proof: A salary slip, bank statement, or income tax return acknowledgement.

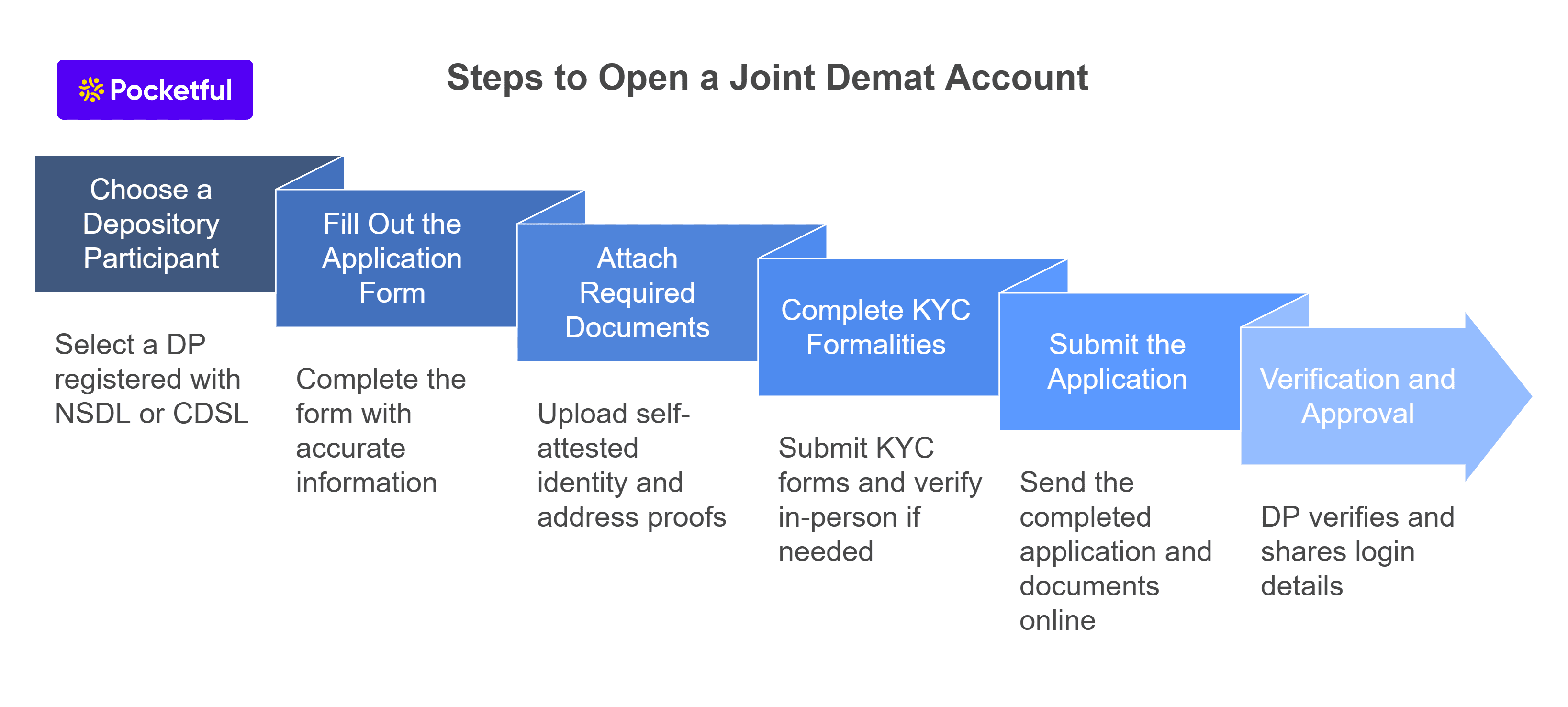

Select a Depository Participant (DP) that is registered with the NSDL or CDSL.

2. Fill Out the Application Form

You can get the joint demat account opening form from the DP’s website. All account holders are required to disclose their information. Verify the accuracy of all the information.

3. Attach Required Documents

Upload scanned copies of the identity proofs, address proofs, bank proofs, and photographs of all the holders. These should all be self-attested by the holders concerned.

4. Complete KYC Formalities

All holders should submit KYC forms and complete in-person verification if needed.

5. Submit the Application

Submit the application and the documents in their complete form on the DP’s website.

6. Verification and Approval

After verifying the details submitted, the DP shares the login details and authorizes it.

Points to Consider Before Opening a Joint Demat Account

Here are the key joint demat account rules to consider before opening an account:

1. Approval of All Account Holders

Transactions in a joint demat account require approval from each account holder. The transaction is invalid if full consent is not obtained. This guarantees that everyone is aware of the activities occurring within the account.

2. No Changes to Account Holder Details

Once the joint demat account is opened, you cannot change details such as names or birth dates. If there is an error, you will have to create a new account. To avoid future account issues, make sure to double-check all information before applying.

3. Tax Responsibility

In a joint demat account, the primary account holder is liable for paying capital gains taxes. Despite the fact that there are several account holders, the principal holder is responsible for paying taxes.

4. One Trading Account Only

Only one trading account is connected to the joint demat account. This is usually held by the principal account holder. This main holder is the recipient of all messages pertaining to the account. This implies that they are in charge of overseeing the account. They also get information about all the activities occurring within the account.

5. Account Changes after Opening

You cannot convert an individual Demat account into a joint one. To open a joint account, you must apply from the start.

By now, you must have understood how to open joint demat account. Understanding the principles and techniques can help you maximize your money. It’s an excellent choice for anyone wishing to invest jointly.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Can I add or remove joint holders after opening a joint Demat account?

No, once a joint Demat account is opened, you cannot add or remove joint holders. If any changes are required, you will have to close the existing account and open a new one.

Is it possible to convert an individual Demat account into a joint Demat account?

No, an individual Demat account cannot be converted into a joint Demat account. You must apply separately for a joint account from the beginning.

Who is responsible for taxation in a joint Demat account?

The primary account holder is responsible for paying capital gains tax, even though the account has multiple holders. Tax liabilities are calculated based on the transactions made in the account.

Can all joint account holders access the trading account linked to the joint Demat account?

No, only the primary account holder has access to the trading account linked to the joint Demat account. The principal holder also receives all transaction-related notifications.

What happens to a joint Demat account if one of the account holders passes away?

In case of the demise of one of the joint holders, the surviving holder(s) continue to manage the account. The account is seamlessly transferred without complex legal formalities.

A Demat account is necessary to participate in the stock market in India. Although many brokers in the market offer Demat account services, you should select one based on your needs.

In this blog, we will give you an overview of the best Demat account in India for 2026, along with the top three recommendations for traders and investors.

What is a Demat Account?

An investor can keep financial assets, including stocks, mutual funds, ETFs, bonds, and more, in an electronic demat account. Before 1996, securities were exchanged in physical certificates, which had several dangers, including damage from forgeries and theft. Demat accounts were created to remove these risks. If you wish to trade on the Indian Stock Market, you must have a Demat Account.

What to Look for in a Demat Account App?

The key considerations for selecting the best Demat Account:-

Brokerage – Brokers typically charge a commission as a fee for using their platform to execute trades. You should choose the broker for opening a Demat account that offers you the lowest brokerage.

Account Maintenance Fees – Customers are charged fees for maintaining their Demat accounts by the broker. Since these yearly maintenance charges differ from broker to broker, it is essential to consider brokers who offer lower annual maintenance fees.

Account Opening Fees – A one-time fee is charged by some brokers while opening a demat account with them. However, the majority of brokers are offering zero account opening fees.

Margin Interest – Brokers lend money to their clients and charge interest on it at a certain rate; therefore, if you wish to opt for a margin trading facility, then you must consider the broker who charges a minimum interest rate on this facility.

Research Tools – There are various types of research tools offered by brokers; therefore, one must choose a broker who offers the most advanced trading tools.

Customer Support – One of the most important things to consider when opening a Dement account is customer service. Customer service is crucial because you want any issue you encounter when managing a Demat account to be fixed as soon as possible.

Overview of the Top 10+ Demat Accounts Apps for Traders and Investors

An overview of 10 + Best Demat Accounts for traders and investors is given below:-

1. Pocketful – Free Demat Account App

Pocketful is a new-age discount broking firm offering a wide range of investment options such as equity, commodity, derivatives, etc. Pocketful was launched in 2024 and is backed by Pace Financial Group. Pocketful is developed by professionals with more than 30 years of experience, which ensures enhanced user experience. Pocketful is different from other discount brokers as it offers one of the best trading platforms and does not charge any fees for equity delivery-based trades, account opening, or yearly maintenance fees. Therefore, it is the best option for both traders and investors.

Key Features

Pocketful provides a free trading platform since there is no brokerage on equity delivery trades, zero account opening fees and zero annual maintenance fees for the first year. These benefits make it a strong contender for users searching for the best demat account in India.

An online account can be opened with Pocketful within five minutes.

Pocketful offers many advanced features for investors, including Curated Pockets, Superstar Investor portfolios, stock-specific news, and in-depth technical and fundamental analysis—helping investors research better, track opportunities, and make more informed investment decisions.

For traders, Pocketful offers advanced TradingView charts, an advanced option chain, Scalper Mode, basket orders, and several other professional tools to analyze markets efficiently—making it a strong choice for opening a Demat account.

Pocketful offers MTF interest rates starting at 5.99%, which are among the lowest available in the market, helping traders reduce funding costs while maintaining flexibility.

You can create your trading strategies using free Pocketful APIs.

Best For: Because of its user-friendly design, zero brokerage on equity delivery transactions, and no annual maintenance fees for the first year, Pocketful is the best broker for traders and investors. Additionally, it offers advanced trading tools to analyze the market. Therefore, one can consider opening a Demat account with Pocketful.

2. Zerodha

Zerodha is one of the major players in the Indian stock broking industry. It was established in 2010 by the Kamath Brothers and offers a distinctive trading platform focusing on cutting-edge technology. It introduced a new pricing structure in the broking industry, which was known as flat brokerage for trading. Many traders searching for the best demat account in India consider Zerodha due to its transparent pricing and tech-driven ecosystem.

Key Features

Zerodha is renowned for its user-friendly trading platform.

It has a dedicated customer service team that assists its clients in resolving their queries.

Varsity is a free education platform offered by Zerodha to enhance the knowledge of their client.

Best For: Investors who want to trade in the stock market with the broker that offers the lowest brokerage can opt for this platform.

3. Angel One

Angel One is one of India’s top full-service brokers. It was established in 1996. It offers trading and investing in a variety of assets such as equity, commodity, derivatives, etc., and investment advisory services. Their cutting-edge software platform prioritizes customer requirements, making it a strong choice for individuals evaluating the best demat account in India.

Key Features

The main advantage of opening a demat account with Angel One is their customer-focused approach.

Advanced trading tools are available in Angel One’s application.

The company has a strong offline presence across the nation.

Best For: Angel One is suitable for traders who prefer offline broking services.

4. ICICI Direct Securities

One of the top stockbrokers in India is ICICI Direct Securities. One of the biggest banks in India’s private sector, ICICI Bank, owns ICICI Direct as a subsidiary. It offers a three-in-one account, which combines savings, trading and a Demat account through which an investor can effortlessly move funds from their savings account to their trading account. They offer a large variety of investment products that are tailored to meet the customers’ requirements.

Key Features

Through its local offices, the company maintains a strong national presence, assisting its investors with any questions they may have.

ICICI Direct also provides its clients with consultancy and research services.

Additionally, it provides its investors with individual or customized wealth management solutions.

Best For: ICICI Direct Securities is a good option for investors who need assistance from local branch offices.

5. Kotak Securities Limited

Kotak Securities is a division of Kotak Mahindra Bank, one of the largest private sector banks in India. It makes it simple for their customers to link their bank account to their trading and demat accounts. Kotak Securities provides its investors with a variety of investment products, such as equities, commodities, and derivatives. Kotak Securities’ desktop-focused Neo Web and the mobile application Kotak Neo both provide real-time market data to traders and investors.

Key Features

Apart from trading in equity and commodities, it also offers a wide range of investment options, such as mutual funds.

Kotak Securities educates investors through various educational initiatives.

Because Kotak Bank supports the company, it enjoys a great reputation as a brand.

Best For: Kotak Securities is a good choice for investors who want to enhance their stock market knowledge through their online tutorials.

6. Upstox

Upstox offers a modern trading platform and technical tools that help investors predict the trend of a commodity or a stock price. Additionally, they provide an option chain with a strategy mode that allows you to formulate and carry out your trading plans.

Key Features

The mobile application offered by Upstox makes it simple for a beginner to start trading.

You can create several watchlists on the platform and add equities, commodities, etc., for intraday trading.

There are no annual maintenance charges payable by the investor while keeping an Upstox account.

Best For: Upstox is suitable for traders who wish to utilize technical analysis as a tool for intraday and swing trading.

7. 5Paisa

One of the leading discount brokers in India, 5Paisa offers a variety of services, including commodity and equities trading. It was founded in 2016 with the main goal of providing broking services at low prices. 5Paisa is an AMFI-recognized distributor of mutual funds.

Key Features

They offer user-friendly web-based and mobile-based trading platforms to investors that offer them a seamless trading experience.

5Paisa offers investment in mutual funds through its platform.

Their FnO360 platform offers advanced tools so that investors can make informed decisions.

Best For: 5Paisa is an option for those who want to learn about the stock market through interactive workshops.

8. Sharekhan

Established in 2000, Sharekhan was among the first broking firms in India to provide online trading services to regular clients. By opening franchises around the nation, it expands its business at an exponential rate. It was purchased by the French investment banking company BNP Paribas later in 2016 and was then sold to Mirae Asset Financial Group in 2024.

Key Features

They provide a smooth mobile application with advanced trading tools.

Sharekhan offers an advanced training program for its investors through its online courses, popularly known as the Sharekhan Classroom.

It has a dedicated customer support team that addresses its customers’ queries.

Best For: For people who want to learn about technical and fundamental analysis, Sharekhan is the ideal choice.

9. Motilal Oswal Financial Services Limited

Motilal was founded in 1987 and is regarded as a major participant in the Indian broking industry. It offers advisory services, portfolio management services and investment in various asset classes. With more than 30 years of experience and multiple awards in recent years, they offer research reports in addition to advanced trading tools through their website and their mobile application named RISE.

Key Features

Motilal Oswal Financial Services Limited provides its clients with customized financial solutions.

Their mobile application is one of the best in the industry due to its user-friendly interface.

Loans against securities are also offered by the company.

Best For: Ideal for investors who wish to have access to a variety of specialized financial products in one location, including portfolio management services.

10. SBI Securities

It was incorporated in the year 2006, and initially, it was known as SBICap Securities Limited. It is a wholly-owned subsidiary of the State Bank of India, which is India’s largest public-sector bank. SBI Securities is known for its extensive branch network and trust among investors due to government support for SBI. Along with equity and commodity trading services, it also offers research and advisory services.

Key Features

They have personalized relationship managers for their high-net-worth individual clients.

SBI Securities can increase the purchasing power of existing customers by offering them margin trading facilities for intraday traders.

Best For: This platform is suitable for both new and experienced investors as it offers comprehensive services. However, the fees charged by them are comparatively higher than those of others.

11. Axis Direct

Axis Direct was founded in 2011 and is a division of Axis Securities Limited, which is a subsidiary of Axis Bank. The company used innovative technology and created the Axis Direct platform, which is now among the top trading platforms in the Indian broking industry. The customers of Axis Bank can easily link their bank account to their demat account. The company’s headquarters is situated in Mumbai.

Key Features

It offers advanced trading and investing platforms to its customers.

The Axis Direct provides regular, in-depth fundamental research reports on different stocks, sectors, and commodities.

Margin funding is also an additional feature provided by Axis Direct to their investors.

Best For: Investors looking to use the margin trading facilities provided by the broker can consider Axis Direct as an option.

12. IIFL

In 1985, IIFL was established as a division of the India Infoline Group. Originally founded as an advisory firm, its primary focus was on research and related activities. In 2005, it changed its name to India Infoline and went public on the Indian Stock Exchange. The company offers an advanced trading platform and ensures that its investors make wise investment decisions through its research reports.

Key Features

IIFL offers research and advisory services to its customers.

It also offers a user-friendly trading platform.

Various free educational sessions are also provided by IIFL to their customers to enhance their knowledge.

Best For: Investors may choose to open a demat account with IIFL if they would like research and advisory services in addition to quick trade execution.

13. Edelweiss Broking

The Edelweiss Group chose to expand their business in 2008, and decided to enter into the broking service industry, and established Edelweiss Broking Limited. From 2010 to 2015, the company focused on research and advisory services. Along with this, they offered their clients a cutting-edge investing platform. The company began to diversify its product portfolio and included mutual funds and portfolio management services in 2015.

Key Features

It offers algorithmic trading services to its customers.

They also suggest actively managed funds to their customers based on market conditions.

Daily market updates are also provided by Edelweiss to their investors so that they stay updated about the market conditions.

Best For: Edelweiss broking is suitable for those investors who are looking for a comprehensive array of services, such as advisory, trading etc., in one place.

14. Groww

It was incorporated in 2016 by the four Flipkart employees. Over time, this platform has grown in popularity among beginners in trading because of its easy-to-use interface.

Key Features

It charges minimal fees from its customers.

They provide investment in stocks, ETFs, mutual funds, etc., along with credit and bill payment services.

Best For: It is suitable for investors who wish to have access to all their investments in one place or at a single application.

15. Paytm Money

When Paytm Money was launched in 2017, it started operations as a direct mutual fund investment platform. One97 Communications Limited, the parent firm of Paytm, gained popularity right away among individual investors looking to cut costs when investing in mutual funds. In 2019, the company decided to provide low-cost stock trading services. The company’s headquarters is situated in Bengaluru.

Key Features

Paytm offers a user-friendly application to provide their investors with a hassle-free trading experience.

It also offers access to direct mutual funds through which a customer can save costs.

It offers various calculators, such as SIP, lumpsum, etc., on its platform.

Best For: It is suitable for investors who are looking for platforms that offer trading facilities at a lower cost and fulfill their investment needs.

The 3 recommended brokers for the traders are as follows:-

Zerodha: Due to their cost-effectiveness, investors adore Zerodha, which is regarded as the biggest broker in India with millions of customers, affordable pricing, and flat brokerage costs. Sensibull for sophisticated options trading, Streak for algo trading, KITE for web and mobile-based trading, and a tiny case for theme-based investment are some of its intelligent trading tools. Their trading tools make it easy to place orders, and Varsity, their educational program, is a special selling point.

Pocketful: Another up-and-coming stock broking company that provides a variety of investing possibilities and has no equity delivery fees. The application is simple to use and navigate. The platform, which aims to make investing easier, is a relatively new fintech platform in India. Its goal is to offer a smooth trading experience. The Goel brothers, Rishabh and Sarvam, founded it. The Goel Brothers are differentiating Pocketful from other bargain brokers by using their family’s experience from the Pace Stock Broking company, which has been involved in financial services for more than 30 years.

Upstox: In addition to offering slick trading interfaces, Upstox charges trading costs that are comparable to Zerodha’s flat rates. It has sophisticated charting capabilities, and Upstox has a special feature called Tick-by-Tick Engine that gives retail traders information regarding buy and sell orders. Previously, this capability was restricted to institutional and wealthy individual clients.

Top 3 Demat Account Recommendations for Investors

The 3 recommended brokers for the investors are as follows:-

Pocketful: The ideal alternative for those who want to make long-term investments is Pocketful. This finance platform is modern. There are no annual maintenance fees, account opening fees, or delivery fees with Pocketful. Their platform is built on state-of-the-art technology created by experts with over 27 years of experience. Through their site, one can invest in a wide range of assets, improving the user experience.

Kotak Securities: One of the biggest private sector banks in India, Kotak Mahindra Bank, owns Kotak Securities as a subsidiary. Additionally, it provides its clients with bank accounts and integrated demat trading for simple money transfers. Kotak Securities offers a vast array of investing options, such as mutual funds, stocks, derivatives, fixed-income products, and more. It provides cutting-edge trading platforms like Kotak Stock Trader, a web-based trading platform, and KEAT Pro X, a desktop-based trading platform that gives active traders access to real-time market data. It also offers sophisticated charting tools.

Motilal Oswal Financial Services Limited: Founded in 1987, it is one of the top broking organizations in India, providing a wide range of investment alternatives, portfolio management services, and consulting services. Their advanced trading systems include. It provides the desktop trading terminal in addition to the investor and trader apps. Motilal Oswal’s research and advising services are regarded as some of the best in the business. It provides customized consulting services for its HNI clientele and has thirty years of research knowledge. One of the best PMS services available in the market is their portfolio management platform.

Cost Efficient – A good demat account must be cost-efficient, which means the brokerage and other kinds of fees levied by the broker are less.

Ease of Tracking and Managing Investment – As securities are held in electronic form, the tracking and managing of investments is efficient and hassle-free.

Enhanced Trading Experience with Advanced Platforms – The trading platform offered by the broker must be equipped with advanced trading tools to enhance the trading experience of a trader.

Ease of Account Opening – The process of opening an account with a broker should be easy and convenient. Nowadays, a demat account can be opened in just 24 hours.

Free Research Tools—Many brokers provide demat accounts for free. However, their trading and research tools are paid; for this reason, one should consider opening a demat account with a broker that provides free research resources.

Reliability – The broker with whom you open your demat account must be credible and reliable.

Transparent Pricing – The pricing offered by the broker must be transparent. There must be no hidden charges.

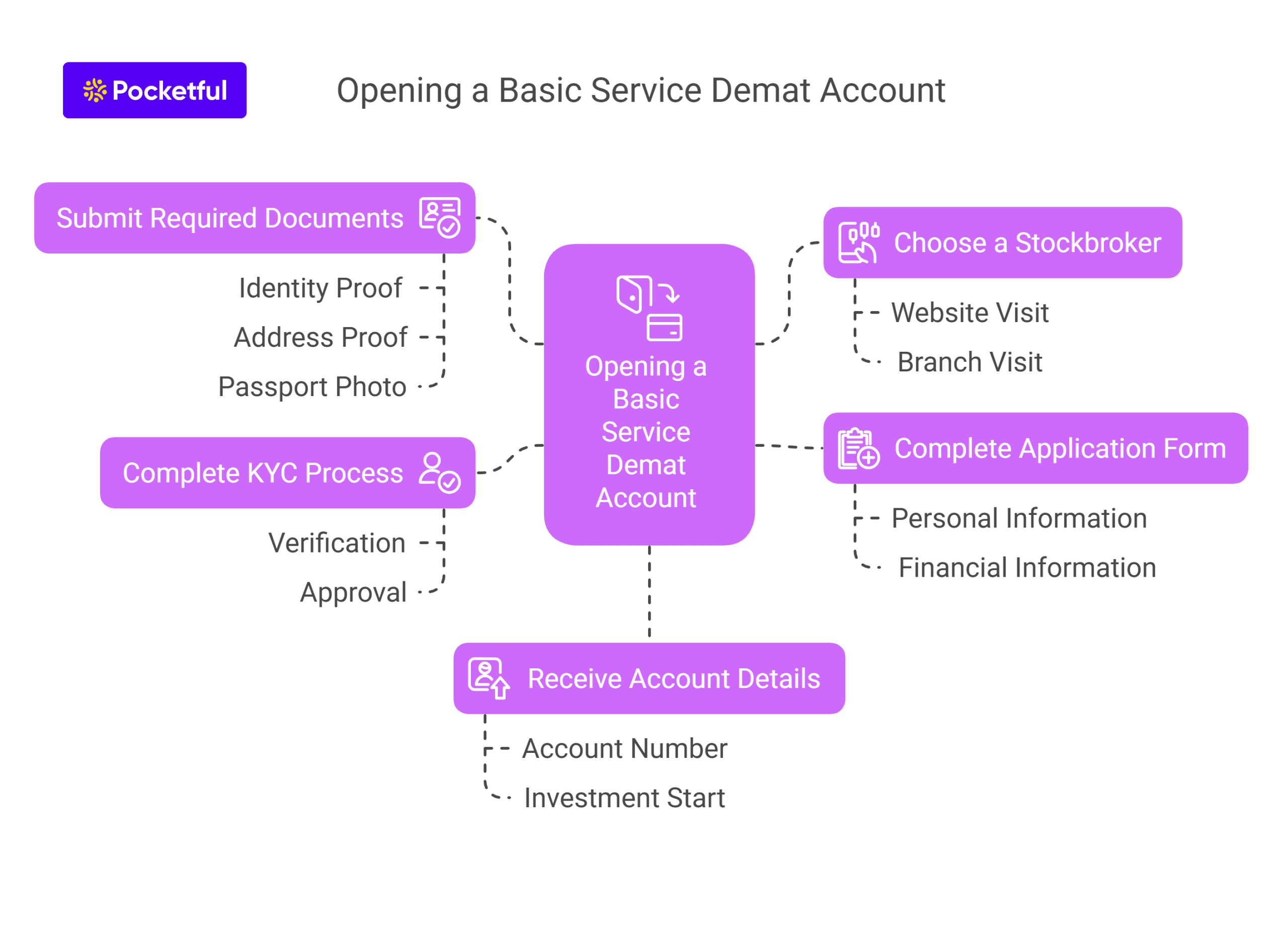

How to Open Demat Account: A Step-by-Step Guide

Opening a Demat account with Pocketful is quick, fully digital, and hassle-free. Follow the simple steps below to get started with your investment journey.

Step 1: Download and Register: Download the Pocketful app from the Google Play Store or Apple App Store and click on ‘Register’ to begin.

Step 2: Enter Personal Details: Fill in your name, mobile number, date of birth, PAN number, and address to start your application.

Step 3: Upload KYC Documents: Upload your Aadhaar card, PAN card, and a recent bank statement to complete the KYC process.

Step 4: Complete eSign & Submit: Verify your information and eSign the application using your Aadhaar-linked mobile number.

Step 5: Verification & Account Activation: Pocketful verifies your details, and once approved, your Demat account is activated. You’ll receive your Client ID and login credentials to start investing.

Importance of a Demat Account in Trading and Investing

There are various of having demat accounts, a few of which are mentioned below-

Holding Securities – A Demat Account allows you to hold securities electronically.

Transactions – If you want to sell or buy any securities, a demat account makes the process simpler.

Nomination – An investor can nominate their close ones who will inherit the securities held in their demat account in case of the holder’s unfortunate death.

No Minimum Balance – You are not required to have any minimum balance in your demat account.

Corporate Actions – The demat account manages all the corporate actions like right issues, bonus shares, etc.

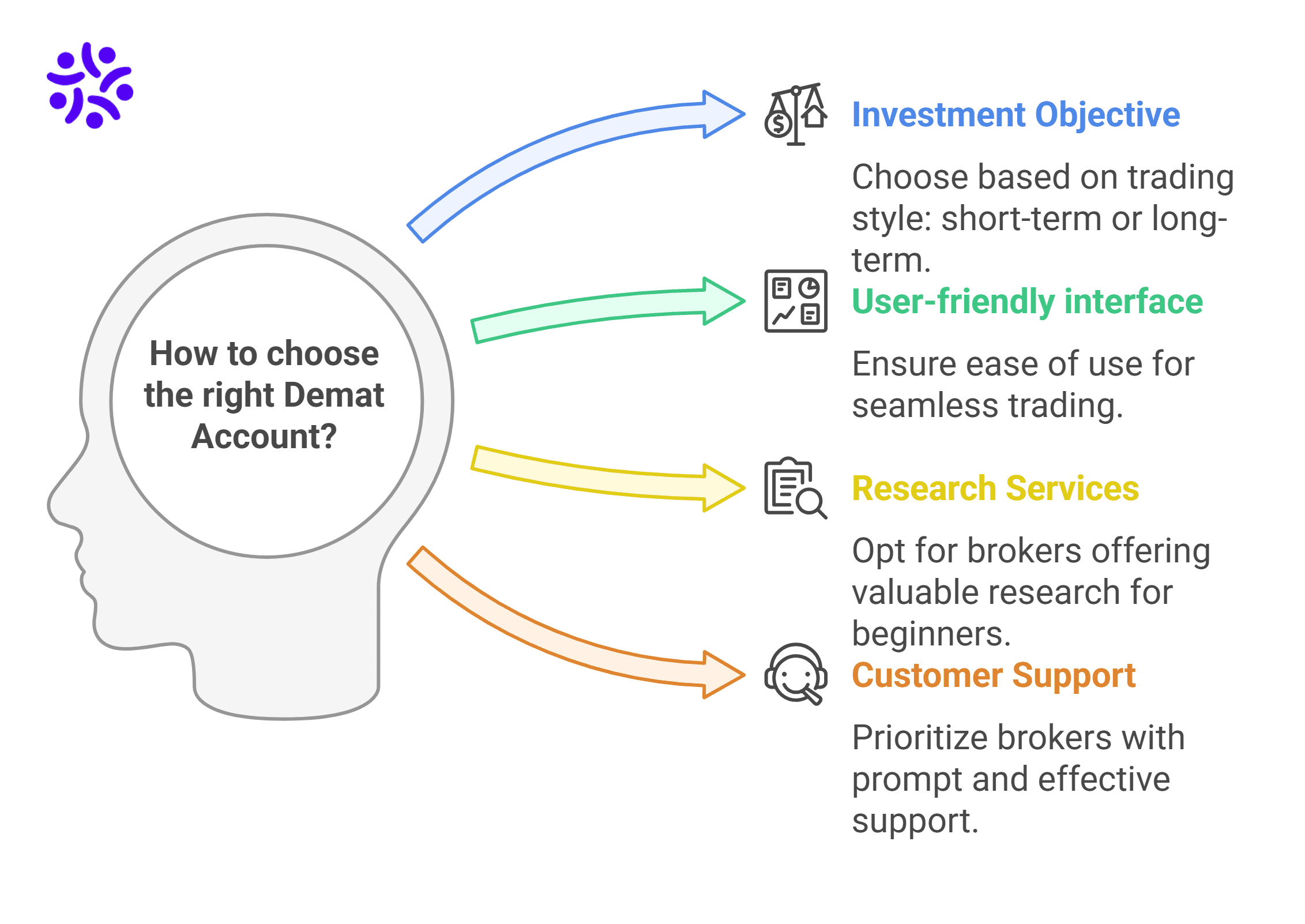

How to choose the right Demat Account for Long-Term Investment

There are various factors one should consider before choosing the right demat account, a few of which are mentioned below:-

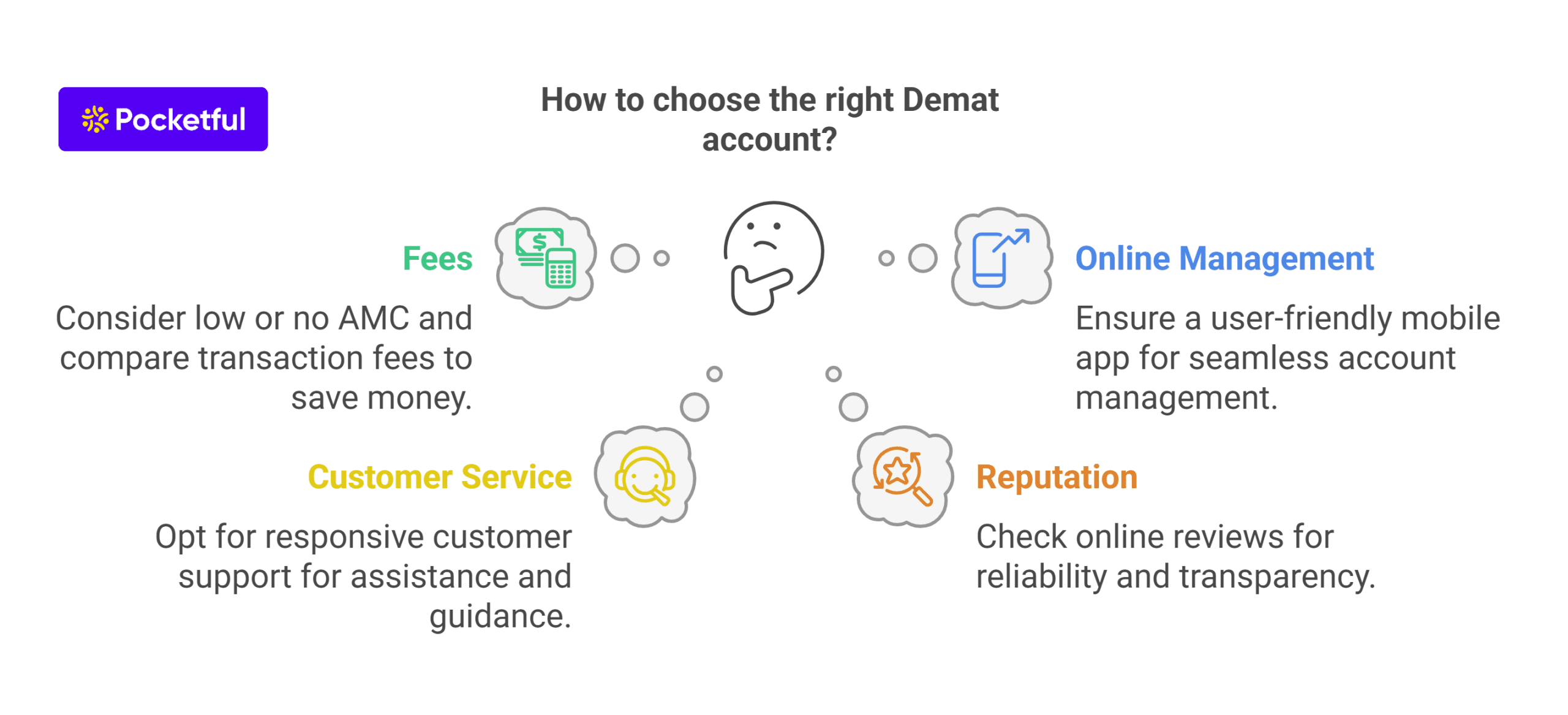

Investment Objective: Selecting a platform that provides sophisticated trading tools and cheap transaction fees is essential if you are a short-term trader. However, you should search for a broker that offers cheap annual maintenance fees if you are a long-term investor.

User-friendly interface: Before selecting a broker, you should confirm that the platform they provide is user-friendly and straightforward to use so that you can trade with ease.

Research Services: If you are new to investing, then you must opt for a broker which offers you valuable research reports and research calls that can make your investments.

Customer support: The customer support offered by the broker must be taken into consideration as Whenever you face any issues the queries must be resolved on an immediate basis.

Hidden charges: Various brokers in the industry charge some kind of hidden fees from their customers; therefore, before choosing a broker, one must conduct proper research about the hidden charges.

Trading Platform: Before choosing a broker, one must consider a trading platform which offers all the key features required by a trader or investor.

In conclusion, you should evaluate the services, fees, customer service, etc., that your broker offers if you intend to open a demat account. The investor’s investment goal also influences the broker’s choice. A Demat account, which provides the lowest brokerage and cutting-edge trading platforms, is something you should think about if you are a short-term investor. Choose a broker that offers the lowest or no annual maintenance fees, though, if you are a long-term investor.

With its cutting-edge trading tools, lowest brokerage, lowest annual maintenance fees, and other features, Pocketful provides you with a demat and trading account. By clicking the link, you can open a demat account with us.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Depending on their investing goal, beginners should select a Demat account. When searching for short-term trading opportunities, a Demat account with the lowest brokerage is a requirement, but when seeking long-term investment, a Demat account with the lowest yearly maintenance expenses is a must. We at Pocketful provide you with the most affordable brokerage and yearly maintenance fees.

How to open a demat account online?

You can open a demat account online by completing KYC, uploading documents, and eSigning using your Aadhaar-linked mobile number. Apps like Pocketful, Zerodha, and Angel One allow fully digital onboarding.

Is there a difference between a demat account and a trading account?

Indeed, the trading account allows you to buy or sell assets, whereas the Demat account just keeps them in electronic form.

Can I open a trading and demat account with the same broker?

Yes, you can open both trading and demat accounts with any broker that offers integrated account services.

Who can open a trading and demat account?

Any resident or non-resident person, corporate entity, or minor may open a Demat account; however, the legal guardian must be the only person able to manage the minor’s account.

What is the minimum amount required to open a demat account?

To start a demat account, you simply need to pay the opening fees, which are typically waived by brokers. There is no minimum amount needed.

Which demat account has the lowest brokerage?

Pocketful, Zerodha, 5Paisa, and Upstox offer low or flat brokerage, making them ideal for those looking for a low brokerage demat account.

What are SBI demat account charges?

SBI demat account charges include account opening fees (₹0), AMC (₹750 after year 1), and brokerage charges based on the type of trade.

Is Groww app safe for investing?

Yes, the Groww app is SEBI-registered and considered safe for investing and trading.

Which bank offers the best demat account in India?

Banks like ICICI Direct, HDFC Securities, SBI Securities, and Kotak Securities are popular choices among bank-linked demat accounts.

Is Zerodha better than Groww?

Zerodha offers advanced charts and tools, while Groww is known for simplicity. For advanced traders, Zerodha may be better; for beginners, Groww may be easier.

What is the Groww app and how does it work?

The Groww app is a beginner-friendly investment platform that allows users to invest in stocks, mutual funds, ETFs, and more through a simple and intuitive interface.

Is Zerodha good for opening a demat account?

Yes, Zerodha is one of India’s most popular brokers, known for its low brokerage fees, advanced charting platform (Kite), and reliable customer support.

Is Angel One a good choice for trading?

Yes, Angel One offers a powerful app, advanced charting tools, and competitive brokerage, making it suitable for both beginners and experienced traders.

What services does SBI Securities provide?

SBI Securities offers equity trading, derivatives, mutual funds and research.

How good is the HDFC demat account?

The HDFC demat account offers strong banking integration, a secure platform, and efficient customer service through HDFC Securities.

Is ICICI demat account good for investors?

Yes, the ICICI demat account is popular for its 3-in-1 account setup, strong research tools, and excellent customer support.

In 2026, selecting the right Demat account is crucial for retail and institutional investors as India’s financial markets expand. Demat accounts play an important role in the electronic holding and trading of securities. However, understanding the fees related to these accounts is essential for maximizing your returns.

This blog explains the types of demat account charges and compares demat account charges.

Why Should You Compare Demat Account Charges?

Demat accounts have various visible and hidden fees that can impact investment costs. Investors can boost their returns and minimize costs by comparing account opening fees, maintenance charges, transaction fees, and other related expenses.

Types of Demat Account Charges

Before we start with the comparison, it is essential to know the main types of demat account charges as listed below:

Account opening charges: It is a one-time charge that is incurred for opening a demat account.

Annual maintenance charge (AMC): It is a yearly fee for keeping your demat account active.

Brokerage charges: These are the costs incurred for executing trades on the platform.

Dematerialization and Rematerialization charges: Fees for converting securities from physical to electronic forms and vice versa.

Off-market transaction charges: Fee applicable for transferring securities between demat accounts.

DP Charges: These charges refer to the fees imposed by depository participants on behalf of depositories such as CDSL or NSDL for holding your securities

Pledging Charges: These are the charges that are applied by the broker when securities are used as loan collateral or fulfill margin requirements.

Comparison of Demat Account Charges Across Popular Brokers

Broker

Account opening charges

Account maintenance charge

Dematerialization and Rematerialization charges

Brokerage Charges

Pocketful

0

₹0 (Zero account opening charges)

1. Demat: Rs. 150/- per certificate 2. Remat: Rs. 150/- per certificate + CDSL Charges

Subscription-based brokerage

• Equity Delivery: ₹0 within active plan • Equity Intraday: Included in subscription • Futures: Included in subscription • Options: Included in subscription

(Statutory charges like STT, GST, exchange fees apply separately)

1. For BSDA: Rs. 0 if holding > INR 4 Lakh 2. Non-BSDA: INR 300/year+18% GST charged quarterly

1. Demat (Per certificate) : Rs. 150/- per certificate. 2. Remat (Per certificate): Rs. 150/- per certificate+ CDSL Charges

Courier charges of Rs. 100 are applicable for each demat/remat request.

1. Equity Delivery: Rs.0 2. Equity Intraday: 0.03% or INR20/ executed order, whichever is lower 3. Futures: 0.03% or INR 20, whichever is lower 4. Options: Rs. 20 per executed order

5 Paisa

Free

1. For BSDA a) 0 per month if your holding value is less than INR50,000 b) INR 8 per month if your holding value is INR 50,000 to INR 2,00,000 c) Rs. 25 per month if your holding value is above INR 2,00,000 2. For Non-BSDA: INR 25 per month

1. Demat – INR 15 per certificate 2. Remat – INR 15 per Certificate ORper 100 Units/shares(whichever is higher)

1. Equity Cash/ Equity F&O: INR 20 per order

Angel One

0

1. For Non-BSDA: INR 60 + GST per quarter

2. For BSDA: a) NIL if Holding Value less than INR 4,00,000.00 b) Rs. 100 + GST per year if holding value greater than Rs. 4 lakh and less than Rs. 10 lakh c) Holding value above Rs. 10 lakh is a non-BSDA account.

1. Demat: INR 50 per certificate 2. Remat: INR 50 per certificate + Actual CDSL Charges

1. Equity Delivery: Rs. 0 up to Rs. 500 for first 30 days. Then lower of INR 20 or 0.1% perexecuted order, a minimum INR 2 2. Intraday: Rs. 0 brokerage up to Rs. 500 for first 30 days, then lower of INR 20 or 0.03%. 3. F&O: Rs. 0 brokerage up to INR 500 for the first 30 daysthen, INR 20 per executed order

Upstox

0

Only for those accounts opened before August 2021 1. AMC of INR 150 + GST = ₹177/- 2.Quarterly maintenance charges of ₹75 + GST = ₹88.50/- (as applicable as per offer/plan)

1. Demat: INR 200 per share certificate, INR 50 for courier services +18% GST. 2. INR 25 for every certificate

1 . Equity Delivery: INR 20 per executed order 2. Equity Intraday: INR 20 or 0.05%, whichever is lower 3. Futures: INR 20 or 0.05%, whichever is lower 4. Options: INR 20 per executed order.

Groww

0

0

Demat/Remat – INR 150 per certificate + courier charges.

1. Equity: INR 20 or 0.05% of order value, whichever is lower. 2. F&O: INR 20 per executed order

Non-BSDA or Regular Demat Account: This account suits active traders and investors with higher investment volumes and usually involves higher maintenance charges.

Factors to Consider When Choosing a Demat Account

Various factors to consider before choosing a Demat account are:

Demat Account Charges: Certain brokers impose fees for opening a demat account, while others provide the service at no cost. When opening a demat account, an individual should factor in the amount of the account opening fee and AMCs.

Brokerage: Compare brokerage rates for intraday trading, delivery trades, and future & options trading. Choose discount brokers for frequent trading as they generally offer lower fees than full-service brokers.

Trading Platforms and Tools: Make sure the broker offers a dependable and user-friendly platform for trading on mobile applications. Look for advanced features such as real-time charts, technical analysis tools, and quick execution speed.

Regulatory compliance and Ratings: Check if the broker is registered with regulatory authorities such as SEBI. You can go through the customer reviews and ratings on the internet to assess the reliability of their service.

Customer support: Seek brokers that provide fast and easy customer service via phone, email and live chat. Also, check their service hours and availability during trading hours.

Nomination services: Select a broker that lets you choose a nominee to protect your investment. Use brokers with strong security measures like two-factor authentication to safeguard your account.

Geographic reach and branch network: If you value in-person support, consider choosing brokers that offer an extensive branch network. Assess their capability to offer services in various cities or regions.

Account closure and Transfer process: Check the process and any fees for closing your account or transferring holdings to a different demat account.

Hidden Charges to Watch out for

You must be aware of the hidden charges associated with a Demat account:

Call & Trade Charges: These are fees charged for placing orders via phone with your broker instead of using online trading platforms. If you find yourself unable to execute trade online because of technical difficulties, you can choose the call & trade option.

Stamp Charges: This is a kind of tax imposed by the government on the value of security traded in your account. It is charged during the purchase of stocks and other assets.

Account with Debit Balance: It is a penalty or interest imposed on a demat account because of insufficient funds for unpaid balances.

Margin Trading Facility (MTF): It is a facility that allows investors to borrow funds from the broker to trade larger positions than their available cash balance. Additional interest charges are imposed when an individual avails margin facility to buy shares.

DIS Slip Request Charges: DIS stands for delivery instruction slips. These are the charges levied for obtaining DIS booklets to transfer shares offline between demat accounts. It is applicable for manual share transfers instead of online ones and is often needed by investors with accounts at different DP.

DDPI Charges: DDPI stands for Demat Debit and Pledge Instruction. These charges are levied when issuing DDPI, which allows brokers to debit or pledge securities from an individual’s demat account.

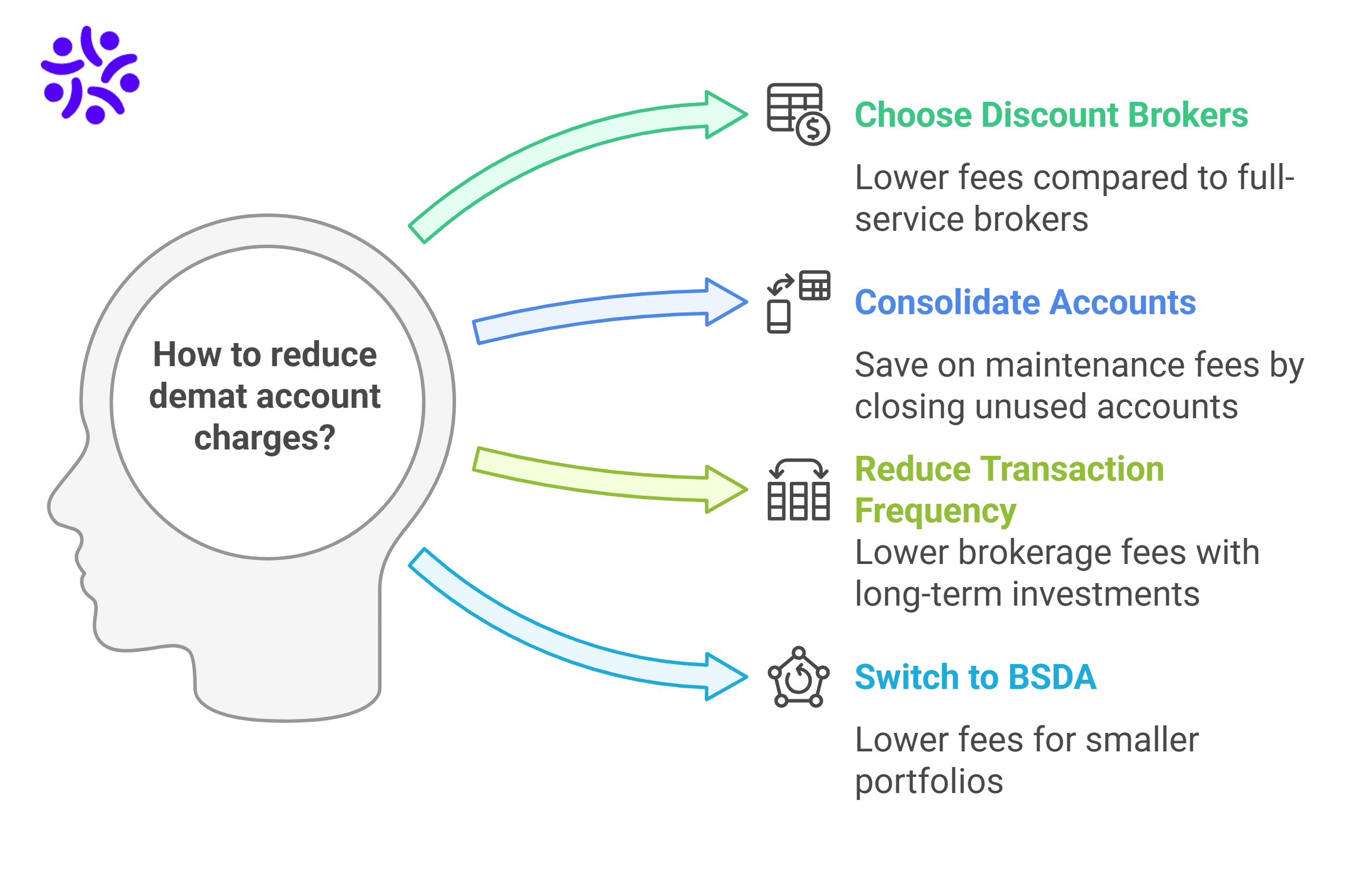

How Can I Reduce My Demat Charges?

Lowering your demat account fees can improve your investment returns. Some of the points by which you can reduce your demat charges are listed below:

Choose discount brokers because they usually have lower account opening fees, AMC, and transaction costs than full-service brokers.

Avoid having multiple demat accounts unless necessary since each one has its own maintenance fees. Transfer holdings from unused accounts to your active account and close dormant accounts to save on AMC.

Reduce the frequency of transactions because every trade comes with transaction fees. Choose long-term investments instead of high-frequency trading (HFT) to lower brokerage fees and other costs.

If your portfolio is worth up to ₹4,00,000 in India, you can think about switching to a BSDA or basic service demat account.

Evaluate your broker’s performance and fees regularly. If you are paying high fees or their services are unsatisfactory, you can consider transitioning to a more cost-effective broker that offers better options.

Selecting the ideal broker for a demat account involves striking a perfect balance between cost-effectiveness and the variety of features available. Choose the platform that matches your financial goals and trading style, has lower fees, advanced features and offers personalized support. By assessing the fees, services and benefits, you can make a smart decision to enhance your investment returns in 2025. It is advised to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

A demat account is used to hold financial assets such as stocks, bonds, and ETFs in electronic form. It removes the need for physical share certificates and ensures faster, secure trading in the stock market.

Can I open a demat account without linking it to a trading account?

You can open a standalone demat account to store securities. However, if you want to trade in the stock market, you will need a trading account as well.

Are there any hidden charges I should watch out for?

Some of the common hidden charges include call & trade fees when using customer support and higher AMC after initial promotional periods.

Can we maintain 2 demat accounts?

You can open multiple demat accounts with different DPs.

What is the difference between CDSL and NSDL?

CDSL and NSDL are two depositories in India where your securities are stored, and your demand account is opened at one of these depositories. There is no difference between CDSL and NSDL as both provide the same services and are regulated by the SEBI.

With the wide range of investment options available in India today, a lot of people have chosen the stock market to secure their financial future. A Demat account is essential to participate in the stock market, and individuals usually open one by contacting a stockbroker who is a Depository Participant (DP). But can an investor open a Demat account without a broker? The answer is yes! It is possible to open a Demat account without a broker.

In this article, we will discuss how to open a demat account without a broker, the documents required to open a demat account in India, and its benefits.

What is a Demat Account?

A Demat account is a form of an electronic account that stores stocks and securities in the form of electronic records. This account provides a convenient location for the storage of stocks, bonds, and mutual funds, among other investment instruments. The Demat system in India was created to facilitate the storage and transfer of shares without the need for physical certificates. Some of the inherent features of a Demat account include the following:

Secure Holdings: A demat account makes it convenient for investors to secure different types of securities in one account and eliminates the hassle of handling numerous physical certificates.

Enhanced Efficiency in Share Trades: Buying and selling shares becomes simpler due to the short settlement period.

Lesser Danger: Because the shares are in the Demat account, it eliminates potential dangers like theft, loss or damage to physical share certificates.

Comprehensive Record of All Holdings: An investor has online access to information about his/her holdings, transaction details and his/her account balance within any given time frame.

You might be thinking, “Can I start trading without a Demat Account?” The answer to your question is yes. Investors can open a trading account with a broker to trade securities listed on the stock exchange.

Considering the advancements in technology and the rise of online trading platforms, questions arise regarding the relevance of a broker in the process of opening up a Demat account.

First, we need to understand the difference between a Depository Participant (DP) and a broker. A DP acts as an intermediary between the investor and the depository, i.e., CDSL and NSDL. On the other hand, a broker acts as a link between the investor and the stock exchange. Some of the financial institutions in India offer services of both DP and a broker.

According to SEBI regulations, investors can only open a Demat account with the help of a DP. This makes it possible to open a Demat account with the help of a financial institution that is a DP but not a broker. However, you might think, “Can I buy shares without a broker?” The short answer is no. One must open a trading account with a broker to buy and sell shares.

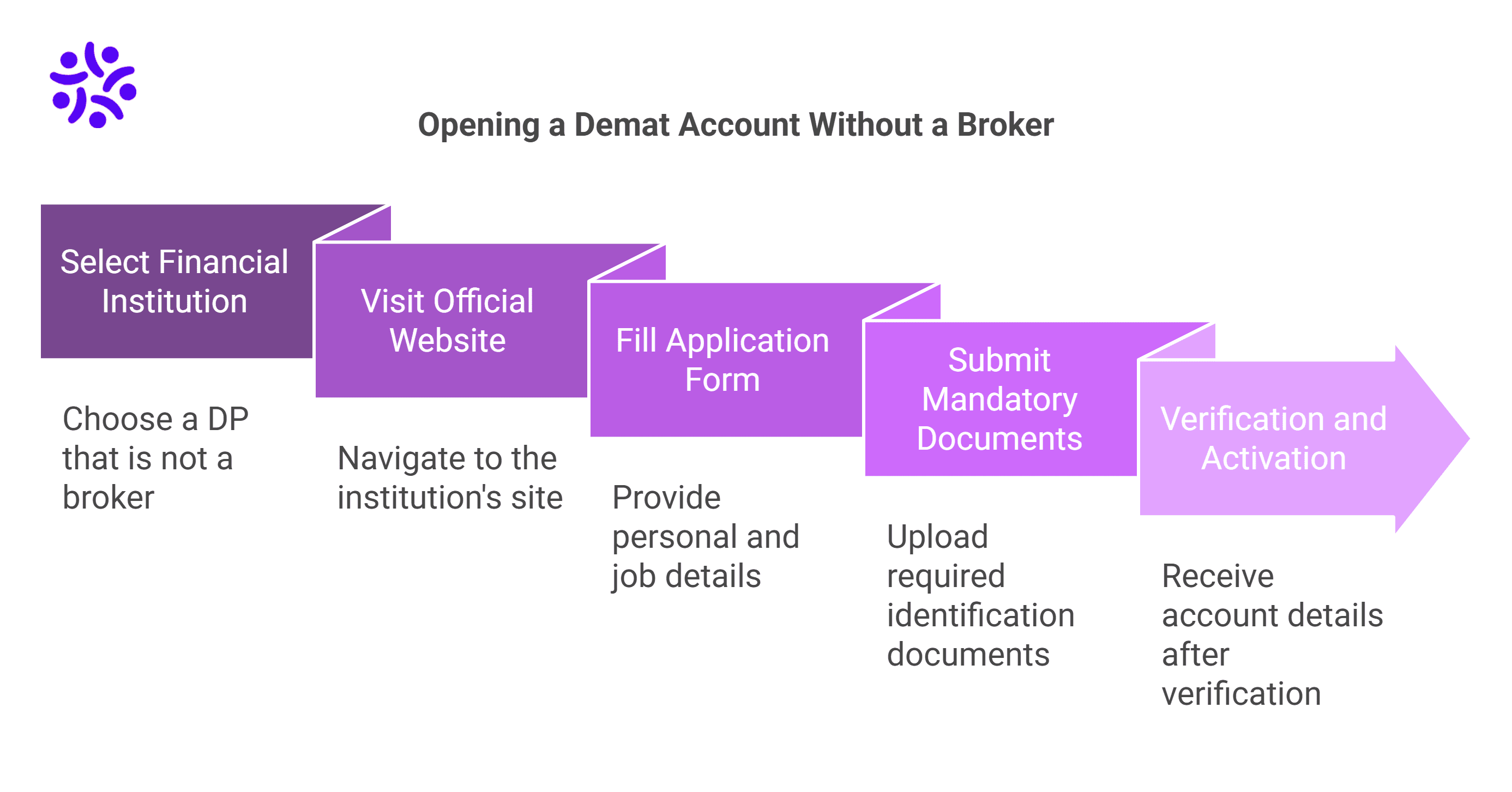

Opening a Demat account without a broker is an easy task. Below is the step-by-step procedure.

1. Select Financial Institution

First, choose a financial institution that is a Depository Participant (DP) but not a stockbroker. Many banks, financial services companies, and even fintech platforms offer Demat account opening facilities.

2. Official Website

Open the official website of the selected financial institution. Most of them have online account opening procedures in place. Click on a subsection for Demat Accounts entitled “Open a Demat Account” or “Account Opening.”

3. Fill the Application Form

Fill an application in which you provide the following details:

Full name and address and mobile number/landline phone number, Email ID

Source of income and job particulars.

4. Mandatory Documents

You will be asked to submit the following documents :

Proof of Identity

Proof of Address

PAN Card

Passport-sized Photographs

Verification and Activation of Account

After submitting the application and the documents, the financial institution will verify the information. This can take some hours to a few days. Upon verification, you will receive the details of your Demat account, including your login credentials.

1. Proof of Identity: The following documents can be submitted as a proof of identity:

Aadhar card

Passport

Voter ID

Driving License

2. Proof of Address: The following documents can be submitted as a proof of address:

Utility bills: electricity, water, gas, etc.

Bank statement

Rental agreement

Any government document with your address

PAN Card: You cannot open a Demat account without a PAN Card, making it a mandatory document.

Passport Size Photographs: Typically, two passport-sized photographs are required, not older than six months from the date of submission of the application.

Bank Account Information: A canceled cheque or bank statement might be required to link your trading account with your bank account for smooth transactions.

All the documents must be accurate and complete, which will help in speeding up the process of opening an account.

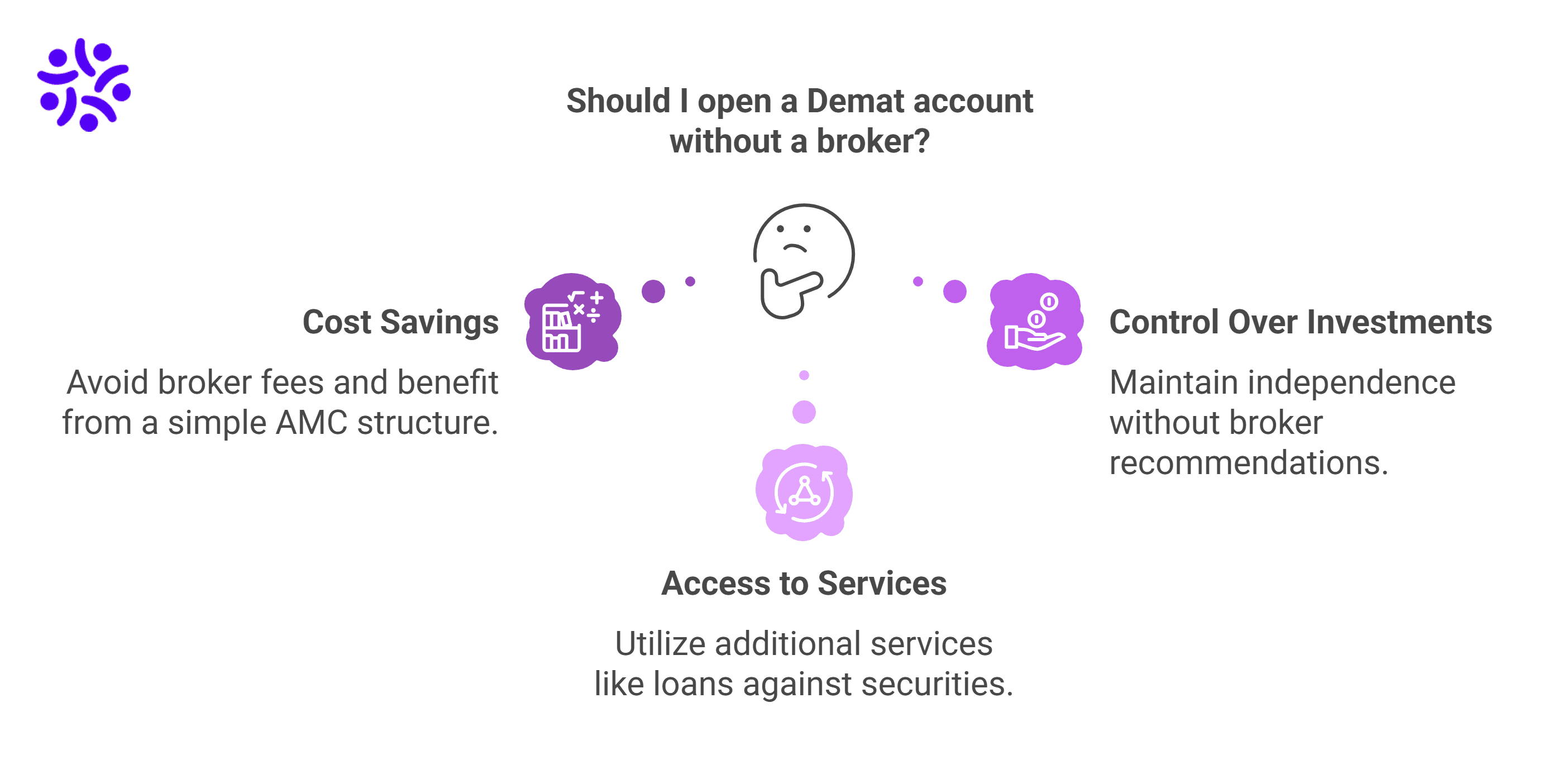

Advantages of Opening a Demat Account Without a Broker

There are many advantages to opening a Demat account without a broker. These are:

1. Cost Savings

Opening a Demat account without a broker helps investors avoid paying charges related to trading. DPs who are not stockbrokers offer a simple fee structure that consists of AMC.

2. Control Over Investments

Brokers usually give out trade recommendations to their clients. Due to the absence of brokers, investors can continue to hold investments without any distractions and have complete control over their investments.

3. Access to the Other Services

Investors opening only a Demat account are usually long-term investors. Investors can take advantage of other services provided by the non-broker DPs, such as loans against securities or other privileges for opening a Demat account with the DP.

The investors can open a Demat account without a broker, which enables the investor to focus on the safe storage of financial assets without worrying about trading. Using the procedure mentioned above, one can easily open a Demat account.

Opening a Demat account without a broker is ideal for investors who just want a safe storage facility for their investments and wish to hold them for a long time. However, if you are thinking, “Can I trade without a broker?” The answer is no, as you must have a trading account with a broker to execute buy and sell transactions.

Frequently Asked Questions (FAQs)

Can we buy shares in India without a broker?

It is not possible to buy shares listed on the stock exchange without a broker.

Can I trade without a Demat account?

You only need a trading account to buy and sell shares, and a Demat account is required to store them electronically.

What are the charges associated with opening a Demat account without a broker?

The charges vary across different DPs, but most of them don’t charge account opening fees. However, DPs charge account maintenance charges to keep your demat account active.

How long does it take to open a Demat account without a broker?

If all details and documents submitted are correct, then it may take a few hours to a few days to open a demat account, depending on the DP’s verification process.

Is it safe to open a Demat account without a broker?

It is safe to open a Demat account without a broker as these DPs are authorized by the depositories to offer Demat account services.

Individuals invest their hard-earned money to maximize profits. A dematerialized account helps investors hold and manage securities electronically. However, there are numerous charges that one must pay brokers while investing, which makes the selection of an appropriate demat account a necessity in today’s financial markets. A lifetime free demat account is a type of Demat account that provides all the benefits of a Demat account at zero Annual Maintenance Charges (AMCs).