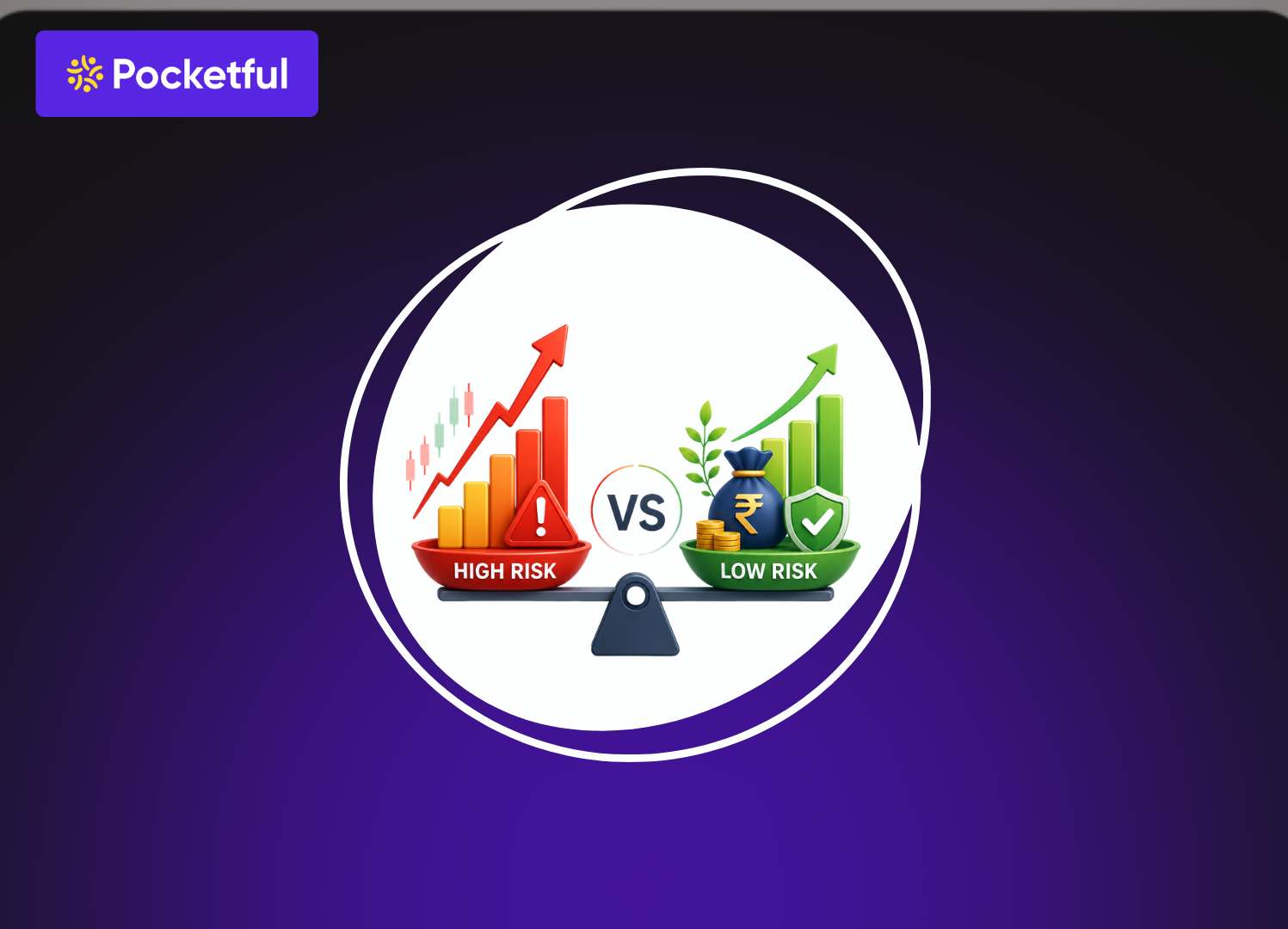

Before investing in mutual funds, the biggest question is whether I should invest in high-risk funds or low-risk funds. High-risk funds offer high returns but come with volatility, and low-risk funds offer lower returns and provide stability in the portfolio during market fluctuations.

In today’s blog post, we will give you an overview of high-risk funds and low-risk funds, along with their key differences and also tell you which one is suitable for you.

What are High Risk Mutual Funds?

High-risk mutual funds are those funds that primarily invest in equity and other volatile assets. Their primary objective is to generate higher returns over time. However, they are volatile in nature. High-risk can show volatility in the short-run, but can generate higher returns in the long-run, hence they are suitable for investors who have a longer investment horizon. High-risk mutual funds generally invest in small-cap and mid-cap stocks.

Key Features of High Risk Mutual Fund

The key features of a high-risk mutual fund are as follows:

- Higher Returns: The high-risk mutual fund can generate higher returns over the long term as these funds invest in equities.

- Volatile: High-risk mutual funds are highly volatile in nature. Their prices can fluctuate very sharply during a market correction.

- Long-Term Investment Horizon: High-risk mutual funds are suitable for the investor who has a long-term investment horizon.

- Inflation-Beating Return: The high-risk mutual fund can beat inflation in the long-run as it tends to generate high returns.

What are Low Risk Mutual Funds?

Low-risk funds are those mutual funds whose primary role is to protect the capital of investors and provide steady returns. Unlike any other high-risk mutual fund, a low-risk fund primarily invests in instruments having fixed returns, such as government bonds, treasury bills, etc. The low-risk fund posts low returns and is suitable for conservative investors. These funds are often used by the investor as an investment option when they want to create a balance in their portfolio.

Key Features of a Low-Risk Mutual Fund

The key features of a low-risk mutual fund are as follows:

- Capital Preservation: The key objective of a low-risk mutual fund is to preserve capital from any downside.

- Low Returns: As the low-risk mutual fund focuses on low volatility they also provides consistent low returns.

- Conservative Investor: The low-risk mutual funds are suitable for investors having a conservative risk profile and prefer safety over high returns.

- Stability in Portfolio: During volatile market conditions, a low-risk mutual fund helps in balancing the overall investment portfolio.

Read Also: Difference Between Large Cap vs Mid Cap Mutual Fund

High Risk vs. Low Risk Mutual Fund

The key difference between high-risk and low-risk mutual funds is as follows:

| Particulars | High Risk Mutual Fund | Low Risk Mutual Fund |

|---|---|---|

| Objective | The primary objective of investing in a high-risk mutual fund is wealth creation. | The key objective of investment in a low-risk mutual fund is to preserve capital. |

| Underlying Asset | High-risk mutual funds generally invest in equities, including small-cap and mid-cap stocks. | A low-risk mutual fund invests in fixed-income securities. |

| Returns | High-risk mutual funds post higher returns. | A low-risk mutual fund offers low to moderate returns in the portfolio. |

| Volatility | High-risk mutual funds are highly volatile in nature. | These funds offer low volatility. |

| Suitability | These funds are suitable for aggressive investors. | Low-risk mutual funds are suitable for conservative investors. |

| Taxation | High-risk mutual funds follow the equity taxation rule. | The low-risk mutual funds are taxed based on the investor’s income tax slab. |

| Impact of Market Fluctuations | These funds are highly affected by the market fluctuations. | Low-risk mutual funds are the least affected by market fluctuations. |

| Safety of Capital | The safety of capital is not guaranteed in a high-risk mutual fund. | In a low-risk mutual fund, capital is generally safer than in a high-risk mutual fund. |

Which is suitable for you – High Risk or Low Risk Fund?

Choosing among high-risk and low-risk funds depends on the investor’s financial goal, investment objective and risk profile. If an investor is looking to create wealth in the long run, they can opt for a high-risk mutual fund, as they have the potential to generate a high return. On the other hand, a low-risk mutual fund is suitable for a conservative investor whose priority is to preserve capital and earn steady returns. In most of the cases, it is advisable to have a mix of both high-risk and low-risk mutual funds.

Conclusion

On a concluding note, both high and low-risk mutual funds serve different purposes. High-risk mutual funds are suitable for investors seeking long-term wealth creation and who are comfortable with market volatility. While there is a category of investor who do not want to take risks, are not comfortable with volatility in their portfolio, and prefer low-risk investment options with stable and predictable returns. However, both funds carry certain risks, such as high-risk funds carry market risk and low-risk funds carry interest rate risk, credit risk, etc. Therefore, it is advisable to consult your investment advisor before making any investment in mutual funds. Pocketful offers access to 2,000+ mutual fund schemes. Download now and enjoy zero brokerage on delivery trades and mutual fund investments.

Frequently Asked Questions (FAQs)

What is the meaning of high-risk and low-risk mutual funds?

High-risk mutual funds are those funds that invest primarily in equities and have the potential to post higher returns. Whereas low-risk mutual funds invest in fixed-income securities, such as government bonds, etc. and post stable returns with lower volatility.

How to reduce risk while investing in a high-risk mutual fund?

One can reduce their risk by increasing their investment horizon. High-risk mutual funds are volatile in the short run; however, in the long run, they post inflation-beating returns.

Do high-risk mutual funds always post high returns?

No, a high-risk mutual fund does not always post high returns their performance depends on the fund manager’s capabilities and market performance. Returns are not guaranteed in a high-risk mutual fund.

What are the key examples of high-risk mutual funds?

The key examples of high-risk mutual funds are mid-cap funds, small-cap funds, sectoral and thematic funds, etc.

Do low-risk mutual funds always invest in debt securities?

No, it is not necessary that a low-risk fund always invest in debt securities. There are categories of hybrid funds, such as a conservative hybrid fund, which invests a small portion of its portfolio in equity-related instruments.