A thread on the wrist for Raksha Bandhan is more than just a thread. It is a promise of love, protection, and support. Every year, we strive to find the perfect gift to convey what words cannot. What if, though, you could give your sister something this year that will make her happy today and appreciates in value over the years?

Instead of the usual chocolates, gadgets, or gift cards, why not give her something associated with a brand she already likes such as shares of some of her favourite companies that are listed on the stock market. These include the companies behind the jewellery she wears and the skincare products she uses. Now, she can go beyond being just a consumer — she can actually own a piece of them.

In this blog, we will explore some of the best stocks to give your sister this Raksha Bandhan the process of gifting shares.

Why Gift Stocks Instead of Traditional Gifts?

Rakhi is all about celebrating your relationship with your sister, and what better way to express your love than by giving her a gift that will grow with time?

Not that chocolates, perfumes, or handbags are not wonderful, they certainly are, but consider giving her something that could contribute towards making her future financially secure. That is where gifting stocks is better than other traditional gifts.

1. Creates Long-Term Wealth

A quality stock can increase in value over time, unlike most gifts that are overlooked or lose their value over time.

2. Helps Her in Beginning Her Investment Journey

This could be an interesting and mindful approach that could build your sister’s interest in investing, if she were not already. How great is it that it could even spark her interest in investing or personal finance?

3. It is symbolic and personal

Picture her checking the price of the stock gifted each Rakhi and seeing it grow year after year; it becomes a custom, a memory, and a bond that lasts beyond the celebration.

4. It is simple and tax-free

No need to stress about the paperwork — if your sister has a demat account, transferring shares is quick and hassle‑free. Plus, gifts between siblings are tax‑free, making it even more worthwhile.

Falguni Nayar started Nykaa in 2012 as an online beauty store. It has since grown into a huge marketplace for cosmetics, skin care, fashion, and personal healthcare products. It introduced many Indian customers to international beauty brands, and now it has a presence in India both online and in stores.

Why Gift It: If your sister loves beauty products, Nykaa is already a part of her life. Giving her shares means saying, “You’re not just a customer; you’re now a co-owner.”

Titan is a part of the Tata Group, which started making watches in 1984 and later added jewellery (Tanishq), eyewear, and other accessories to its product portfolio. Tanishq and CaratLane as household names for getting good jewellery and gifts.

Why Gift It: If she loves her Tanishq necklace or often finds herself searching for new jewellery on CaratLane, Titan is already part of her lifestyle. This Rakhi gift shares to turn that connection into ownership.

Kalyan started in Kerala in 1993 and has since grown into one of India’s biggest jewellery chains. It is known for its large selection of gold, diamond, and bridal jewellery. The “Trust is Everything” campaign hit a chord with people all over India.

Why Gift It: Kalyan feels personal if she likes traditional jewellery. You are giving her a piece of a brand that she already feels emotionally and culturally connected to.

4. Hindustan Unilever Ltd

HUL is a British-Dutch company that has been in India since 1933. It owns almost all of the major personal care brands you can think of, like Lakme, Dove, Sunsilk, Pond’s, Tresemme, and Pears.

Why Gift It: She probably uses these products every day. By owning HUL shares, she can start creating wealth from the very brands she already trusts and loves — turning everyday purchases into long-term value.

Dabur, which was founded in 1884, is a leader in Ayurvedic and herbal health products. Its products are very common in Indian households due to well-known brands like Gulabari, Vatika, Real Juices, and Fem.

Why Gift It: If she believes in natural, Ayurvedic self-care, Dabur represents a blend of heritage, trust, and long-term growth — making it an ideal gift.

Here are the steps you need to take to gift stocks:

1. First things first: Does she have a demat account?

Your sister needs a demat account to own stocks. You can help her create if she doesn’t have one yet. Most brokers let you open a demat account online in less than 10 minutes.

2. Choose the Stock You Want to Gift

Pick a stock that you believe in, one that has a stable performance and that she might be able to relate to. For instance, Titan, if she likes jewellery or HUL, for long-term stability. If it is a brand that she already uses or likes, it makes it even better!

3. Give her the stock

If you use a traditional broker, you will need to fill out a simple form called a Delivery Instruction Slip (DIS). This document specifies the stocks you are gifting and to whom. If you use an app-based broker, you can do everything online.

4. This is all there is to it

She must accept the gift and then you will be asked to authorize the transaction using CDSL T-PIN. The stocks will show up in her demat account.

Giving stocks as a gift might seem strange, but it is one of the best ways to show your sister you care about her future. You are not just giving her a gift; you are also introducing her to the world of investing.

This Raksha Bandhan, go beyond the usual. Gift her growth. Gift her ownership. Gift her a piece of the brands she already loves.

Frequently Asked Questions (FAQs)

Is gifting shares taxable?

No, gifting shares to your sister is not taxable in India. Gifts between siblings are exempt under the Income Tax Act. However, if she sells those shares later and makes a profit, capital gains tax may apply at that time, just like with any regular stock sale.

Can I gift mutual funds instead of shares?

You can gift mutual fund units too and the process is similar.

What if my sister does not have a demat account?

She can open one easily online through platforms like Pocketful. The whole process takes just 10–15 minutes.

Are these stocks suitable for long-term investment?

The companies discussed have performed consistently over the past many years, but future performance cannot be guaranteed. Hence, it is advised to consult a financial advisor before investing.

Is there a minimum amount for gifting stocks?

No, there’s no fixed minimum amount. You can gift even a single share or as many as you like, based on your budget and the stock’s price.

In Hindu tradition, Rakshabandhan is more than just a festival or a symbolic thread of protection, it represents an unsaid commitment to safeguard your sister. In the same way, you can protect her financial future by giving financial gifts instead of material ones, as financial assets usually appreciate in value, helping her secure her future and achieve her dreams.

In this blog, we will give you an overview of the best financial gifts for your sister, which you can give to her this Rakshabandhan.

What is a Financial Gift?

A financial gift is a transfer of property, money, or assets to another person without expecting anything in return. It is a way to give valuable assets to your close ones. The financial gifts include cash, fixed deposits, mutual funds, stocks, etc. The main objective of these gifts is to help your close ones in building long-term wealth and encourage financial discipline.

Importance of Financial Gift

The key benefits of a financial gift are as follows:

Financial Security: A monetary gift can help an individual build a strong foundation for creating long-term wealth.

Encourage Discipline: Gifting mutual funds and fixed deposits can encourage financial discipline.

Wealth Creation: Financial gifts can help an individual build long-term wealth while reducing the tendency to spend the amount immediately.

Financial Goals: Financial gifts can be given for achieving specific financial goals such as marriage, education, house purchase, etc.

Tax Efficiency: Gifts given to close ones, such as siblings, parents or children, are exempted from tax in India.

Best Financial Gifts for Sister 2025

The list of the best financial gifts for a sister is as follows:

1. Mutual Funds

Mutual funds are financial assets which can help a person create wealth in the long run. There are various options through which one can gift mutual funds to their sister, such as in the form of a lump sum investment or SIP. It is best to save based on specific goals such as education, marriage, etc. Mutual funds are professionally managed funds that offer diversification, helping to reduce risk. One can start a SIP for her and help her learn the importance of financial discipline over time. However, you also invest a lump sum amount in the mutual fund and gift it to her.

2. Stocks

It is important to introduce your sister to the world of the stock market so that she can understand the benefit of compounding at an early stage. You can give her shares of fundamentally strong companies so that the value of her equity portfolio increases over time. You can transfer shares from your demat account to her demat account directly. However, she will have to pay capital gain tax whenever she sells the shares. It is advisable to conduct thorough research before choosing any stock for investment.

3. Digital Gold

Gold has always been considered a traditional investment option and a safe haven. Earlier, people used to give gold jewellery to their sisters, but owning physical jewellery carries certain risks, such as storage cost, wear and tear, etc. Hence, digital gold in the form of gold mutual funds, gold ETFs, and Sovereign Gold Bonds can be a better option to gift your sister. You can purchase digital gold in her name and gift it to her.

4. Fixed Deposit

Investment in fixed deposits is low risk and has assured returns. Therefore, fixed deposits can be a suitable gift option for your sister if you are looking for stable returns. Returns on fixed deposits may not be inflation-beating but they can be used as an emergency fund or for short-term financial goals. You can easily open a fixed deposit in her name and give the fixed deposit receipt to her, and on maturity, she can visit the bank and get it encashed.

5. Sukanya Samriddhi Yojana

It is a government scheme in which you can open a Sukanya Samriddhi account in the name of your sister who is below 10 years of age. Investment in the Sukanya Samriddhi Yojana comes with a lock-in period, which lasts 21 years from the date of opening of the account or gets married after attaining 18 years of age. These are backed by the government, hence carry the lowest risk. Sukanya Samriddhi Yojana cannot be gifted directly unless you are a guardian.

6. Gift Cards

A perfect balance between thoughtfulness and freedom, letting your sister decide what she loves most. Various online retailers offer gift cards. You can purchase the gift card from them and gift it to your sister on Rakshabandhan.

7. Cash

It is the most convenient financial gift which one can give to their sister on Rakshabandhan. Unlike other financial gifts that are meant for long term financial goals, cash can be used anytime by your sister.

Tax Implications of a Gift

All the above-mentioned gifts, if gifted to your sister, are considered tax-free. No tax is payable by your sister. However, the interest or capital gain earned on these financial gifts are subject to taxation as per the applicable capital gain tax rate or as per her income tax slab. And if your sister is a minor, the income on these financial assets may be clubbed with the parents’ or guardian’s income.

Conclusion

On a concluding note, gifting financial assets to your sister on the auspicious occasion of Rakshabandhan is a smart choice. The financial gifts can help your sister achieve her financial goals. The Income Tax Act also allows tax-free gifting to your siblings, hence making it one of the most efficient ways to create wealth. The value of material gifts decreases over time, but the value of financial assets increases. Therefore, consider gifting financial assets to your sister but only after consulting your investment advisor to ensure they align with her risk profile and investment objectives.

Frequently Asked Questions (FAQs)

What is the applicable tax rate on giving financial gifts to my sister?

There is no tax payable by you or by your sister on the gift given to her. However, the income generated by the financial assets is taxable as per the applicable tax laws.

Is there any limit on the amount that is tax-free when gifting to a sister?

No, there is no limit. Gifts given to your sister are fully exempt from tax under the Income Tax Act.

How can I gift stocks to my sister?

First, you need to open a demat account for your sister, and then you can choose the stock from your demat account and gift it directly to your sister. It will be debited from your demat account and credited to her demat account.

Is a gift deed required for financial gifts given to a sister?

No, it is not mandatory to prepare a deed while gifting a financial asset to your sister. However, it is advisable to create one for high-value gifts to avoid any future inconvenience.

Is the income generated from the gifts given to the sister taxable?

Yes, income generated from the financial gifts given to your sister is taxable.

Anyone who has ever scrambled to find spare change in a crowded market knows how frustrating and time-consuming cash payments can be. That’s where UPI apps come in to save the day as they let you send money with just a few taps.

This blog will introduce you to some of the most popular UPI apps in India, helping you choose the one that fits your needs best. With so many options available, each with its own unique features, strengths, and drawbacks, understanding the pros and cons of each app will make it easier for you to make the right choice.

What is UPI?

Unified Payments Interface, or UPI for short, is an instant money transfer system built by The National Payments Corporation of India in 2016. With UPI, money moves straight from one bank account to another, with just the help of a smartphone almost like a text message traveling with cash inside. This system enables high speed digital financial transactions.

Since the launch, UPI has transformed the way we think about payments. In 2022, close to half the world’s instant transactions passed through Indian phones. India literally tapped its way through 18.68 billion UPI payments in May 2025, moving a jaw-dropping ₹25.14 trillion before the month even ran out. If the current trend holds, UPI could claim nearly 90% of every retail digital rupee spent by the end of 2026-2027. This rising growth is also fueling a boom in the wider digital wallet scene, where UPI sets the pace. Meanwhile, the Reserve Bank of India keeps a watchful eye, adding a layer of regulatory oversight and increasing trust among the users.

UPI : A Simple Breakdown

Sending cash through a UPI app is all about smart tech and user friendly technology doing its job behind the curtain. Digital IDs, mobile networks, and a high tech savvy system together enable instant payments that barely gets noticed. Encryption wraps around the data like a security blanket, keeping prying eyes out until your phone beeps to confirm the transfer.

Every transaction begins and ends with the Virtual Payment Address (VPA) also known as UPI ID. This is a unique ID of the user’s bank account and using this unique ID helps in securing the other sensitive information like the IFSC code or full bank account details as the odds of important financial information leaking out during a money transfer drop sharply.

To authorise a transaction the app asks for a UPI PIN. This is a secret 4 or 6 digit code which is similar to an ATM PIN. This PIN adds a security layer to the transaction, with two-factor-authentication process safeguarding the transaction till the last step, keeping fraudsters locked outside the vault.

The NPCI manages the entire UPI ecosystem, making it an easy to use, smooth and secure way of transaction with integration of all banks and payments applications.

UPI payment methods fall into two categories :

Push Payments: You decide to send cash, either by typing in a virtual payment address (VPA) or by scanning a QR code that someone hands you. Once you hit send and enter your PIN, the money is sent to the other person’s account almost instantly.

Pull Payments: A shop owner or a friend can ping you with a money request. If you agree, you approve the request with your PIN, and the funds are sent from your account to fulfill these requests.

UPI allows a single app to add and transfer funds to several bank accounts, this means you can switch to pay to different users, giving you flexibility and convenience to manage your finances by using one interface.

Top UPI Apps in India

App

Key Features

Unique Selling Point

Best For (User Type)

PhonePe

User-friendly interface, multi-language, bill payments, recharges, QR scan, investments (MFs, Gold, NPS), insurance, loans, PhonePe Switch

Comprehensive “Super App” with wide merchant network

All-round users seeking diverse financial services

Google Pay

Minimalist design, NFC tap-to-pay, bill payments, recharges, expense tracking, voice transactions, tokenization security, loans via partners

Simplicity, strong security, Google ecosystem integration

Security-conscious users, those preferring a clean interface

Rewards for creditworthy users; enables credit usage via UPI.

Affluent credit card users, those wanting to use credit via UPI

Overview of Top UPI Apps in India

An overview of the top UPI apps in India is given below:

1. PhonePe

Launched in 2016, it carries about 600 million users and handled nearly half of the nation’s transactions as of March 2025. The app ticks off more than 330 million payments a day, adding up to over ₹150 lakh crore in a year. PhonePe aims to be a one-stop shop. You can pay bills, recharge your phone, and even jump to other apps such as shopping, food, travel, etc. from the PhonePe app through a feature called PhonePe Switch. Every feature sits behind tight security, with tools like Security shield watching for suspicious activity. Frequent users also rack up cashback and discount rewards, adding a nice bonus to everyday payments.

2. Google Pay

It first showed up in India as Tez before its rebranding for a wider audience. The app now handles a hefty chunk of UPI traffic, roughly 35 to 37% of the market share. Using the app feels nearly effortless due to its clean, minimalist design and robust security. Biometric locks and Google Play Protect offer an enhanced level of security for the users. NFC (near field communication) in GooglePay offers users tap-to-pay, bill payments and voice generated transactions. The app has now expanded to lend personal loans and ticket booking via partnerships. For rewarding the users it uses reward based scratch cards and vouchers for transactions done.

3. Paytm

It began as a mobile wallet but has now emerged as a one-stop digital payment app with a total market share of about 10% to 15%. Paytm combines its wallet with UPI services. Paytm has features like QR payments, ticket bookings, personalized UPI IDs like name@pytes, which helps in ensuring the privacy of your mobile numbers. Safety is maintained by UPI PIN verification and two-factor authentication. Paytm ecosystem includes Paytm Money for investment, Paytm Mall for e-commerce, also it has various services like mutual funds, loans, and even credit cards. Cashback coupons and promo are available round the corner for its wider range of services.

Bharat Interface for Money or BHIM is NPCI’s official UPI app designed for promoting financial inclusion and digital payments in India. It has a multilingual option with over 15 languages inbuilt and is highly optimised for low connectivity areas. Key features of BHIM include “Spend analytics” feature allowing users to track their personal expenses, UPI Lite for small amount transactions without the requirement of PIN. Also it is built to link your credit cards (generally RuPay cards) for hassle free credit card payments.

BHIM is a government supported initiative which serves as the backbone of the UPI ecosystem in India. The main aim is to provide simple, secure and effortless digital payments.

5. Freecharge

It began as a simple prepaid top-up platform and now serves a customer base of 100 million people. Today the app functions as any other UPI application, meaning you can easily send money from your phone in seconds. Freecharge also offers UPI Lite, which lets you pay small amounts even when the connectivity is low, the app also consists of a Credit Line on UPI feature, making merchant payments easier.

The app is supported by Axis Bank and allows you to securely set up your UPI PIN via Aadhaar OTP. Freecharge provides various options for the app users like personal loan, co-branded credit card, or even buy Digital Gold.

6. MobiKwik

It is a “Pocket UPI” app that lets you pay from your wallet balance rather than directly linking your bank account. This allows you to put money directly into your wallet where you can easily monitor your daily expenses.

With Pocket UPI, you can transfer as much as Rs.2,00,000 into your MobiKwik wallet with a daily limit of Rs.1,00,000, making it easier for users to scan a QR and pay instantly. Mobikwik securely detaches your bank account with its secure wallet so that risk of frauds could be evaded. It provides additional services like utility bills, travel booking, recharge etc.

It is for premium class users that have a high credit score, it rewards the credit card payments with “CRED Coin”. CRED UPI helps in linking the users credit cards (especially Rupay) for making UPI payments from one’s credit card directly. CRED also offers “CRED Cash” which allows instant personal loan facility, “CRED Mint” where peers can lend money among themselves.

It is a holistic app that combines UPI and credit card services. Biometric locks and PIN shields your personal data, keeping it secure during transactions.

Advantages of using UPI to make payments are listed below:

Lightning-Fast Payments : The most unique feature of UPI is the instant one click payment helping users with speedy transactions. The money transferred instantly appears in the receiver’s wallet or bank account.

24×7 : UPI has no time restrictions as you can pay anytime, may it be a holiday or non banking hours, as via UPI one has the leverage of making payments 24×7, 7 days a week as compared to primitive money transfer options like NEFT or RTGS.

Super Convenient : UPI apps run smoothly on your smartphone, which means paying for chai, booking a movie ticket, or splitting dinner with classmates can be done in seconds.

Top-Notch Security : People worry about money, and UPI addresses this concern. Every payment is authenticated with UPI PIN before money is sent.

No Need to Share Personal Information : Sharing your bank account details can feel risky. With UPI you simply use your VPA ID or even your mobile number to receive money.

Mostly Free (for Users) : Most of the time, sending cash via UPI costs you nothing, which is a nice perk for students living on pocket money. Most people who send money directly from one bank to another using UPI find the transfer costs zero, but merchants may incur some fees associated for certain types of transactions.

One App, Many Accounts : Switching from one banking app to another for payments might feel irritating sometimes, with most UPI wallets you can stack several accounts into one screen and pick your desired bank for different kinds of payments.

Accepted Almost Everywhere : UPI apps have widely grown across the country making it acceptable by everyone, by just scanning the QR code bills or purchases can be dealt instantly even if you are at a chai stall or buying a gadget from an electronics shop.

Various limits concerning UPI are mentioned below:

1. General Daily Limit

If you’re using UPI the usual way, the National Payments Corporation of India (NPCI) lets you send up to ₹1 lakh per day.

2. Bank-Specific Variations

Not every bank has the same rules. Some lenders quietly trim the ceiling to ₹25,000 or ₹50,000. Check your official banking app to know the exact maximum amount allowed.

3. Higher Limits for Specific Categories (NPCI Guidelines)

When money is transferred to purchase stocks, mutual funds, or even insurance premiums, the limit jumps to ₹2 lakh per day. The same ₹2 lakh ceiling also includes EMI collections for NBFCs and foreign inward remittances.

IPOs, RBI Direct Bonds, schools fees, and Hospital payments have a ₹5 lakh per transaction limit.

4. Transaction Count Limit

UPI isn’t just about how much, it’s also about how often. Most apps keep the daily peer-to-peer transaction limit between 10 and 20 transfers a day.

Basic Tips for UPI App Security

If you want to use UPI in a secure manner, then it is advised that you follow the below tips:

Keep Your UPI PIN Secret : UPI pin acts as the main payment authenticator, so never scribble it on a sticky note or share it with someone.

Double-Check the Payee details : Before proceeding with payments, slow down and look at the name and UPI ID correctly. A tiny typo could send cash to a different account incurring loss.

Beware of Unknown payment request : If a payment request pops up from someone you don’t recognize, hit decline without hesitation.

Don’t scan unknown QR codes : A square barcode can be both a shortcut and a trap. Skip scanning any QR code other than where you need to pay.

Stick to official and updated apps : Apps are powerful, but fraudulent apps can carry viruses. Download your preferred UPI app only from the Play Store or Apple’s App Store.

Layer on Extra Security : Keep your smartphone secure using a pin, app lock, fingerprint scan, or face ID to prevent unauthorized access.

Skip Public Wi-Fi : A private home network or using your mobile data to make payments is safer.

Dispute Resolution : If a payment is mistakenly done to a different account, tap into the transaction history to dispute it right away. You can also call your app’s customer support or dial NPCIs helpline (1800-120-1740) for resolution.

Conclusion

Unified Payment Interface (UPI) has transformed the Indian money transfer ecosystem, with a highly secure, fast, and convenient digital transaction system. With evidently massive online transactions and wider acceptance UPI is taking over the traditional payment methods. Features like UPI lite, ticket booking, UPI’s inbuilt credit services are indicating the ongoing innovation. UPI’s adaptability and reliability among the users making it the next big thing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

No worries, your money is safe with the bank and you try making the payment after some time.

Can multiple bank accounts be linked to one UPI App?

Yes, majorly all the UPI apps can integrate multiple bank accounts in one application and you can even select the bank which you want to use for your next payment.

Can UPI be used for international payments as well?

UPI is prominently used in India only. However, NPCI recently launched UPI Global Acceptance, a feature that enables users to make QR-based payments at select international merchant locations.

What is UPI lite and when shall it be used?

UPI lite is a type of a wallet, in which small payments are done without the requirement of the PIN.

How to judge which UPI app is the best?

It depends upon the app’s interface and services offered. For a clean interface and easy to use application one shall consider GooglePay, Phonepe for multiple bill payment options, CRED for credit services.

Have you ever had trouble understanding the difference between gross margin and net margin? While they may sound alike, these two financial metrics serve distinct purposes and provide different insights into a business’s profitability.

In this blog, we will understand in simple language what is net margin, what is gross margin, and why it is important for every business to know the difference between gross margin and net margin.

What is Gross Margin?

Gross margin is an important financial metric that shows how much profit your company makes by selling its products or services, after deducting direct costs (COGS – Cost of Goods Sold) as a percentage of the total revenues. This margin shows only the profit that comes directly from the sale of the product, all other expenses (such as salary, rent, tax etc.) are not included in it. Gross margin helps in understanding how much profit a product or service is generating and whether the decisions related to pricing or production are correct or not.

Gross Margin Formula:

Gross Margin (%) = [(Total Revenue – Cost of Goods Sold) ÷ Total Revenue] × 100

Example : Suppose your company made sales of ₹10,00,000 and the total cost of manufacturing and selling the products (COGS) was ₹6,00,000.

This means that for every ₹100 sold, you are left with ₹40 as gross profit.

What all is included in COGS?

COGS i.e. Cost of Goods Sold includes all the direct expenses that are required to manufacture a product or provide a service:

Raw Materials

Direct Labor Costs

Manufacturing Costs (Factory Overheads)

Packaging and Shipping Costs (if it is related to product delivery)

The lower the COGS, the better the gross margin.

What is the role of Gross Margin in business?

In deciding the pricing strategy : If the gross margin is low, then either you have to increase the price or reduce the cost.

In understanding product performance : By determining products with high gross margins, you can focus more on it.

Help in Inventory Management : You can optimize your inventory on the basis of COGS.

What is Net Margin?

Net margin is a financial metric that shows how much profit your company has earned after subtracting all expenses from total sales as a percentage of total sales. This includes not only product-related costs (COGS) but also operating expenses, marketing, interest, taxes and all other costs.

Net margin is often called the bottom line, because it comes at the end of the report and reflects the overall profitability of the company.

Net Margin Formula :

Net Margin (%) = (Net Profit ÷ Total Revenue) × 100

Example : Suppose the total sales of your company is ₹10,00,000. Out of this, the total expenses including cost of products, operating expenses, salary, rent, interest and tax is ₹9,00,000.

So Net Profit = ₹10,00,000 – ₹9,00,000 = ₹1,00,000

Both gross margin and net margin are important but they are used in different situations. It is wise to use the right metric at the right time.

1. If you are a product manager or sales head

Gross margin is the most important tool for you. Because it shows how much profit is left after making and selling a product. This metric plays a direct role in pricing strategy, discount planning, and supplier negotiation.

Example: If a T-shirt has a gross margin of 60% and another has 30%, then you can immediately understand which product to promote.

2. If you are a business owner or investor

Net margin should be the main metric you look at. It tells how much net profit the entire business has earned, that is, what is the actual return on your investment.

Example: A company with a gross margin of 70% but a net margin of only 5% means that operating expenses or taxes are very high, which can be a red flag in the long term.

Case study: The truth about a D2C brand

A small D2C clothing brand was selling T-shirts for ₹1,000 through Facebook Ads. Their gross margin was 50%, that is, a profit of ₹500. But when ad spend, packaging, returns, and customer service were added the net margin was -10%, that is, signifying an overall loss.

Why Both Margins Matter in Financial Analysis?

It is beneficial to understand gross margin vs net margin separately, but when you analyze both together, then the real health of your business comes to the fore. They do not just tell the profit figure, but tell where the money is coming from and where it is going.

The whole story of profitability : Gross margin shows how much basic earnings are being made on your products or services – that is, how much is left after deducting direct cost. On the other hand, net margin focuses on overall profitability – it also includes all expenses like salaries, rent, tax and interest. If you focus only on gross margin, then it is possible that there is a loss in net and you do not even know.

Deep understanding of expenses : If the gross margin of a company is good but the net margin is weak, then it means indirect expenses can be significant. These are signals that you need to optimize your expenses.

Long-term growth and investor confidence : Net margin tells how sustainable a company is in the long term. Companies with high net margins are not only stable, but investors are also more interested in them because they are considered to be efficient overall.

Both metrics are important for better decisions : Whether you are running a startup or working in an established business – looking at both margins together makes your decision-making smarter. This helps you know which area needs improvement – product pricing, cost control or operations.

Limitations of Gross and Net Margin

Gross margin and net margin help you understand your profitability, but both these metrics have their own limitations. Relying only on these figures and judging the financial health of the entire company can sometimes be misleading.

Just numbers, do not tell the reason : Gross or net margin do not tell why there is income or loss.

Interpretation varies according to the industry : Margin expectations can differ widely across industries. Service-based companies often have higher margins because they usually incur lower overhead and production costs. In contrast, manufacturing businesses typically face higher expenses for materials, labor, and equipment, which can lead to lower profit margins.

One-time expenses/earnings are also included : If any exceptional income or heavy expenditure has happened for one time in the net margin, then it can distort the margin.

The effect of management decisions is not visible immediately : The effect of cost-cutting or growth strategy takes time to reflect in margins.

Many investors make some basic mistakes while interpreting financial data. These mistakes can affect profitability in the long run:

Considering Gross margin and Net margin as the same : The biggest mistake is not understanding the difference between these two margins. Many people think that if the gross margin is good, then the business is profitable. Whereas the difference between gross margin and net margin shows that gross margin is just the production related expenses, but net margin shows the true picture of the entire operation.

Estimating profit by looking at gross margin only : Gross margin may look good, but if operating and indirect expenses are high, then net margin can be very low or negative. This can hide the real profitability of the company.

Relying on only one metric : To understand profitability, it is important to analyze not just gross or net margin, but both together. This reveals both the strengths and weaknesses of the business.

Conclusion

Both gross margin and net margin are important financial metrics for understanding the profitability of a business. But they serve different purposes: gross margin gives you an idea of efficiency of a company’s core operations, while net margin shows the financial health of the entire company. A smart business leader analyzes both of them together to make accurate business decisions. If you learn to read and analyze margins of the companies correctly, then you can make informed investment decisions.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

With inflation on the rise and job stability becoming increasingly uncertain, building passive income streams has become more essential than ever. Whether you’re a working professional, student, or homemaker, having an additional income source can offer financial security and peace of mind.

In this blog, we will talk about 50 best passive income ideas in India, which you can easily start in 2025. From digital ventures to investment-based earnings and physical assets, these ideas cater to different needs, time commitments, and capital levels, so you can find what suits you best.

What is Passive Income?

Passive income is income that comes in continuously after the initial setup effort like rent from a property or returns from a mutual fund. But it’s important to understand that no income stream can be 100% passive. Every income source takes time, effort or money to set up. This is not a get-rich-quick scheme. Most passive income sources fall into three categories:

Asset-based: like real estate, mutual funds

Content-based: like blogging, YouTube

System-based: like affiliate funnels or automated tools

With the right perspective, the benefits of passive income can be realized in the long term.

50 Passive Income Ideas in India

S.No

Passive Income Idea

Description

1

Stock Market Investing

Invest in long-term stocks for dividends and capital appreciation.

2

Mutual Fund Distributor

Become a certified mutual fund distributor and earn commissions.

3

Real Estate Rental

Rent out property for steady monthly income.

4

REITs (Real Estate Investment Trusts)

Invest in property via REITs and earn dividends.

5

Digital Gold Investment

Hold gold digitally for long-term appreciation.

6

P2P Lending Platforms

Lend on regulated platforms and earn interest.

7

Dividend Stocks

Build a portfolio focused on dividend-paying companies.

8

Government Bonds

Invest in RBI/SGB bonds for assured returns.

9

Covered Call Writing

Earn premiums by writing calls on your stocks.

10

Arbitrage Mutual Funds

Exploit market inefficiencies via hybrid funds.

11

High-Interest Digital Savings Accounts

Park idle money in high-interest savings apps.

12

YouTube Channel (Automated)

Create evergreen content and monetize passively.

13

Blogging with Affiliate Links

Write SEO blogs and earn through affiliate sales.

14

eBook Publishing

Self-publish eBooks on Amazon or other platforms.

15

Print-on-Demand Products

Sell custom products via platforms like TeeSpring.

16

Instagram Theme Pages

Grow niche pages and monetize via sponsors.

17

Online Course Sales

Build and sell courses on Skillshare, Udemy etc.

18

Dropshipping Store

Automate sales using third-party fulfillment.

19

Subletting Co-Working Desks

Rent larger spaces and sublet desks to freelancers.

20

Domain Name Flipping

Buy trending domains and sell at a profit.

21

Newsletter Sponsorships

Grow email lists and sell direct ad slots.

22

App-Based Cashback & Referral Income

Use cashback apps for deals & referrals.

23

Voiceover Licensing

Upload voice samples to stock platforms.

24

Stock Photography & Video Licensing

Sell high-quality images/videos on stock sites.

25

NFT Royalties

Earn from resales of your digital art/NFTs.

26

Online Data Set Licensing

Sell curated data sets for AI/ML training.

27

Audiobook Narration & Publishing

Narrate or publish audiobooks on Audible.

28

Create & Sell WordPress Themes

Build themes and sell via marketplaces.

29

SaaS Tools with Freemium Model

Build a simple tool and charge for the premium version.

30

PLR Content Reselling

Repackage and resell private-label content.

31

Voice Cloning Software Licensing

Build voice models and license to creators.

32

Used Book Resale Automation

Set up used book resale via Amazon seller tools.

33

ATM/Vending Machine Hosting (Space Owner)

Lease space to ATM or vending machine companies.

34

Build & Sell Financial Tools

Create and sell Budgeting or SIP calculators or embed them

35

Google News Blog on Finance

Monetization by bringing traffic from realtime finance news

36

Automated Investment Bots

Hands-free investment by investing in robo-advisory bots

37

Personal Finance Podcasts

Sponsorship deals and ad revenues from Spotify or YouTube

38

Budget Tour Planning Portal

Revenue from offering low-budget friendly travel plans

39

Local Business Automation (White-Label SaaS)

Help small businesses automate using SaaS tools

40

Online Ad Space Arbitrage

Buy low CPC traffic, send to high-paying affiliate offers.

41

Rent Out Gaming Consoles

Lease PlayStations, VR gear etc. on hourly basis.

42

Language Translation Assets Licensing

Create language assets and license to edtechs.

43

Sell Website Templates or UI Kits

Upload on ThemeForest or Creative Market.

44

Solar Panel Leasing

Lease your rooftop for commercial solar use.

45

Start a Podcast

Monetize via sponsorships, premium episodes

46

Sell Canva Templates

Earn by selling ready-made design templates.

47

Social Media Influencer

Build a niche audience and earn brand income.

48

Online Coaching or Consulting

Increase reach through selling record sessions as courses

49

Rent Out Your Vehicle

Give cars or bikes on lease to gig workers.

50

Rent Out Mini Warehouse

Let others use your storage space.

1. Stock Market Investing

Investing in the stock market is a popular and long term passive income source. In this, you buy shares of companies and earn from their growth or dividends. You have to understand the financial health of the companies, sector analysis and market trends. There is a possibility of higher returns but the risk is also the same. It is wise to invest in SIP or Bluechip Stocks for the long term.

2. Mutual Fund Distributor

You can earn passive income by becoming a registered mutual fund distributor with AMFI. Once registered, you earn commissions whenever clients invest in mutual fund schemes through you. This income can become recurring as long as clients continue their SIPs. It’s an ideal option for those with a network or basic financial knowledge, and the income grows as your client base expands. SIPs themselves are also great for low-risk, long-term investors seeking wealth creation.

If you have a property, then you can earn stable monthly income by renting it out. This income is stable and inflation-proof. With property management facilities, you can make this income almost passive. Commercial properties can give higher returns than residential ones.

4. Real Estate Investment Trusts (REITs)

REITs are for those who want to invest in real estate without buying a property. These are listed on the stock exchange and you can buy them like shares. They give the rental income from the property to investors in the form of dividends. It is a liquid and low-risk option.

5. Digital Gold Investment

Through digital gold, you can start investing from as little as ₹1 and it is stored in a secure vault in your name. It can be purchased from online platforms like PhonePe, Google Pay etc. Digital gold can be converted into physical gold in the future. It is also liquid and is considered a good option for long term wealth.

6. P2P lending platforms

On P2P (Peer-to-Peer) lending platforms like LenDenClub or Faircent, you can earn interest income by lending. Here you become an investor giving personal or business loans and can get good returns (10-15%). However, this option is a bit risky, so invest only after checking the right platform and credit rating.

7. Dividend stocks

Stocks that pay regular dividends are a good source of passive income. The financial performance of these companies remains stable and they distribute a part of their profits among investors. Dividend income is taxable, but with a good portfolio it can give good returns annually. Companies like HDFC, ITC come in this category.

These instruments issued by the government are considered reliable for fixed interest income. They have very low credit risk and predictable returns. In portfolios where safety and stability are given priority, government bonds prove to be a trusted option.

Passive income can be generated by selling call options on owned stocks in the form of option premium. This method provides steady return with limited downside risk. Combined with disciplined investing and good stock selection, this strategy is a smart way to utilize capital.

These funds capitalise on the price gap between the equity and derivatives markets and offer low-risk returns. With arbitrage opportunities, these funds offer relatively stable and tax-efficient returns, suitable for conservative portfolios.

11. High-Interest Digital Savings Accounts

Operated by neo-banks and fintech platforms, these accounts offer higher interest rates than traditional banks. Features like zero maintenance charges, auto-sweep options and instant liquidity make them a practical way to earn passive returns on idle cash.

12. YouTube Channel (Automated)

Once content is created using AI tools or faceless video formats, a YouTube channel can generate recurring income from advertising, affiliate links and sponsorships. Automated channels with niche-based or evergreen topics can create a strong earning stream over time.

13. Blogging with Affiliate Links

Niche-focused blogs can promote affiliate products through informative content. Commission is generated when purchases are made from the links provided by readers. The flow of passive income from SEO optimized evergreen articles continues for years.

14. eBook Publishing

After launching an eBook on self-publishing platforms like Kindle, one can earn continuous income in the form of royalty. An eBook written for a good quality and targeted audience can sell repeatedly for a long time, especially in popular niches like finance, productivity or education.

15. Print-on-Demand Products

Custom designed T-shirts, mugs, or stationery can be uploaded on POD platforms to sell products without handling inventory. As soon as the order comes, print, pack and delivery happens automatically, due to which passive margin starts being received on every sale.

16. Instagram Theme Pages

By building an audience on pages with specific interest (travel, quotes, fitness), steady income can be generated from sponsored posts and affiliate links. When consistency and engagement rate is better, brands themselves contact for outreach.

17. Online Course Sales

Skill-based or subject-specific courses, once created, can be sold on platforms like Udemy, Teachable or personal websites to create automated income. High-quality content and structured modules for learners keep the course sellable for a long time.

18. Dropshipping Store

An eCommerce model where there is no need to stock products yourself. The supplier directly ships to the customer upon receiving an order. Platforms like Shopify and niche-specific targeting can create a passive income stream without any inventory investment.

19. Subletting Co-Working Desks

Unutilized workspaces or extra desk spaces can be rented out to startups or freelancers on short-term rental to generate recurring income. Location advantage and flexible pricing can ensure steady occupancy and good returns.

20. Domain Name Flipping

High-potential domain names can be bought cheaply and later sold at a premium rate. Domains with brandable, SEO-friendly or trending keywords can prove to be valuable assets for future resale.

21. Newsletter Sponsorships

Niche-specific newsletter audiences can be built to generate recurring income through direct brand sponsorships and affiliate promotions. High open-rate and loyal readership increase monetization potential manifold.

22. App-Based Cashback & Referral Income

Using offers on apps like Cred, Magicpin, Paytm and adding friends through referral links earns passive income in the form of cashback and rewards. This income can be increased with consistent usage and smart referrals.

23. Voiceover Licensing

Posting pre-recorded generic voiceovers (welcome messages, explainer scripts, AI prompts) on licensing platforms and selling licenses repeatedly can earn recurring royalty. Good audio quality and clear articulation make it scalable.

24. Stock Photography & Video Licensing :

Professionally clicked images and short videos are uploaded on sites like Shutterstock or Adobe Stock to generate passive income. Once uploaded, these contents are licensed multiple times and bring recurring revenue.

25. NFT Royalties

Digital art or collectibles are minted as NFTs and set embedded royalties upon resale. The creator receives a percentage royalty each time a secondary sale occurs, creating a long-term passive flow.

26. Online Data Set Licensing

Curated datasets (text, image, audio) can be licensed to AI companies or researchers to generate recurring income. Niche-specific or cleaned datasets attract high-value buyers.

27. Audiobook Narration & Publishing

Self-narrated or recorded audiobooks from professional voice artists can be published on platforms like Audible. Royalties are earned per listen, allowing content to be created once and provide a passive return for years.

28. Create & Sell WordPress Themes

Custom-designed WordPress themes can be sold on marketplaces like ThemeForest to generate recurring income. High-speed, SEO-friendly and niche-specific designs ensure better sales and long-term downloads.

29. SaaS Tools with Freemium Model

A useful SaaS tool (such as invoice generator, SEO checker) can be launched in a freemium structure to generate recurring revenue through paid upgrades. Premium offerings such as automation, team features or API access create a stable income flow.

30. PLR Content Reselling

Ready-made PLR (Private Label Rights) ebooks, videos or courses are rebranded and resold. By selecting a high-converting niche, this can be converted into a passive income source through email funnels or affiliate platforms.

31. Voice Cloning Software Licensing

AI-based voice cloning tools can be developed and offered in a monthly or yearly license model. Their demand is growing rapidly in the media, audiobooks and virtual assistants industries.

32. Used Book Resale Automation

Old or second-hand books can be sourced in bulk and sold on Amazon or Flipkart through resale automation systems. With barcode scanners and listing tools, this becomes a completely systemized passive hustle.

33. ATM/Vending Machine Hosting (Space Owner)

Fixed passive rental income can be earned by renting out empty space in a busy location to ATM or vending machine providers. Long-term lease and maintenance-free setup make it hassle-free.

34. Build & Sell Financial Tools

Excel-based or web-based financial calculators, loan planners or SIP trackers can be developed and sold. Affiliate deals and embedded sales target finance bloggers and YouTubers to generate recurring income.

35. Google News Blog on Finance

Create a Google News-approved finance blog to publish trending news, policy updates and insights. AdSense and sponsorship deals generate a reliable passive revenue stream.

36. Automated Investment Bots

Algorithm-based bots (for equity, crypto or mutual funds) are developed and offered on a subscription or performance fee model. Transparency and risk management maintain trust and customer retention.

37. Personal Finance Podcasts

Launch a weekly podcast on finance-related topics and generate income from sponsorships, affiliate promotions and listener donations. Niche topics (tax saving, credit score, retirement) build audience loyalty.

38. Budget Tour Planning Portal :

Launch a website with curated budget travel plans and DIY itineraries for low-cost travel lovers and generate recurring income from affiliate bookings and consultation fees. Easy to scale with SEO and content marketing.

39. Local Business Automation (White-Label SaaS)

Ready-made automation tools (billing, CRM, SMS alerts) for small businesses can be white-labeled and resold. Local resellers or agencies earn monthly recurring revenue by selling it under their brand.

40. Online Ad Space Arbitrage

Arbitrage income is generated by buying traffic from low-CPC countries and redirecting it to high-paying ad networks. Scalable automation tools and precise targeting make this a strong model for digital revenue.

41. Rent Out Gaming Consoles :

Passive income can be generated by renting out gaming consoles like PlayStation, Xbox on an hourly or daily basis. College hostels, birthday events or local gaming cafes are ideal customers.

42. Language Translation Assets Licensing :

Recurring licensing fees are earned by licensing pre-built glossaries, term-banks and translation memory files to companies or freelance translators. It is highly valued in niche areas like legal, medical and finance.

43. Sell Website Templates or UI Kits

Passive design income is generated by selling pre-designed HTML templates, Figma UI kits or WordPress themes on online marketplaces. niche-specific designs (e.g. SaaS, blogs, portfolios) are high-converting.

44. Solar Panel Leasing

By installing solar panels on unused rooftops, electricity can be leased to nearby businesses or homes. Government subsidies and long-term PPAs (Power Purchase Agreements) make this financially viable.

45. Start a Podcast

Start a topic-specific podcast (e.g. finance, health, productivity) to generate revenue from brand partnerships, affiliate ads, and listener donations. Consistency and niche focus build a loyal audience base.

46. Sell Canva Templates

Customized Canva templates (Instagram posts, resumes, planners) can be sold on platforms like Etsy or Gumroad. One-time effort leads to long-term passive income through downloads.

47. Social Media Influencer

Develop a niche audience (fitness, tech, parenting) and generate income from sponsored posts, affiliate links, and product launches. Authentic engagement and micro-niche targeting help in sustainable growth.

48. Online Coaching or Consulting

Skill-specific coaching (e.g. Excel, digital marketing, stock trading) can be delivered in recorded video format to generate recurring access fees. Lead magnets and email funnels provide consistent client flow.

49. Rent Out Your Vehicle

Passive earning can be earned by renting out a car or two-wheeler on an hourly, daily or subscription basis. Self-drive rental platforms like Zoomcar, Revv, or Drivezy allow vehicle owners to monetize unused vehicles securely. With proper insurance coverage and verified users, this can become a steady, low-effort revenue stream.

50. Rent Out Mini Warehouse

Extra garage or vacant property is rented out to small businesses or urban tenants for storage use. Monthly rent and zero operational involvement make this an ideal passive rental income model.

How to Choose the Right Passive Income Idea for You

Choosing the right passive income source is a smart decision that takes into account several factors:

Time Requirement: For those who have less time, investment-based options (like dividend stocks or government bonds) are more beneficial. If time is available, then one can focus on content creation or creating and selling digital services.

Risk bearing capacity: If you want a secure income, it is better to choose low-risk options. Whereas those who want to earn more will have to focus on high-risk-high-reward options.

Interest and skills: Starting with the field in which you have some knowledge or interest will be easy and sustainable.

Scalability and automation: A passive income source that does not demand substantial effort repeatedly is better.

Tax and legal aspects: The tax regulations governing different passive income sources can different. Decisions should be taken only after understanding this.

There are many smart and scalable ways to earn passive income today; whether it is from the stock market, selling digital products, or owning real assets. Once set up with proper planning and a little hard work, these sources keep generating passive income for a long time. Everyone should choose a passive income idea according to their skills, budget, and time. With gradual growth, this side income can become a strong financial backup. The real key is to move in the right direction while constantly learning.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Have you ever felt confused when the salary credited to your account doesn’t match the amount mentioned in your offer letter? You’re not alone! The large figure you see in your job offer is usually your gross salary, while the actual amount you receive each month, i.e., your net salary is often quite different.

Understanding the difference between gross and net salary is crucial for effective budget planning and tax planning. In this blog, the difference between the two has been explained in simple language with all the calculations involved.

What is the Gross Salary?

Gross salary is the total salary earned by an employee, including all allowances and bonuses before any taxes or other deductions. This is the amount offered by the company, which includes Basic Pay, House Rent Allowance (HRA), Dearness Allowance (DA), Special Allowances, Performance Bonus, etc.

For example, if someone’s gross salary is ₹50,000, it means that the total earnings for the month are ₹50,000, even if the amount received in the account is less than this.

Gross salary is often also linked to CTC (Cost to Company), but CTC may also include some additional benefits like leave encashment, gratuity, reimbursement of medical expenses, etc.

Gross salary in the salary slip is the amount from which subsequent deductions are made, such as PF, professional tax and income tax.

Important points :

Gross Salary = Basic + DA + HRA + Allowances + Bonus

Income tax, PF, and other deductions are deducted from gross salary

Net salary represents the actual amount that is transferred to the bank account every month. It is also called take-home salary. It is slightly less than the gross salary because some necessary deductions are made from it.

For example, if someone’s gross salary is ₹50,000 and a total deduction of ₹8,000 is made from it, then the net salary will be ₹42,000, and this is the amount that comes into the account.

Net salary means the amount left after taking out all the necessary deductions from the gross salary. This salary is one’s actual disposable income, which an employee uses for household expenses, savings and investment.

Important points :

Net salary = Gross salary – All necessary deductions

Represents actual amount transferred to the bank account

Gross Salary vs Net Salary: Key Differences

Point

Gross Salary

Net Salary

Definition

The total salary earned by an employee including all allowances and bonuses, but without any deductions.

The salary that is transferred to the bank account after all the necessary deductions, such as tax, PF, insurance etc. are deducted from gross salary.

Included Components

Basic Salary, HRA, DA, Travel Allowance, Medical/Special Allowance, Bonus/Incentive

Balance amount after deducting professional tax, EPF contribution, income tax (TDS), medical or group insurance deductions etc.

It is important for every employee to have a proper understanding of their salary structure so that it is easy to estimate the in-hand salary and deductions. You can easily calculate your gross and net salary yourself by following the steps given below.

Step 1 : Calculating Gross Salary

Gross salary usually consists of the following components:

Components

Details

Basic Salary

Part of fixed monthly salary

HRA

Rent Allowance (if applicable)

Other Allowances

Travel, Medical, Special Allowance etc.

Performance Bonus

Based on quarterly or annual performance

Formula: Gross Salary = Basic + HRA + Other Allowances + Bonus

Example : If Basic is ₹28,000, HRA is ₹10,000 and other allowances are ₹7,000, then

Gross Salary = ₹45,000

Step 2 : Calculation of Net Salary

Net salary is the amount that is credited to your bank account after all applicable deductions are made from the gross salary.

Deductions that reduce gross salary to net salary typically include:

Deduction Type

Average Rate/Price

EPF(Employees Provident Fund)

12% of (Basic salary + DA)

TDS (Tax Deduction)

As per income tax slab

Professional Tax

This is a state-level tax, which is applicable only in some states. Its amount varies in every state.

Health/Group Insurance

Deduction as per company policy

Formula: Net Salary = Gross Salary – (All valid deductions)

Example: If gross salary is ₹45,000 and total deductions are ₹6,000, then

Net Salary = ₹39,000

Common Salary Slip Terms Explained

There are many terms in the salary slip which have a direct impact on the gross and net salary. All the main terms are explained in simple language below:

CTC (Cost to Company) : CTC (Cost to Company) is the total amount a company spends on an employee in a year. In addition to the gross salary, CTC includes components like the employer’s contribution to PF, gratuity, health insurance, performance bonuses, and other benefits.

Basic Salary : The main part of the salary, on which EPF and many other allowances are based. It is taxable and is usually 35-50% of the gross salary.

HRA (House Rent Allowance) : Rent allowance, which is given to employees living on rent.

DA (Dearness Allowance) : Dearness allowance which is given to the government or some private sector employees to reduce the effect of inflation.

TA (Transport Allowance) : This allowance is given to cover the expenses incurred on travel. To some extent it can also be tax free.

Special Allowance / Other Allowance : These are fixed allowances which are used to cover performance bonus, mobile, fuel, or other expenses. It is usually taxable.

EPF (Employees’ Provident Fund) : A part of the basic salary is deposited in the PF account by both the employee and the company. It is a long term savings scheme.

Professional Tax : It is a tax imposed by the state government in some states. Its amount and rules are different in every state.

TDS (Tax Deducted at Source) : The company deducts direct tax from your salary as per the tax slab fixed by the government and deposits it with the government.

Gratuity : The retirement benefit amount received by the employee after working in a company for more than 5 years. It is a part of CTC, but does not come in the in-hand salary.

LTA (Leave Travel Allowance) : The allowance given for travel expenses. Based on certain conditions, it can be tax free when the employee submits travel receipts.

Bonus / Incentive : This is a performance-based payment, which is added to the salary slip from time to time. Performance bonus inflates gross salary only in the month/quarter of payout; annual CTC already includes the target bonus.

Medical Insurance Premium : If the company provides health insurance, then its premium is also included in the CTC and can sometimes be deducted from the salary.

Conclusion

It is very important for every employee to understand the difference between gross and net salary. Often we get excited after seeing a big amount in the offer letter, but the actual in-hand amount turns out to be less. Therefore, it is important to pay attention not only to the CTC but also to the salary breakup. A clear understanding of your salary structure helps you plan your monthly budget more effectively, make smarter saving and investment decisions, and stay prepared for taxes and other deductions.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Earlier, whenever you went out for shopping or dinner, you probably carried physical cash to make payments. However, with the launch of UPI or Unified Payment System by NPCI (National Payments Corporation of India) in 2016, things have changed drastically. Now, you can make all kinds of payments through your UPI mobile application. But sometimes the payment gets stuck. In that case, the user must know how to file a UPI complaint.

In this blog, we will explain to you how to register a UPI complaint and what details are required to raise a complaint.

What is UPI Payment?

UPI or Unified Payment Interface allows a user to make payments on a real-time basis. This system was developed by the National Payments Corporation of India (NPCI) in 2016. NPCI is regulated by the Reserve Bank of India. This system has changed the landscape of the Indian payment system. One can easily transfer the funds using their mobile 24*7, UPI even works on holidays.

Features of UPI Payment

The key features of UPI are as follows:

Immediate Transfer: One can easily transfer money in real time, which makes UPI a preferred way of making payments today.

Convenient: An individual doesn’t need to worry about carrying physical cash or going through the hassle of finding change, as UPI allows you to transfer the exact amount easily.

Link Multiple Bank Accounts: One can easily link their multiple bank accounts to a single UPI ID.

QR Code: Using UPI allows one to easily transfer money without sharing any bank details. Scanning a QR code, one can instantly transfer the money.

Cost-efficient: UPI transactions are free for most users, especially those involving direct bank-to-bank transfers. However, a 1.1% interchange fee may apply to transactions over ₹2,000 made using Prepaid Payment Instruments (PPIs) such as digital wallets. This fee is paid by the merchant, not the customer.

Secure: The use of two-factor authentication allows you to securely transfer money to other users.

The common issues with the UPI payments are as follows:

Failed Transaction: In a failed transaction, the amount is deducted from the bank of the payer, but it does not get credited to the bank of the receiver. It generally happens because of network errors or server issues.

Payment Decline by Bank: Your payment can be declined by the bank because of several reasons, such as invalid UPI PIN, insufficient balance, etc.

Failed UPI Registration: There are some cases when the user is not able to register themselves on the UPI application, due to inactive SIM, etc.

Daily Limit: UPI generally has a daily transaction limit. If the limit has been exceeded by the user, then further payments cannot be made.

Bank Server: Sometimes the bank server does not respond or faces some issue; during such times, the payments cannot be made.

How to Register a UPI Complaint?

One can easily raise a UPI complaint following the mentioned steps:

UPI Application: The UPI application, which you were using, allows you to file a complaint and report fraud through the in-app complaint or help section.

NPCI Website: Alternatively, you can visit the website of NPCI, and go to the “Dispute Redressal Mechanism” section and file your complaint.

Customer Care: One can reach out to the customer support department of the company offering UPI services via the helpline provided on their website or application.

Bank: The user can also contact their banks regarding the rejection of UPI payment and can file a complaint for the same.

There are a few details that one should keep handy while registering a UPI complaint.

Registered Mobile Number.

Transaction ID or UTR (Unique Transaction Number).

Date and Time of Transaction.

Amount of Transaction.

Details of the beneficiary account to which you were making the payment.

Error message or screenshot.

Having these details handy can make filing a UPI complaint much easier.

Checking Status of UPI Complaint

One can easily track the status of their UPI complaint online by following the steps mentioned below:

NPCI Website: To check the status of a complaint made on the NPCI website, one can click on the tab “Click here to check the complaint status” and choose their product type, bank and enter CRN number.

UPI Application: If the complaint has been made through the UPI application, then one can track the status of their complaint on the help and support section of the UPI application.

Bank: If you have filed a complaint through the bank, then you can visit the branch or call their customer support number and ask them about the status of your complaint.

On a concluding note, UPI, or Unified Payment Interface, has transformed the way people make payments and shop in India. Now you do not need to carry physical cash while travelling; you can just pay or transfer an amount using the UPI application installed on your mobile phone. However, sometimes the users also face minor difficulties, such as payment being deducted but not credited to the receiver’s account, etc. In this case, you do not need to worry and can easily file a complaint through various modes and get a resolution. However, it is advisable to carefully select a reliable UPI application to avoid any fraud.

Frequently Asked Questions (FAQs)

What is the full form of UPI?

UPI refers to Unified Payment Interface, which NPCI launched to digitise the payment ecosystem.

What type of UPI complaint can I raise?

One can raise complaints about money debited from one’s bank account but not credited to the receiver’s account, a failed transaction, a payment made to the wrong person, or an unauthorized transaction.

Where can I file a complaint about UPI payments?

One can file a complaint on the official website of NPCI, the UPI application, and with your bank.

Where can you check the status of a UPI complaint?

The status of the UPI complaint can be checked on the official website of NPCI or the UPI application

Where to escalate the UPI complaint?

The UPI complaint can be escalated to your bank grievance portal, NPCI portal, or the banking ombudsman.

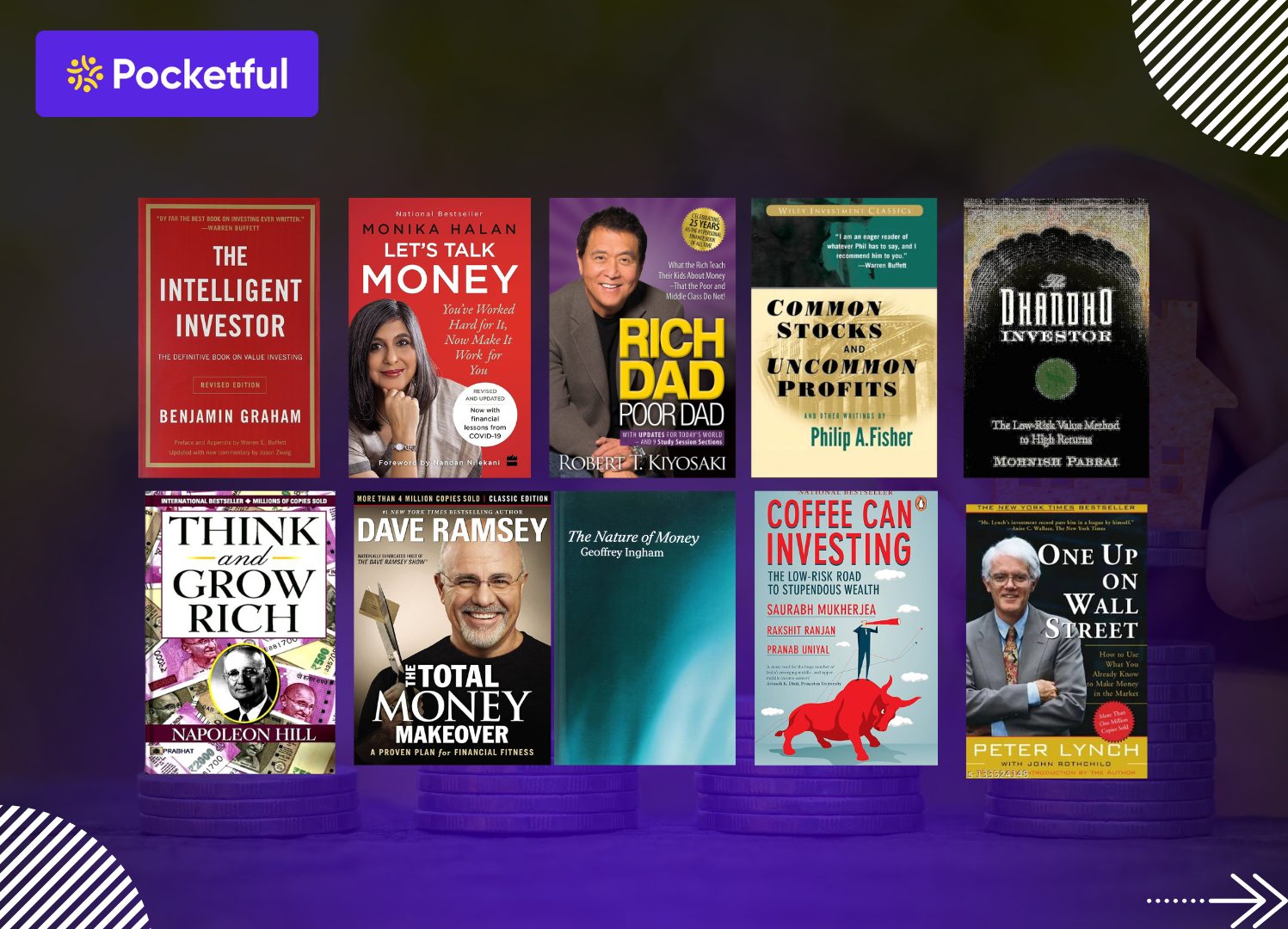

Mastering personal finance is key to building wealth, avoiding debt, and achieving financial freedom. The right books can transform your mindset and guide you toward smarter money decisions. Here, we’ve handpicked the 10 best personal finance books that offer timeless strategies and practical insights to help you take charge of your financial future.

In this blog, we will give you an overview of the top 10 personal finance books.

Top 10 Personal Finance Books

S.No.

Book Name

Year

Author

Rating (Goodreads)

1

The Intelligent Investor

1949

Benjamin Graham

4.3

2

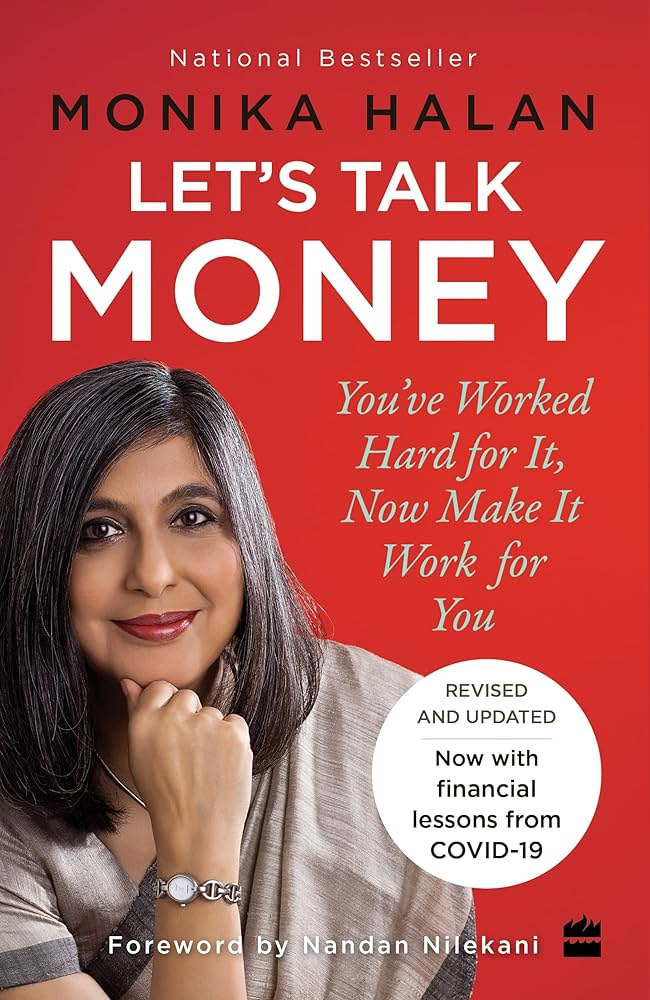

Let’s Talk Money

2018

Monika Halan

4.3

3

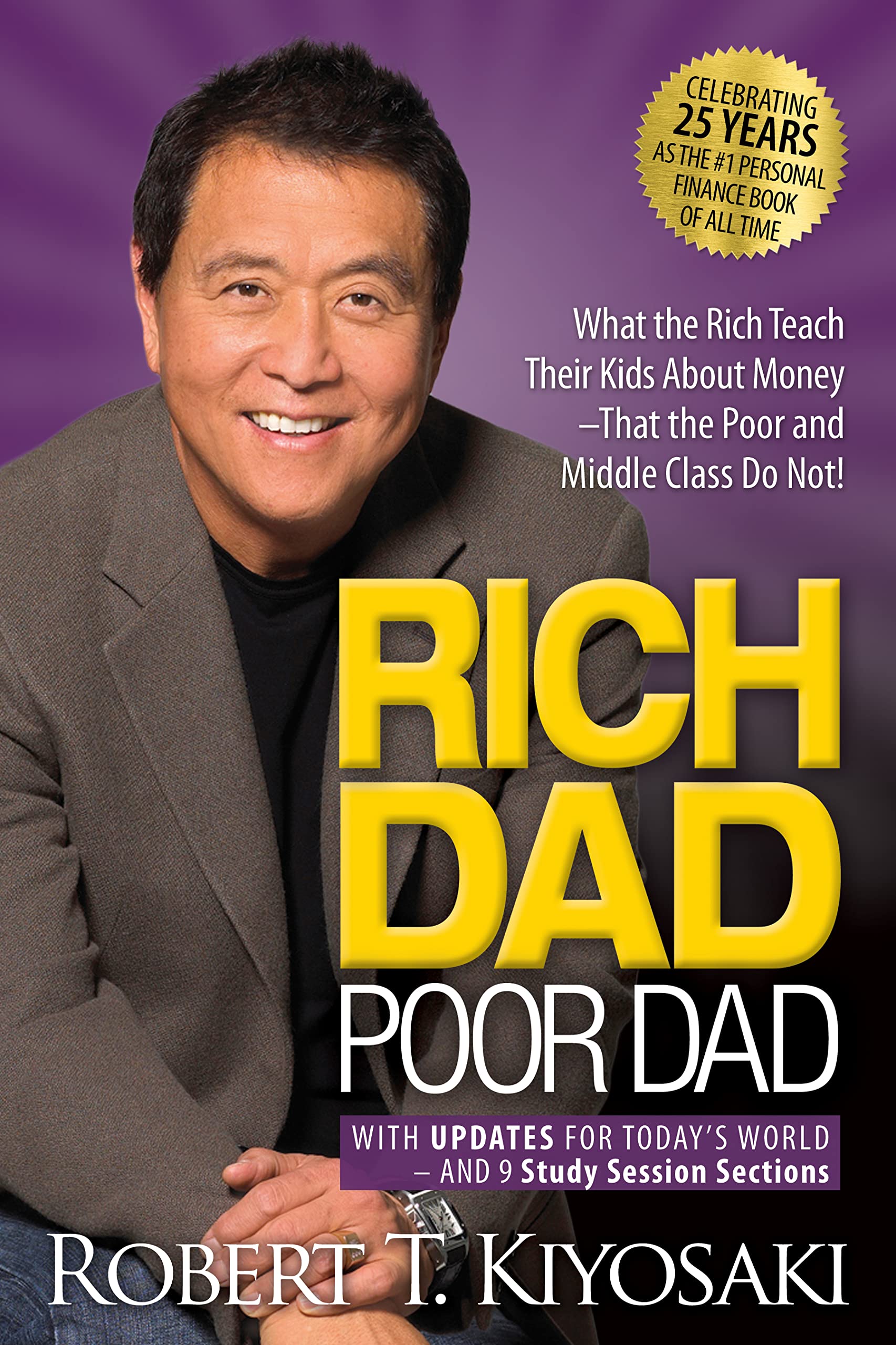

Rich Dad Poor Dad

1997

Robert T. Kiyosaki

4.1

4

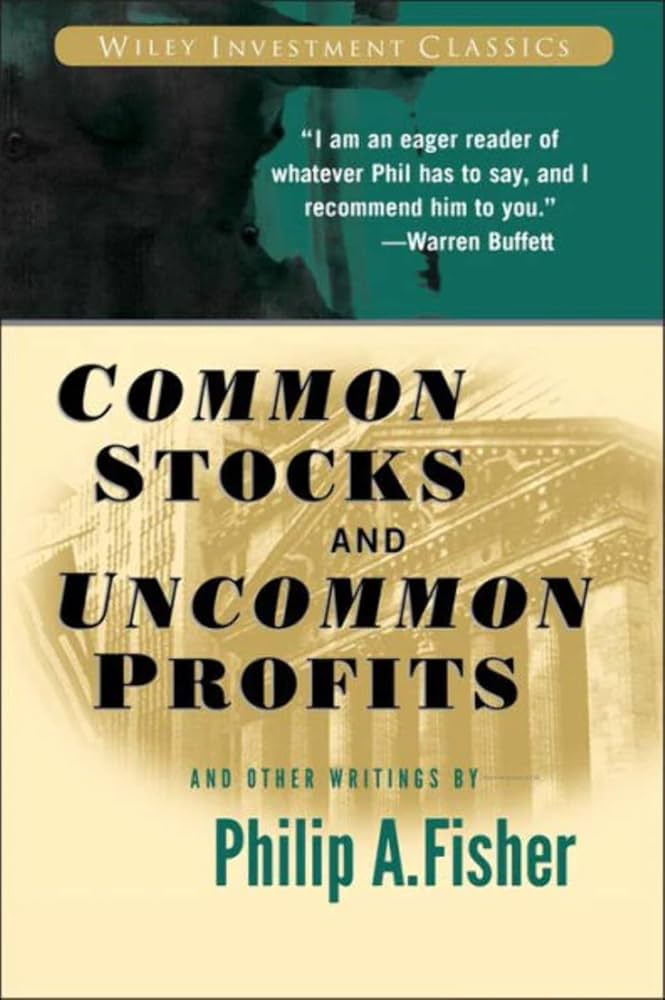

Common Stocks and Uncommon Profits

1958

Philip A. Fisher

4.2

5

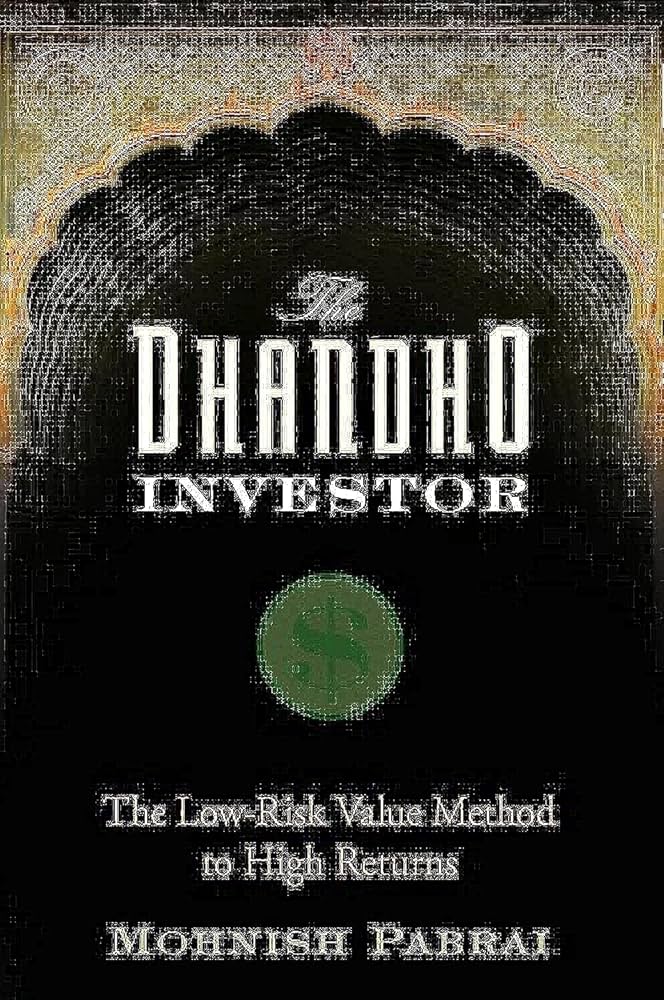

The Dhandho Investor

2007

Mohnish Pabrai

4.3

6

The Nature of Money

2011

Geoffrey Ingham

3.9

7

One Up on Wall Street

1989

Peter Lynch

4.3

8

Think and Grow Rich

1937

Napoleon Hill

4.2

9

Coffee Can Investing

2018

Saurabh Mukherjea

4.2

10

The Total Money Makeover

2003

Dave Ramsey

4.3

Overview of the Top Personal Finance Books

1. The Intelligent Investor

This book was written by Benjamin Graham and was published in 1949. Benjamin Graham is known as the father of value investing. In this book, he explains key characteristics of an investor that separates them from a speculator. The book emphasises long-term investing and suggests that an intelligent investor ignores the mood of the market and only trades when there are favourable prices. He said investing is not a get-rich-quick scheme but a serious business. Considered a must-read by many, The Intelligent Investor remains one of the most influential finance books ever written.

2. Let’s Talk Money

The book was written by Monika Halan, who is a renowned financial journalist. The book is divided into three parts: building the foundation of a financially sound life, creating wealth, and getting wealthy. This book is written in an easy to understand language that can help an individual make informed decisions related to different stages of life. She covers essential topics such as budgeting, emergency funds, insurance, retirement planning, and choosing the right investment products suited to individual goals and risk profiles.

3. Rich Dad Poor Dad

This book was written by Robert T. Kiyosaki and was published in 1997. In this book, the author has explained his life experience of the difference in mindset between his biological father, who was poor and the father of his best friend, who was very rich. Through their contrasting approaches to money, he highlights the difference in mindset between working for money and making money work for you. Kiyosaki encourages readers to break free from the traditional cycle of earning, spending, and saving, and instead focus on building assets that generate passive income. This book emphasises how financial literacy and self-belief help you in creating wealth.

4. Common Stocks and Uncommon Profits

The book was first published in 1958 and was written by Philip A. Fisher. In this book, Fisher focuses on a growth-oriented approach to investing, which was based on qualitative analysis, i.e., analysing company’s management, its capacity for innovation, competitive advantages, and long-term vision. It remains a must-read for anyone interested in growth investing and learning how to identify outstanding companies before they become widely recognized.

5. The Dhandho Investor

The book was written by Mohnish Pabrai, who was the founder of Pabrai Investment Fund. The book was published in 2007. The writer introduces the “Dhandho” approach of investing, which means investing in simple, predictable businesses. According to the book, one should not invest in futuristic ideas; instead, invest in businesses which have a proven track record. The principles of investing discussed in this book are similar to those used by Benjamin Graham and Warren Buffett.

6. The Nature of Money

Written by Geoffrey Ingham and published in 2004, this book offers a unique and thought-provoking perspective on what money truly is. Ingham challenges the traditional economic view of money as merely a neutral medium of exchange. Instead, he explores money as a social construct, emphasizing its role in shaping relationships of credit and debt within society. This book dives deep into the sociology and politics behind money, providing readers with a richer, more nuanced understanding of how modern financial systems operate. It’s an essential read for anyone interested in exploring the foundations of money beyond conventional economic theories.

7. One Up on Wall Street

This book was written by Peter Lynch and published in 1989. Peter Lynch is a successful mutual fund manager. He managed various Fidelity Magellan Funds from 1977 to 1990, and achieved an annualised return of 29%. In this book, he emphasises the importance of daily observation of individual investors, which they can use to find common and promising investment opportunities. Focusing on the principle of “Invest in what you know”, the author believes that anyone can discover great stocks before they’re widely recognized by analysts.

8. Think and Grow Rich

This book was published in 1937 and was written by Napoleon Hill. Based on decades of studying the habits and mindsets of highly successful people, the book is much more than a guide to earning money; it’s a blueprint for achieving success in any area of life. Napoleon interviewed several successful people and found some common characteristics, which are mentioned in the book. Once you finish reading this book, you will get to learn the psychology of creating wealth.

9. Coffee Can Investing

The book was written by Saurabh Mukherjea, Rakshit Ranjan, and Pranab Uniyal, and it was published in 2018. In this book, the authors discusses a long-term approach to wealth creation, especially tailored for Indian investors. The authors introduce the concept of “Coffee Can Investing,” inspired by an old American practice where people would stash valuable possessions in a coffee can and forget about them for years. In investing terms, this means identifying high-quality, fundamentally strong stocks and holding them untouched for at least 10 years.

10. The Total Money Makeover