In the fast-paced world of finance, selecting an investment option can be difficult. Mutual funds, which combine investor funds to invest in a variety of assets, present an attractive option. It is extremely important to maintain investor confidence in the markets and ensure that these funds function responsibly and within the laws. The Securities and Exchange Board of India (SEBI) is responsible for regulating India’s securities market, including mutual funds.

This blog explores SEBI’s important function in overseeing mutual funds, protecting the interests of investors, and promoting a robust investment environment.

SEBI Regulates Mutual Funds in India

Imagine investing your hard-earned money in a mutual fund, only to later discover that it was mismanaged. Therefore, it is important to protect investors and ensure fair and transparent functioning of the industry. The Securities and Exchange Board of India (SEBI) regulates the mutual fund industry in India and performs the following functions:

SEBI establishes rules and regulations to protect the interests of investors.

The regulation aims to restrict fund managers from prioritizing their interests and upholding the integrity of the market.

SEBI regulations are designed to promote the development and expansion of the mutual fund industry.

These regulations can help authorities create and maintain a safe and trustworthy investment environment, promoting investor confidence and stability in the financial markets.

Important Regulations and Guidelines

SEBI has established several guidelines to protect investor interests and maintain transparency. Some of these are listed below:

SEBI issues a comprehensive set of regulations that outlines the framework for establishing, operating, and regulating mutual funds in India.

It outlines the norms for mutual fund advertisements and marketing materials to ensure fairness.

SEBI regulations require mutual funds to disclose their holdings periodically, which enables investors to make informed decisions.

SEBI decides the roles and responsibilities of different entities in a mutual fund, such as sponsors, trustees, AMCs, custodians, and registrar & transfer agents (RTAs).

SEBI requires mutual funds to have a strong system in place for addressing investor grievances and measures to prevent insider trading and fraudulent practices.

SEBI mandates clear and comprehensive disclosures in offer documents and regular reports. This consists of information on investment objectives, fees, risks, and performance.

Role of AMFI

The Association of Mutual Funds (AMFI) is responsible for regulating the mutual fund industry in India under the supervision of SEBI. The key roles of AMFI are listed below:

AMFI focuses on ethical conduct among AMCs and intermediaries, which helps minimize fraudulent activities and ensures fair treatment of investors.

It acts as a bridge between SEBI, the government, and the mutual fund industry.

It facilitates transparency in the mutual fund industry by implementing operational guidelines for all AMCs.

AMFI distributes important information regarding mutual funds on its websites, such as the daily NAV and the performance of all mutual fund schemes.

AMFI issues a unique ARN (AMFI Registration Number) to mutual fund distributors. ARN certifies that the distributor has knowledge of dealing in mutual funds.

It is also involved in making mutual funds popular through mass media.

The year 1963 marked a milestone in the history of mutual funds in India when the Unit Trust of India was established through an Act of Parliament. UTI operated under the regulatory supervision of the Reserve Bank of India.

In 1964, UTI introduced its first mutual fund scheme called “Unit Scheme 1964”. This stage laid the foundation of mutual funds, encouraging retail investors to invest in the stock market.

In 1987, The government permitted the public sector banks, Life Insurance Corporation (LIC), and General Insurance Corporation (GIC) to launch mutual fund schemes.

The arrival of new competitors intensified the competition, and investors had access to various new schemes catering to various risk profiles and financial objectives. The increased complexity resulted in the establishment of SEBI, which started overseeing the mutual fund industry, except UTI, initially.

Structure of Mutual Funds

As per SEBI, the structure of mutual funds in India is three-tiered and consists of the following entities:

Sponsor: The sponsor is the initial promoter of the mutual fund. They establish the trust and appoint a trustee and an asset management company (AMC). Sponsors are usually banks and financial institutions. For example, SBI is the promoter of the SBI mutual fund.

Trust and Trustee: The mutual fund operates as a trust. The trustee is like a legal guardian for the fund’s assets. They make sure that AMC works in the interest of the investors.

Asset Management Company (AMC): AMC manages the mutual fund. They employ fund managers who make investment decisions based on their research and invest money collected from investors into different asset classes.

In addition to the three main tiers, other participants also play a key role in the functioning of the mutual fund.

Custodian: It holds and safeguards the securities of a mutual fund.

Registrar and Transfer Agents (RTA): They keep a record of all investors, manage and provide periodic investment statements, and facilitate transactions such as purchase, and redemption of mutual fund units.

Distributors: They sell mutual fund units to investors. These intermediaries recommend mutual funds to investors and, in return, get commissions from the AMCs.

To wrap it up, SEBI plays an important role in regulating India’s mutual funds. Investor-centric regulations and emphasis on market integrity ensure a fair and transparent investment environment that benefits investors. Understanding SEBI’s functions and guidelines will empower investors to make better decisions and navigate the mutual fund landscape easily.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Batteries have become indispensable for powering our daily lives and providing energy for a wide range of devices and applications. Whether it is our mobile, laptops, or renewable energy systems, batteries play an important role in keeping our world connected. India’s growing economy and focus on clean energy are driving the growth of the battery industry.

In today’s blog, we will explore the best battery companies in India, the products they offer and the future of the industry.

Overview of the Battery Industry in India

The Indian battery market is currently valued at approximately USD 7.2 billion, and it is poised to soar to USD 15.65 billion by 2029, with a remarkable CAGR of 16.80%. The government is focused on developing a domestic manufacturing ecosystem with programs like the Production-Linked Incentive (PLI) scheme.

Additionally, the National Program on Advanced Chemistry Cell (ACC) Battery Storage aims to incentivize the establishment of advanced battery production facilities, with a budget of INR 18,100 crore.

Top Battery Stocks Based on the Market Capitalisation

Best Battery Stocks in India 2026 Based on Market Capitalization – An Overview

The best battery stocks in India are given below, along with a brief overview:

1. Exide Industries Ltd.

Exide Industries is a household name in India that has been synonymous with dependable batteries for many years. The company’s primary focus is on manufacturing storage batteries and allied products in India.

Exide Industries Ltd. has a long history that started in the 1880s when W.W. Gibbs, an executive at a gas company, started the Electric Storage Battery Company, which later became Exide Technologies. He bought the patents for Clement Payen, an innovative French inventor who made significant advancements in electrical storage. This was the starting point for Gibbs as he began turning those ideas into reliable commercial products.

Exide Industries’ core business lies in the manufacturing and selling storage batteries. Lead-acid batteries are dominant in their product portfolio, catering to 2 major segments,

Automotive Division (batteries for 2-wheelers, 4-wheelers, 3-wheelers, e-rickshaws, inverter and UPS for homes and businesses)

Industrial Division (Telecom, Railways, Mines, Specialized batteries for submarines)

2. Amara Raja Energy & Mobility Ltd.

Amar Raja Energy and Mobility Limited, formerly known as Amara Raja Batteries, is a major player in India’s battery industry. It was founded in 1985 by Ramachandra N Galla, a first-generation entrepreneur who wanted to empower people through technology. The first manufacturing facility and office were established in the remote area of Andhra Pradesh.

The company began with car batteries and expanded to industrial batteries, lithium-ion technologies, and related products.

The product portfolio of the company is as follows,

Automotive batteries for passenger vehicles, commercial vehicles, farm vehicles, etc.

Industrial batteries for UPS, telecom, railways, solar applications etc.

Amara Raja has established a strong presence in the overseas market owing to our excellent quality and performance.

3. HBL Engineering Ltd.

HBL Engineering Ltd is a prominent company in the Indian battery industry and is known for its diverse range of battery products and power electronics solutions. The company was founded in 1977 with a focus on lead-acid batteries.

HBL Engineering Ltd division is the main source of revenue, contributing 70-75% of the company’s total sales and fueling its growth. The batteries are used in several industries such as telecom, railways, aviation, oil and gas, and defense. The company’s battery product line includes lead-acid batteries, nickel-cadmium batteries, lithium batteries, etc.

The company holds a global presence in North America and Australia. Furthermore, GULF BATTERIES COMPANY LLC is a joint venture collaboration of HBL Engineering Ltd. It was formed in 2009 in the Eastern province of the Kingdom of Saudi Arabia to manufacture specialized batteries.

4. Eveready Industries Ltd.

National Carbon (India) Limited started importing Eveready batteries in 1905. Eveready Industries India Ltd. (EIIL) was incorporated in 1934, and it established its state-of-the-art battery manufacturing plant in Kolkata in 1940. In 1941, Union Batteries was merged with Eveready and the name was changed to National Carbon Company (India) Limited. In 1958, EIIL established a torch factory in Lucknow, which is now one of the biggest in Southeast Asia. In 1958, the company started selling flashlights to its customers, which was a huge success. In 1995, the name of the company was changed to Eveready Industries India Ltd. and came with the famous slogan “Give me Red”.

The company focuses on offering high-quality products that are reliable and long-lasting. The product portfolio of Eveready is as follows,

Batteries – Zinc carbon batteries for toys, remote controls, flashlights, and alkaline batteries for electronic gadgets.

Lighting – Consumer and professional lighting solutions

Electrical accessories – Extension reels, surge protectors, multi plugs, etc.

Also, they are a market leader in flashlights. The company has a well-established distribution network, fulfilling the needs of a broad customer base.

5. Indo National Limited

Indo National Limited (INL), the company that makes Nippo Batteries, has been a big part of the Indian battery industry for more than 50 years. It was founded in 1972 by P. Obul Reddy with a vision to provide reliable and affordable batteries to the Indian market. Indo National collaborated with Matsushita Electric Industrial Co. Ltd. (now Panasonic) of Japan to produce Nippo batteries. This partnership brought new technology and knowledge to the Indian market.

Indo National is India’s first dry cell battery company to achieve ISO 9001 and ISO 14001 international standards, demonstrating a firm dedication and environmental responsibility.

The company’s core business involves offering dry cell batteries catering to household and commercial applications and to complement their core business, Indo National has expanded into flashlights, LED lighting products, etc.

Key Performance Indicators of Battery Stocks

Company

ROE (%)

ROCE (%)

Debt-to-equity

P/E

P/B

Exide Industries Ltd.

6.80

9.82

0.05

52.21

3.57

Amara Raja Energy & Mobility Ltd.

13.74

17.71

0.01

31.9

4.24

HBL Engineering Ltd.

23.01

31.80

0.05

64.02

14.73

Eveready Industries India Ltd.

17.26

20.22

0.74

44.5

7.68

Indo National Ltd.

4.07

9.08

0.59

44.79

1.83

(all the above data is of year ended March 2025)

Benefits of Investing in Battery Stocks

The benefits of investing in battery stocks are:

High demand: The demand for batteries is set to rise in future due to increased usage of electric vehicles and consumer electronics

Multiple sources of revenue: Batteries are used in various industries such as automotive, industrial, solar, defense, etc.

Government support: The Government of India aims to make India a battery manufacturing hub through Production-Linked Incentive (PLI) schemes. Additionally, a budget of INR 18,100 crore has been allocated to develop advanced battery facilities in India.

Factors to Consider Before Investing in Battery Stocks

Some key factors to consider before you invest in battery stocks are as follows,

Analyze the company’s market share, position within the sector, and target customer segments.

Assess the company’s financial health by examining revenue growth, profitability, debt levels and cash flows. Consider investing in companies with a strong track record and sustainable growth plans.

The battery industry is getting more competitive. Find companies with a strong brand, unique product offerings, and a clear advantage.

Future of Battery Stocks

A 2023 report by McKinsey & Co. states that the global battery demand is expected to jump from 700 GWh in 2022 to a whopping 4.7 TWh by 2030. India is working to become a leader in the battery industry. As part of this, India is focusing on improving battery production to meet the growing needs of the sector. Also, the industry is still at its initial stage, and a strong push from the government is necessary for domestic battery production.

The Indian battery sector is on the brink of remarkable growth, fuelled by the EV revolution, government initiatives, and the increasing demand for consumer electronics. As the Indian government continues to promote renewable energy and incentives for electric vehicles, the demand for batteries is expected to surge in the coming years. Additionally, the growing adoption of smartphones, laptops, and other consumer electronics further contributes to the positive outlook for the battery industry in India. However, it is advised to consult a financial advisor before making any investment decision.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What is driving the growth of the Indian battery industry?

The EV revolution, government initiatives, and rising consumer demand for electronic devices are the key factors driving the growth of the battery industry.

What are the different types of batteries manufactured in India?

Lead-acid and lithium-ion batteries are the main types of batteries being manufactured in India.

What are the risks of investing in battery stocks?

Risks include market competition, technological changes, regulatory impacts, raw material price fluctuations, supply chain disruptions, etc.

How can I invest in top battery stocks?

Identify the top battery stocks through research and understand the risks involved. Also, battery stocks can be volatile; invest according to your risk tolerance and investment horizon.

Is it a good time to invest in battery stocks?

The industry holds a high growth potential. However, it is essential to carefully analyze the individual companies and risk tolerance before investing.

Selection Methodology and Important Disclaimer

The stocks included in this list are selected primarily on the basis of their market capitalisation, which represents the total market value of a company’s outstanding shares. The companies are arranged in descending order of market capitalisation, with larger companies appearing first, followed by relatively smaller companies. This methodology is intended to provide a structured approach for identifying companies based on their market size and overall presence within a sector.

However, market capitalisation should not be considered the sole factor while evaluating investment opportunities, as it does not guarantee future performance, profitability, or returns. Investors should also assess other important factors such as financial health, business fundamentals, management quality, valuation metrics, industry outlook, and market conditions before making investment decisions.

The information provided is for educational and informational purposes only and should not be construed as investment advice, recommendation, solicitation, or an offer to buy or sell any securities by Pocketful Fintech Capital Private Limited.

Are you thinking about investing in India’s rapidly growing paper sector? The beginning of 2025 has been fantastic for the paper industry, with high demand for both packaging and sustainable paper products.

If you are interested in the paper industry and want to invest a chunk of your capital and diversify your portfolio, this blog will help you explore the top paper stocks in India and will guide you in understanding the market further.

Overview of The Paper Industry

The best paper stocks in India are typically those with long operating histories, strong balance sheets, and consistent capacity expansion. The industry has transformed from traditional mills into modern, technology-driven and eco-friendly operations focused increasingly on packaging and specialty paper. As of 2025, India’s paper and packaging market is valued at over ₹1.5 lakh crore, with packaging paper and board forming the largest share of demand.

Domestic production stands near 24 million tonnes annually, while overall consumption continues to grow at around 6–7% per year. Rising e-commerce, FMCG demand, urbanisation, and sustainability initiatives are driving expansion. Government support for domestic manufacturing and recycling further strengthens long-term sector prospects.

Top Paper Stocks in India Based on Market Capitalization

The best paper stocks based on market capitalization in 2025 are:

The best paper stocks in India are given below, along with a brief overview:

1. JK Papers Ltd.

In 1962, JK Papers Ltd was established as one of the key players in the paper industry in India. The business model of the company ranges from integrated pulp and paper mills to the finer production of paper. The product basket consists of office papers, packaging boards, and coated papers that cater to market segments such as educational publishing, corporate requirements, and packaging. JK Papers Ltd. has been involved in the Agro-Farm Forestry Initiative and has planted 123 crore saplings till now.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

9.03%

-13.31%

140.47%

(Data as of 18 February 2026)

2. West Coast Paper Mills Ltd

Western India Paper Mills Limited, set up in 1955, is a prominent paper manufacturing company in India. The company’s plant in Dandeli, Karnataka, manufactures products, including office, publication, and packaging paper. The company operates according to its guiding principles to promote sustainable, eco-friendly manufacturing and efficient utilization of resources. The company makes a range of high-quality paper products that are used in publishing, packaging, and writing, confirming its presence across an assortment of industrial sectors with a high level of innovation and environmental awareness.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-7.32%

-15.07%

106.71%

(Data as of 18 February 2026)

3. Seshasayee Paper and Boards Ltd.

Seshasayee Paper and Boards Limited (SPB) is a leading paper manufacturer in India that has a portfolio of a wide range of paper products, including printing, writing, and packaging paper. The business model of SPB is based on an emphasis on sustainability, using renewable resources and advanced technology to implement environmentally friendly business practices. The paper manufacturing company caters to industries such as publishing, packaging, and education and is committed to high quality through innovation.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

0.40%

7.45%

89.41%

(Data as of 18 February 2026)

5. Andhra Paper Ltd.

Established in 1964, Andhra Paper Ltd. is a prominent Indian paper producer. The company manufactures several paper types, namely writing, printing, and copier papers. With great emphasis on sustainability, Andhra Paper Ltd. strategically incorporates sustainable practices into its operations. The company has developed a business model grounded in quality and innovation to meet varied customer needs. The company offers different products, including premium printing paper products, specialty paper products, and office documentation solutions.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-11.26%

-21.85%

45.93%

(Data as of 18 February 2026)

6. Tamil Nadu Newsprint and Papers Ltd. (TNPL)

Founded in 1979, Tamil Nadu Newsprint and Papers Ltd. (TNPL) is an initiative of the Government of Tamil Nadu. The company exclusively manufactures eco-friendly paper and utilizes bagasse – a sugarcane byproduct for making the paper. TNPL also manages an integrated pulp and paper mill in Karur and a packaging board plant in Trichy. Considering TNPL’s sustainability model of paper production, they mainly concentrate on research and development of green paper and related products. Their sustainable practices include the production of eco-friendly paper, sustainable packaging boards, and renewable energy solutions.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

1.42%

-37.09%

-37.09%

(Data as of 18 February 2026)

6. Kuantum Papers Ltd.

Kuantum Papers Ltd is an India-based paper manufacturer engaged in producing agro and wood-based writing, printing, copier, and specialty papers. Established in 1980, it operates a fully integrated manufacturing facility in Punjab, combining pulping, paper making, and finishing processes. The company emphasizes sustainable sourcing, energy efficiency, and water conservation while serving domestic and export markets. With a focus on quality, innovation, and operational efficiency, it caters to publishers, corporates, and educational institutions across India and overseas.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-12.96%

-27.54%

73.18%

(Data as of 18 February 2026)

6. Orient Paper & Industries Ltd.

Established in 1939, Orient Paper & Industries Ltd. is a significant player in the Indian paper industry. As it runs an integrated paper mill in Madhya Pradesh, the business has flourished, manufacturing a variety of paper types. The company principally manufactures high-quality writing, printing, and tissue papers. The company’s sustainable model emphasizes eco-friendly practices and consistently provides the benefit of reducing waste. Orient Paper promises to deliver high-quality services and a diverse product line.

Stable Demand: Paper industry products have a constant demand in the market because paper products are required for packaging, printing, and educational purposes.

Sustainability: The inclusion of eco-friendly products has made them sustainable, and investors prefer such companies.

Dividend Payment: Many paper industries have good financial results, which means they pay high dividends.

Pricing Power in Specialty Segments: Companies focused on specialty paper, packaging boards, or premium products often enjoy better pricing power and higher margins compared to commoditized segments.

Factors To Consider Before Investing In Paper Stocks

An investor must consider the following factors before investing in paper stocks:

Market Demand: The outlook of the paper products market needs to be assessed globally. Rapid digitalization can reduce paper usage, which can cause a decline in the stock performance of paper stocks.

Environmental Regulations: Investors must understand the environmental regulations as strict regulations can raise production costs and reduce profitability for the company.

Company Financial Health: One has to look at the financial statements and the profit margins. A strong balance sheet and stable earnings are essential for long-term profitability.

Cyclicality of the Industry: The paper sector is cyclical and linked to economic activity. During slowdowns, demand for packaging and printing paper may weaken, affecting revenue and profitability.

Future Of Paper Industry

The future of the paper industry depends on the following factors:

Sustainability Focus: The paper industry will likely focus more on environmental awareness, including green initiatives such as recycling and sustainable forestry.

Innovative Products: To be more specific, companies are likely to modify the already established methods to manufacture crafting and special papers for different uses.

Emerging Markets: One of the things that you can consider is the fact that the development of certain countries will create a demand for paper for packaging and even for educational purposes.

Technological Advancements: Automation, AI-driven quality control, and energy-efficient production processes are likely to improve productivity, reduce wastage, and enhance margins.

Paper stocks are stocks of companies that manufacture and sell paper products. Some major characteristics of the paper industry are stable demand, sustainable practices, and growth potential. Some of the major advantages of investing in paper stocks are stable dividends, diversification, and inflation hedging. You should consider company fundamentals, market share, and prospects for growth while choosing the best paper stock to invest in. However, it is advised to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Paper stocks represent the shares of the companies engaged in the manufacturing and distribution of paper products all over India.

What are the features of the paper industry in India?

Product diversification, increase in domestic consumption, rising eco-friendliness, and improving operational efficiency.

What are some risks of investing in paper stocks?

Cyclicality in raw material prices, sensitivity to global trends in the economy, and environmental regulations are some risks associated with investing in paper stocks.

What has been the trend of the paper industry in India over the last 5 years?

Growth in India’s paper industry has been steady in the past five years and has been driven by growing demand in the packaging, education, and publishing industries.

What are some of the advantages associated with an investment in paper stocks?

Portfolio diversification, capital appreciation, and dividend yield are some advantages of investing in paper stocks.

Selection Methodology and Important Disclaimer

The stocks included in this list are selected primarily on the basis of their market capitalisation, which represents the total market value of a company’s outstanding shares. The companies are arranged in descending order of market capitalisation, with larger companies appearing first, followed by relatively smaller companies. This methodology is intended to provide a structured approach for identifying companies based on their market size and overall presence within a sector.

However, market capitalisation should not be considered the sole factor while evaluating investment opportunities, as it does not guarantee future performance, profitability, or returns. Investors should also assess other important factors such as financial health, business fundamentals, management quality, valuation metrics, industry outlook, and market conditions before making investment decisions.

The information provided is for educational and informational purposes only and should not be construed as investment advice, recommendation, solicitation, or an offer to buy or sell any securities by Pocketful Fintech Capital Private Limited.

Have you ever thought about what keeps your daily essentials wardrobe all stocked up? The answer lies in the Fast Moving Consumer Goods industry, a dominant force propelling the Indian economy. From the products you use daily to the delicious snacks you munch on, FMCG brands are intricately woven into the fabric of our daily lives. This multi-billion-dollar giant is experiencing explosive growth, particularly in rural India. For investors, identifying the best FMCG stocks in India can open doors to steady returns and portfolio diversification.

Today’s blog will explore some of the top FMCG stocks in India, their offerings, factors that should be considered before investing in FMCG stocks, and what the future holds for the entire FMCG sector.

Overview of the FMCG Industry

The FMCG industry refers to the industry that deals with products that are bought and consumed quickly and are priced relatively low. The FMCG market is valued at $615.87 billion by 2027, with a remarkable annual growth rate of 27.9%. The rapid expansion is fuelled by increased disposable income, particularly in rural regions. Household and personal care products account for a huge 50% of sales. Healthcare accounts for 31-32% of total spending, encompassing products such as OTC medicines and personal hygiene items.

Several factors are driving the growth of the FMCG sector, including the rising disposable income in India. As Indian consumers are earning more, their spending on consumer goods is also increasing. Lifestyle changes are also driving a surge in demand for premium products. Additionally, the rise of e-commerce has brought about a revolution in the way consumers shop. Online platforms offer a vast array of choices and unparalleled convenience, especially in rural areas where access to physical stores may be limited.

Top FMCG Stocks in India Based on Market Capitalization

The FMCG stocks have been listed in descending order based on their market capitalization in the table below:

Company

Market Capitalisation (in INR crore)

Current Market Price(in INR)

52 Weeks High

52 Weeks Low

Hindustan Unilever Ltd.

5,53,329

2,355

2,660

2,044

ITC Ltd.

4,02,501

321

472

318

Nestle India Ltd.

2,50,864

1,301

1,333

1,055

Varun Beverages Ltd.

1,57,212

465

593

419

Godrej Consumer Products Ltd.

1,18,098

1,154

1,309

980

(Data as of 30 January 2026)

Best FMCG Stocks in India 2026 – An Overview

The best FMCG stocks in India are given below, along with a brief overview:

1. Hindustan Unilever Ltd.

Hindustan Unilever was founded in the late 1980s. The Lever brothers, established by William Hesketh Lever, first entered the Indian market in 1888 with a product known as sunlight soap. However, the soap was marked with the phrase “Made in England by Lever Brothers.”

Hindustan Vanaspati Manufacturing Company, Unilever’s first Indian affiliate, was founded in 1931. Lever Brothers India Limited followed in 1933, and United Traders Limited followed in 1935. In 1956, these companies amalgamated to establish Hindustan Unilever Limited. The company’s headquarters is located in Mumbai.

Product Portfolio of the company is as follows,

Home care products – Laundry detergents, fabric conditioners, dishwashing liquids, and toilet cleaners. (Surf Excel, Rin, Wheel).

Personal care products – Soaps, shampoos, skin care products, hair care products, deodorants, oral care products.

Beverages, packaged foods, water purifiers, healthcare products, baby soaps, shampoos, body lotions, cosmetic and beauty products.

1Y Return (%)

3Y Return (%)

5Y Return (%)

-1.11%

-9.34%

4.01%

(Data as of 30 January 2026)

2. Varun Beverages Ltd.

Varun Beverages Limited was established in 1995 by Ravi Jaipuria, the chairman of RJ Corp. The corporation first set up bottling facilities in India for PepsiCo products. Outside of the United States, VBL is the second-biggest PepsiCo beverage bottling company globally. In 2016, the company conducted its first initial public offering (IPO) to raise funds.

The company’s primary activities include bottle manufacture and distribution of PepsiCo’s product line, which includes bottled water, juices, and other non-carbonated drinks and carbonated soft drinks like Pepsi and Mountain Dew. The company and PepsiCo have a franchisee agreement that grants them the authority to manufacture and market PepsiCo beverages within their designated regions.

1Y Return (%)

3Y Return (%)

5Y Return (%)

-14.42%

87.27%

484.33%

(Data as of 30 January 2026)

3. ITC Limited

ITC Limited is an Indian conglomerate headquartered in Kolkata, India. The company has a diversified presence across several industries, such as FMCG, hotels, packaging, etc. The company is considered a major player in the Indian economy and exports its products to over 90 countries, and is known for its commitment.

ITC holds a rich history that traces back to 1910 as the Imperial Tobacco Company of India Limited, a subsidiary of British American Tobacco. The company initially focused on tobacco products and established its first cigarette factory in Bangalore in 1913. The name of ITC was later changed to India Tobacco Company in 1970. The company continues to innovate and expand its FMCG portfolio while focusing on sustainability initiatives.

1Y Return (%)

3Y Return (%)

5Y Return (%)

-25.76%

7.42%

57.43%

(Data as of 30 January 2026)

4. Nestle India Ltd.

Nestle is the world’s largest food and beverage company, with a rich history dating back to the 1980s. Henri Nestle, a German pharmacist, created ‘Farine Lactee’ to reduce the infant mortality rate, and the American Brothers founded the Anglo-Swiss company in 1866 and developed innovative milk products. Both companies succeeded with innovative milk products, targeting the urban population with changing lifestyles. In 1905, a merger formed the Nestle company we know today.

The company focuses on providing nutritious and convenient food and beverage products for customers of different ages and backgrounds. The company’s major products include infant formula, instant coffee, nutritional bars, frozen foods, etc.

1Y Return (%)

3Y Return (%)

5Y Return (%)

18.83%

35.83%

51.23%

(Data as of 30 January 2026)

5. Godrej Consumer Products Ltd.

Godrej Consumer Products Ltd. is a prominent Indian company established in 1897. Ardeshir Godrej started a lock company in 1897, laying the foundation for the Godrej Group for the Godrej Group. The consumer products business became a separate entity in 2001. The company has grown through strategic acquisitions like Keyline Brands (UK) in 2005 and hair care companies in South Africa.

It offers a wide range of good quality and affordable products across home care, personal care, and hair care segments. GPCL mainly generates revenue by selling FMCG products in different categories.

The FMCG stocks have been listed in descending order based on their 1-year returns in the table below:

Company

1-Year Returns

Varun Beverages Ltd.

-28.61%

Colgate Palmolive (India) Ltd.

-23.45%

Mrs Bectors Food Specialities Ltd.

-26.36%

Zydus Wellness Ltd.

19.96%

Bikaji Foods International Ltd.

0.01%

(Data as of 30 January 2026)

Best FMCG Stocks in India 2026 based on 1-Year Return – An Overview

The best FMCG stocks according to 1-year return are given below, along with a brief overview of the services they provide:

1. Colgate Palmolive

Colgate Palmolive, known for toothpaste, has a long and interesting history since the early 19th century. William Colgate started a new business in New York in 1806. In the 1870s, the company introduced its first toothpaste. In 1896, Colgate launched the first toothpaste in a tube. It was merged with Palmolive-Peet in 1928. Today, Colgate-Palmolive is a multinational corporation known for its oral care products.

The company holds some trusted brands like Ajax and Hill’s Science Diet, offering products in oral care, personal care, home care, and pet nutrition. The products are available in over 200 countries. It also invests in research and development to create new products for the ever-changing demands of the consumer. With a presence in over 200 countries, Colgate Palmolive products have become a well-known choice for consumers around the globe.

1Y Return (%)

3Y Return (%)

5Y Return (%)

-23.45%

44.60%

30.54%

(Data as of 30 January 2026)

2. Mrs Bectors Food Specialities Ltd.

Mrs Bectors Food Specialities Ltd In the 1970s, Mrs. Rajni Bector started making homemade treats and established Mrs. Bector’s Foods with her husband’s support. Her incredible baking skills quickly earned her a well-deserved local reputation for crafting mouth-watering homemade treats such as ice creams, puddings, cakes, cookies, and buns. Later, her husband set up a small manufacturing unit, marking the beginning of Mrs. Bector’s Food.

The company manufactures and sells bakery and frozen products like buns, pizzas, kulchas, and cakes to several businesses in India. It also sells products such as ‘Mrs. Bector’s Cremica’ and ‘English Oven’ apart from its domestic biscuits business.

1Y Return (%)

3Y Return (%)

5Y Return (%)

-26.36%

135.90%

198.71%

(Data as of 30 January 2026)

3. Zydus Wellness Ltd.

Zydus Wellness began its operations in 1988 with the introduction of Sugar-Free, India’s first zero-calorie sugar substitute. This marked the beginning of a transformative journey that would position the company as a leader in consumer wellness. Originally operating as Carnation Nutra-Analogue Foods, the company focused on dairy substitutes and margarine products. The turning point came in 2006 when Cadila Healthcare acquired a significant stake in the company. In 2009, Cadila’s consumer goods business merged with Carnation Nutra Foods to create Zydus Wellness.

The company holds a strong portfolio that showcases a robust collection of renowned brands such as Sugar-Free, Glucon-D, Complan, Everyuth, and Nycil. These brands have cultivated a profound sense of trust and loyalty among customers.

1Y Return (%)

3Y Return (%)

5Y Return (%)

19.96%

51.61%

14.01%

(Data as of 30 January 2026)

4. Bikaji Foods International Ltd.

The history of Bikaji Foods International can be traced back to the late 1980s. It was founded by Shivratan Agarwal. The company was originally named Shivdeep Industries Limited, which was incorporated in 1986. It subsequently changed its name to Bikaji Foods International in 2016.

Bikaji Foods International Limited is a major Indian snack food company and one of the largest fast-moving consumer goods (FMCG) brands in India. The company manufactures a wide variety of snacks across various categories. Bikaji is the third largest ethnic snacks company in India and the largest manufacturer of Bikaneri Bhujia. Their products are popular in India and are exported to over 25 countries, including North America, Asia Pacific, the Middle East, the European Union, Africa, and the United Kingdom.

1Y Return (%)

3Y Return (%)

5Y Return (%)

0.01%

62.27%

104.72%

(Data as of 30 January 2026)

Note: The overview of Varun Beverages Ltd. is in the overview section of FMCG companies based on market capitalization.

FMCG stocks provide portfolio diversification as they are stable businesses.

Investors get a consistent dividend income.

These stocks are preferred by investors who don’t want to take excessive risks.

Factors to Consider Before Investing in FMCG Stocks

Investors must consider the following factors before investing in FMCG stocks:

Brand Recognition – Find companies with strong market share and established brands. Recognized brands have loyal customers and can withstand economic downturns.

Product Innovation – Assess the company’s product portfolio to ascertain its level of diversity and innovation. Companies that create and launch new products regularly meet changing preferences and stay ahead.

Profitability – Examine the company’s profit margins and return on equity (ROE). Consistent growth in these areas shows a financially healthy company.

Economic Condition – Consider the overall economic environment. FMCG companies are usually more resilient in economic downturns because consumers still need essential everyday items.

Future of the FMCG Industry

The future of the FMCG industry looks bright due to the following factors:

Rising Disposable Income – Due to rising incomes, especially in developing markets, will lead to higher demand for a variety of consumer goods.

E-commerce Penetration – E-commerce is rapidly growing, which will help FMCG companies increase their customer base and revenues.

Sustainability – Consumers prefer companies that prioritize eco-friendly practices, such as using sustainable packaging and production methods.

Overall, the FMCG sector is poised for growth in the future and is expected to remain a good investment option. However, it is important to analyze the market trends of individual companies before investing your money.

The FMCG sector presents an exciting opportunity marked by consistent growth, strong brand loyalty, and the potential for significant returns. Investors can find good opportunities by evaluating a company’s strengths, financial performance, and industry trends. Do thorough research or seek advice from a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

FMCG stocks are generally considered a defensive investment option because customer’s demand for these goods remains relatively stable even during economic downturns.

What are the risks involved in FMCG stocks?

Factors like rising input costs, intense competition, and changing consumer preferences can affect the performance of these stocks.

How to select FMCG stocks for investing?

When choosing FMCG stocks, you can look for factors like market share, product portfolio, and past financial performance.

Are FMCG stocks good for long-term investment?

Historically, these stocks have delivered consistent returns over the long term, but it is important to do proper research before investing.

Do FMCG stocks provide dividends?

Many FMCG companies have a history of paying regular dividends.

Selection Methodology and Important Disclaimer

The stocks included in this list are selected primarily on the basis of their market capitalisation, which represents the total market value of a company’s outstanding shares. The companies are arranged in descending order of market capitalisation, with larger companies appearing first, followed by relatively smaller companies. This methodology is intended to provide a structured approach for identifying companies based on their market size and overall presence within a sector.

However, market capitalisation should not be considered the sole factor while evaluating investment opportunities, as it does not guarantee future performance, profitability, or returns. Investors should also assess other important factors such as financial health, business fundamentals, management quality, valuation metrics, industry outlook, and market conditions before making investment decisions.

The information provided is for educational and informational purposes only and should not be construed as investment advice, recommendation, solicitation, or an offer to buy or sell any securities by Pocketful Fintech Capital Private Limited.

Indian Railways plays an important role in connecting different parts of the country, facilitating transportation, and contributing to the economic development of the country. It is often regarded as the “Lifeline of the Nation.”

In this blog, we will explore the railway sector and discuss services offered by the top railway companies in India operating in the sector.

The railway sector is considered a monopoly because of the significant entry barriers that make it difficult for other companies to compete. For example, building, running, and maintaining rail services require huge investments. In addition, most railway systems are publicly owned, which further contributes to their monopoly status.

Overview of the Railway Sector in India

The railway industry in India is one of the largest and most complex in the world. It was established more than 150 years ago when the first passenger train in India ran from Mumbai to Thane on April 16, 1853. Over the decades, the network expanded significantly. The economic impact of this sector is huge as it generates employment and revenue, which makes it a significant contributor to the GDP.

Key services provided by the railway sector are:

Passenger Services: Local Trains, Long Distance Trains and Luxury trains

Freight Services: Transportation of commodities like coal, iron ore, cement, grains, etc.

Best Railway Stocks in India 2026 Based on Market Capitalization – An Overview

The best railway stocks in India are given below, along with a brief overview of the services they provide:

1. Indian Railway Finance Corporation (IRFC)

IRFC was incorporated in 1986, and its main business activity is to raise funds from the financial markets to acquire or manufacture assets, which are then leased out to the Indian Railways as a finance lease. It is under the Government of India, and the Ministry of Railways has administrative control over it. It was listed on the stock exchange on 29 January 2021.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-22.43%

432.45%

382.73%

(Data as of 17 February 2025)

2. Rail Vikas Nigam (RVNL)

Rail Vikas Nigam is the construction arm of the Ministry of Railways and is involved in various rail infrastructure projects. It was established in 2003 to meet the rising demand for rail infrastructure. It was listed on the stock exchange on 19 April 2019.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

33.70%

906.19%

1,375.05%

(Data as of 17 February 2025)

3. Indian Railway Catering and Tourism Corporation (IRCTC)

IRCTC was incorporated in 1999 and is one of the most important companies operating in the railways sector. It provides ticketing, catering, and tourism services to its customers. IRCTC was listed on the stock exchange on October 14, 2019.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-23.25%

-13.13%

130.30%

(Data as of 17 February 2025)

4. IRCON International Ltd.

IRCON was incorporated in 1976 and is primarily involved in railway infrastructure projects in India and abroad. In addition to the railway projects, it also builds ports and highways. The company has expertise in completing challenging projects. IRCON won the “Navratna” status in 2023 due to its strategic importance. IRCON was listed on the stock exchange on September 28, 2018.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-32.09%

254.32%

177.36%

(Data as of 17 February 2025)

5. Titagarh Rail Systems Ltd.

Titagarh Rail Systems is a private-sector company that manufactures railway wagons. It was incorporated in 1984 as a rolling stock foundry unit and, in 1997, manufactured its first railway freight wagon. It was formerly known as Titagarh Wagons Limited. Apart from freight coaches, the company also manufactures Metro trains, train electricals, steel castings, etc, for both domestic consumption and export markets.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-24.63%

679.38%

1,444.85%

(Data as of 17 February 2025)

6. BEML Ltd.

BEML, or Bharat Earth Movers Ltd., manufactures heavy machinery used in Indian Railways, defense forces, Metro, and the construction industry. It was established on 11 May 1964 and is headquartered in Bangalore. It has manufacturing facilities in Kolar Gold Fields, Mysore, Pallakad, and Bangalore. The Government of India owns 54.03% of BEML and has plans to divest its stake in the future.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-15.16%

54.11%

186.36%

(Data as of 17 February 2025)

7. RITES

RITES, or Rail India Technical and Economic Service, is a public sector enterprise involved in delivering transport consultancy and engineering services. It was established in 1974 and has its headquarters in Gurgaon, India. RITES is also involved in export activities and has clients in more than 55 countries. In 2023, RITES was given the “Navratna” status by the Ministry of Finance.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-45.79%

59.60%

27.58%

(Data as of 17 February 2025)

Key Performance Indicators of Railway Stocks

Company

Net Profit Margin (%)

ROCE (%)

Debt to Equity

P/E

IRFC

24.06

53.32

8.38

39.08

RVNL

6.71

16.74

0.68

78.64

IRCTC

26.02

45.48

0.00

70.14

IRCON International Ltd

7.16

13.2

0.44

29.60

Titagarh Rail Systems Ltd.

7.49

18.59

0.03

77.20

BEML Ltd.

6.94

11.82

0.02

67.92

RITES

19.96

22.89

0.00

36.51

(all the above data is of the year ended March 2024)

Benefits of Investing in Railway Stocks

Indian railway stocks have been experiencing an upward trend for more than a year due to several factors. Here are some of the key factors:

1. Government focus & Initiatives

Infrastructure Development: The government is investing significantly in railway infrastructure, including modernization, electrification, and the development of high-speed rail corridors.

Dedicated Freight Corridors (DFCs): Progress on the DFC projects aimed at increasing freight capacity and reducing blockages on existing lines.

2. Policy Reforms

Privatization: Initiatives to involve private players in operations and station redevelopment, hence increasing efficiency and quality of services.

Favorable Policies: Reforms and policy changes aimed at improving the operational efficiency and profitability of railway companies.

3. Financial Performance

Strong Earnings: Positive financial results (because of various policy reforms and Government initiatives) from key railway PSUs like IRCTC, IRFC, and RITES.

Cost Management: Effective cost management and reduction in operational expenses have resulted in better profit margins.

4. Increased Demand

Passenger Traffic: Revival in passenger traffic post-pandemic, with increasing demand for travel and tourism.

Freight Services: Growth in freight volumes driven by economic recovery and increased industrial activity.

5. Technological Advancements

Digital Transformation: Implementation of digital services like online ticketing, real-time tracking, and e-commerce integration.

Modernization: Modern technologies in signaling, communication, and rolling stock are adopted to enhance safety and efficiency.

7. Investors Sentiment:

Investor Sentiment: Positive investor sentiment towards infrastructure and transportation sectors, driven by expectations of sustained economic growth.

8. Strategic Partnerships and Expansion

International Ventures: Companies like RITES and IRCON are expanding their business operations internationally, securing contracts and consultancy projects abroad.

Collaborations: Strategic partnerships with global players to enhance technological and operational efficiency.

Factors to consider before investing in Railway Stocks

An investor must consider the following factors before investing in railway stocks:

Type of Competition: Some companies are monopolistic or have a strong market position in their respective niches.

Government policies: Investors must stay updated about recent or upcoming policy changes related to the railway sector.

Investment profile of the sector: Continuous government investment and reforms in the railway sector change the dynamics of the industry.

Economic indicators: Overall economic conditions and their impact on demand for transportation influence the whole sector.

Technological advancements: Adoption of new technologies and modernization efforts makes the sector more accessible and attractive.

Future of the Railway Industry

The railway sector is of strategic importance in the Indian economy, and its future growth depends on the following factors:

Privatization: Initiatives to involve private players in operations, maintenance, and infrastructure development will increase the quality of service.

Sustainability: Focus on green initiatives and sustainable practices.

Technological Advancements: The adoption of cutting-edge technology in operations and customer services will increase the operational efficiency of the companies.

Indian Railways remains a major part of India’s transportation network, with the government’s focus and ongoing efforts to modernize and improve its services to meet future demands. The combination of government support, financial performance, recovery in demand, and positive economic indicators contribute to the price rise of Indian Railway sector companies. Investors are optimistic about the sector’s future growth and profitability potential, making it an attractive investment opportunity. For those considering investing, exploring all railway stocks can provide a comprehensive view of opportunities in this promising sector., but before investing, it’s always advisable to do thorough research or consult with a financial advisor to understand the risks and potential of these stocks.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

An investor must analyze the railway industry as a whole and identify the key challenges. Then, key players should be identified, and a thorough financial analysis should be performed before investing.

What is the recent performance of railway stocks?

Stock prices of companies in the railway sector have increased over the past year due to economic recovery and the government’s focus on this sector.

Why are railway stocks popular among investors?

Railway stocks are popular due to favorable government policies and increased demand for infrastructural growth.

What is one of the risks of investing in railway stocks?

An economic downturn is one of the risks with railway stocks as it will reduce the number of passengers and freight volumes.

Where can I find more information about railway stocks?

It can be found on stock exchanges, company websites, financial news portals, and research reports.

Which railway stock is Penny?

At present however, there aren’t any pure-play railway sector penny stocks in India.

Selection Methodology and Important Disclaimer

The stocks included in this list are selected primarily on the basis of their market capitalisation, which represents the total market value of a company’s outstanding shares. The companies are arranged in descending order of market capitalisation, with larger companies appearing first, followed by relatively smaller companies. This methodology is intended to provide a structured approach for identifying companies based on their market size and overall presence within a sector.

However, market capitalisation should not be considered the sole factor while evaluating investment opportunities, as it does not guarantee future performance, profitability, or returns. Investors should also assess other important factors such as financial health, business fundamentals, management quality, valuation metrics, industry outlook, and market conditions before making investment decisions.

The information provided is for educational and informational purposes only and should not be construed as investment advice, recommendation, solicitation, or an offer to buy or sell any securities by Pocketful Fintech Capital Private Limited.

Volatility is a concept we’ve all encountered. It is a statistical measure of the dispersion from the mean, or to put simply, indicates the tendency to change.

In financial markets, we have Historical Volatility and Implied Volatility. Historical Volatility reflects past price movements, but what exactly is Implied Volatility, and can traders leverage it in trading?

In this blog, we will deep dive into Implied Volatility and explore its use cases in trading.

What is Implied Volatility?

Implied Volatility (IV) is a fundamental concept in options trading and financial analysis, offering a forward-looking perspective on market expectations. It reflects the forecast of future price fluctuations of an underlying asset, derived from the current prices of options.

Key points about Implied Volatility

Unlike historical volatility, which is calculated based on past price movements, IV is forward-looking.

IV is not directly observable but is derived using option pricing models such as the Black-Scholes model.

The formula of IV involves equating the market price of the option to the theoretical price given by the model and solving for volatility.

IV can be influenced by several factors such as market sentiment, economic events, supply & demand, etc.

Traders can use IV in:

Options Trading: Traders use IV to price options. Higher IV leads to higher option premiums because the potential for significant price swings increases the value of the option. Higher IV gives the opportunity to Option sellers (expensive options), and Lower IV gives the opportunity to Option buyers (cheaper options).

Risk Management: By understanding IV, traders can gauge the level of risk and uncertainty in the market.

Did you know?

There is a term ‘Volatility Smile’, which is a pattern observed in the IVs of options across different strike prices. Generally, options that are deep in-the-money (ITM) or out-of-the-money (OTM) have higher IVs than those at-the-money (ATM), forming a curve or “smile” when plotted on a graph.

Factors Affecting IV

Implied Volatility can be influenced by various factors, including market sentiment, upcoming events, and macroeconomic conditions. Traders and investors closely monitor such factors to anticipate changes in IV and adjust their strategies accordingly.

Factors That Cause IV to Rise:

Market Uncertainty: IV tends to rise during periods of market uncertainty or stress. Events like economic downturns, geopolitical tensions, and natural disasters can increase uncertainty, leading to higher IV. For example, during the 2008 financial crisis, IV across many assets spiked due to increased market fear and uncertainty.

Earnings Announcement:IV typically increases before the earnings announcements of companies. Traders anticipate significant price movements based on the results, driving up the IV.

Economic Data Releases: Important economic reports (e.g. GDP data, employment figures) can cause IV to rise as traders anticipate the impact of these data on the markets.

Central Bank Announcements: Announcements or policy changes by central banks, such as interest rate decisions, often lead to higher IV as market anticipates changes in monetary policy. An example is an upcoming RBI meeting with potential interest rate changes.

Corporate Events: Mergers, acquisitions, or other major corporate events can lead to increased IV due to the anticipated impact on the stock’s price.

Factors that cause IV to fall

Resolution of Uncertainty: IV tends to decrease once uncertainty is resolved, such as after earnings announcements, economic data releases, or central bank meetings.

Market Stability: During periods of market stability and lower volatility, IV generally decreases. Stable economic conditions and positive market sentiment contribute to lower IV.

Decreased demand for Options: Lower demand for options can lead to decreased IV. This may happen when market participants expect less volatility or when there is a general lack of interest in options trading. Example – A decrease in trading volume for options on a particular stock can lead to a decline in IV.

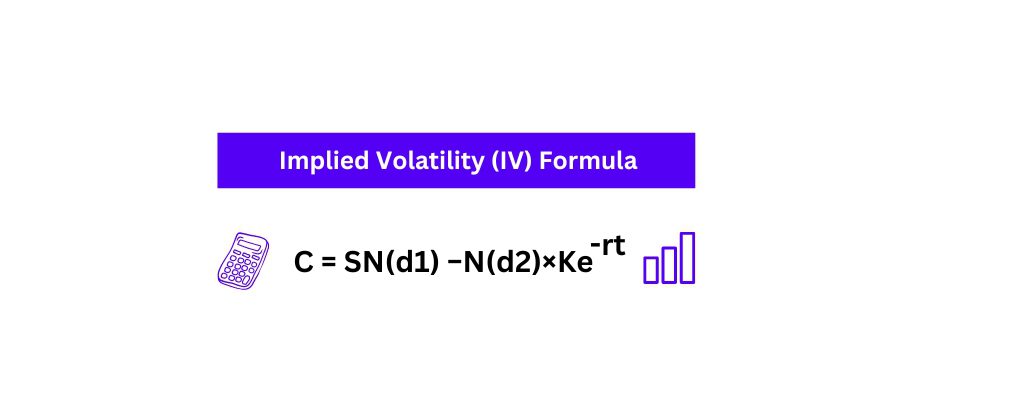

Calculation of Implied Volatility (IV)

Implied volatility (IV) is not calculated using a direct formula but rather derived from an option pricing model. The most commonly used model for this purpose is the Black-Scholes model.

IV is the volatility input in the Black-Scholes formula that equates the theoretical option price to the current market price of the option.

The formula is: C = SN(d1) −N(d2)×Ke-rt

Where:

C is the Call option price.

S is the current stock price or spot price.

N is the normal distribution.

d1 and d2 are probability factors that are used to calculate the value of a call option.

K is the exercise or strike price.

e is the exponential term.

r is the annualized risk-free rate (generally yield of a govt. bond).

t is the time for the option to expire.

Historical Volatility vs. Implied Volatility

Historical Volatility provides a record of past price behavior, while Implied Volatility offers a glimpse into market expectations for the future, making it a critical tool for options traders and risk managers.

Key Differences:

Particulars

Implied Volatility

Historical Volatility

Nature

Forward-looking, based on market expectations.

Backward-looking, based on past price data.

Calculation

Derived from current option prices and models.

Using statistical analysis of historical prices.

Usage

Used to price options, gauge market sentiment, and predict future volatility.

Used to analyze past price movements and assess historical risk.

Interpretation

Represents the market’s forecast of future price fluctuations.

Represents actual past price fluctuations.

Implied Volatility & Vega

Implied Volatility (IV): As we explained above, theIV is the market’s forecast of a likely movement in an asset’s price and is derived from the price of options. It is forward looking and represents the market’s expectations of future volatility.

Vega: Vega is one of the Greeks in options trading, representing the sensitivity of an option’s price to changes in the IV of the underlying asset.

Key points:

Vega measures the rate of change of the option’s value with respect to a 1% change in IV.

It applies to both call and put options.

Generally, Vega is higher for at-the-money options and decreases as options move further in- or out-of-the-money.

Vega is also higher for longer-dated options compared to shorter-dated ones.

Relationship Between Implied Volatility and Vega

Sensitivity: Vega directly measures how sensitive an option’s price is to changes in IV. If Vega is high, a small change in IV will result in a significant change in the option’s price.

Impact of IV Changes: When IV increases, the price of options (both calls and puts) with positive Vega will increase. Conversely, when IV decreases, the prices of options with positive Vega will decrease.

Time to Expiration: Vega is higher for options with longer times to expiration. This is because there is more time for the underlying asset’s price to experience significant volatility.

Moneyness Impact: Vega is maximized when the option is at-the-money (the strike price is close to the current price of the underlying asset).

Implied Volatility (IV) is a crucial concept in the world of options trading. It measures the market’s expectation of volatility and represents the forecast of a likely movement in a security’s price.

Implied Volatility and Vega (Option Greek) are intertwined, as Vega measures how sensitive an option’s price is to changes in IV. This relationship is crucial for options traders to assess and manage the impact of volatility on their positions.

By incorporating IV into trading and risk management strategies, traders can better navigate the complexities of options trading and make informed decisions.

Frequently Asked Questions (FAQs)

What is Implied Volatility?

Implied Volatility (IV) is a metric that reflects the expectations of future volatility of the underlying asset’s price. It indicates the anticipated magnitude of price fluctuations.

Can Implied Volatility (IV) be negative?

No, IV cannot be negative because it represents the market’s expectation of volatility, which is essentially a non-negative value.

How does Implied Volatility change over time?

IV tends to change in response to market conditions, upcoming events, and changes in supply and demand for options. It often increases during periods of market uncertainty or ahead of significant events and decreases when markets are stable.

What is automation in Implied Volatility?

Automation involves using algorithms and software to calculate, monitor, and analyze IV in real-time.

Which automation tools are available for the Implied Volatility?

There are several tools available for automation. Python, with libraries like QuantLib, can be used for options pricing and volatility calculations. For simpler setups, Excel with VBA offers the capability to create dynamic option pricing models. Additionally, dedicated software platforms such as MATLAB, R, and various trading software solutions provide built-in functions for IV calculation and analysis, making them robust options for professionals in the field.

Futures & Options (F&O) trading is no walk in the park—it can take years to become profitable. And with various charges and taxes eating into your profits, it’s a bit of a negative sum game. Now, the Indian government has hiked the Securities Transaction Tax (STT) in the Union budget of 2024-25. But what exactly is STT, and what is the motive behind this increase?

In this blog, we will discuss the changes introduced in the Budget 2024-25 regarding the Securities & Transaction Taxes and explore what it means for traders.

What is Securities Transaction Tax (STT)?

Securities Transaction Tax (STT) is a form of direct tax charged on the buying and selling of securities listed on the stock exchanges, i.e. NSE and BSE in India. It increases the transaction cost for the market participants and reduces overall returns. It was introduced in 2004 by P. Chidambaram, former finance minister. It has the following features:

STT is calculated as a percentage of the transaction value.

The rate is different for different assets.

STT is a source of revenue for the government.

STT is collected by stock exchanges, i.e., NSE and BSE and then subsequently paid to the central government.

Did you know?

In 2013, brokers and trading members protested against the STT, and the government was forced to lower the taxation rate of STT.

Impact of STT

The STT significantly affects investors and traders in the following ways:

Transaction Cost – The imposed STT rate elevates the cost of trading, which ultimately reduces net profit, particularly for active traders who trade frequently.

Liquidity – As the STT increases trading costs and lowers profits, some traders might avoid the market and seek alternative investment options, affecting the overall market volume.

Investment Strategies – Taxes such as STT may influence investment strategies, prompting market participants to favor long-term investments over short-term trades.

Important updates from Budget 2024-25

The Budget 2024 introduced changes in Securities & Transaction Tax rates applicable to the F&O segment. Experts believe that the STT hike aims to discourage retail traders from engaging in speculative activity in the F&O segment. The changes introduced are:

STT applicable on the futures increased from 0.0125% to 0.02%

STT applicable on the options premium increased from 0.0625% to 0.1%

Impact of STT hike on F&O Traders

Let’s understand the impact of change in STT rates on Futures & Options (F&O) trading.

Impact on Futures

Let’s suppose a trader buys 5 lots (1 lot = 25 qty.) of Nifty futures at INR 24,000 and sells it for INR 24,050; then the calculation of STT will be:

As per previous STT rate: The previous STT rate for futures was 0.0125%, which was applicable on the sell side of the transaction. In the above example, the 5 lots of Nifty futures were sold for 24,050, and the STT for this transaction would be:

STT = 0.0125% * 24,050 * 25 * 5 = INR 375.78

As per revised STT rate: The new STT rate for futures is hiked from 0.0125% to 0.02%. Based on the changes introduced in Budget 2024-25, the STT on the transaction would be:

STT = 0.02% * 24,050 * 25 * 5 = INR 601.25

So, the increase in the STT rate has increased the tax liability and decreased the net profit.

Impact on Options

Suppose Nifty is trading at 24,000, and the trader sells 10 lots of call options with a strike price of 24,200 for a premium of INR 60.

– 1 Lot size of Nifty = 25

– Total premium received = 25*10*60 = INR 15,000

For Options, the STT will be calculated as a percentage of the option premium shorted by the trader or the intrinsic value of long options that are exercised. In our example, the trader has initiated a short position, so the calculation of STT is as follows:

As per previous STT rate: The previous STT rate for options was 0.0625%, applicable to the option premium received from the short positions.

STT = 0.0625% * 15,000 = INR 9.375

As per revised STT rate: The new STT rate for options is hiked from 0.0625% to 0.1%. Based on the changes introduced in Budget 2024, the STT would be:

STT = 0.1% * 15,000 = INR 15

From the above case, we can conclude that due to an increase in the STT rate, the trader is liable to pay more in taxes, and thus, returns are reduced.

The Securities and Exchange Board of India regulates the financial markets in India and aims to protect the interests of market participants, i.e. the investors and traders. In recent years, there has been a sharp rise in the participation of retailers in the F&O trading. In Q1 2024, 84% of all equity options traded globally were on Indian exchanges, i.e., the NSE and BSE, up from just 15% a decade ago.

According to a study conducted by the SEBI in 2023, 9 out of 10 retail traders lose money in the F&O trading of equity segment with an average loss of INR 50,000. The worst part is the majority of these losses are incurred by those who cannot afford to lose. Now, the SEBI is worried about this and is looking to curb the speculation activity happening in the F&O segment.

In order to protect retail traders, the SEBI formed an expert panel led by G Padmanabhan, former Reserve Bank of India Executive Director. Some of the measures suggested are:

Proposal to increase the minimum lot size from INR 5 lakh to INR 25 lakh.

Increase in upfront margin requirements.

Increased monitoring of intraday position limits.

Decreasing the number of strike prices for option contracts.

Limiting weekly options to one expiry per exchange per week.

The expert panel has presented the above measures, and the SEBI is quite serious regarding this and may come up with a consultation paper in the coming months.

Securities Transaction Tax (STT) is one of the taxes imposed based on the transaction value of securities. It reduces the net return for the market participants, i.e., Traders and Investors.

In Budget 2024-25, the STT rates for the F&O segment have been increased from 0.0125% to 0.02% for futures and from 0.0625% to 0.1% for options premium. This hike is anticipated to affect market behaviour significantly. Experts suggest that the aim of this increase is to curb speculative trading in the F&O segment.

Frequently Asked Questions (FAQs)

What is STT?

The Securities Transaction Tax (STT) is a form of direct tax charged on the buying and selling of securities. It is levied as a percentage of the transaction value.

What are the changes introduced in Budget 2024-25 related to STT?

The STT was hiked for both futures and options segment. For futures, the STT has been increased from 0.0125% to 0.02%, and for the options premium, the STT has been increased from 0.0625% to 0.1%.

When was STT introduced in India?

In India, the Securities Transaction Tax (STT) was introduced in 2004 by Finance Minister P. Chidambaram.

Why is SEBI worried about rise of retail participation in the F&O segment?

According to a study conducted by the SEBI in 2023, 9 out of 10 individual traders lose money in equity F&O trading, and the concerning part is most of the losses occur by those who can’t afford to lose. This is why the SEBI aims to reduce retail participation in the F&O segment.

Who regulates financial markets in India?

The Securities and Exchange Board of India (SEBI) regulates the financial markets in India.

The Government of India introduced the Union budget for the 2024-25 on July 23, 2024. It was the first budget of the third term of the Modi Government. The budget featured a wide array of changes to achieve economic development targets.

For the middle class, some of the key features of the budget are introduction of new tax slabs under the new regime, hike in the standard deduction limit, etc.

In this blog, we will discuss the changes introduced in Budget 2024 for the general public, i.e., the new tax slabs and standard deduction.

What is Income Tax and the Slab Rates?

Income tax is the direct tax which is imposed on income or profits earned by individuals and corporations. It is a major source of revenue for the government; in fact, almost 19% of the govt. revenue comes from Income tax only in FY 23-24. This 19% covers Corporation Tax (CIT) and Personal Income Tax (PIT) including Securities Transaction Tax (STT).

India has a progressive income tax system, which means people with higher incomes pay more of their income in taxes. Income is divided into different slabs, each with a specific tax rate.

Additionally, India offers two tax regimes: the old tax regime and the new tax regime. The new regime offers a lower tax rate but comes with fewer deductions. An individual can choose the regime that best suits their situation.

In the union budget of 2024-25, the govt. has revised the tax slabs under the new tax regime. Keep in mind that there is no modification in slabs of the old tax regime. Let’s have a look at the existing slabs of new tax regime:

The income tax slab rates for the new tax regime proposed in Budget 2024-25 are:

Income Tax Slab (in INR)

Income Tax Rate (%)

Up to 3,00,000

0

3,00,001 – 7,00,000

5%

7,00,001 – 10,00,000

10%

10,00,001 – 12,00,000

15%

12,00,001 – 15,00,000

20%

15,00,001 and above

30%

Did you know?

Finance Minister Nirmala Sitharaman made history on 23 July 2024, by presenting her seventh consecutive budget—six annual budgets and one interim budget. No other finance minister in India’s history has reached this milestone. This achievement surpasses the previous record held by former Finance Minister Morarji Desai, who presented six budgets in a row.

What is Standard Deduction?

In the Income Tax Act, we have certain exemptions and deductions to reduce our tax liability. Deductions are provisions that allow an individual to reduce his/her income and, thus, reduce the tax liability.

Standard deduction is one of the most popular deductions claimed by individuals. It is a flat deduction that an individual can subtract from the total salary or pension received in a given financial year. Remember that the standard deduction is not available for business income.

An important change regarding the standard deduction under the new tax regime was announced in the Budget 2024-25. The limit was hiked from INR 50,000 to INR 75,000. Similarly, for family pensioners, the deduction has been increased from INR 15,000 to INR 25,000.

Now the main question arrives: how much can an individual actually save because of the above-mentioned changes? Let’s have an analysis on this.

We will calculate the income tax based on the new slab rates and the slab rates prior to the Budget 2024-25. Suppose Raman works in an MNC and earns INR 13,50,000 from salary in a given financial year. Considering he has no other source of income, let’s calculate his tax liability based on existing and revised slab rates of new tax regime:

Based on the existing slab rates (prior to Budget 2024-25)

Salaried Income = INR 13,50,000