Meesho, one of India’s fast-growing e-commerce platforms backed by prominent investors, is launching an initial public offering (IPO) to raise up to ₹5,421.20 crore. The issue opens for subscription on December 3, 2025, and will close on December 5, 2025, with a price band fixed at ₹105 to ₹111 per share. The IPO comprises a fresh share issuance of ₹4,250 crore and an offer-for-sale (OFS) of about ₹1,171.20 crore by existing shareholders. The shares are proposed to be listed on both the Bombay Stock Exchange (BSE) and the National Stock Exchange of India (NSE), with tentative listing scheduled for December 10, 2025, subject to allotment and regulatory approvals.

Meesho,IPO Day 2 Subscription Status

On Day 2, Meesho. IPO witnessed a strong investor turnout, closing with an overall subscription of 8.26 times. The Qualified Institutional Buyers (QIB) category with a robust 7.15 times subscription, indicating solid institutional participation. Among Non-Institutional Investors (NII), the bNII (above ₹10 lakh) portion was subscribed 8.82 times, while the sNII (less than ₹10 lakh) segment saw Robust Leading with 11.20 times subscription, resulting in an overall NII subscription of 9.61 times. The Retail Individual Investors (RII) category was subscribed 9.59 times, reflecting healthy retail interest. Overall, the issue garnered 29,06,810 applications, with total bids amounting to approximately ₹24,633.37 crore, showcasing strong confidence across investor categories in the company’s growth potential.

Investor Category

Subscription (x)

Qualified Institutional Buyers (QIB)

7.15

Non-Institutional Investors (NII)

9.61

bNII (above ₹10 lakh)

8.82

sNII (less than ₹10 lakh)

11.20

Retail Individual Investors (RII)

9.59

Total Subscriptions

8.26

Total Applications: 29,06,810

Total Bid Amount (₹ Crores): 24,633.37

Objective of the Meesho IPO

Meesho plans to utilize the net proceeds from the fresh issue for the following purposes. The proceeds from the Offer for Sale (OFS) will be received by the selling shareholders and not by the company :

Use of IPO Proceeds

Amount (₹ Cr)

Investment in cloud infrastructure (via subsidiary)

1,390

Salaries for AI / ML and technology teams (tech development)

480

Marketing, brand-building and customer acquisition initiatives

1,020

Inorganic growth (acquisitions / strategic initiatives) & general corporate purposes / working capital

1,360

Meesho IPO GMP – Day 2 Update

The grey market premium (GMP) of the Meesho IPO stands at ₹₹44.5 as of December 04, 2025 (Day 2). Considering the upper end of the price band at ₹111 per share, the estimated listing price is around ₹155, reflecting a potential gain of approximately 40.09% per share in the grey market.

Date

GMP

Est. Listing Price

Gain

04-12-2025 (Day 2)

₹44.5

₹155

40.09%

Disclaimer: The above GMP (Grey Market Premium) is just unofficial market information, which is not officially confirmed. These figures are shared for informational purposes only and investment decisions based on these should be based on the investor’s own research and discretion. We do not conduct, recommend or support any kind of transaction in the grey market.

Meesho IPO – Key Details

Particulars

Details

IPO Opening Date

December 03, 2025

IPO Closing Date

December 05, 2025

Issue Price Band

₹105 to ₹111 per share

Total Issue Size

48,83,96,721 shares(aggregating up to ₹5,421.20 Cr)

Meesho is one of India’s fastest-growing e-commerce platforms, designed to make online shopping affordable and accessible while empowering small businesses and home-based entrepreneurs. Operating a zero-commission, asset-light marketplace, it uses advanced AI, analytics, and automation to optimize product discovery, pricing, and logistics. Meesho has built strong penetration across Tier 2 and Tier 3 cities, serving millions of value-seeking consumers and sellers. Its technology-driven model enables low customer acquisition costs, faster deliveries, and scalable operations. As the company continues to expand, it remains focused on sustainable growth, profitability, and strengthening its position in India’s digital commerce ecosystem.

Frequently Asked Questions (FAQs)

What is the opening and closing date of the MeeshoIPO?

Groww IPO is open on December 03, 2025 and will close on December 05, 2025.

What is the price band of the Meesho IPO?

Its price band is fixed from ₹105 to ₹111 per share.

What is the GMP (Grey Market Premium) of the Meesho IPO today?

The GMP on December 04, 2025 is ₹5, which leads to a possible listing price of ₹105.

What is the total issue size of the Meesho IPO?

The total issue size of the MeeshoIPO is ₹5,421.20 crore, structured as a combination of fresh issue and Offer for Sale (OFS) by existing shareholders.

What is the expected listing date of the Meesho IPO?

This IPO is expected to be listed on BSE and NSE on December 10, 2025.

Aequs Ltd’s IPO concluded with a strong overall subscription of 11.40 times. Retail Individual Investors (RII) dominated the demand with an exceptional 34.20 times subscription, followed by the sNII (less than ₹10 lakh) category at 24.05 times. The bNII (above ₹10 lakh) segment also showed heavy interest at 14.14 times, taking the total NII subscription to 17.44 times. The Employees category subscribed 16.04 times, while Qualified Institutional Buyers (QIBs) participated at 0.75 times. The issue received 18,09,025 total applications, with aggregate bids amounting to ₹5,792 crore.

Aequs Ltd. IPO Day 2 Subscription Status

Aequs Ltd’s IPO concluded Day 2 with a steady overall subscription of 1.12 times. The strongest participation came from Qualified Institutional Buyers (QIBs) at 2.04 times, reflecting healthy institutional interest. The Retail Individual Investors (RII) segment was subscribed 0.95 times, indicating near-full demand from retail investors. The Non-Institutional Investors (NII) portion reached 0.41 times, with sNII (below ₹10 lakh) at 0.38 times and bNII (above ₹10 lakh) at 0.44 times.

Investor Category

Subscription (x)

Qualified Institutional Buyers (QIB)

0.75

Non-Institutional Investors (NII)

17.44

bNII (above ₹10 lakh)

14.14

sNII (less than ₹10 lakh)

24.05

Retail Individual Investors (RII)

34.20

Employees

16.04

Total Subscriptions

11.40

Total Applications: 18,09,025

Total Bid Amount (₹ Crores): 5,792

Objective of the Aequs Ltd. IPO

Aequs Ltd. plans to utilize the net proceeds from the fresh issue for the following purposes:

Use of IPO Proceeds

Amount (₹ Cr)

Repayment and/ or prepayment, in full or in part, of certain outstanding borrowings and prepayment penalties

433.17

Funding capital expenditure to be incurred on account of purchase of machinery and equipment by company

8.11

Funding capital expenditure to be incurred on account of purchase of machinery and equipment by one of the wholly-owned Subsidiaries, AeroStructures Manufacturing India Private Limited, through investment in such Subsidiary

55.89

Funding inorganic growth through unidentified acquisitions, other strategic initiatives and general corporate purposes

–

Aequs Ltd. IPO GMP – Day 2 Update

The grey market premium (GMP) of Aequs Ltd. IPO is ₹41, as on 5:00 PM December 04, 2025. The upper limit of the price band is ₹124 and the estimated listing price as per today’s GMP can be ₹41, giving a potential gain of around 33.06% per share.

Date

GMP

Est. Listing Price

Gain

04-12-2025 (DAY 3)

₹41

₹165

33.06%

Disclaimer: The above GMP (Grey Market Premium) is just unofficial market information, which is not officially confirmed. These figures are shared for informational purposes only and investment decisions based on these should be based on the investor’s own research and discretion. We do not conduct, recommend or support any kind of transaction in the grey market.

Aequs Ltd., incorporated in 2000, has evolved into a vertically integrated precision manufacturing company with a strong foundation in the aerospace segment. Operating a dedicated Special Economic Zone, the company delivers end-to-end manufacturing capabilities, producing components for engine systems, landing gear, cargo structures, interiors and complex assemblies. Over time, Aequs has diversified beyond aerospace to include consumer electronics, plastics and consumer durables, broadening its technological footprint. As of September 30, 2025, the company had produced over 5,000 aerospace products across major global aircraft programs such as the A220, A320, B737, A330, A350 and B787. Its product portfolio spans structures, interiors, landing systems and actuation systems, reflecting deep engineering expertise. With a workforce of more than 4,500 employees across various roles, Aequs benefits from an experienced talent pool. Its competitive strengths include advanced precision capabilities, a vertically integrated ecosystem, global manufacturing presence and long-standing partnerships with high-entry-barrier customers. Supported by a founder-led leadership team, Aequs is positioned as a significant player in global precision manufacturing.

Easy Steps to Apply for Tata Capital IPO via Pocketful

The role of investment bankers has evolved significantly in the Indian Capital Market. They play important roles in corporate restructuring, such as mergers and acquisitions, fundraising, etc. However, their role is not limited to providing advisory services to corporations.

In today’s blog post, we will give you an overview of the top investment banks in India.

Overview of Investment Banking

Investment Banks are a special division of every country which helps individuals and especially corporations in raising capital, and other corporate restructuring. They generally act as a mediator between companies that need capital and the investors.

Fundamentals of Investment Banking

The key fundamentals of investment banking are as follows:

Shares – Investment Banking firms help companies raise capital through the issue of shares and also help in buybacks of shares from the public. while offering strategic advisory services for mergers, acquisitions, and restructuring.

Bonds – If a company is looking to raise funds, it can use a debt instrument to raise capital. In it, they generally issue bonds to the public and raise funds from them, and once the purpose is fulfilled, they repay the borrowed amount along with the periodic repayment of interest.

IPO – An Initial Public Offering is a method through which a company goes public for the first time. This whole process involves the various steps in which an investment banking company helps.

Merger and Acquisition – When a company buys another company or merges with another company to strengthen its position in the market.

Overview of Top 10 Investment Banking Companies in India

1. JP Morgan Limited

JP Morgan opened their first office in India in 1945. Initially, it started offering services like mergers and acquisitions, capital raising, etc. Later, the company started dealing in domestic and international transactions related to GDR. The headquarters of the company are situated in Mumbai.

2. Goldman Sachs Limited

As the company has been operating in India since 1980, It established a fully owned on‑shore presence in December 2006, following its termination of a ten-year partnership with Kotak Mahindra. The company has played an important role in major deals such as the acquisition of Essar Steel by Mittal’s and the sale of Flipkart to Walmart. It also helped companies like Reliance Industries and ICICI Bank to raise funds from the public. The company’s head office is situated in Mumbai.

3. Avendus Capital Limited

In 1999, the company was incorporated. Prior to expanding into wealth management, asset management, and credit solutions, the company focused on offering advisory services. Over time, the company has evolved to be an important player in the Indian capital market. The company’s head office is situated in Mumbai.

4. Axis Capital Limited

Established in 2005, Axis Capital is a major investment banking company in India. The company plays a major role in raising funds, mergers and acquisitions, etc. of companies. Over time, it has established itself as a key player in the Indian Investment Banking Industry. The headquarters of the company are situated in Mumbai.

5. Edelweiss Financial Services Limited

Edelweiss Financial Services Limited Rashesh Shah and Venkat Ramaswamy founded the company in 1995. Before expanding into other financial services, the company initially offered investment banking and advisory services. Over the years, it has made significant changes in both the retail and institutional sectors. The company’s head office is situated in Mumbai (Edelweiss House, Kalina).

6. IDBI Capital Limited

Founded in 1993, IDBI Capital Limited is a fully-owned subsidiary of IDBI Bank. Before venturing out into corporate advisory, stockbroking, and financial product distribution, this company initially focused on capital market and investment banking services. Equity and debt placements, mergers and acquisitions advisory, and retail and institutional broking are some of the services provided by IDBI Capital. The company’s head office is situated in Mumbai.

7. SBI Capital Market Limited

SBI Capital Market Limited company was incorporated in 1986. It is a subsidiary of SBI Bank. And it is one of the oldest investment banks in India. The company offers various services to corporations like mergers and acquisitions, debt restructuring, raising funds, etc. Being the leader of the investment banking industry, it has helped many companies in raising funds through IPO. The company’s head office is situated in Mumbai.

8. ICICI Securities Limited

ICICI Securities Limited company was founded in 1995 as an ICICI Bank subsidiary. The services provided by the company include portfolio management, investment banking, retail and institutional broking, etc. It also offers consultancy services to many companies related to mergers and acquisitions, etc. The company’s headquarters is situated in Mumbai.

9. JM Financial

The company was founded in 1973 and is currently one of the largest investment banking companies in India. It helps various companies in raising capital, mergers and acquisitions, etc. Various companies have taken the advisory services from JM Financial to raise capital through IPO. The company’s headquarters is situated in Mumbai.

10. Morgan Stanley Limited

The company was incorporated in NewYork, but it has been operating in India since 1998 and has become a key player in the Indian Capital Market. The services offered by Morgan Stanley include mergers and acquisitions advisory, equity and debt capital markets, and institutional securities. It offers client-centric innovative solutions. The company’s headquarters is situated in Mumbai. Therefore, we can say that these investment banking companies are the backbone of the Indian Financial Ecosystem.

On a concluding note, investment banking companies play an important role in the growth of the Indian Economy by providing advisory services, such as mergers and acquisitions and capital raising, to Indian Companies. However, competition in the investment banking industry has increased over time due to a range of multinational and domestic players. Investment banking companies help various players in launching their IPOs and getting them listed on the Indian Stock Exchange.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

A financial company that helps other companies raise capital and provides advice on corporate restructuring, such as mergers and acquisitions, is known as an investment banking firm.

Which are India’s top investment banking firms?

Edelweiss Financial Services Limited, JP Morgan, Goldman Sachs Limited, and others are among the leading investment banking firms.

Who regulates the investment banking companies in India?

The investment banking companies in India are regulated by the SEBI (Securities and Exchange Board of India).

How do investment banking companies earn their revenue?

Investment banking companies generally get their revenue from underwriting commissions, advisory fees, etc.

Which city in India has the most investment banking companies?

Most of the investment banking companies are located in Mumbai, which is also known as the Financial Capital of India.

In the Indian stock market, there are mainly two ways to trade in the stock market. One way is where you make money slowly and steadily identical to a 5 day test match and you hold these shares for a long time hoping they’ll grow in value over time. This is called investment.

The other way is where you buy and sell the share on the same day hoping to make small quick profits, it has characteristics like a fast-paced T20 match quick and full of action. This strategy is known as intraday trading and for this fast game, traders use a special tool called MIS.

What is MIS?

As a trader whenever you open a trading app you might have seen a little option that says ‘MIS’, have you ever wondered what exactly it is? The full form of MIS is Margin Intraday Square-Off where:

Margin stands for a small loan from the broker for a day. It helps traders with more money to invest than you have in your account.

Intraday stands for within the same day, here any trade that you make using MIS has to be opened and closed on the same day.

Square-Off stands for a simple action of closing your trade, meaning the already bought shares shall be sold and if you have sold them first, you must buy them back.

MIS in the stock market is a special order for day traders who borrow margin to increase their investment and shut these trades before the market closes.

How MIS Works?

Let’s look at an example to learn how MIS works in the stock market, let’s say as an investor you had a strong feeling that Reliance Industries stock will rise today, if the stock is trading at Rs.1,500 and you decide to buy 10 shares. When you open your trading app to place the order, you specifically select the MIS option. This is a signal to the broker that this is a one day trade. But here as an investor you need to sell these shares before the market closes regardless of whether you make profit or loss, as this is the golden rule of MIS where you need to clear everything before the market closing time.

Now, let’s get to the most powerful and riskiest part of MIS that is the Margin.

Suppose you have Rs.10,000 in your savings account but you want to buy shares of a company worth Rs.50,000 because you have a strong feeling that there will be a price jump today. Here comes the role of MIS where your broker will give you a margin of the remaining Rs.40,000 and will add you Rs.10,000 as a security deposit. Now you can invest this cumulative Rs.50,000 in your desired stock with just spending Rs.10,000 of your own pocket. This power to control a large asset with a small amount of your own money is called leverage. It’s like using a lever to lift a heavy object you couldn’t lift on your own.

In India, brokers generally offer a leverage up to 5 times on stocks for MIS trades. This means for every Rs.1 you have, you can trade with Rs.5. So, with just Rs10,000, you can command a trading position of Rs.50,000. This is the real use of MIS as it allows traders to aim for bigger profits from small price movements by trading with a much larger sum of money than they personally have.

The Square-Off Mechanism

What if you get caught up in a meeting and completely forgets to sell the shares that were bought using MIS. This is where the “Square-Off” becomes very important.

You can close your MIS position yourself anytime during market hours (9:15 AM to 3:30 PM), this is known as manual square-off. But if you do not close your positions in the given time then your broker will step in and do it for you. This is called an auto-square-off. Most brokers in India have a cut-off time, usually between 3:15 PM and 3:25 PM, after which their systems will automatically close all open MIS positions.

The leverage received to the investors is only for that single day, where you need to settle the books and close the temporary loan. This protects both you and the broker from the massive risk of an overnight price crash. Because the broker has to perform this action for you, they will charge a penalty, typically around Rs.50 + GST, for every order that is auto-squared-off.

How to Trade Stocks Using MIS in the Share Market?

Placing an MIS order is straightforward on most modern trading platforms. While the buttons might look a little different on Zerodha Kite, Pocketful, or Angel One, the process is largely the same.

Select Liquid Stock: You need to select stocks that are highly traded in the stock market, meaning lots of people are buying and selling them throughout the day. These stocks are known as liquid stocks as they ensure that you can buy and sell your trades easily.

Order Window: As an Investor you should log in to your trading app, find the stock you want to trade using the search bar, and tap on ‘Buy’ (if you think the price will go up) or ‘Sell’ (if you think it will go down).

Select ‘Intraday’ or ‘MIS’: This is the crucial step where investors see product types like ‘Intraday (MIS)’ and ‘Longterm (CNC)’. You must select ‘Intraday (MIS)’ to tell your broker this is a day trade.

Select Quantity and Price: Decide how many shares you want to trade. You will also need to choose an order type meaning either market order or limit order. Where market order means your trade happens instantly at whatever the current market price is. And limit order is set at a specific price and your trade will only happen if the stock reaches that price.

Place and Monitor Your Order: Once you’ve placed the order, it will appear in the ‘Positions’ or ‘Orders’ tab of your app and you can easily watch your profit or loss changing in real-time.

Square Off Your Position: This is the final and most important part of the trade, where you need to close your trade before the auto-square-off time kicks in. Go to your open position and place an opposite order, let’s say if you bought 10 shares, you must now sell all 10 shares, but if you short-sold 5 shares, you must now buy back 5 shares. This completes your MIS trade.

Benefits of Margin Intraday Square-Off (MIS)

Bigger Trade Potential: Here Leverage is the main attraction as you can increase your capital up to 5 times increasing your buying power and allowing you to take a significant position in the market with a relatively small amount of capital.

Higher Profits Potential: As you’re trading with a larger, leveraged amount, even a tiny price movement can result in a handsome profit on your initial capital. Let’s say a 2% profit on a leveraged amount of Rs.50,000 is Rs.1,000. Then you can earn a solid 10% return on your own funds of Rs.10,000.

No Overnight Risk: As in this you need to close all your positions before the market closes, news and rumours in the after market hours do not affect your profits, since all MIS trades are closed the same day and you are completely protected from any such overnight changes.

Profit from Short Selling: MIS allows you to do something called ‘short selling’, which means you can sell shares first (even if you don’t own them) at a high price, and then buy them back later at a lower price. The difference is your profit. This is a powerful way to make money even when the market is going down.

Lower Brokerage Costs: Many brokers offer a discounted brokerage fee for intraday trades compared to delivery trades, which can save you a lot of money if you trade frequently.

Risks Associated with Margin Intraday Square-Off (MIS).

1. Amplified Losses

This is the other side of the leverage, just as profits are magnified, losses are magnified too. That same 2% price move that could have made you a 10% profit can also hand you a 10% loss on your capital if it goes against you. A slightly larger adverse move can wipe out your entire trading capital in a matter of minutes.

2. Auto-Square-Off Risk

The market might be temporarily against you, and you might feel it will recover if you just wait a little longer. But with MIS, you don’t have that, the broker’s system will automatically close your position at the cut-off time, forcing you to accept a loss even if you wanted to hold the stock.

3. The Circuit Limit Trap

This can be a major risk for intraday traders as every stock has a ‘circuit limit’, which is a price band set by the exchange, in this if the stock price hits the top or bottom of this band, trading is halted.

Lets say You Buy a stock and it hits the Lower Circuit, now there are only sellers (like you, desperate to get out) and zero buyers as the stock is drastically falling. In this situation you are stuck and cannot sell your shares. Because your MIS trade cannot be squared off, your broker will be forced to convert it into a delivery trade meaning, you are now obligated to pay the full 100% value of the shares you bought with leverage. If you don’t have enough cash the broker might sell your other holdings or charge you heavy interest until you pay up.

Also when you short-sell and it hits the Upper Circuit. You short-sold a stock, betting that it will fall. But instead of falling, it skyrockets and hits its upper circuit. In this situation there are only buyers and no sellers and you cannot buy the shares back to close your position which is also known as ‘short delivery’. You have failed to deliver the shares you sold. The stock exchange will then hold an auction to buy the shares on your behalf, often at a much higher price, and you will have to bear the cost plus a significant penalty.

4. Mental Pressure

The combination of high speed, high stakes, and the risk of rapid losses can be incredibly stressful. It can push traders to make impulsive decisions driven by fear or greed, which can feel as a huge burden.

MIS vs. CNC

Feature

MIS (Margin Intraday Square-Off)

CNC (Cash and Carry)

Main Purpose

Same-day trading (Intraday)

Investing for more than one day (Delivery)

Holding Period

Must be closed the same day

Can be held for days, weeks, or years

Leverage

Yes, up to 5x leverage is available

No, you need 100% of the money

Auto Square-Off

Yes, broker closes it automatically if you don’t

No, you are in full control of when to sell

Best For

Active traders trying to profit from daily price changes

Investors who want to own shares for long-term growth

MIS is a powerful tool built for the fast and furious world of intraday trading and it gives traders the option of leverage, letting traders make bigger trades than their own account balance would allow leading to quicker and larger profits.

But with great opportunities comes a great risk. This same leverage can amplify your losses easily and can wipe out your hard-earned money in the blink of an eye. Success with MIS isn’t about luck, it is about deep knowledge, a solid trading plan, and the discipline to manage your risk and emotions on every single trade.

If you’re just starting out, treat MIS with extreme caution. The smart move is to first learn everything you can, maybe even practice using an online simulation account. Only then should you consider stepping into the MIS, and only with money you are fully prepared to lose.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What if manual square off is not done for my MIS position?

In this scenario the broker will automatically close your position for you at a fixed time, usually between 3:15 PM and 3:25 PM. For this service, you will be charged a penalty fee ( around Rs50 + GST) on top of any trading loss.

Can MIS trade be converted to a delivery (CNC) trade?

Most ‘buy’ trades can possibly be converted, if you buy shares using MIS, the price starts to move in your favor and you decide you want to hold them for longer, then you can convert your position to CNC. However, you must have enough cash in your account to cover the full 100% value of the shares, and you must make the conversion before the auto-square-off time begins.

How is profit or loss calculated in an MIS trade?

The profit or loss is always calculated on the full, leveraged trade value, not just on your margin amount. Let’s say you used Rs.10,000 of your money to take a leverage of Rs.50,000 position. Here, if the stock moves up by 2%, your profit is 2%×50,000=Rs.1,000. This is a 10% return on your capital. But what if the stock falls by 2%, your loss is also Rs.1,000, which is a painful 10% loss of your capital.

Are all stocks available for MIS trading?

No, certain selective stocks are only available for MIS trading, generally stocks that have a high liquidity and high trading volumes are selected. This is a safety measure to ensure that traders can always find a buyer or seller to exit their positions easily.

Can beginners start MIS trading?

Honestly, MIS trading is very risky and not recommended for someone beginners. It demands a solid understanding of how markets move, technical analysis, and, most importantly, strict risk management.

Interest rates play the most important role in the world of money. They are not just a percentage, but the real cost of borrowing and investing. It is important to understand the different types of interest and types of interest rates, because some of them are such which type of interest can change over the life of a loan? That is, such interest rates which can change over time. In this article, we will understand 10 types of interest rates in simple language and know how they affect our financial decisions.

What is Interest Rate?

Interest rate is the price that is paid on any borrowed money. In simple words, if a loan is taken from a bank or NBFC, the additional amount that has to be paid on it is the interest. It is measured in percentage (%) and this rate decides how much your EMI will be or how much return you will get from the investment.

Why is it important to understand interest rates?

Interest rates are not just a number or percentage, but they affect your entire financial journey. Many people take a loan just by looking at the “low interest”, but do not understand whether the rate is fixed or variable.

Example : Suppose someone took a home loan and thought that the interest will always be 8%. But after a few years he came to know that he had chosen a floating interest rate, and after the change in RBI policies, the EMI increased to 10%. Result—he had to pay thousands of rupees more every month.

Interest rate game in banks and credit cards

Banks, NBFCs and credit card companies apply different types of interest rates. For example, personal loans and credit cards have higher interest rates because they are unsecured loans. On the other hand, home loans or car loans may have lower rates because they have collateral.

Why is it dangerous to look at only the percentage?

Most people look at the interest rate only as a percentage (%). But due to not understanding the “type” of the rate, the actual cost can increase manifold. That is, despite the low percentage, if the rate is compound or floating, then the payment in the end can be very high.

Fixed interest rate is a type of interest rate in which the interest rate remains fixed during the entire loan tenure and there is no change in it. Whether interest rates rise or fall in the economy, the EMI on your loan will remain the same as it was decided in the beginning.

How does it work?

When you take a loan from a bank, the bank offers a fixed rate. If you choose it, your EMI will be calculated at the same interest rate for the entire loan tenure. The bank locks this rate so that you have to pay the same installment (EMI) every month.

Advantages:

EMI remains stable, which makes budget planning easier.

Your loan will not become expensive even if the interest rate increases.

You get peace of mind for a long time as there is no uncertainty in payment.

Disadvantages :

Even if interest rates go down in the future, you will still have to pay the same high rate.

Initially, the fixed rate can be a little more expensive than the floating rate.

Some banks have a reset clause, which means the rate can be reset after 5–10 years.

Example : Many banks in India offer fixed rate home loans for 10–15 years. Suppose, someone has taken a loan of Rs 20 lakh at a fixed rate of 8.5%. For the next 15 years, even if RBI reduces the repo rate to 6%, the EMI of that person will remain the same.

This interest rate is best suited for people whose income is stable, like government employees or people with fixed salaries. Such people do not want to take risks and they want stability in EMI.

2. Floating Interest Rate

What is it?

Floating interest rate is a type in which the interest rate of the loan keeps changing from time to time. This rate depends on RBI policies, repo rate, and market conditions. That is, your EMI can increase or decrease during the loan period.

How does it work?

When you choose a floating rate, the bank links your interest rate to the repo linked lending rate (RLLR) or marginal cost of funds-based lending rate (MCLR). As soon as the RBI decreases or increases the repo rate, your EMI also changes accordingly.

Advantages:

If interest rates decrease, your EMI also decreases.

Initially, floating rate is cheaper than fixed rate.

There is a possibility of saving interest in the long run.

Disadvantages:

There is uncertainty in EMI, which can make budget planning difficult.

EMI can be very high if interest rates increase suddenly.

Loan tenure can increase if EMI is kept the same.

Example : Suppose someone has taken a home loan of 20 lakhs at 8.5% floating rate. If RBI reduces the repo rate to 6%, then the interest rate can also come down to 7%. But if RBI reduces the repo rate to 7%, the interest rate can increase to 9%.

This interest rate is good for those whose income is likely to increase, like private sector employees or business people. It gives them an opportunity to take advantage of low interest rates, but there is also a risk of fluctuations in EMI.

3. Reducing Balance Interest Rate

What is it?

Reducing Balance Rate is the interest rate in which EMI is calculated on the decreasing principal amount every month. That is, after paying every EMI, the principal decreases and the next month’s interest is charged on the same reduced principal.

How does it work?

Suppose, you have taken a loan of 10 lakhs. After paying the first EMI, the principal will decrease a little. The interest of the second EMI will be charged on the newly reduced principal. In this way, your interest keeps decreasing over time and the loan gets repaid quickly.

Advantages:

Interest is charged only on the remaining principal, due to which the total interest has to be paid less.

It proves to be economical for the borrower in the long run.

Gradually the interest part in EMI decreases and the principal part increases.

Disadvantages:

The initial EMI may be a little higher.

Understanding the EMI structure can be difficult for new borrowers.

Some banks may have higher processing fees or hidden charges.

Example : Most banks follow the reducing balance method for home loans and personal loans. For example, taking a loan of Rs 10 lakh at 8% reducing balance rate results in lower total interest than a fixed rate loan.

This interest rate is best for those who take a large loan for a long period. This saves on interest and repayment is faster.

4. Simple Interest Rate

What is it?

Simple Interest Rate is the interest rate in which interest is charged only on the principal, not on the previously added interest. It is often used in short-term loans, education loans or small borrowings.

How does it work?

Simple Interest is calculated as (Principal × Rate × Time) ÷ 100. Suppose 1 lakh rupees is taken at 10% simple interest for 1 year, then the interest will be only Rs 10,000.

Advantages:

The calculation is easy and transparent.

The borrower knows how much interest he will have to pay.

It is economical for short-term loans.

Disadvantages:

The borrower does not get much benefit in long-term loans.

There is a lack of compounding benefit.

EMI repayment structure is not flexible.

Example : Many microfinance loans or short-term agriculture loans are given using simple interest methods.

This interest rate is suitable for those who need a loan for a short period and want a clear calculation of repayment.

5. Compound Interest Rate

What is it?

Compound Interest Rate is one in which interest is charged on the principal as well as on the previously added interest. That is, the concept of “interest on interest” applies.

How does it work?

Suppose, Rs 1 lakh is taken annually at 10% compound interest. After the first year, the interest will be Rs 10,000, which will make the amount Rs 1,10,000. Next year interest will be charged on Rs 1,10,000 i.e. Rs 11,000.

Advantages:

The lender gets higher return due to compounding effects.

In short-term loans, the borrower does not make much difference.

Banking and credit card interest is based on this.

Disadvantages:

In the long run, the borrower may have to pay a lot of interest.

Loans can be expensive if repayment is not done on time.

Interest calculation may seem complicated for the borrower.

Example : Credit card dues and overdraft facilities are based on compound interest rates.

This interest rate is beneficial for the lender. Borrowers should always repay the loan taken at compound rate on time, otherwise the debt can increase rapidly.

6. Prime Lending Rate (PLR) – (Prime Lending Rate)

What is it?

Prime Lending Rate (PLR) is the minimum interest rate at which the bank gives loans to its most trusted and creditworthy customers. It works like base rate.

How does it work?

Banks decide PLR by looking at RBI’s monetary policy and their cost of funds. Customers with good credit scores and strong repayment capacity get loans at PLR. Other borrowers are given loans at rates above PLR.

Advantages:

Borrowers with high credit scores get loans at lower interest rates.

Loan rates are transparent and RBI linked.

PLR is a benchmark for creditworthy borrowers.

Disadvantages:

Average borrowers do not get loans at PLR.

Changes in PLR depend on RBI’s policy.

The actual loan rate for common borrowers is higher.

Example : Top corporates and big companies get working capital loans and term loans at PLR.

This rate is more useful for high-profile borrowers and corporations. Common borrowers usually have to take loans at rates above PLR.

7. Discount Interest Rate

What is it?

Discount Interest Rate is the rate at which commercial banks do short-term borrowing from RBI. It mainly applies to discounted bills of exchange and short-term securities.

How does it work?

This rate is applicable when RBI discounts commercial papers, treasury bills or promissory notes. It is a monetary tool of the RBI to control short-term liquidity.

Advantages:

Helps to overcome short-term liquidity crunch.

Maintains credit flow in the market.

Regulates borrowing cost.

Disadvantages:

Short-term borrowing becomes expensive when the rate is high.

The general public does not get the benefit directly, it is relevant for banks.

This rate is often dependent on market conditions.

Example: If a commercial bank suddenly needs short-term liquidity, it borrows from RBI at a discount rate.

Discount rate acts as a short-term liquidity stabilizer in the banking system. It does not directly affect borrowers, but indirectly affects loan rates and market liquidity.

8. Real vs Nominal Interest Rates

What is it?

Nominal Interest Rate – This is the rate in which inflation is not included.

Real Interest Rate – It is derived by subtracting inflation from nominal interest rate.

How does it work?

Suppose nominal interest rate is 8% and inflation is 5%, then real interest rate will be only 3%. Real rate shows actual purchasing power and return.

Advantages:

Nominal Rate Easy to understand and compare.

Real Rate Shows real return and cost.

Disadvantages:

The nominal rate is not inflation-adjusted, which can hide the actual benefit.

Accurate inflation data is required to calculate the real rate.

Example: An FD gives 7% nominal interest. If inflation is 6%, then the actual return will be only 1%.

Investors and borrowers should always pay attention to the real rate, because it shows their real cost and real return.

9. Secured vs Unsecured Loan Interest Rates

What is it?

Secured Loan Loans which are given against collateral (such as property, gold, FD).

Unsecured Loan Loans which do not have any security, such as personal loan, credit card loan.

How does it work?

If there is collateral, the risk to the bank is reduced, so the interest rate on secured loan is low. Whereas in unsecured loans, the rate is high due to higher risk.

Advantages:

Secured Loan Lower interest rate and higher loan amount.

Unsecured Loan Fast approval and no need for collateral.

Disadvantages:

Risk of losing assets on defaulting on secured loans.

High interest rate and short repayment period in unsecured loans.

Example:

Home loan and car loan are secured.

Personal loan and credit card loans are unsecured.

Secured loans are cheaper for borrowers, but there is collateral risk. On the other hand, unsecured loans are expensive but prove useful in an emergency.

Penalty Interest Rate is the additional interest that is charged in case of delay or default of loan EMI.

How does it work?

If the borrower does not repay on time, a penalty rate is charged over and above the normal interest rate. This rate may vary according to the terms & conditions of the banks.

Advantages:

Makes borrowers disciplined for timely repayment.

Helps banks cover default risk.

Disadvantages:

The financial burden on borrowers increases.

High penalty rates can put borrowers in a debt trap.

Example : The EMI of a personal loan is Rs. 10,000 and the borrower delays. The bank can charge an extra 2% per month penalty rate on it.

Penalty rate is a harsh financial cost for borrowers. The best way to avoid it is by repaying on time.

Look at the stability of income : If the income is stable and EMI can be paid comfortably every month, then fixed rate proves to be better. But for those whose income is variable, like people working in business or commission-based jobs, floating rate is more practical.

Importance of Loan Tenure : For short-term loans i.e. 1 to 5 years, floating rate is a good option, because short-term fluctuations remain manageable. On the other hand, for long-term loans i.e. 10 to 20 years, fixed rate keeps EMI stable and financial planning becomes easy.

Effect of Inflation : If inflation is expected to increase in the coming time, then fixed rate keeps EMI stable. On the other hand, in case of inflation decreasing, floating rate benefits the borrowers, because interest rates can come down.

Risk Appetite : For conservative borrowers, fixed rate is better, so that EMI remains predictable. Floating rate is good for those whose risk-taking capacity is moderate or high, so that they can get the benefit of low interest rate.

Purpose of Loan : Fixed rate provides more stability for home loan and education loan. Floating rate is more suitable for working capital or business loans because it provides cash flow flexibility. In case of investment-linked loans, one should choose after understanding the real interest rate and compound effect.

Practical Checklist : Before taking a loan, it is important to think about how much percentage of income EMI is manageable, for how long the loan has to be taken, how much impact will inflation and RBI policy changes have on EMI, what will be the long-term difference between fixed and floating and what will be the penalty charges or foreclosure rules.

It is important to understand the different types of interest rates as they determine your loan cost and financial planning. Choosing the right interest rate depends on your income, loan tenure and market conditions. A wise decision not only makes EMI management easier but also ensures financial stability in the long term.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Imagine a company wants to sell its shares to thousands of people to raise money. To do this fairly, the law says it must give you a detailed report card called a prospectus. This document tells you everything you need to know as an investor: the company’s health, its goals, and the risks involved, so investors or buyers can make a smart decision.

But what if a company doesn’t directly sell you the shares, rather it sells a huge chunk of its shares to a merchant bank (middleman). Then, that bank turns around and offers those same shares to you. It seems like the company is avoiding its duty to give you the full story.

This is where the law introduces new rules. In this blog, we will understand what a deemed prospectus is. The idea is straightforward: if a document is used to offer a company’s shares to the public, even through an intermediary, the law treats it as a prospectus. For example, when a bank issues an “Offer for Sale” for shares it recently purchased from a company, the law considers that document as the company’s own deemed prospectus. This means the company remains fully accountable for all the information it contains.

What is a Deemed Prospectus?

The concept of a deemed prospectus is defined under Section 25(1) of the Companies Act, 2013. It states that if a company allots its shares to an intermediary with the intention of selling them to the public, then the document used for that sale will be treated as a prospectus issued directly by the company.

It doesn’t matter what the document is called, if its job is to get the company’s shares into the hands of the public, the law holds the original company responsible. This keeps the company accountable for the information you receive.

For Example : A company called “XYZ Pvt. Ltd.” needs funds to expand the company. Instead of launching a regular IPO, the company sold a large number of its shares to “ABC Bank” on January 1st. Within the next 6 months the ABC Bank creates a document called an “Offer for Sale” and invites the public to buy XYZ Pvt. Ltd. shares.

As the selling of the shares has started within six months, the law gets automatically triggered. The “Offer for Sale” document from ABC Bank is now legally considered the deemed prospectus of XYZ Pvt. Ltd. meaning the directors of XYZ Pvt. Ltd. are fully responsible for information provided by the bank related to the company’s details.

When is a Deemed Prospectus Triggered?

The Six-Month Rule

The first trigger is set according to the timing, where if the merchant banker (middleman) offers the shares to the public within six months of getting them from the issuing company, the law steps in and a quick sale like this suggests it was never a real investment by the banker but just a step in the company’s plan to reach the public.

The Unpaid Bill Rule

The second trigger is set according to the money, here if the issuing company hasn’t received the full payment for the shares by the time the middleman starts selling them, it is concerning. This shows that the company’s payment depends on the public buying of the shares, meaning the company is the one truly raising money from you.

Complete Information: The main role of a deemed prospectus is to provide you with complete and honest information before you plan to invest. It makes the company to be transparent about its functions, fundamentals, business, finances and associated risks.

Issuing Company’s Accountability: It holds the company and its directors accountable instead of the middlemen as they are legally responsible for each and every information provided in the deemed prospectus, just as if they had written it themselves.

Protects Investors and Builds Trust: By preventing companies from bypassing disclosure through middlemen, the rule strengthens investor protection and builds trust in the fairness and reliability of the securities market.

Deemed Prospectus vs. Prospectus

Features

Regular Prospectus

Deemed Prospectus

Issuer

Directly issued by the company

Issued by a middlemen like Bank

Offers

It offers a direct invitation to the public

It is an indirect offer to the public

Primary Document

Known as “Prospectus”

The Document is called ‘Offer For Sale’ but treated as Prospectus under law.

Responsibility

The Company and its directors

Both the middlemen and the company

What is Included in the Deemed Prospectus?

Deemed prospectus includes all necessary information required as per the normal Prospectus like:

All details about the company history and businesses.

Transparent information about the directors and company’s management.

Yearly audited financial reports or we can also say the company’s report card.

Clear information about the offered shares.

It also tells us the risks that are prominent in the company’s growth.

Although Deemed Prospectus also requires two extra details for complete transparency about the deal with the middleman:

The Net Payment: It must state exactly how much money the company received from the middleman for the shares. This lets you see the profit the middleman is making.

The Contract: It must tell you where and when you can go and see the contract signed between the company and the middleman. This provides a paper trail for regulators.

Liabilities for Wrong Information

If a deemed prospectus contains misleading or false information, the consequences are severe, just like with a regular prospectus.

Civil Liability: If investors lose the invested amount just because of the wrong and misleading information of the prospectus, then they can sue the company, its directors and the banker for compensation.

Criminal Liability: If things turn out to be right and it’s proven that the prospectus was intentionally fraudulent, then the responsible people can face jail time of up to ten years and heavy fines can be imposed depending on the gravity of fraud.

Deemed Prospectus turns out to be a powerful tool that protects the investors money ensuring that the shares offered by the company via deemed prospectus is true, as it is directly provided by the company to the investors. It guarantees that you get the full picture needed to make informed decisions, building a stock market that is safer and more trustworthy for everyone.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Are Red Herring Prospectus (RHP) the same as Deemed Prospectus?

No, they are different, an RHP is a draft prospectus for a direct IPO that doesn’t include the final price or number of shares.

Who is liable for wrong information in a deemed prospectus?

For any misleading and wrong information the Director as well as the middlemen both are responsible.

Why are middlemen used instead of a direct IPO by the company?

It is a faster way to enter the market and also a faster way to raise funds by using the existing middlemen network.

Main thing to know about a deemed prospectus?

The most important thing to be known by an investor is that their rights are protected as law treats a deemed prospectus just like a regular one, meaning you are entitled to receive complete and accurate information, and the company is fully accountable for it.

Deemed prospectus have to be filed with the government?

Yes. Because it is legally considered a prospectus “for all purposes,” it must be filed with the Registrar of Companies (RoC) before it can be shared with the public, just like any other prospectus.

An Exchange Traded Fund, or ETF, is a simple way to invest, where there is a basket that holds different types of stocks like Nifty 50 ETF which holds shares of the top 50 companies of India. When you invest in one unit of the ETF you get small pieces of all 50 companies in one go.

As ETFs are similar to stocks in terms of price change, in an ETF the price also changes every second but how can you decide which exact price is fair for you making an investment. Here comes the role of Indicative Net Asset Value (iNAV) or in simpler terms you can refer to it as live MRP for an ETF as it shows you the real-time fair price of one unit and gets updated in every few seconds.

What is iNAV in ETFs and How Does It Work?

iNAV or Indicative Net Asset Value or to make it more easy to understand it is the real time fair price of one unit of an ETF which gets updated every 15 seconds in India while the market is open.

The main job of an iNAV ETF is to be your guide. It helps you to show what one unit of the ETF should be worth at any moment, based on the live prices of all the stocks inside its basket. You can look at the iNAV and compare it with the actual trading price on your screen to see if you’re getting a good deal.

How does iNAV Works?

Let’s understand how an iNAV works by using a simple example:

Let’s assume an ETF basket only has two company stocks, one is share of Company A and one is share of Company B. To calculate the iNAV, the system constantly checks the live market price of both stocks. It adds them up, makes tiny adjustments for any cash or expenses, and then shows you the fair value of one ETF unit automatically.

This gives you a transparent, live value for you to invest in your desired ETFs. This is needed because an ETF is a mix as it trades like a stock, but is actually built like a fund. A normal mutual fund’s price is set only once a day. But since you trade ETFs with other people all day, a once-a-day price is not enough and iNAV solves this problem.

NAV is like the snapshot of information that you get once or typically at the end of the day on the other hand iNAV gives you live updates about all the latest happenings throughout the day. Here are some of the main differences between the both:

Calculated: NAV is calculated only once a day, after the market closes whereas iNAV is calculated throughout the day in every 15 seconds.

Product Compatibility: NAV is for traditional mutual funds and iNAV is specially made for ETFs because they trade all day.

Usage: For mutual funds, NAV is the actual price at which traders buy or sell. iNAV is just a guide to check the fairness of the market price for the ETFs as here you trade at the market price, not the iNAV.

Feature

NAV (net asset value)

iNAV (Indicative net asset value)

Calculation Time

Once a day, after the market closes.

Every 15 seconds during market hours.

Portrays

The final, official price for the day.

A live, estimated fair value.

Usage

Traditional Mutual Funds.

Exchange-Traded Funds (ETFs).

Relivance

The actual price you buy or sell at.

A guide to check if the market price is fair.

Why is iNAV Important for You?

Let’s understand this by looking at a few points related to iNAV.

Fair Price Detection: ETFs do not have an exact underlying value, either it can be priced higher (at premium) or lower (at discount) as using iNAV you can spot the differences in real-time, helping you know the fair price of the ETF.

Avoid Overpaying: Using iNAV helps traders with choosing the right fair price as it helps in ensuring that the traders get to know the correct ETF price and not lose money by paying more than it’s worth.

Unlock Opportunities: iNAV is essential for traders who trade throughout the day, as it helps in highlighting the price discrepancies which creates opportunities for arbitrage, the strategy of buying an asset at a lower price and selling it for a higher one almost instantly.

Provides Confidence: If you are planning to hold your ETFs for years iNAV offers valuable transparency because it confirms that your investment is being valued fairly and helps you track your portfolio by telling you if it is on the right path or not.

Crucial for Global ETFs: Global ETFs are susceptible to different prices, currency and even time zone, iNAV helps in comparing all these factors and gives you the information so that you can make an informed decision while buying or selling these global funds.

It’s very easy to check the iNAV. Here are the best places to find it:

AMC Websites: You can directly check the official website of the fund house (AMC) that runs the ETF as it is one of the most reliable sources. For example, you can go to the websites of Zerodha Fund House, Motilal Oswal, or Mirae Asset to see the live iNAV for their ETFs.

Stock Exchange Websites: Both NSE and BSE helps the traders by showing the iNAV on their websites. You just need to look for the term “i-NAV” on the ETF’s page.

Your Trading App: Most trading apps like Zerodha Kite or Pocketful also show the iNAV, but be a little careful, as the data can sometimes be slightly delayed and a fraction of seconds can give you a different result, so if you are making any big investments then always cross check it on the AMC’s website.

Advantages of iNAV

Real Picture: iNAV gives you a live, transparent view of an ETF’s fair price.

Better Decisions: It helps the traders in making better decisions whether to buy or sell if the ETF is overpriced (premium) or underpriced (discount).

Keeps Informed: It protects investors from accidentally paying too much price, especially during the bullish market.

Disadvantages of iNAV

No real price: You can check the price but you can’t place an order to buy at the iNAV as it is just for your market price reference and remember trades will always happen at the real market price.

Delays: The iNAV updates every 15 seconds and in a very fast-moving market, even this tiny delay means the iNAV might be a little behind the real value, so always consider this.

The International Problem: For ETFs that hold foreign stocks (like US stocks), the iNAV can be tricky. While calculating the US market’s ETFs and if the market is closed, iNAV generally uses the previous day’s price making it less useful.

iNAV is a simple but very powerful tool for anyone investing in ETFs as it functions as a guide for your busy stock market schedule. It makes investing clearer and gives power to every investor, whether you are a beginner or an expert.

Remember as a good investor you always need to compare the market price with the iNAV before you click the buy or sell button. This two-second check can save you from bad deals, keep you calm when the market is shaky, and protect you from costly mistakes.By understanding simple ideas like iNAV, you are taking control of your money and making smarter choices for your future.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

NAV is the official price for a mutual fund, calculated once a day after the market closes. iNAV is a live, estimated price for an ETF, updated every 15 seconds during the day to act as a guide.

If an ETF’s market price is much higher than its iNAV, should I invest in it or not?

If the price is much higher than the iNAV, it means you are overpaying so it’s better to wait for the price to come closer to the iNAV before you make your investment.

How often is iNAV updated in India?

For stock ETFs in India, the iNAV is updated at least every 15 seconds during market hours.

Is iNAV always 100% correct?

It’s a very close estimate, but not perfect. There can be a small delay, also for ETFs with international stocks, the iNAV can be based on old prices if the foreign market is closed, which makes it less accurate at that time. Use it as a reliable guide, not a perfect number.

Where can I check iNAV?

You can directly look for the iNAV from the official websites of the fund houses (AMC) which manages the ETF. Or you can also go on the stock exchange websites like NSE OR BSE to know the fair prices of your desired ETF funds.

Retirement planning has always been a key financial goal for an individual. For Central Government Employees, there are various retirement schemes such as PPF, NPS, etc. But recently, the Government has introduced another scheme commonly known as “UPS” or “Unified Pension Scheme”, this scheme offers a minimum guaranteed Pension.

In this blog post, let’s understand about the Unified Pension Scheme, its eligibility criteria, the process to apply and the key difference between NPS and UPS.

What is the Unified Pension Scheme?

The Unified Pension Scheme was introduced by the Government of India on 24th August 2024, and it became effective from 1st April 2025 for Central Government Employees. This scheme does not include armed- force personnel. The central Government employees can continue with the National Pension Scheme or switch to UPS. If the employee opts for UPS, they cannot be changed back to NPS.

Eligibility Criteria for Unified Pension Scheme

The following are the eligibility criteria for an individual to become eligible for the Unified Pension Scheme:

Only central Government employees who are serving on 1st April 2025 and are covered under NPS can invest in UPS.

Any new employee joining after 1st April 2025 is eligible for UPS.

Any central Government employee covered under NPS who has taken voluntary retirement on or before 31st March 2025.

The spouse of a Central Government employee, who was an NPS subscriber and passed away before exercising the option to opt for the OPS.

Who is Not Eligible for the Unified Pension Scheme

The following persons are not eligible for the Unified Pension Scheme:

Employees retiring from their service before the period of 10 years.

Employees who have been removed from the service.

The Central Government of an employee who has been dismissed from the service.

UPS Scheme Minimum Pension Amount

The minimum Pension amount guaranteed under the Unified Pension Scheme will be 10,000 per month only for employees who have completed 10 years of service.

Benefits of Unified Pension Scheme

The key benefits of the Unified Pension Scheme are as follows:

Fixed Pension: An individual will receive a fixed sum of amount after their retirement, which is equal to 50% of their average basic pay over the previous 12 months of retirement.

Contribution: The employee will contribute only 10% of their basic salary, whereas the Government contributes 18.5% of the employee’s basic salary.

Family Pension: In case of the demise of the account holder before retirement, 60% of the Pension will be given immediately to the spouse of the Pensioner.

Minimum Amount of Pension: An employee who has completed only 10 years of service and retires is eligible for 10,000 INR of monthly Pension.

Inflation Benefit: The individual will get the benefit of inflation adjustment based on the dearness allowance.

One can apply for the Unified Pension Scheme either online or offline:

1. Online Process:

To apply for UPS through online mode, one can follow the steps mentioned below:

First, an employee needs to visit the Protean Website.

On the home page of the website, there is an option for the Unified Pension Scheme. Click on it.

There you will find Register for UPS; however, if you want to migrate NPS to UPS, you can also select the same on this page.

You can fill out the form and submit the details.

2. Offline Process:

For the offline process, one can follow the steps mentioned below:

The first step is to visit the Protean website.

You will find a ‘Forms’ section under the Unified Pension Scheme. Download the relevant form depending on your service status.

You need to fill in the form and submit it to the drawing and disbursing officer.

The DDO will check the form and send it to the Pay and Accounts Officer for approval.

UPS Withdrawal Rule and Conditions

The conditions related to the withdrawal are based on two rules, namely complete withdrawal or partial withdrawal, the details of which are as follows:

Complete Withdrawal: An employee can withdraw a maximum of 60% of their corpus under the Unified Pension Plan. The remaining amount of the corpus will be utilised towards the regular monthly Pension. However, if the withdrawal is made, the monthly Pension can be reduced proportionately. In case of the death of an employee, their spouse receives 60% of the last Pension for their lifetime.

Partial Withdrawal: An employee can make a partial withdrawal a maximum of three times during their service period. The provision of partial withdrawal is applicable only after a period of three years. Only 25% withdrawal is allowed each time for specific circumstances, such as children’s higher education, medical expenses, etc.

The key difference between the Unified Pension Scheme and the National Pension Scheme is as follows:

Particular

UPS

NPS

Pension Amount

UPS offers a fixed Pension amount.

The Pension through NPS depends on the corpus accumulated.

Minimum Pension

A minimum guaranteed Pension of INR 10,000 is provided in this scheme.

There is no provision for a minimum Pension.

Eligibility

This scheme applies only to central Government employees.

Both central and state Government employees, along with private individuals, are eligible for NPS.

Market Risk

There is no market risk in it.

As the amount under this scheme is invested in market-linked instruments. Hence, it carries a high risk.

Inflation

The amount of the Pension is adjusted for inflation.

There are no provisions for inflation adjustment.

Portability

Central Government employees opting for UPS can port their investment.

Portability across sectors applies to it.

Conclusion

The recent introduction of the Unified Pension Scheme by the Government of India is a major reform by the Indian Government in providing benefits to Central Government Employees. It offers an assured Pension without any market risk. However, the Pension amount depends on the corpus accumulated by the employee during their service period. However, it is advisable to consult your investment advisor for your comprehensive retirement planning, as it can help you in managing your expenses post-retirement.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

What is the minimum Pension amount under the Unified Pension Scheme?

If an employee has served a minimum period of 10 years, they will get a minimum Pension of 10,000 INR per month.

Can a private sector employee get a Pension under the Unified Pension Scheme?

No, a private sector employee cannot invest in the Unified Pension Scheme; therefore, they are not eligible to get a Pension under UPS.

Will UPS provide a Pension to the employee’s family after their death?

Yes, UPS provides a family Pension scheme, which means that in case of the death of an employee, their spouse or an eligible family member will get 60% of the Pension that the employee would have received.

Can an existing employee opt for the Unified Pension Scheme?

Yes, an existing central Government employee can opt for the Unified Pension Scheme once in their service tenure. However, once they opt for UPS, they cannot switch back to NPS.

When will the Unified Pension Scheme come into effect?

The Unified Pension Scheme came into effect from 1st April 2025.

The year 2025 presents both new opportunities and challenges for investors. The Indian economy continues to grow, and stable interest rates have further improved the investment climate. At such a time, the biggest question is where and how to invest money to get good returns while minimizing risk? In this article, we will tell you about investment options for 2025 that are reliable and can help you achieve your financial goals.

What Defines a “Good Investment” in 2026?

A good investment is one where your money is safe and grows. It’s not just about getting high returns but also about having access to your money when you need it. The right investment is one that aligns with your life and goals, such as funding your children’s education, purchasing a house, or planning for retirement.

Safety: The first rule of any investment is that your money shouldn’t be lost. If you have any doubts, choose reliable options like PPF, Post Office schemes, or government bonds. These may offer lower returns, b:ut they provide greater peace of mind.

Returns: Everyone wants their money to grow, but the smart approach is to ensure the returns are higher than the inflation rate. By taking a calculated risk and investing wisely, you can achieve a good balance between equity and debt, which can provide a return higher than the inflation rate.

Liquidity: Always keep some money in investments that can be easily accessed. You never know when you might need money in life. Fixed deposits or liquid funds are very useful in such situations.

Taxes: Earnings only matter if there’s something left after paying taxes. Some investments like NPS or SGB are considered better from a tax perspective. Therefore, always consider the tax implications before making an investment.

Goals: Every investment should have a purpose. If you plan to buy a car in two years, invest in a safe option. But if you are planning for retirement in ten years, choose growth-oriented options. The real benefit of an investment comes when it serves its purpose at the right time.

Low-Risk Investment Options

If you’re looking for an investment where your money is safe and you receive stable returns, these options are right for you. While the profits may be slightly lower, you’ll definitely have peace of mind.

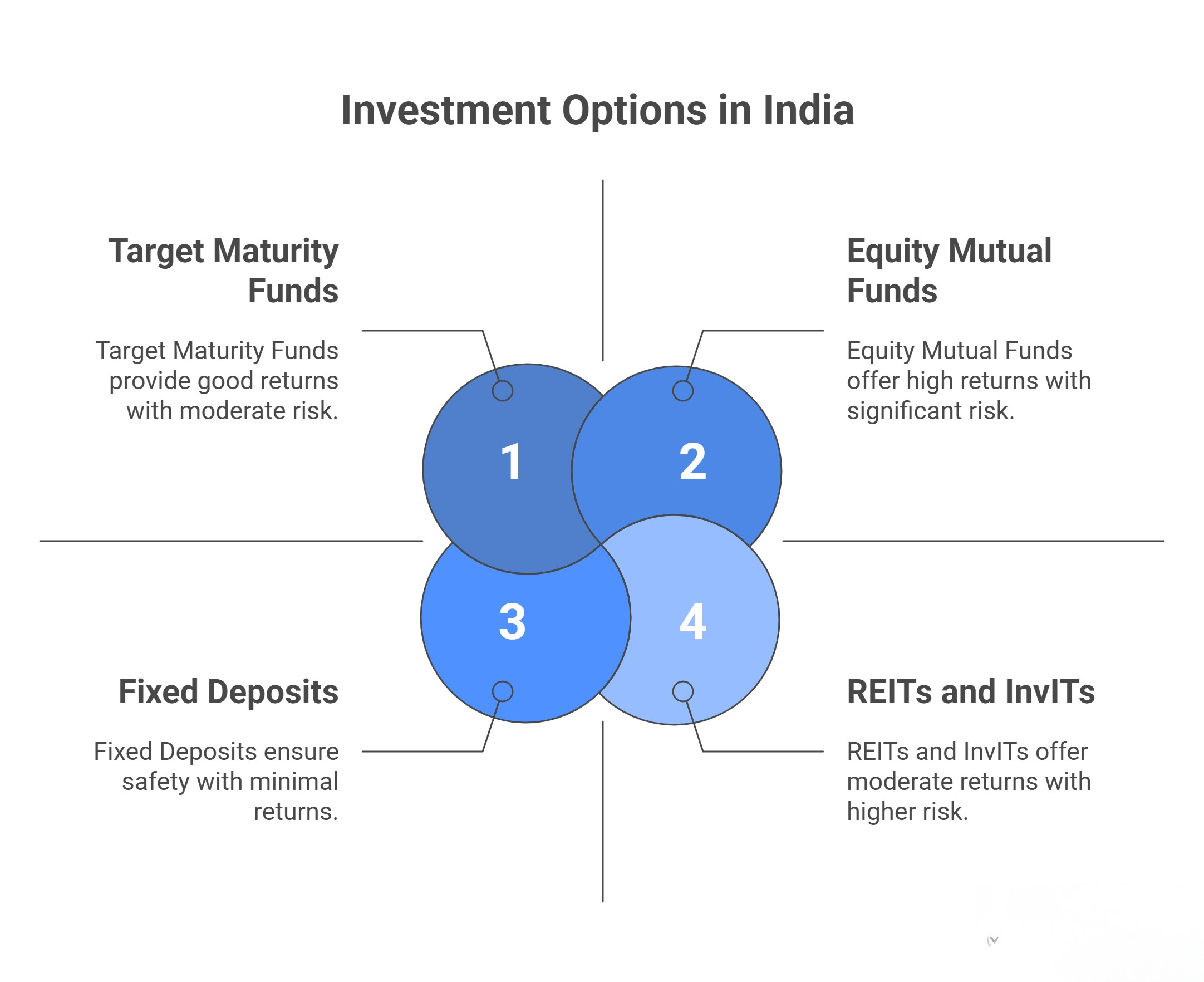

Fixed Deposits (FDs) : FDs have always been the most reliable way to make a safe investment. Here, your money is locked in for a fixed period, and you know in advance how much interest you will receive. Currently, interest rates in most banks are between 6% and 7%. This option is best for those who want stable and risk-free returns.

Public Provident Fund (PPF) : If you are looking for a safe investment for the long term, PPF is a great option. It comes with a government guarantee, an interest rate of 7.1%, and the earnings are completely tax-free. It can be used for retirement or long-term goals.

Post Office Schemes : Post office schemes like NSC and Senior Citizen Savings Scheme are suitable for investors who want stable returns and don’t want to take any risks. These schemes offer both government security and a fixed interest rate.

RBI Bonds and Treasury Bills : If you want your money to be completely safe, RBI bonds and Treasury Bills are a good option. These are issued directly by the government, so there is no risk of default.

These investments are suitable for people who want to grow their money moderately but cannot tolerate significant fluctuations. They generally offer better returns than fixed deposits and do not involve excessive risk.

Target Maturity Funds (TMFs) : These are mutual funds that have a fixed maturity date. This means you know in advance when you will receive your money. These funds include government and PSU bonds, making them safe and providing good returns.

Hybrid Mutual Funds : These funds are a mix of both equity and debt. The advantage is that returns increase when the market performs well, and losses are limited when the market falls. This is a good option for those who want to start investing in the stock market.

Sovereign Gold Bonds (SGBs) : This is the best way to invest in gold. It is government-guaranteed, provides a small annual interest, and is tax-free on maturity. It’s a good way to stabilize your portfolio in the long term.

REITs and InvITs : If you want to invest in real estate or infrastructure without buying any property, these two are excellent options. They provide regular income similar to rent, and the value of the asset can also appreciate over time.

Tax-Efficient Investments

Most people focus only on returns when investing, but they forget about the taxes they’ll have to pay. The reality is that the real benefit is what’s left after paying taxes. Therefore, before investing, it’s important to understand which method is more tax-efficient.

Debt Mutual Funds: These funds no longer offer the same indexation benefits as before, meaning any profits will be taxable according to your income tax bracket. However, due to their liquidity and transparency, they are still considered slightly better than FDs.

Sovereign Gold Bonds (SGBs): These are government-guaranteed and tax-free upon maturity. They also offer a small amount of interest annually. If you want to invest in gold but also avoid taxes, this is the cleanest and simplest method.

National Pension System (NPS): This is a good and tax-friendly option for retirement planning. It offers an additional tax deduction of up to ₹50,000, which is not available in any other scheme. In the long term, it proves to be a safe and disciplined investment.

Equity Mutual Funds and ELSS: If you want to save on taxes and grow your money, then ELSS is the right choice. It has a three-year lock-in period and offers a tax deduction of up to ₹1.5 lakh.

Not Understanding Risk : Many times, people invest simply by following others, without considering how much risk they can handle. Everyone’s financial situation is different. The stock market might be right for some, but not for others. Investing without understanding your risk tolerance is one of the biggest mistakes.

Chasing Past Returns : People often invest in funds or stocks that performed well in the previous year. But the market doesn’t always behave the same way. What was at the top yesterday might be at the bottom today. Therefore, making decisions based solely on past returns is not wise.

Investing in Too Many Funds : More funds don’t necessarily mean more profit. On the contrary, it complicates your portfolio and makes it difficult to track. Stick to a few good and reliable funds to maintain better control.

Ignoring Taxes and Charges : Many people invest only by looking at returns, but they don’t consider taxes or exit loads. These small details can significantly reduce your net return. Therefore, always understand the tax structure before investing.

Not Creating an Emergency Fund : Many people invest all their money, but don’t keep anything aside for emergencies. When a sudden need arises, they have to liquidate their investments at a loss. Always keep an emergency fund equivalent to at least six months’ worth of expenses.

Putting money in is only one aspect of investing; another is making sure it goes in the right direction. Your needs and time horizon should be taken into consideration when selecting an option. The best long-term outcomes come from consistent, deliberate investing that is not hurried. Your money will only grow steadily if you do this.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

The energy sector in India is in the news these days. Rising power demand, fluctuating oil and gas prices, and rapidly expanding renewable projects have all brought this topic back into the spotlight. Many investors are now wondering how to invest comfortably in this transition, and that’s where energy ETFs become a convenient option. In this blog, we’ll explore the available energy ETFs in India, how they work, and which option might be right for you.

What are Energy ETFs?

An Energy ETF is a fund that offers the opportunity to invest in multiple energy-related companies. These include companies such as oil and gas, power generation, power grids, refining, and sometimes renewable energy. You buy and sell them on the exchange just like stocks, but you get a mix of exposure to the entire sector; there’s no reliance on a single company.

Energy Sector ETF India vs. Broad Energy ETFs

Two types of energy ETFs are available in India:

Energy Sector ETF India : These are ETFs that follow a specific index—such as the Nifty Oil & Gas or Nifty Energy Index. They mostly include major companies in the oil, gas, and power sectors. This structure is considered more stable and less volatile.

Broad Energy or Thematic ETFs : These funds cover traditional energy as well as renewables, equipment manufacturers, grid companies, or global clean-tech firms. This option is for investors who believe in the energy transition and want long-term growth.

Why are ETFs considered better than individual stocks?

In the energy sector, the risk and performance of individual companies can vary significantly; sometimes crude prices fall, affecting refining companies, or sometimes power utilities rise, boosting demand. ETFs balance these fluctuations because:

Investments are spread across multiple companies

Risk is reduced

Research becomes easier

Long-term returns are relatively stable

Can be bought and sold at any time, just like stocks.