If you talk to someone who invested in the stock market 15-20 years ago, they will tell you how different things were back then. You could not just open an app and buy shares in seconds. You had to call a broker, place your order, and wait. Today, things have completely changed.

You can buy or sell stocks anytime, from anywhere. But even now, both options still exist, online trading and offline trading.

So which one is better? And what exactly is the difference?

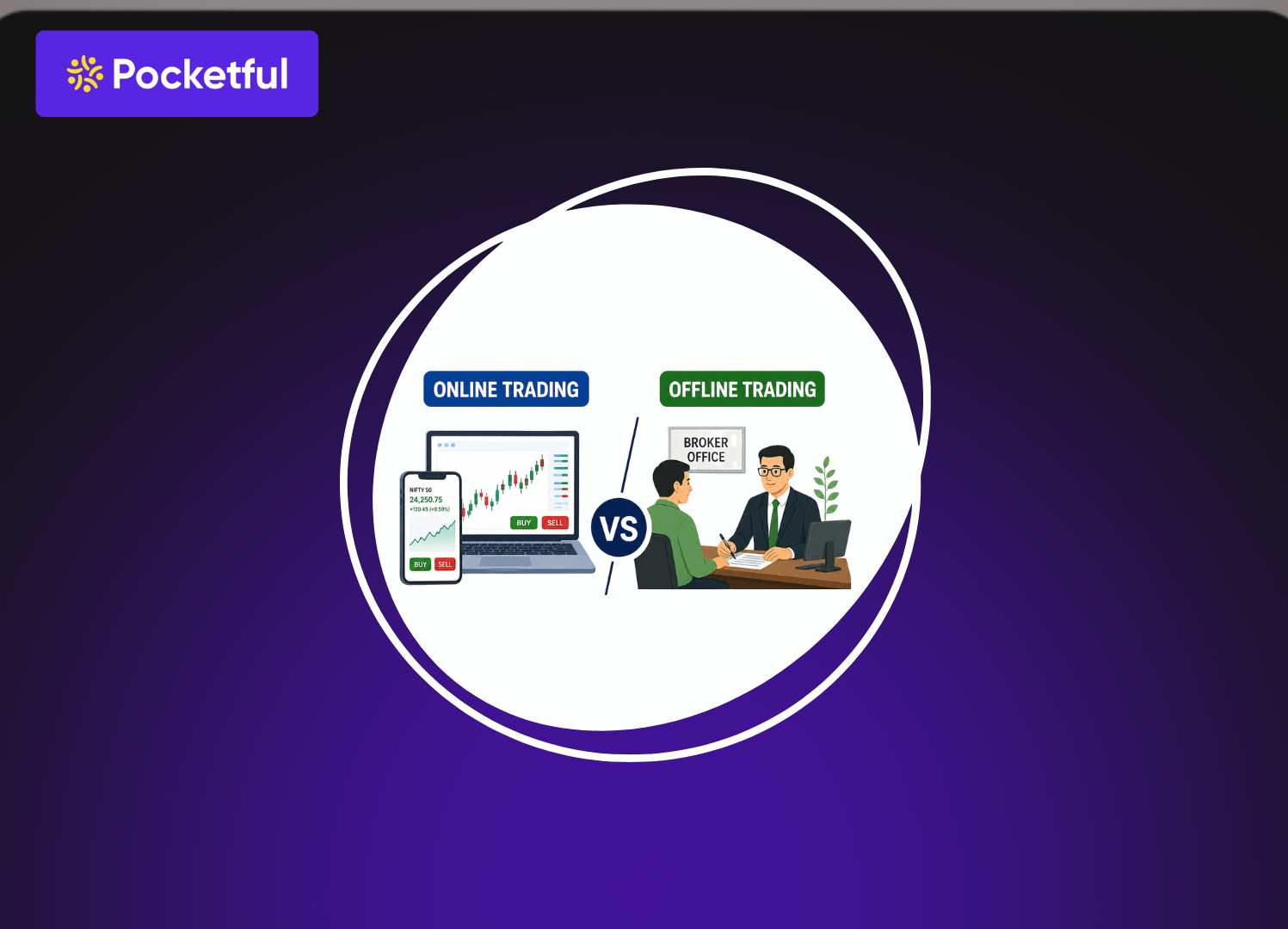

What is Online Trading?

Online trading is when you buy and sell stocks using a mobile app or website, without making any calls, and without a middleman.

You log in to your trading account, check stock prices, place your order, and it gets executed instantly. Platforms today also give charts, research tools, and portfolio tracking, all at one place.

What is Offline Trading?

Offline trading is the traditional way of trading. Here, you do not place the trade yourself. Instead, you call your broker (or sometimes visit them), tell them what you want to buy or sell, and they execute the trade for you.

The History

In the past, the stock market felt like a private club. You needed a lot of money and a personal broker to trade.

If you wanted to buy a stock, a broker literally had to shout your order to another person. It was chaotic, slow, and prone to errors.

In the 1990s, the internet changed the rules. Websites replaced phone calls, and for the first time, you could see stock prices on your screen at home.

Around 2010, the use of mobile phones turned trading into a daily habit. Apps were simple and easy to use.

That is how we evolved from offline to online trading.

Read Also: Benefits of Online Trading

Online Trading vs. Offline Trading – Table of Differences

| S. No | Basis | Online Trading | Offline Trading |

|---|---|---|---|

| 1 | Meaning | Buying and selling shares through apps or websites | Buying and selling shares through a broker (call or in person) |

| 2 | Control | You have full control over your trades | Broker executes trades on your behalf |

| 3 | Speed | Instant execution | Slower due to communication with the broker |

| 4 | Convenience | Can trade anytime, from anywhere | Limited to broker availability |

| 5 | Cost (Brokerage) | Usually low | Generally higher |

| 6 | Transparency | Real-time updates and tracking | Depends on the broker for updates |

| 9 | Risk of Errors | Less, since you place orders yourself | Possible miscommunication errors |

| 10 | Human Interaction | Minimal | High personal interaction |

Why People Prefer Online Trading Today?

- It is more convenient: With online trading, you do not have to depend on anyone. You can sit at home, open an app, and place a trade within seconds, just like using UPI or ordering food.

- Speed: Markets move quickly. Prices change every second. Online trading lets you act instantly. You see an opportunity, you place the order right away. In offline trading, even a small delay can change the price you get. That is why speed becomes a big reason people switch.

- Less Expensive: Most online platforms charge much lower fees compared to traditional brokers, which, over time, saves money, and especially if you trade regularly, those savings really add up.

- Transparency: Online platforms show everything in real time, prices, profit or loss, charts, and past orders. You do not have to call someone to ask, “What’s happening with my investment?” You can just check it yourself in a few seconds.

- No back-and-forth with brokers: In offline trading, communication can sometimes slow things down. Maybe the broker is busy, maybe there is confusion in the order; small issues like these happen.

Risks Involved of Online Trading vs. Offline Trading

Online Trading

- You might trade too much: Since everything is just a click away, it is tempting to keep buying and selling. Over time, this can hurt your returns and lead to unnecessary overtrading.

- Emotional decisions happen quickly: When prices move fast, people often react without thinking, which often leads to wrong decisions, and people end up losing their capital. You might buy out of excitement or sell out of panic.

- Knowledge gap: If you do not fully understand what you are investing in, it is easy to make poor decisions. There is no one stopping you at that moment.

Offline Trading

- Delays: You call your broker, explain your order, and then they place it. At that time, prices may already have changed, and you might not be able to buy at your desired price, which will lead to frustration.

- Miscommunication: Sometimes things get lost in conversation, wrong quantity, wrong price, or wrong order type. You say something else, your broker understands something else, which becomes very chaotic.

- Advice may not always fit you: Even though brokers guide you, their suggestions may not always match your exact goals or risk level.

What Should You Choose?

If you like doing things on your own, online trading will probably suit you better. You get full control, you can act quickly, and you do not have to depend on anyone. It also saves money on brokerage, which matters in the long run.

However, you will need to take responsibility for your decisions and keep learning along the way.

Alternatively if you prefer guidance, then offline trading will be a good fit for you. Having a broker means you can ask questions

Today, people use online platforms to place trades, but still take advice from someone they trust when needed.

Read Also: Silver ETF vs Physical Silver: Which Is Better?

Conclusion

The internet has made online trading easily accessible. But that does not mean offline trading is completely outdated. It still has its place for people who value advice and personal interaction.

At the end of the day, the best method is the one that matches your comfort level, because in investing, being consistent and confident matters more than the platform you use.

Start your online trading and investing journey with Pocketful – offering lower brokerage than peers, an easy-to-use platform, and advanced trading tools.

Frequently Asked Questions (FAQs)

Is online trading safe?

Yes, if you use trusted platforms, online trading is usually safe.

Should beginners start with online trading?

Yes, but they should learn the basics first to avoid losses.

Is offline trading outdated?

No, it is not outdated, but less commonly used now.

Which one is better overall?

For most people today, online trading is more convenient and easier

Which app is best for Online trading?

Pocketful is a good option since the app has a simple and clean user interface, which makes trading easy and fun.