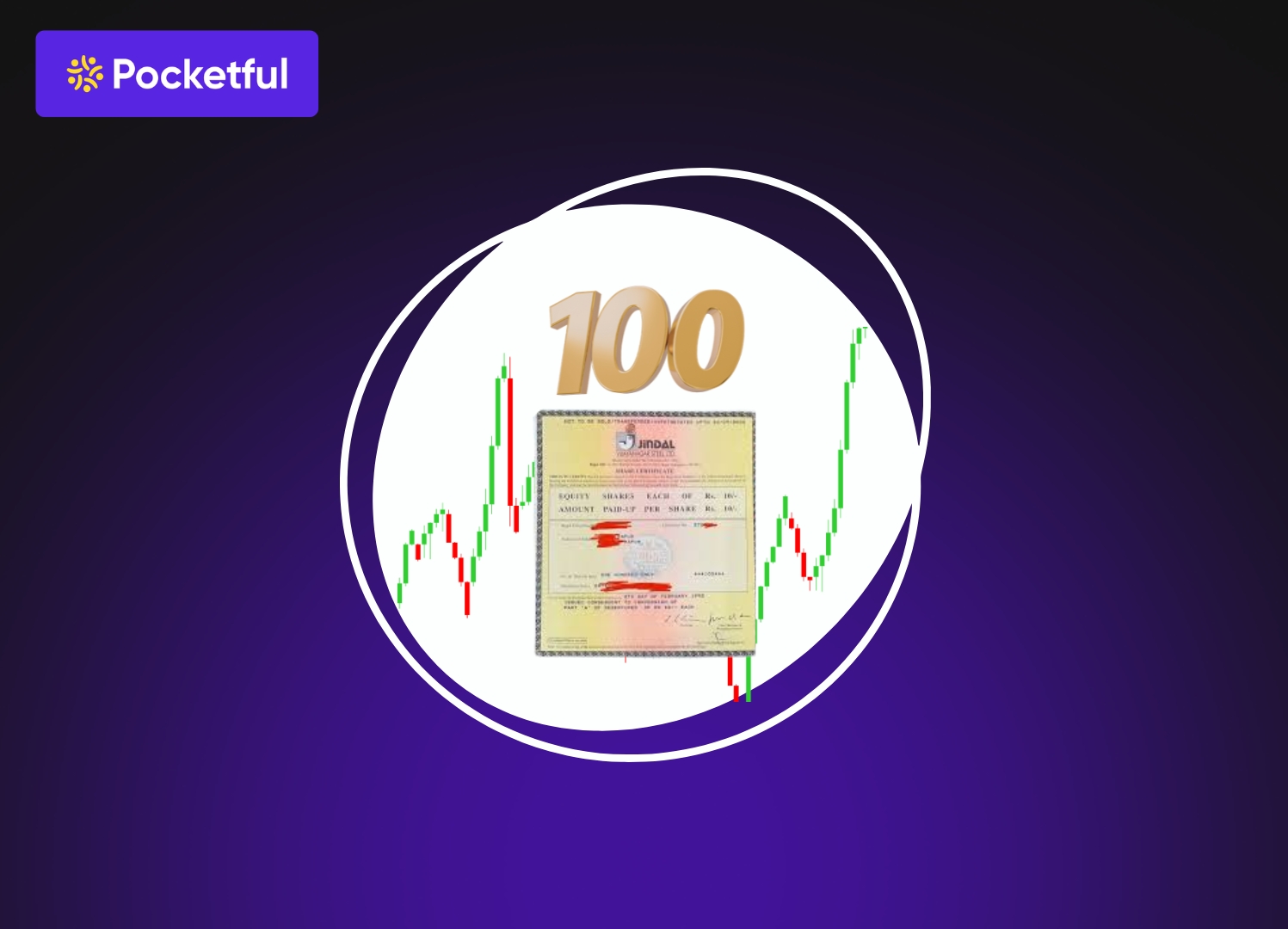

Imagine you are cleaning an old shelf and found out some old share certificate of Jindal Vijaynagar Steel Limited purchased by your father decades ago. Now, you will be looking for someone who can provide the exact valuation of those shares.

In today’s blog post, we will give you an overview of Jindal Vijayanagar Steel Limited’s history and its current value.

Evolution of Jindal Vijayanagar Steel Limited

Jindal Vijayanagar Steel Limited was founded in 1994 and was established as a part of the O.P. Jindal Group. The group entered the steel industry. The company has integrated steel plants situated in Toranagallu, Karnataka, which is often known as the hub of modern steel production. The company was listed on the Indian Stock Exchange in the year 1990. Over time, the share prices have risen exponentially and later in 2005, the company was merged into JSW Steel Limited.

Merger and Corporate Actions in Jindal Vijayanagar Steel Limited

When Jindal Vijaynagar Steel Limited was merged into JSW Steel Limited in 2005, the shareholders received new shares of JSW Steel. The shareholders will get 16 shares of JSW Steel for every one share held by them.

Later in 2017, JSW Steel split its shares in the ratio of 1:10. Which increases the number of shares.

Now let’s calculate:

100 Shares of Jindal Vijayanagar Steel Limited were converted to 1600 shares of JSW Steel

After the split, 1600 Shares of JSW Steel Limited were increased to 16000 shares.

Current Value of Jindal Vijayanagar Steel Limited Shares

Now, let’s calculate the value of Vijayanagar Steel Limited Shares in today’s terms.

As mentioned above, the 100 shares of Jindal Vijayanagar Steel Limited are converted to 16000 shares of JSW Steel Limited.

The formula to calculate the value of a share is as follows:

Quantity of Shares * Current Price of Share

The current share price of JSW Steel Limited as of 25th Feb 2026 is 1274.

Based on the above formula, the value of JSW Steel shares will be calculated as follows:

16000 * 1274

= 2,03,84,000 INR

It is roughly 2 Crore INR.

Summary of 100 Jindal Vijaynagar Steel Limited Shares

| Particular | Result |

|---|---|

| Old Shares of Jindal Vijaynagar Steel Limited | 100 |

| Merger of Jindal Vijaynagar Steel Limited into JSW Steel Limited | 1600 JSW Steel Limited Shares |

| Stock Split of JSW Steel Shares | 16000 JSW Steel Limited Shares |

| Current Price of JSW Steel Shares (As of 26th Feb 2026) | 1274 |

| Current Value of Shares | 2,03,84,000 INR |

Process to Convert Physical Shares into Demat Form

The steps to convert physical shares into demat form are as follows:

- Opening a Demat Account: The first step toward converting physical shares into demat form is opening a demat account with a broker. Pocketful offers an opportunity to open a lifetime free demat and trading account; it also offers zero brokerage on delivery trades.

- DRF Form: The next step after opening a demat account is to complete the DRF (Dematerialisation Request Form). The form is available with your broker. One can easily fill out the form, which requires basic details such as the company’s ISIN, the quantity of shares to be dematerialised, etc.

- Submitting Form: Once the form is filled, you can send it to your broker, who, after scrutiny, finally sends it to RTA for final credit of shares in your demat account. The physical shares also need to be sent along with the DRF form.

- Credit of Shares: After the final verification by the RTA, the shares were credited in the demat account of the holder. After which, if they want, they can trade them.

Key Factors to Consider Before Converting

The key factors to consider before converting the physical shares into demat form are as follows:

- Existence of Company: First, an investor needs to check whether the company is in existence or not. If the company is delisted from the exchange, then there is no option to convert such shares into demat form.

- Name Match: One should check the name printed on the share certificate against their PAN number and in the demat account. All the names must have an exact match else an affidavit needs to be submitted.

- Signature: The signature on the DRF form must be similar to the signature mentioned in the RTA records. If the signature does not match, the bank verification is required.

- IEPF Fund: If the dividend or the shares are unclaimed for seven consecutive years, they will automatically be transferred to the Investor Education Protection Fund.

- Corporate Actions: The next step would be checking the corporate actions in the company. The old physical shares may have undergone several corporate actions such as stock splits, bonuses, rights issues, etc.

Conclusion

On a concluding note, old physical shares carrying 100 shares of Jindal Vijaynagar Steel Limited would have valued more than 2 Crores today. Which indicates that the modest investment of a few INR can be valued as a huge sum after a few decades, which is possible only because of several corporate actions, such as the merger of companies and split of shares. However, converting physical shares into demat form is mandatory to realise the actual value of those stocks.

Download Pocketful for market insights and finance blogs. Enjoy zero brokerage on delivery trades, along with zero AMC and zero account opening charges—making investing smarter and more cost-effective. Therefore, it is advisable to consult your investment advisor if you have any share certificates of Jindal Vijaynagar Steel Limited in physical form.

Frequently Asked Questions (FAQs)

Are the old Jindal Vijaynagar Steel Limited share certificates still valid today?

Yes, old physical shares of Jindal Vijaynagar Steel Limited are still valid today. However, to realise the actual value, one must get it dematerialised at the earliest possible.

Jindal Vijaynagar Steel Limited has been converted into which company shares?

The Jindal Vijaynagar Steel Limited company’s shares were converted into the JSW Steel Limited after the merger.

How much time is required to get the physical shares of Jindal Vijaynagar Steel converted into demat form?

Generally, it takes around 15-20 working days once the form is submitted to the RTA to get the shares credited into the demat account.

What is the current value of 100 Jindal Vijaynagar Steel Limited shares?

The current value of 100 Jindal Vijaynagar Steel Limited is around 2 crores after including all the major corporate actions.

How to convert the physical shares of Jindal Vijaynagar Steel Limited into demat form?

To convert the physical shares of Jindal Vijaynagar Steel Limited into demat form, one is required to open a demat account and submit the DRF form along with the physical shares to the RTA.