Dr Reddy’s Laboratories Case Study was established in the pharma and health segment in 1984. The company currently offers a wide range of pharmaceuticals both nationally and internationally. Today’s blog will include details on market data, KPIs, Financials, and SWOT analysis.

Dr. Reddy’s Laboratories Overview

Dr. Reddy’s Laboratories is one of the leading pharmaceutical companies in the country. It offers a wide variety of pharmaceutical products, active ingredients, and more. The company’s purpose is to treat its customers with innovative products at an affordable price point.

| Company Type | Public |

| Founder | Anji Reddy |

| Industry | Pharmaceuticals |

| Founded | 1984 |

Acquisitions and Joint Ventures

- Acquisition of Betapharm

Betapharm is one of the leading pharmaceutical companies in Germany. The integration of these companies allows access to each other’s markets, helping to reach more patients and creating a great impact on healthcare.

- Joint Venture with FUJIFILM Corporation

This alliance works on increasing advanced technologies to diagnose patients at affordable prices and provide access to healthcare to the expansive population.

Awards and Achievements

- 2021 – CII Industrial Innovation

- 2022 – Bloomberg Gender-Equality Index

- 2021 – Indo-American Chamber of Commerce

- 2023 – India Risk Management Award

Dr. Reddy’s Laboratories Business Model

Products

The company’s primarily deals in pharmaceutical products such as:

- Diagnostics

- Biologics

- Generic drugs

- Over-the-counter drugs

- Vaccines.

Business Strategy

The company is known to employ multiple strategies in order to maintain and boost market share. Some of these strategies are:

- Biosimilar opportunities: Dr. Reddy Lab. is securing bio-similar substances derived from living organisms to create active drug substances.

- Investing in R&D: This strategy has led to the next wave of growth and also helps to get the product pipeline ready for the market.

- Sustainability: The company is incorporating initiatives to sustain the health of the planet.

- Deliver Future growth: The company is heavily invested in its production game and hopes for an increase in volume and product portfolio.

Market Data

| Market Cap | ₹ 1,02,725 Cr. |

|---|---|

| Stock P/E | 19.6 |

| ROCE | 26.7 % |

| Current Price | ₹ 6,158 |

| Book Value | ₹ 1,528 |

| ROE | 21.6 % |

| High / Low | ₹ 6,506 / 4,383 |

| Dividend Yield | 0.65 % |

| Face Value | ₹ 5.00 |

Read Also: GSK Pharma Case Study: Business Model, Product Portfolio, and SWOT Analysis

Dr. Reddy’s Laboratories Financial Highlights

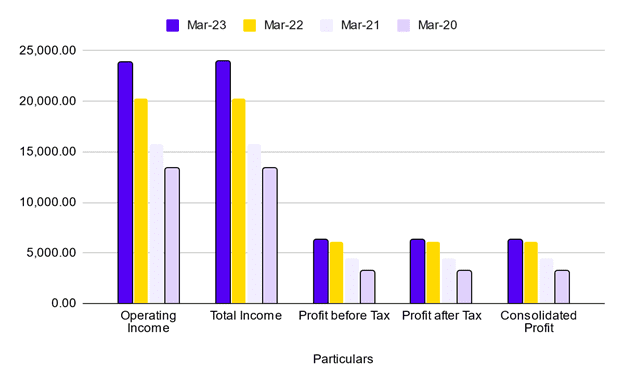

Income Statement

| Particulars | Mar-23 | Mar-22 | Mar-20 | Mar-20 |

|---|---|---|---|---|

| Operating Revenue | 24,669.70 | 21,545.20 | 19,047.50 | 17,517.00 |

| Total Income | 25,725.20 | 22,029.90 | 19,338.90 | 18,137.60 |

| Total Expenditure | 18,320.70 | 17,777.80 | 15,177.60 | 15,046.60 |

| Profit before Tax | 6,048.50 | 3,061.40 | 2,883.50 | 1,885.70 |

| Consolidated Profit | 4,507.30 | 2,182.50 | 1,951.60 | 2,026.00 |

The graph and table indicate a growing trend over the past four years. Revenue grew continuously during this period, and the same was carried over to the profit.

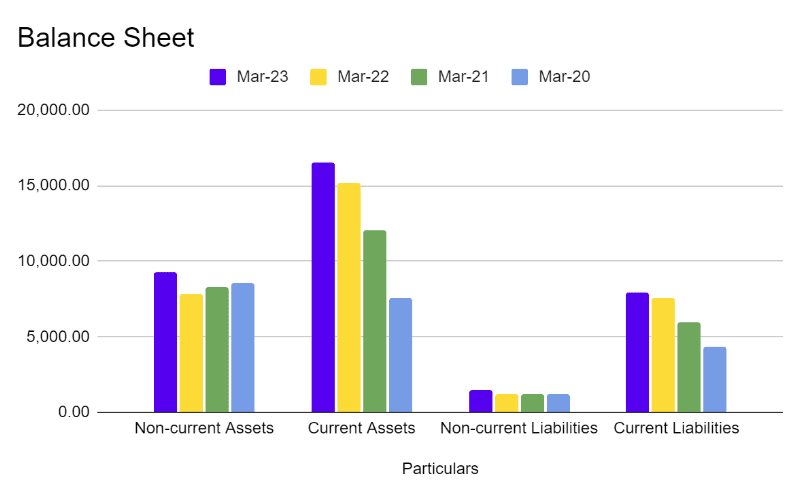

Balance Sheet

| Particulars | Mar-23 | Mar-22 | Mar-21 | Mar-20 |

|---|---|---|---|---|

| Non-Current Liabilities | 460.9 | 768.70 | 871.3 | 412.40 |

| Current Liabilities | 8,572.10 | 9,765.80 | 8,103.80 | 7,214.10 |

| Non-Current Assets | 11,263.80 | 10,682.00 | 10,997.90 | 9,406.30 |

| Current Assets | 20,316.10 | 17,787.90 | 14,535.20 | 12,599.10 |

The balance sheet shows the low amount of debt in its capital structure. This is a positive sign as it reduces the risk of financial burden during periods of low profitability.

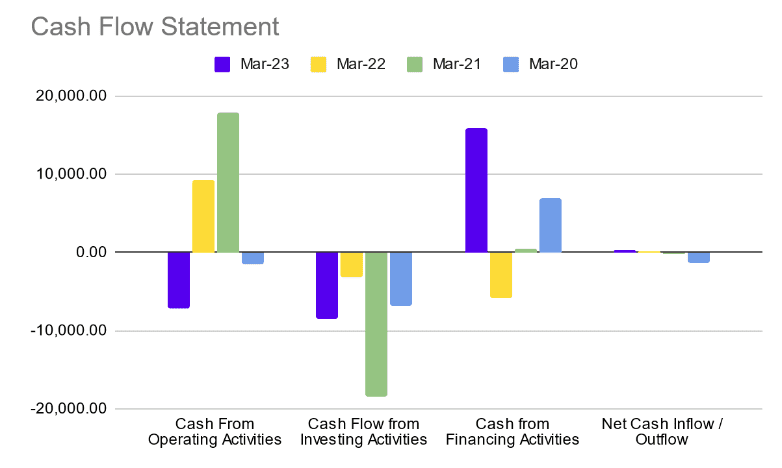

Cash Flow Statement

| Particulars | Mar-23 | Mar-22 | Mar-21 | Mar-20 |

|---|---|---|---|---|

| Cash From Operating Activities | 5,887.50 | 2,810.80 | 3,570.30 | 2,984.10 |

| Cash Flow from Investing Activities | -4,137.30 | -2,638.70 | -2,266.00 | -492.30 |

| Cash from Financing Activities | -2,686.10 | -242.20 | -29.80 | -2,515.90 |

| Net Cash Inflow / Outflow | -935.90 | -70.10 | 1,274.50 | -24.10 |

Cash flow from operating activities indicates a steady position and consistent investment and financing outflows. Investment outflows result in increased income later in life, and debt repayment outflows demonstrate debt reduction.

Profitability Ratios

| Particulars | Mar-23 | Mar-22 | Mar-21 | Mar-20 |

|---|---|---|---|---|

| ROCE (%) | 26.22 | 14.59 | 15.49 | 11.12 |

| ROE (%) | 21.36 | 11.93 | 11.82 | 13.76 |

| ROA (%) | 15.01 | 8.08 | 8.21 | 9.20 |

| EBIT Margin (%) | 20.67 | 12.08 | 13.87 | 7.46 |

| Net Margin (%) | 17.52 | 9.91 | 10.09 | 11.17 |

Dr. Reddy’s Laboratories SWOT Analysis

The SWOT analysis of Dr. Reddy’s Laboratories highlights the company’s strengths, weaknesses, opportunities, and threats in the pharmaceutical industry.

Strengths

- Dr Reddy’s Laboratories products enjoy strong branding power in the biotechnology and pharmaceutical industries. Due to its higher brand value, the company became popular after Ranbaxy and GSK.

- The company had invested time and resources in Research and development to bring new drugs to the market.

- The business mainly focuses on its pricing strategy, which means providing products at reasonable prices.

Weaknesses

- The pharmaceutical industry is an unpredictable segment.

- In the pharmaceutical segment, numerous competitors are making it hard to sustain in the market.

- The regulatory frameworks can be complex and time-consuming for the company.

Opportunities

- The company can focus on creating a base in emerging markets and improving its product pipeline.

- A good investment in Research and development can lead the company to formulate new products.

Threats

- The company operates in an extremely stringent regulatory environment, and failure to comply with these norms can invite severe penalties.

- The Indian government is heavily pushing generic medicines, and as more and more people become aware of this facility, the company may see an effect in sales.

Read Also: Case Study on Procter & Gamble Marketing Strategy

Conclusion

Dr Reddy’s Laboratories is a well-known pharmaceutical brand with a global identity. The company enjoys its brand value and identity and has made successful acquisitions. It acknowledges new opportunities, reaches potential clients, and has international exposure.

While the company shows great potential, it is important to perform your analysis before investing.

FAQs

Why is Dr. Reddy’s Laboratories famous?

The company is famous for dermatology, oncology, pain management, urology, and cardiovascular medicines and pharmaceutical products.

who is the current ceo of dr. reddy?

The current CEO of Dr. Reddy’s Laboratories is Erez Israeli. He took over as the CEO in 2020, bringing extensive leadership experience to the company. Before becoming CEO, Erez Israeli held several senior positions at Teva Pharmaceuticals, and his leadership is focused on continuing the company’s growth and expanding its global presence.

When was Dr. Reddy Laboratories established?

It was established in 1984.

Who is the owner of Dr reddy’s laboratories?

Dr. Reddy’s Laboratories was founded by Dr. Kallam Anji Reddy in 1984. He was the chairman and managing director of the company until his passing in 2013. After his death, the leadership passed on to his son, G.V. Prasad, who currently serves as the Co-Chairman and CEO of Dr. Reddy’s Laboratories. G.V. Prasad plays a key role in the strategic direction of the company.

Who was the founder of Dr. Reddy Laboratories?

Kallam Anji Reddy was the founder of Dr. Reddy Laboratories.

Who is the CEO of Dr. Reddy Laboratories?

Erez Israeli is the current CEO of Dr. Reddy Laboratories.