When we hear the word “bond,” we usually think of a secure and reliable way to invest. You give the issuer money, they pay you interest/coupon, and then you get your invested money back at maturity. Isn’t that too simple? Perhaps not always.

Callable bonds are a kind of bond with an embedded call option. These bonds let the company pay you back early, like paying off a loan before the due date. It might sound strange, but there is a reason for it, and it could impact your returns.

In this blog, we will explain what callable bonds are, why companies prefer issuing them, how they work, and what you should be careful of if you want to buy them.

Understanding Callable Bonds

Callable bonds, sometimes referred to as redeemable bonds, are the kinds of bonds in which the issuer may choose to repay you before the bond’s actual maturity date. For example, if a company issues a bond with a 10-year term, they may decide to return your money and stop giving you interest after five or six years. They are “calling” the bond at that point.

Let us say you buy a bond from XYZ Ltd. It should mature in ten years and pay you 8% interest annually. However, market interest rates fall to 7% after five years. XYZ chooses to call back the bond, simply returning your money early and issuing new bonds at the lower rate, after realising it can now borrow money at a lower interest rate.

Example

Assume you purchase a bond issued by ABC Ltd. This is how the transaction looks like:

You give them a ₹1,000 loan. They guarantee to give you ₹80 a year, or 8% interest or coupon. The bond has a 10-year term. However, after five years, the company may choose to “call” the bond.

What You anticipate: In ten years, you expect to earn ₹80 annually and receive your ₹1,000 back along with ₹800 in coupon payments.

However, here is the catch: Suppose that after five years, market interest rates fall to 7%. Now the issuer will think that why are they still paying 8% when they could borrow money from someone else at just 7%?” Thus, the bond is called back. In simple terms, they return your ₹1,000 and stop coupon payments after that.

Now, How Does That Affect You? You received your ₹1,000 back. However, you must now reinvest that ₹1,000, and since interest rates are lower, your future earnings will be lower.

Companies prefer issuing callable bonds because of the following reasons:

1. To Reduce Interest Expenses

Suppose a business borrows funds by issuing bonds with a 9% coupon rate. Interest rates drop to 8% a few years later. The company now has the option to pay back the bonds early and issue new bonds at a lower interest rate.

2. Adaptability Always Pays Off

Markets fluctuate, and objectives change. Companies can control their debt with callable bonds. Instead of being stuck with the bonds for the long run, they can easily call them back if they are doing well financially or no longer need the borrowed funds.

3. Restructuring Debt

Companies prefer to be a few steps ahead. They would prefer the option to restructure their debt at a later time if they believe that interest rates will decrease or that their credit score will rise. They are able to keep that door open through callable bonds.

4. Investors Continue to Express Interest

Callable bonds do carry some risk for investors, primarily the possibility that the bond will be called early. However, issuers generally offer higher interest rates to offset this risk. Thus, a lot of investors are still happy about buying them.

Adding them to your portfolio can be very helpful. Let’s find out what makes them interesting:

1. They usually pay more interest

Callable bonds usually have a higher interest rate than regular bonds. Why? The company might pay you back early, so they give you more to make it worth your while. If you want better returns on fixed income, this could be a good option.

2. Early payout with a bonus

If a bond is called before maturity, the company returns your principal along with a small extra amount known as the call premium. This means you could receive your money back plus a bonus earlier than expected.

3. Good When Interest Rates Are High

When interest rates are high, you can get higher payouts on callable bonds for as long as the bond is active. Even if the bond gets called, you have still made a good amount of money in the meantime.

4. Good for Goals That Will Take a While to Reach

Are you making plans for something that will happen in a few years, like buying a house or paying for your child’s education? Callable bonds might work well, especially since many of them get called back before they reach full maturity.

Risks Involved in Callable Bonds

Some of the risks involved when investing in callable bonds is given below:

1. They Can Lower Your Expected Returns

One of the worst things callable bonds is that the company has the right to call the bond before its maturity . So, if you thought you would earn interest for 10 years before investing and they call it back in 5 years, then you might have to reinvest and settle for lower interest earnings or returns.

2. Planning for the future is not always easy.

You know exactly for how long regular bonds will last and how much money you will make. But with callable bonds, there is always a question mark: “Will they call it back?” If yes, then when? It is a little harder to plan for the long term when things are so unpredictable.

3. You could miss out on bigger gains.

Let us say that interest rates go down and bond prices go up. That would be great most of the time! But if the bond is called right when prices are going up, you lose out on those possible profits, which obviously does not feel good.

The issuer can buy the bond back early, before maturity

You can sell the bond back early if you want out

Objective

Usually happens when interest rates drop, they want to refinance at cheaper rates

Usually, when interest rates go up, you want to reinvest at a better rate

Who controls the timing?

The issuer calls the bonds; you have no say if they decide to call the bonds

You get to choose when to exit (within the allowed window)

Risk

You might stop receiving the interest payments earlier than expected

Not much risk, you have the flexibility to exit if needed

Benefit

Higher interest rates, they are paying you more to take on the call risk

More control, you are not locked in if things change

Coupon

Generally higher, because of the risk you are taking on

Usually lower, since you have the advantage to exit early

Where do you find these?

Common in corporate and some government bonds

Not as common, found in select government or structured bonds

Conclusion

Callable bonds offer a mix of pros and cons. They typically pay higher interest, which is attractive, but the issuer has the option to end the agreement early.So, are they worth it? Callable bonds can be a smart option if you are comfortable with some uncertainty in exchange for potentially better returns.

In the end, like any investment, it depends on your financial goals, your risk tolerance, and how comfortable you are with unpredictability. It is advised to consult a financial advisor before investing in callable bonds.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Yes, most of the time. They offer a higher interest rate to make up for the risk that they could be called early.

If a bond is called early, could I lose money?

Not usually; you will get your principal back. But you will not get the interest payments you were expecting till maturity and may have to reinvest the capital at a lower interest rate.

When can issuer call a bond?

After a certain amount of time, called the “call protection period,” which is usually a few years after the bond is issued.

Are callable bonds a good investment for the long term?

They can be, especially if you want to make more money, but only if you can deal with some uncertainty.

What happens if the bond never gets called?

If the bond is not called then it is just like a regular bond, you keep getting interest payments until the bond matures.

In today’s volatile market, if you are looking for an investment that will give you both regular income and capital protection over a fixed period of time, then a straight bond can be an excellent option. This traditional bond type is beneficial for long-term investors, retired people and those who want stable returns while being risk averse.

In this blog, we will tell you how a straight bond works, what are its special features, what are the benefits, and what risks need to be kept in mind – that too in simple language and from a practical perspective.

What is a Straight Bond?

Straight Bond is a simple fixed income security in which the investor gets a fixed coupon payment (interest) at fixed intervals and the entire principal is returned on maturity.Unlike convertible bonds, it does not offer the option to convert into equity, and the issuer cannot redeem it before maturity (non-callable). It is also called “Plain Vanilla Bond” because it does not have any complications.

How Does It Work ?

When you invest in a straight bond, you basically give a loan to the company or government issuing the bond for a fixed period of time. In return, you get a fixed interest every 6 months or annually. When the bond matures, your entire principal is returned to you.

For example, if you invest ₹1 lakh in a 5-year bond at 8% coupon rate, you will earn ₹8,000 interest every year and get back ₹1 lakh after 5 years.

Straight Bond vs Other Bonds

Features

Straight Bond

Callable Bond

Convertible Bond

Coupon Rate

Fixed

Fixed/Floating

Fixed/Reduced

Maturity

Fixed

The issuer may call the issuer before time

Fixed, but conversion option

Risk Level

Less

A little more

More (Link to Equity)

Conversion/Call Option

No

Yes

Yes

Key Features of a Straight Bond

Straight Bond is considered a stable and transparent investment option, especially for investors who prefer regular income and capital protection. Below we explain some of its important features in a simple and professional manner:

1. Fixed Coupon Payments

In Straight Bond, you get a fixed interest (coupon) every year or every 6 months. These returns are pre-determined, which keeps your income stable.

Example: If the coupon rate is 7% and you have bought a bond of ₹1 lakh, then you will get ₹7,000 interest every year.

2. Fixed Maturity Date

Every Straight Bond has a fixed period – like 3, 5 or 10 years. On this date your entire principal is returned. This makes it easier for the investor to plan his funds.

3. Non-Callable Nature

The special thing about Straight Bond is that the institution issuing it cannot withdraw it before maturity. That is, you get the guarantee of both the fixed interest and the period, due to which there is no sudden change in the return.

4. Credit Rating Dependency

The safety of such bonds depends largely on the credit rating of the issuer. Bonds with better ratings (such as AAA) are considered more secure. Before investing, definitely check the ratings of agencies like CRISIL, ICRA or S&P.

5. Secondary Market Liquidity

Although straight bonds are usually bought for hold-to-maturity, they can also be sold in NSE/BSE or over-the-counter (OTC) markets. Some bonds have good liquidity, while others have limited liquidity-so consider this aspect as well before buying.

It is ideal for investors who want to add a low-volatility and tax-efficient option to their portfolio.

Predictable Income Stream : A straight bond pays you fixed interest at fixed times, say, a 7% coupon every year. It is ideal for those looking for passive income after retirement or while working.

Capital Preservation : The very nature of bonds is such that the principal amount of your investment is protected unless the issuer defaults. Hence, it is much safer than high-risk options like equities.

Simplicity & Transparency : A straight bond is free from any kind of complexity (such as conversion, call or derivative link). This gives the investor complete transparency about when and how much return they will get.

Portfolio Diversification : If you have invested all your money in the stock market or real estate, then bonds provide stability to your portfolio. This reduces your overall risk.

Low Correlation with Stocks : The performance of bonds is quite different from the stock market. So even when the stock market falls, bonds continue to give you a fixed return it becomes a kind of hedge.

Real-Life Case Study:

Sandeep is a 55-year-old retiring employee of a private company. He invested ₹10 lakh in a 5-year AAA rated straight bond with a coupon rate of 7.5%. This started giving him a steady income of ₹75,000 every year, and after 5 years he got his entire principal back safely. This became an important part of his retirement plan.

Although straight bonds are considered a stable and safe investment option, there are some risks associated with it which must be assessed before investing. Below we are understanding these major risk factors in a simple and professional way:

1. Interest Rate Risk

The prices of bonds and interest rates have an inverse relationship. When interest rates rise in the market, the attractiveness of old straight bonds decreases because their coupon is fixed. This can reduce their market value.

Example : You invested in a bond with a 7% coupon, but the new rates in the market became 8%, then your bond will trade at a discount. Floating rate bonds perform better in this situation because their coupon keeps changing according to the market rate.

2. Credit Risk

If the financial position of the company issuing the bond weakens or it defaults, then you may have trouble getting interest or principal. That is why you should check the credit rating (like AAA, AA) before investing.

3. Inflation Risk

If the inflation rate becomes very high, then the fixed coupon you get from your bond actually reduces.

Example: Even a bond with 6% interest will seem ineffective if the inflation rate is above 7%.

4. Liquidity Risk

Not every straight bond can be sold easily. If you suddenly need money and the demand for the bond in the market is low, then you may have to sell it at a loss.

5. Reinvestment Risk

If you want to reinvest the interest you get from the coupon, and by then the market rate has decreased, then your total return may decrease. This is especially seen in long-term bonds.

Who Should Invest in Straight Bonds?

Low-risk investors : For those who want to keep their capital safe and prefer to stay away from the volatility of the stock market, Straight Bond is an ideal option. It provides fixed income, which reduces uncertainty in returns.

Retired and senior citizens : Retired people who need stable and reliable income every year can get regular coupon income from this bond. This helps them meet their monthly needs.

Medium to long-term investors : If your investment period is between 3 to 10 years and you are planning without early exit, then straight bond proves to be a stable and planning-friendly option.

Those seeking stability in portfolio : For investors whose portfolio is predominantly in equities, the bond acts as a balancing tool and provides protection from volatility.

Fixed income planners : For those who want to plan their income in advance, this bond offers a reliable and easy structure.

Check the credit rating : It is very important to check the credit rating of any straight bond before investing in it. Agencies like CRISIL, ICRA, S&P and Moody’s rate the credit quality of the issuer. Bonds with AAA rating are considered the safest, while low-rated bonds have a higher risk of default.

Understand the Yield to Maturity (YTM) : Investing just by looking at the coupon rate is not enough. YTM i.e. Yield to Maturity tells you how much total return you will get if you hold the bond till maturity. It is calculated keeping in mind both the buy price and the coupon.

Keep diversity in issuers : Avoid investing all the money in a single company or sector. Always spread the risk by investing in different companies and government issues.

Keep an eye on macroeconomic factors : Factors like repo rate, inflation rate, fiscal deficit directly affect the bond yield. Keeping an eye on these helps in making the right decision while investing.

Choose the right investment platform : You can buy straight bonds through the RBI Retail Direct portal, NSE/BSE bond platform, or approved brokers. If you want to avoid direct investment, you can also invest through mutual funds.

Straight bonds are a traditional investment option that offer fixed returns and capital protection. Due to their simplicity and stability, they are favored by investors who prefer low risk and long-term planning. Amid market uncertainties, these bonds serve as a source of secure income. However, investors should consider credit risk, as the issuer’s ability to meet interest and principal payments depends on their financial strength. Maximizing the benefits of straight bonds requires careful attention to factors such as maturity period, credit rating, and the credibility of the issuer.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Investing today is no longer just about chasing higher profits. Many investors are also seeking ways to create a positive impact on society. Social Bonds have become one such modern investment vehicle that offer financial returns as well as an opportunity to participate in social development. Whether it is education, health or helping the poor, investments made through these bonds directly support communities that need them the most.

In this blog, we will explore how social bonds work, the benefits they offer, and how they are reshaping the future of finance.

What are Social Bonds?

Social Bonds are a type of debt instrument used to raise capital for social welfare projects. They are issued by governments, companies or international organizations, and the money raised from them is invested only in projects that aim to generate social impact.

Social Bonds Purpose

The main objective of these bonds is to invest in sectors that directly benefit the weaker sections of the society. The major focus areas include:

Affordable Housing

Primary education and digital literacy

Public health and hygiene

Employment generation for the unemployed

Women empowerment and support to the elderly

Comparison with Green Bonds and Sustainability Bonds

While Green Bonds focus on environmental projects such as renewable energy, Social Bonds prioritise social development. Sustainability Bonds are a mix of the two they cover both environmental and social projects.

Who issues Social Bonds?

These bonds can be issued by many entities:

Government bodies

Public & Private Corporations

Multilateral Institutions such as the World Bank, IFC etc.

Example : In 2020, IFC significantly expanded its social bond program, issuing $1.6 billion across 11 bonds to support businesses and vulnerable groups during COVID-19. This brought IFC’s cumulative social bond issuance to over $3.8 billion since the program began in 2017.

Social bonds follow a set process that focuses on transparency, purposeful funding, and social impact. Below is a simple process to explain how they work:

Issuers : Social bonds can be issued by a range of entities such as governments, public and private banks, large companies, and development agencies to raise funds for social welfare projects.

Investors : These bonds are typically funded by institutional investors such as mutual funds, pension funds, insurance companies, and ESG (Environmental, Social, Governance)-focused investors. In some cases, retail investors also have indirect access.

Fund Allocation & Process : Money raised through social bonds is invested in pre-determined social projects such as affordable housing, education, healthcare, women empowerment, etc. There is regular reporting and monitoring so that investors are clear that the funds are being used in the right place.

Certification & Guidelines : Most social bonds are issued in accordance with ICMA (International Capital Market Association) Social Bond Principles (SBP). These principles ensure that:

Fund utilisation is transparent

Monitoring and reporting is done at every stage

Social impact is assessed

Returns + Impact : Social bonds usually offer market-competitive returns, i.e. the returns are the same as any other corporate or government bond. But there is an added benefit that your money also brings about social change.

Key Areas Where Social Bonds Make an Impact

The aim of social bonds is not just to invest but to bring about positive change in the areas of society where it is needed the most. These bonds specifically fund projects that address the following key social needs

Affordable Housing Scheme: These bonds fund the redevelopment of urban slums and affordable housing projects in rural areas.

Education and Digital Literacy: Improvement of government schools, expansion of e-learning facilities and giving scholarships to needy students are part of them.

Health Services: They contribute to the preparation of rural health clinics, maternal-child health schemes and emergency facilities during epidemics.

Help to the weaker sections: Support schemes are started for the LGBTQ+ community, the elderly, migrant laborers and the disabled.

Small industries and employment: MSMEs get easy finance and skill development programs for the youth are supported.

Disaster Relief: Social bonds also play an important role in relief and rehabilitation operations during natural disasters.

Why Social Bonds are Important: Benefits for everyone

Social bonds provide financial support to social projects, but each party benefits at different levels.

Benefits for Investors

Just like traditional bonds, fixed income is accompanied by a meaningful purpose.

Including them in an ESG portfolio also highlights the investor’s social responsibility.

A strong option for diversification especially for investors with a long-term vision.

Benefits for Issuer

A reliable way to raise new capital, that too from investors who value social values.

Improves the brand value and public image of the institution, especially when it uses funds transparently.

Helps maintain investor confidence in the long term.

Impact on society

Funds are directed to underserved communities in areas like education, healthcare, and housing.

Local employment, women empowerment, and upliftment of underprivileged communities.

Contribution to the economy

Social stability and increased productivity provide long-term benefits to the economy.

The government gets help from private investment for social schemes, which reduces the financial burden.

How to invest in social bonds in India?

Investing in social bonds is slowly gaining popularity in India, especially among investors who are looking for safe returns along with social change. Here’s how:

Via public issue or private placement : Some government entities (like NABARD, NHAI, REC etc.) or corporates issue social bonds from time to time. You can buy them:

Via private placement through SEBI registered brokers or dealers

Via ESG or Social-Themed Mutual Funds : As of now, direct access to social bonds for retail investors is limited, but several AMCs (like SBI MF, Axis MF, ICICI Prudential) are running mutual funds that invest in bonds with a social or ESG framework.

Social Bonds may serve a good social purpose, but it is important to understand some of their potential risks before investing:

Social Impact Risk : The purpose of these bonds is to bring positive change in the society. But many times these projects do not reach the stipulated time or impact target. If social goals are not met, it can affect investor confidence.

Credit Risk : Social Bonds are mostly issued by government agencies or companies. If the issuer’s credit rating is weak or the company falls into a financial crisis, there is a risk of default.

Transparency Risk : Reporting and tracking of social impact is necessary in every bond issue. But reporting standards are not the same in many countries, including India, which can make it difficult to get the right data.

Liquidity Risk : Social Bonds are not always liquid in the market. That is, if you need and want to sell the bond, it may be difficult to find an immediate buyer.

Regulatory Risk : SEBI and other regulatory bodies are making guidelines for social bonds, but these rules are still evolving. Regulatory changes in the future may affect your investment.

Social Bonds are an investment option that goes beyond just profits and connects your money to a purpose. These bonds are for those who want to be a part of social change through their investments. Their scope is gradually increasing in India, and both their demand and transparency are expected to improve in the future. If you do not want to limit your investment to just returns, then Social Bonds can be a powerful and meaningful way.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

When it comes to safe investments, many people turn to government securities. What many investors don’t realize, however, is that there are several types of government securities, each with its own purpose, maturity period, and return profile.

In this blog, we will give you a complete list of the different types of government securities, explain their key features, and explain which ones may be better suited for different applicants.

Classification of Government Securities

Government securities issued in India can be classified on several grounds. These classifications help investors understand which security is best suited to their goals and time horizon.

Issuer: These securities are issued by either the Central Government (e.g. Treasury Bills, Dated G-Secs), or the State Government (e.g. State Development Loans SDLs).

Tenure: Some securities are short term (91 to 364 days), while some are long term (5 years to 40 years).

Coupon Type : These have both fixed coupon and floating rate coupon options.

Asset-Linked : Some government securities like Sovereign Gold Bonds are linked to the price of gold, thus providing investors the benefit of returns along with safety.

An overview of the different types of government securities in India is given below:

1. Treasury Bills (T-Bills)

T-Bills are one of the most common types of securities issued by the government. These are short-term instruments with tenures of 91, 182 and 364 days. T-Bills do not pay any interest, rather they are issued at a discount and the full value is returned on maturity. The government uses them to meet its short-term needs. They are extremely safe for investors and most banks, mutual funds and large corporations invest in them.

Suitable for: For investors who are looking for short-term and low-risk options, T-Bills are a good option.

2. Dated Government Securities (Dated G-Secs)

Dated Government Securities are long-term investment options with tenures ranging from 5 to 40 years. In these, investors get fixed or floating coupons (interest) every 6 months. These are also traded in the secondary market, due to which their liquidity remains good.Among the various types of government securities, dated G-Secs are the most widely held by both retail and institutional investors. These are fully government guaranteed, so there is no risk of default in them.

Suitable for: Investors looking for long-term planning and regular income.

3. State Development Loans (SDLs)

State Development Loans (SDLs) are issued by state governments and are similar to dated G-Secs. The interest on these is slightly higher than dated G-Secs, as the risk in them is slightly higher (although they are still considered safe). RBI auctions them and these are also traded in the secondary market. States use them to fund their development work.

Suitable for: Investors who want slightly better returns in government securities.

4. Sovereign Gold Bonds (SGBs)

SGBs are special types of government securities linked to the price of gold. These are issued by the RBI on behalf of the central government. Their tenure is 8 years, but there is a facility of premature withdrawal after 5 years. This type of government security offers dual returns, gold price appreciation and fixed interest. It gives 2.5% interest annually, and the gain on maturity is tax-free.

Suitable for: Investors who want to invest in gold but do not want the hassle of physical gold.

5. Floating Rate Bonds (FRBs)

The interest rate in FRBs is not fixed, rather it resets every 6 months or on an annual basis. This rate is linked to a benchmark (such as NSC rate or repo rate).

When interest rates are likely to rise, these bonds give better returns. Their value is not as much affected in the market as fixed rate bonds.

Suitable for : Investors who want to save real returns during inflation or are expecting interest rates to rise.

6. Capital Indexed Bonds (CIBs)

CIBs are special types of government securities in which the principal amount invested (and sometimes interest as well) is indexed to the inflation rate. That is, the investor gets a chance to save his real purchasing power. However, these are generally issued very rarely and are mostly for institutional investors.

Suitable for : Investors looking to protect against inflation or large institutions whose strategy is to neutralize the impact of inflation.

Comparison Table: Different Types of Government Securities in India

Type of Security

Maturity

Return Type

Tradable?

Treasury Bills (T-Bills)

≤ 1 year

Return is the difference between issue price and face value.

Yes

Dated G-Secs

5–40 years

Fixed / Floating interest

Yes

State Development Loans (SDLs)

5–10 years

Fixed interest

Yes

Sovereign Gold Bonds (SGBs)

8 years (exit after 5)

Gold price return + 2.5% annual interest

Yes

Floating Rate Bonds (FRBs)

4–7 years

Variable interest (reset periodically)

Yes

Capital Indexed Bonds (CIBs)

Varies

Inflation-linked returns

Limited

How You Can Buy Government Securities

Government Securities can be bought from the following platforms:

Through RBI Retail Direct : If you want to buy bonds or T-bills directly from the government, then RBI’s Retail Direct portal is the easiest way. By registering online, you can invest in government securities from the comfort of your home. No middlemen, no extra fees – everything is digital and transparent.

Mutual fund and ETF options : If you do not want to invest directly in bonds, then you can choose options like gilt funds or Bharat Bond ETF. These are better for those who want to keep the risk low and are investing for the long term.

Conclusion

If you are looking for an investment option that is safe, gives fixed returns and is useful in the long term then investing in government securities can be a wise decision. Now the process of investing is not as difficult as before. You can easily buy directly from RBI’s platform or from your broker’s platform. But, before this, you must understand your financial needs and investment timeframe well. It is advised to consult a financial advisor before investing.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

The semiconductor industry in India is growing rapidly and is set to become the backbone of the technology sector in the coming years. Growing demand, government policy support and large-scale investments have made semiconductor stocks attractive for investors. If you want to participate in the future growth of the semiconductor industry, then it is important to take a look at semiconductor companies listed on the Indian stock market.

In this blog, we will give you an overview of the top 10 semiconductor stocks in India , their KPIs, benefits and risks of investing in them.

What Are Semiconductor Stocks?

Semiconductor stocks are shares of companies engaged in different stages of the semiconductor value chain, including chip design, wafer fabrication, assembly, testing, marking and packaging. In India, this segment is evolving rapidly, with firms not only providing design services but also expanding into ATMP (assembly, testing, marking and packaging) and OSAT (outsourced semiconductor assembly and test). These developments are making semiconductor stocks an increasingly attractive option for investors.

Design / IP: Companies that design chips (such as MosChip)

Packaging and Testing (OSAT/ATMP): Units that are used to make chips ready and reliable

Manufacturing / Fabs and Equipment: Recent investments in the country, such as HCL-Foxconn’s OSAT unit, and Tata’s Assembly & Test factory in Assam, show the strength of this sector

Thus, semiconductor stocks India, whether related to design or packaging/testing, are telling the story of real economic and technological change.

India’s Semiconductor Industry: Growth, Policy & What Lies Ahead

India’s semiconductor industry is at a pivotal inflection point rapidly evolving from a chip-consuming nation into an emerging force in global semiconductor production. The domestic market, valued at USD 52 billion in 2024–25, is projected to reach USD 103.4 billion by 2030, growing at a CAGR of 13%. Mobile handsets, IT, and industrial applications currently account for roughly 70% of revenue, with automotive and industrial electronics offering significant future headroom.

The shift from consumer to creator is being powered by decisive policy action. The government’s India Semiconductor Mission (ISM), launched in 2021 with an investment commitment of around USD 10 billion, was set up to boost chip and display fabrication facilities across the country. The Design Linked Incentive (DLI) Scheme complements this by providing companies a 50% subsidy on design costs along with 4-5% incentives on sales making India an increasingly attractive destination for chip design and manufacturing investment.

On the ground, momentum is building. India’s first operational semiconductor assembly and test facility, set up by CG Power in Sanand, Gujarat, went live in August 2024, with plans to scale from 0.5 million to 14.5 million units per day. The industry is also seeing rapid growth in chip design and back-end processes such as inspection and packaging, with Western companies accelerating the establishment of design hubs by leveraging India’s deep talent pool.

Challenges remain infrastructure stability in power and water supply, raw material sourcing, and the need for a far larger pool of specialised talent are areas that need continued attention. But with 10 government-backed projects now underway across six states and global players deepening their India partnerships, the foundation for a self-reliant semiconductor ecosystem is firmly being laid.

Top 10 Best Semiconductor Stocks in India

Company

Current Market Price (in ₹)

Market Capitalisation (in ₹ crore)

52-Week High (in ₹)

52-Week Low (in ₹)

HCL Technologies Ltd

₹1,405

3,81,270

₹1,780

₹1,276

Bharat Electronics

₹428

3,12,493

₹473

₹252

Vedanta Ltd

₹690

2,69,817

₹770

₹362

ABB India

₹6,179

1,30,932

₹6,555

₹4,590

Dixon Technologies

₹10,004

60,825

₹18,472

₹9,600

Hitachi Energy India Ltd

₹25,090

1,11,832

₹26,325

₹10,400

Tata Elxsi Ltd

₹4,270

26,599

₹6,735

₹3,966

ASM Technologies Ltd

₹2,494

3,638

₹4,596

₹1,109

Moschip Technologies Ltd

₹168

3,254

₹288

₹125

MIC Electronics Ltd

₹34.0

819

₹83.0

₹30.0

(Data as of 06 April 2026)

Overview of the Top 10 Semiconductor Stocks in India

A brief overview of the best semiconductor Stocks in India is given below:

1. HCL Technologies Ltd

HCL Technologies was started in 1976 and today it is counted among the largest IT service companies in India. Over time, the company not only focused on software, but also strengthened its hold in engineering and technology development. In recent years, HCL has also entered the semiconductor sector. In partnership with Foxconn, it is setting up an OSAT unit in Jewar, Uttar Pradesh, which can start work by 2027. It is considered to be the country’s first major chip packaging facility. This initiative will not only connect India to the global semiconductor network, but will also prove to be important in the direction of self-reliance in electronics production.

creating electronic solutions for the defense sector since its inception. In the initial phase, BEL made basic components like semiconductors and integrated circuits, which strengthened India’s electronics industry. Today the company manufactures many important products such as radar systems, communication networks and avionics. Recently BEL has started collaboration with Tata Electronics on semiconductor and electronics manufacturing. Due to long experience and government support, BEL is counted among the organizations that will further strengthen India’s semiconductor value chain in the coming times.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

65.97%

337.04%

867.69%

(Data as of 06 April 2026)

3. Vedanta Ltd

Vedanta Ltd is one of the largest mining and metal companies in India. Formed in 1979, this company mainly deals in resources like aluminum, copper, zinc and oil-gas. Its name is in the news in the semiconductor industry because metals like copper and silver play an important role in chip manufacturing and packaging. Some time ago Vedanta had planned to set up a semiconductor fab in India, although the project faced challenges. Still, this initiative makes the company’s direction clear that it wants to be a part of this sector in the future. Direct chip production may not happen right now, but its importance in the supply chain cannot be ignored.

ABB India is the Indian unit of the global ABB group and has been active here for several decades. It is known in power systems, automation and industrial robotics. Even though it does not manufacture semiconductor chips itself, its contribution to this sector is no less important. Any chip factory or packaging unit requires reliable power solutions and smart automation. ABB’s high-voltage equipment and control technology meet this need. This is why the company is considered an indirect but strong partner of India’s semiconductor ecosystem. It plays a role that strengthens the foundation of factories.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

32.24%

83.28%

347.58%

(Data as of 06 April 2026)

5. Dixon Technologies

Dixon Technologies was formed in the early 1990s and today it is counted among the largest electronics manufacturing companies in India. From TVs, mobile phones, washing machines to LED lights Dixon produces for many big brands. Recently, it became a manufacturing partner for the Google Pixel phone, thereby adding its name to the global electronics supply chain. Dixon does not manufacture semiconductor chips itself, but delivers chip-based products to the mass market through electronic assembly and packaging. This is why Dixon is considered an important link in India’s growth story.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-17.89%

241.99%

185.76%

(Data as of 06 April 2026)

6. Hitachi Energy India Ltd

Hitachi Energy India, part of the global Hitachi Energy group, has been operating in India for several decades. The company specializes in power transmission and grid solutions. Semiconductor manufacturing units require a very stable and reliable power supply, and that is exactly what Hitachi Energy offers. Even though the company does not manufacture chips directly, modern chip factories cannot function without high-voltage systems and power control technology. This is why Hitachi Energy is considered a key partner in India’s semiconductor ecosystem. It works at the backend to build the infrastructure that drives the industry.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

140.10%

670.80%

1,712.86%

(Data as of 06 April 2026)

7. Tata Elxsi Ltd

Tata Elxsi was started in 1989 and is part of the Tata Group. The company is known for design, engineering and research services. Tata Elxsi provides technology support to a wide range of industries from automobiles to electronics and healthcare. In recent years, the company has also been involved in India’s chip design programs, especially by working on chips with 28nm to 90nm technology. This initiative has helped India gain a place in global chip design. Tata Elxsi is being considered an important player in the semiconductor ecosystem due to its engineering expertise and innovation capability.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-11.09%

-30.14%

47.32%

(Data as of 06 April 2026)

8. ASM Technologies Ltd

ASM Technologies has made a name for itself in the world of technical engineering. It recently signed an investment agreement of ₹510 crore with the Government of Karnataka, enhancing its capabilities in precision engineering and design-focused manufacturing for the electronics, semiconductor and solar industries. The company is now operating from two new manufacturing facilities Dabaspet (Karnataka) and Sriperumbudur (Tamil Nadu) which will provide mastery in design-led manufacturing. This initiative clearly signifies that ASM is taking confident steps towards technical depth and becoming India as a semiconductor engineering hub.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

120.56%

511.00%

2,253.85%

(Data as of 06 April 2026)

9. MosChip Technologies Ltd

MosChip Technologies is a Hyderabad-based company that specializes in semiconductor design and system engineering. The firm offers solutions at every stage from system-on-chip (SoC), ASIC and product engineering such as voice-to-graphics. Recently, the government’s semiconductor initiatives have boosted investor confidence, with MosChip’s stock jumping 19% to Rs 229 in a single day. The gist is clear: the company is not just a technical force, but is also gaining prominence in the eyes of the market.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

29.17%

-17.54%

-17.56%

(Data as of 06 April 2026)

10. MIC Electronics Ltd

MIC Electronics is an old but still strong name, manufacturing LED video displays, telecom equipment and digital signage solutions. It recently signed an MoU with Singapore-based Neo Semi SG with plans to expand into semiconductor IP, AI-driven energy logistics and circular electronics. This move, coupled with its long-standing technology experience, puts MIC at the centre of new opportunities in the Indian semiconductor theme.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-31.33%

168.70%

4,151.25%

(Data as of 06 April 2026)

Key Performance Indicators (KPIs)

The key performance metrics of semiconductor Stocks in India are mentioned below:

You should consider investing in semiconductor stocks due to the reasons given below:

Growing demand and future prospects : The demand for electric vehicles, 5G networks, artificial intelligence and smart gadgets is growing rapidly in India. The need for chips is the highest in all these sectors. This is the reason why the growth of semiconductor stocks in India will get strong support in the coming years.

Support from government policies : The government has announced PLI and DLI incentives of ₹76,000 crore so far under the “India Semiconductor Mission”, of which about ₹65,000 crore has been committed. In addition, semiconductor fab, OSAT, and 3D packaging projects have been approved in January–August 2025, with a total investment of about ₹1.6 trillion (US$18.2 billion).

Possibility of attractive returns : Since India’s semiconductor industry is still in its early stages, investors who invest for the long term by choosing the right companies can get better returns. Early investors can take full advantage of this growth.

Global supply chain opportunity : The world is looking for alternative suppliers to reduce excessive dependence on China and Taiwan. India is in a position to fill this void. This can help Indian semiconductor companies benefit from global orders and partnerships.

Backbone of the technology sector : The expansion of new technologies like AI, EV, 5G and IoT is directly linked to the semiconductor industry. That is, with the growth of these trends, the value of Indian semiconductor stocks will become even stronger.

Factors to Consider Before Investing in Semiconductor Stocks

Some of the factors that you should consider before investing in semiconductor stocks is given below:

Company position and role in the value chain : It is important to understand where the company operates in the semiconductor value chain whether it is active in design (IP), packaging and testing (OSAT/ATMP), or materials and equipment. This gives an idea of its business model and growth potential.

Customer base and certifications : Before investing in any semiconductor stocks India, it is important to see who its customers are. If the company has certifications related to the auto or industrial sector (such as AEC-Q100, ISO) and long-term contracts, it means that its business is stable and reliable.

Financial strength : Pay attention to the company’s balance sheet and financial performance. Good return on capital employed (ROCE), healthy margins and low debt levels indicate that the company can earn profits over a long period of time.

Policy support and capex visibility : The government in India is taking steps like Production-Linked Incentive (PLI) and “India Semiconductor Mission” to promote the semiconductor industry. It is important to see whether the company is taking advantage of these schemes or not, and how clearly and planned its capex is being done.

Valuation and investment level : While investing in any of the best semiconductor stocks, one should see whether the current pricing is fair or too expensive. Early-stage companies are valued on the basis of EV/Sales, while EV/EBITDA and P/E ratios are more appropriate for mature companies.

Risks of investing in semiconductor stocks are given below:

Policy delays and dependence on subsidies : The Indian government has launched large-scale PLI and incentive schemes for the semiconductor industry. But sometimes there are delays in the implementation of these schemes or obstacles in releasing funds. If a company’s business model is based only on government support, it can increase the risk for investors.

Cyclical nature of global demand : The semiconductor industry is completely dependent on the demand and supply cycle. When the demand for electronic devices decreases globally, it directly affects chip manufacturing and related companies. Therefore, semiconductor stocks in India are also not able to escape this fluctuation.

Capex-heavy business and execution risk : Semiconductor manufacturing requires billions of rupees of investment and a long time. Many times companies announce projects but are unable to complete them on time. In such cases, investors’ money can be stuck for a long time.

Governance and management challenges : Small and medium-sized companies often face problems such as lack of transparency, neglect of shareholder interests or misplaced management priorities. Such governance issues can pose risks for investors.

Liquidity and market risk : Many semiconductor companies in India are still relatively small and their shares have low trading volumes. This means that investors cannot easily convert their investments into cash, especially when the market is in a downtrend.

India’s semiconductor sector is still in its early stages, but its pace seems to be increasing. With strong government support, rising domestic demand, and adoption of new technologies, the industry is poised to become significant. The best way for investors is not to rely only on announcements, but to see what companies are doing on the ground. Semiconductor stocks in India selected with a little patience and proper research can help strengthen your portfolio in the coming times. It is advised to consult a financial advisor before investing in semiconductor stocks.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

Which are the top semiconductor stocks in India right now?

HCL Technologies, BEL, Tata Elxsi, Dixon are some of the top companies involved in the semiconductor industry.

Are semiconductor stocks good for long-term investment?

Semiconductor stocks offer long-term potential from rising chip demand, but always analyze the company and consult a financial advisor before investing.

What are the main risks of investing in semiconductor stocks?

Key risks include policy delays, high capital expenditure requirements, and volatility in global and domestic chip demand.

How can a beginner start investing in semiconductor stocks in India?

Beginners should start with small investments, research companies carefully, and diversify to manage risk effectively.

Are Indian semiconductor companies globally competitive?

Yes, Indian semiconductor companies are competitive in design and packaging, though they remain in the early stages of fabrication.

Selection Methodology and Important Disclaimer

The stocks included in this list are selected primarily on the basis of their market capitalisation, which represents the total market value of a company’s outstanding shares. The companies are arranged in descending order of market capitalisation, with larger companies appearing first, followed by relatively smaller companies. This methodology is intended to provide a structured approach for identifying companies based on their market size and overall presence within a sector.

However, market capitalisation should not be considered the sole factor while evaluating investment opportunities, as it does not guarantee future performance, profitability, or returns. Investors should also assess other important factors such as financial health, business fundamentals, management quality, valuation metrics, industry outlook, and market conditions before making investment decisions.

The information provided is for educational and informational purposes only and should not be construed as investment advice, recommendation, solicitation, or an offer to buy or sell any securities by Pocketful Fintech Capital Private Limited.

Today, when companies want to expand internationally, they need financial tools that can attract global investors. Foreign Currency Convertible Bonds is one such option, the demand for which has increased rapidly in the last few years. This bond allows companies to raise funds in foreign currency and later these can be converted into shares of the company.

In this blog, we will know how these FCCBs work, what their special features are and why they are becoming an important part of the funding strategy of many Indian companies.

What Are Foreign Currency Convertible Bonds (FCCBs)?

Foreign Currency Convertible Bonds (FCCBs) are debt securities issued in foreign currency that can be converted into the issuer’s equity shares at predetermined terms. Initially, it is a debt instrument on which the investor gets a fixed interest. But if the company performs well and the share price rises, the investor can convert this bond into a share, which also gives him the benefit of equity.

1. In which currency are FCCBs issued?

Foreign Currency Convertible Bonds (FCCBs) are issued in currencies that are commonly used for international transactions, aimed at foreign investors. The most common currency is the US Dollar (USD), but sometimes these bonds are also issued in other stable currencies like Euro (EUR) or Japanese Yen (JPY). The reason for this is simple—if a company has to raise funds from the foreign market, it has to issue bonds in the currency that is convenient for the investors there.

2. Why are they attractive for investors?

FCCBs offer investors a combination of debt and equity. On one hand, there is the security of fixed interest, while on the other hand, additional returns can be earned by converting into shares on the possibility of growth of the company. This is why they are becoming a preferred option for investing in companies with high growth potential.

3. Use and trend of FCCBs in India

Indian companies, especially in the IT, pharma and manufacturing sectors, have been using FCCBs for global expansion and raising capital. RBI and SEBI have made clear guidelines for this, due to which FCCBs have once again emerged as a reliable and regulated financing tool.

Issued in foreign currency : FCCBs are issued in foreign currency, such as the US dollar (USD), euro (EUR) or Japanese yen (JPY). This allows companies to raise capital directly from international investors, giving them an opportunity to grow beyond the boundaries of the domestic market.

Conversion to equity : The most important feature of these bonds is that they can be converted into shares of the company after a certain period of time. This conversion takes place at a pre-fixed price, giving the investor upside potential in equity.

Fixed maturity period : FCCBs have a fixed maturity period usually between 3 to 5 years. At the end of this period, the investor can convert the bond or withdraw the entire amount of principal and interest from the company.

Funding at low interest rate : The coupon rate on these bonds is lower than that of normal debt instruments. Since the investor also gets the option of conversion, he is willing to invest even at lower returns.

Delayed share dilution : Another advantage of FCCBs for companies is that there is no immediate share dilution. The conversion happens in the future, thereby protecting the company’s existing shareholding.

International listing : FCCBs are usually listed on international stock exchanges—such as Luxembourg, Singapore or London. This maintains their value in the global market and provides investors with trading facilities.

Impact of currency risk : Since FCCBs are denominated in foreign currency, companies are exposed to currency risk. If the Indian rupee depreciates against the dollar, repayment of the bond may be costly for the company.

Regulatory compliance : For Indian companies, strict guidelines of RBI and SEBI apply to the issuance of FCCBs. The conversion price, maturity period, and listing are all subject to regulations.

Double benefit to investors : Investors get fixed interest on one hand, and on the other hand, there is a possibility of additional profit from share conversion as per the growth of the company. This is why FCCBs are considered a balanced investment tool.

Suitable for institutional investors : FCCBs are usually purchased by large institutional investors, such as hedge funds, mutual funds and foreign portfolio investors. These investors choose this instrument considering the long-term growth and conversion potential.

Easy access to global capital : When it is difficult or expensive to raise capital in the domestic market, companies raise funds from foreign investors through FCCBs. This gives them an opportunity to access capital internationally.

Funding at lower interest rates : The interest rate on FCCBs is usually lower than domestic loans, as investors get the option of conversion into shares later. This reduces the financing cost of companies.

Avoidance of immediate share dilution : Companies get capital without selling their shares initially. Conversion usually happens after a few years, which prevents immediate dilution.

Global presence of the brand : FCCBs are often listed on international stock exchanges (such as Luxembourg or Singapore), increasing the company’s credibility and global recognition.

Favourable regulatory or tax benefits : In some countries, tax or regulatory rules are more favourable, which makes companies interested in raising capital through such means.

Benefits of Foreign Currency Convertible Bonds

Benefits for companies

Low-cost funding : FCCB is a type of debt, but the interest rate is lower than traditional debt. Because the investor gets the option of conversion into shares in the future, financing is cheaper for companies.

No immediate share dilution : Through FCCB, a company can raise capital without issuing equity immediately. This does not reduce the share of existing shareholders immediately; the dilution is gradual.

Access to global investor base : FCCB is denominated in foreign currency and is often bought by international investors. This allows the company to get investments from around the world and also increases its brand value.

Suitable for those with foreign income : If the company’s income is in foreign currency like dollars or euros (like IT or export companies), then FCCB helps in balancing their currency risk.

Benefits for investors

Safe income with low risk : Even if the company does not perform well, a fixed interest is received on FCCB. This gives a basic safety to the investors.

Opportunity to increase returns : If the share price of the company increases, then investors can earn profit by converting FCCB into shares. That is, low risk, high opportunity.

International diversification : This is a great way for foreign investors to invest in companies of emerging countries in a safe and smart way.

Key Risks and Drawbacks of Foreign Currency Convertible Bonds

Currency fluctuation risk : FCCBs are issued in foreign currency (such as the US dollar or the euro). If the rupee weakens, the company has to pay more at the time of repayment, which increases its overall cost.

Possibility of share dilution : These bonds can be converted into shares later. If this happens, the total number of shares of the company increases, which may reduce the stake of old investors and profit per share.

Share price risk : If the company’s stock trades below the conversion price, investors will not convert the bonds into shares. In this case, the company has to pay in cash, which can affect its liquidity arrangements.

Complexity of regulatory process : There are many permissions and regulations to be followed before issuing an FCCB, which can be time consuming and complex for the company.

Refund pressure if conversion is not done : If investors do not exercise the conversion option, the company has to return the entire amount in foreign currency on maturity which can impact its financial position.

Interest rates and return calculations : Although interest on FCCBs is usually low, if conversion does not happen, the company has to pay back the entire amount just like a loan.

Market uncertainty : If market conditions change suddenly such as regulatory policy or a global crisis a financial plan based on FCCBs can become unstable.

Impact on the company’s credit rating : If the company is unable to meet the terms of FCCBs on time, it can have a negative impact on its credit rating.

FCCBs vs Other Instruments

Feature

Foreign Currency Convertible Bonds (FCCBs)

Foreign Bonds

Global Depository Receipts (GDRs)

Non-Convertible Debentures (NCDs)

Currency of Issue

Issued in foreign currency (e.g., USD, EUR)

Issued in foreign currency

Issued in foreign currency like equity instruments

Issued in Indian Rupees

Equity Conversion

Convertible into company equity at a future date

Cannot be converted into equity

Represent equity but not directly convertible

Purely debt, no equity conversion

Interest Payment

Offers low interest rate for the issuer

Generally moderate interest rate

Usually no interest paid (equity-like instrument)

Offers fixed, higher interest to investors

Impact on Ownership

Dilution of ownership may occur upon conversion

No dilution in ownership

May indirectly reflect ownership but no direct dilution

No impact on company ownership

Investor Type

Foreign investors seeking low risk with equity potential

Risk-averse foreign debt investors

Foreign investors interested in international equity exposure

Domestic investors looking for fixed income

Regulatory Requirements

High regulatory scrutiny and compliance

Moderate regulatory framework

Moderate regulatory requirements

Least complex in terms of compliance

Risk Factors

Exposed to both currency and market risk

High currency risk involved

Includes both currency and market risks

Mainly interest rate and credit risk

Use of Funds

Ideal for raising global funds with future equity possibility

Used for long-term international debt funding

Used for equity fundraising and international listing

Suitable for short- to mid-term capital requirements

Indian Context: FCCBs in India Past, Present, Future

FCCBs became a major vehicle for Indian companies to raise foreign funds during the period 2004 to 2008. During this period, companies such as IT, infrastructure and real estate issued FCCBs on a large scale due to the availability of international capital and the strengthening of the rupee.

Post 2008 Crisis and Buyback Pressure : After the global recession of 2008, Indian companies faced a lot of difficulties in repaying FCCBs. Due to the sharp fall in share prices, conversion was not possible, forcing many companies to buy back these bonds at a higher price.

Current Regulations RBI and SEBI Strictness : Today, RBI and SEBI have set stringent norms for FCCBs such as a minimum maturity period, conditions related to conversion price, and mandatory reporting with full transparency. These regulations have reduced the possibility of misuse of FCCBs.

2023–25 trend Return in select sectors : In recent years, FCCBs have been used in a limited but strategic way in sectors such as technology, pharma and green energy. Companies are now issuing these bonds with better planning.

Way forward (2025–30): If the rupee remains stable and global capital flows strengthen, FCCBs could once again become a profitable instrument for Indian companies. The recent regulatory framework and financial discipline will allow them to be used with greater caution and transparency.

Foreign Currency Convertible Bonds (FCCBs) play a vital role in today’s global financing strategy. These bonds provide companies with an option to raise foreign investment that combines the benefits of both debt and equity. If used timely and wisely, they can not only reduce the cost of funding but also open the way for expansion into foreign markets. For Indian companies, this is a tool that can strengthen their presence in the international financial landscape.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

This Kalyan Jewellers case study is an inspiring success story of the Indian jewellery industry where a regional brand started in Kerala in 1993 and today has expanded its network to international level. In this blog, we will explore the business model, marketing strategy, latest financials and detailed SWOT analysis of Kalyan Jewellers. This journey shows how a brand can make a strong reputation in the market with the help of innovation and right strategy.

Kalyan Jewellers Company Overview

Kalyan Jewellers was started in the year 1993, headquartered in Thrissur, Kerala. Initially it was a local jewellery store, which focused on selling gold jewellery in South India. At that time its business was based on trust and quality, which created a strong relationship with the customers.

Gradually the company expanded its operations and stepped out of Kerala in states like Tamil Nadu, Karnataka and Andhra Pradesh. After this, Kalyan Jewellers made its presence felt all over India and today it is one of the leading jewellery brands in the country. The brand identity is not limited to the purity of gold, but is also based on transparency and emotional connection with customers. Kalyan Jewellers is trusted for weddings, festivals, and special occasions, making it the preferred choice of millions of families.

Kalyan Jewellers is one of India’s largest jewellery retail chains, whose business model is based on customer trust, product quality and wide distribution network. The company has designed its operations in a way to serve every segment of the customer. Its business model is mainly based on the following points .

Multi-format retail stores : Kalyan operates multi-format retail stores, with premium outlets in major cities and mid-segment stores in smaller towns, ensuring it serves customers across all budget ranges.

Diverse product range : Offers collections in gold, diamond, platinum, polki, and silver jewellery, catering to both traditional and modern customers.

Region-specific product design : Collections are designed keeping in mind the local culture and design preferences in each region, which strengthens the connection with the customer.

Purity and transparency : Customer trust is enhanced by providing BIS hallmarking, transparent billing and clear weight-rate information.

Brand Ambassadors : Brand association with regional and national celebrities to strengthen brand recognition across states.

Value-Added Services : Gold exchange, resale of old jewellery, installment schemes and festive offers to enhance customer retention.

Omni-Channel Presence : Online platform with physical stores allowing customers to browse and purchase the collection from the comfort of their homes.

Gold Saving Schemes : To build a long-term relationship, customers are offered Gold Saving Plans to ensure repeat purchases.

Kalyan Jewellers has adopted a multi-pronged and thoughtful marketing strategy to strengthen its presence in the Indian jewellery market, bringing the brand credibility and closeness to consumers on a national level.

Celebrity Endorsements : The company has collaborated with national icons such as Amitabh Bachchan and Katrina Kaif as brand ambassadors, thereby creating an image of trust and prestige. Also, regional film stars have been associated with the brand from different states to strengthen the connection with local culture.

Muhurat Campaigns : The “Muhurat” series runs special campaigns during the wedding and festive seasons, connecting consumers to important moments in life through emotional stories.

Emotional Storytelling : The ads emphasise the importance of relationships and traditions, not just the product, thereby connecting the brand on an emotional level.

Digital Transformation : Kalyan Jewellers has adopted digital initiatives such as social media, influencer marketing and virtual catalogues to reach out to new and tech-savvy consumers.

Regional Targeting : Targeted ads are created for different states keeping in mind the local language, culture and design.

Brand Positioning : The company positions itself as a symbol of “Trust and Transparency” where the pricing policy is transparent and competitive.

Premium but Approachable : Design and quality are at a premium level but the prices are such that even the mid-tier customers can afford it.

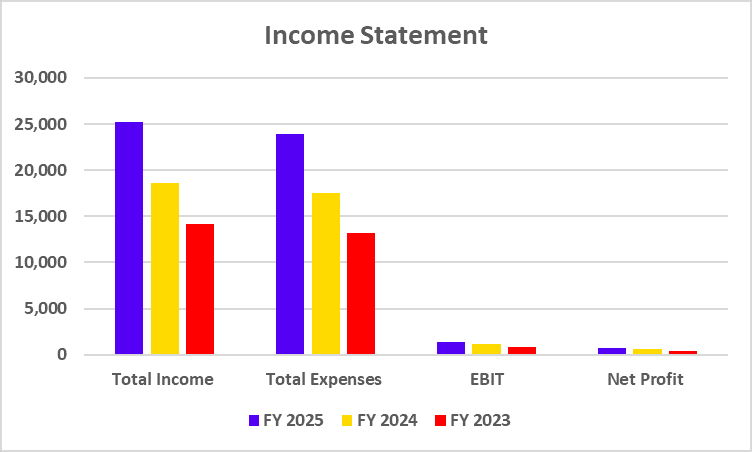

Financial Data of Kalyan Jewellers

Income Statement

Particulars

FY 2025

FY 2024

FY 2023

Total Income

25,189

18,621

14,109

Total Expenses

23,870

17,509

13,235

EBIT

1,319

1,112

874

Net Profit

714

596

431

(The figures mentioned above are in INR crores unless mentioned otherwise)

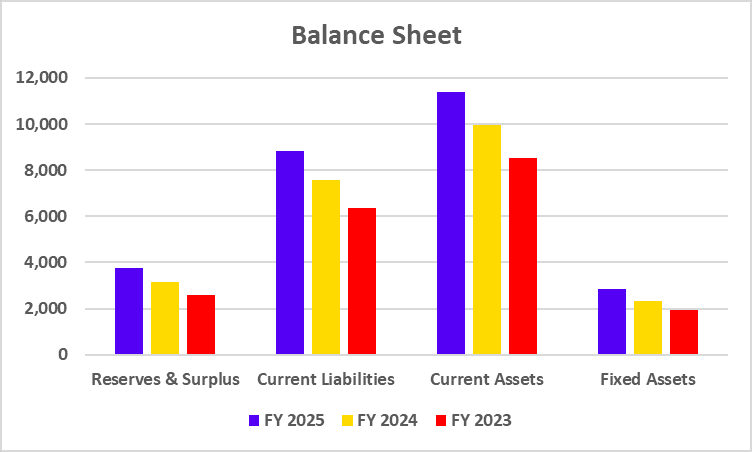

Balance Sheet

Particulars

FY 2025

FY 2024

FY 2023

Reserves & Surplus

3,772

3,159

2,604

Current Liabilities

8,810

7,582

6,368

Current Assets

11,399

9,949

8,515

Fixed Assets

2,848

2,342

1,918

(The figures mentioned above are in INR crores unless mentioned otherwise)

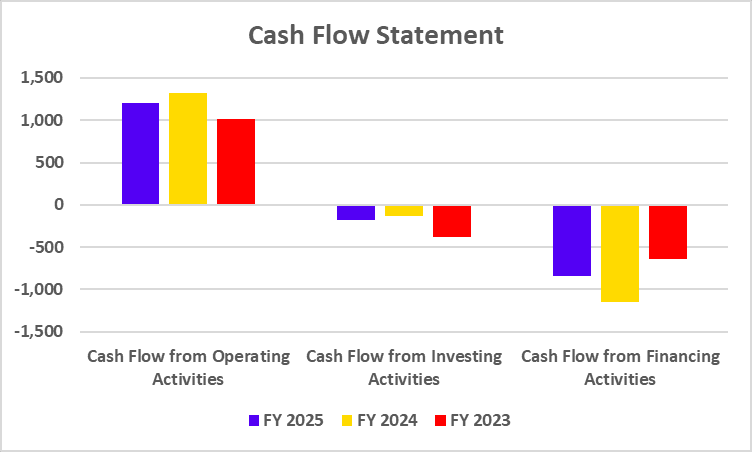

Cash Flow Statement

Particulars

FY 2025

FY 2024

FY 2023

Cash Flow from Operating Activities

1,209

1,321

1,013

Cash Flow from Investing Activities

-176

-136

-383

Cash Flow from Financing Activities

-840

-1,148

-637

(The figures mentioned above are in INR crores unless mentioned otherwise)

Strong brand identity : Kalyan Jewellers is a trusted name in India and abroad. It has a strong presence especially in South India as it has maintained a special place in the hearts of people for decades.

Wide store network : They have stores in almost every big and small city of India, as well as in countries like the Middle East. This makes it easy to reach every type of customer.

Diverse design collection : From traditional to modern and bridal jewellery for weddings, every type of jewellery is available here which attracts people of different age groups and tastes.

Celebrity endorsement: By associating with big names like Amitabh Bachchan, Aishwarya Rai, Nagarjuna, the brand has increased both its credibility and popularity.

Weaknesses

High cost : It costs a lot to run such large stores and get celebrity endorsements, which can affect the company’s profits.

Premium price tag : Many times middle-income customers find Kalyan’s prices a bit high, due to which they hesitate to buy.

Weak online presence : More effort is needed on digital marketing and e-commerce platforms, especially keeping the youth in mind.

Opportunities

Expansion of online market : Due to increasing online shopping, there is an opportunity for the company to increase customers on a large scale.

Keeping the young generation in mind : Bringing new and cool designs for millennials and generation Z can increase the company’s sales.

Expansion in foreign markets : Strengthening its hold especially among the NRIs is a golden opportunity.

Threats

Tough competition : Competition from big names like Tanishq, Malabar Gold and local jewelers is always challenging.

Fluctuation in gold prices : When the price of gold increases or decreases too much, the customer’s purchase is affected.

Competition from counterfeit and unbranded jewellery : The presence of fake and copy products in the market can harm the credibility of the brand.

The story of Kalyan Jewellers shows how a brand can make a place in the hearts of people with constant hard work and smart business decisions. Their strength lies in understanding the changing trends and customer expectations with time. Like every business, they too had to face many difficulties, but they did not give up. This journey shows how with patience and right decisions a company can make its name in the industry.

S.NO.

Check Out These Interesting Posts You Might Enjoy!

India is a developing economy and is also known as a consumption-oriented country. To fulfil the rising energy demand, OMCs play a vital role. They ensure the availability of fuel for both urban and rural sectors. Investment in OMCs provides you with an opportunity to participate in the country’s growth.

In this blog, we will give you an overview of the best OMC companies in India, along with the benefits of investing in this sector.

What are Oil Marketing Companies?

Oil Marketing Companies (OMCs) are companies that are primarily engaged in the refining, distribution, and marketing of petroleum products such as petrol, diesel, kerosene, LPG (cooking gas), aviation turbine fuel (ATF), lubricants, and other petroleum derivatives.

Their key activities include:

Refining crude oil into usable fuels and products.

Storing and transporting petroleum products across the country through pipelines, depots, and terminals.

Retail distribution via petrol pumps, LPG cylinders, aviation fuel stations, and bulk sales to industries.

Marketing and branding petroleum products to end consumers.

In India, OMCs are a critical link between crude oil imports/refining and the final consumer. They ensure the availability of fuel for households, vehicles, industries, and airlines.

Best Oil Marketing Companies in India – An Overview

An overview of the best oil marketing companies in India is given below:

1. Bharat Petroleum Corporation Limited

BPCL was founded in 1952 as a joint venture between the Indian government and Burmah Shell. In 1976, the Indian government acquired Burmah Shell, converting BPCL into a fully owned government company. The company explores, refines, distributes, markets, and retails petroleum and petroleum-related products. The Ministry of Petroleum and Natural Gas of the Indian government is overseeing it. The headquarters of the company are situated in Mumbai.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-11.34%

97.98%

53.25%

(As of 3 September 2025)

2. Hindustan Petroleum Corporation Limited

HPCL was established in 1974 as a result of the merger of Esso Standard and Lube India Limited. The company became the first public sector enterprise to list on the Bombay Stock Exchange in 1992. The company achieved its profit of 10644 crore, and earned the title of Maharatna status. It operates through a network of more than 17,000 petrol pumps in India, out of which 40% are in urban areas and the remaining are located on highways and in rural areas. The company has its headquarters situated in Mumbai.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-9.62%

143.93%

187.26%

(As of 3 September 2025)

3. Indian Oil Corporation Limited

The Indian Oil Company was incorporated in 1959 in order to market petroleum products. Later in 1964, it merged with Indian Regiments Limited and formed Indian Oil Corporation Limited. During the 1970s and 80s, it was considered the largest refinery and marketing company in India. Later, the company diversified its business into petrochemicals, pipelines and started its overseas operations. It works under the Ministry of Petroleum and Natural Gas, and it was awarded the status of Maharatna Company. The company has its headquarters situated in New Delhi.

Know the Returns:

1Y Return (%)

3Y Return (%)

5Y Return (%)

-21.16%

96.92%

146.44%

(As of 3 September 2025)

4. Reliance Industries Limited

Mr. Dhirubhai Ambani founded the company in 1966, and it became a publicly listed company in 1977. It began its expansion into the petrochemical industry later in 1980. After the death of founder Dhirubhai Ambani in 2002, Reliance was divided between his two sons. Mukesh Ambani continues to lead Reliance Industries Limited, which remains focused on petrochemicals, refining, retail, and telecom. However, the company’s core business is petrochemicals. The company is also making significant investments in the renewable energy sector. The company has its headquarters situated in Mumbai.

The significant benefits of investing in oil marketing companies are as follows:

Consistent Demand: OMCs deal with important fuels such as petrol, diesel, etc., which are always in demand, no matter what the condition of the economy. Regular earning is made possible due to constant demand.

Government Incentives: OMC companies receive financial and policy support from the government, due to which their operational risk is reduced.

Dividend: Public sector oil marketing companies generally distribute their profit in the form of dividends, which can be a regular source of income for a conservative investor.

Factors to be considered before investing in Oil Marketing Companies

The following are the factors which need to be considered before investing in oil marketing companies:

Volatility in Crude Oil Price: The raw material for OMCs is crude oil prices of which fluctuate due to various factors, including global economic factors, etc. A sudden rise in crude oil prices may impact the profit margin of these companies.

Exchange Rate: Crude Oil is imported from different countries, the prices of which are to be paid in USD. A weak rupee can increase the input cost and reduce the profit margin of the company.

Geopolitical Risk: The conflict among the countries of the Middle East and the decision by OPEC can affect the demand and supply of crude oil globally.

Future of Oil Marketing Companies in India

The government of India is importing more oil and gas to meet the country’s expanding energy needs. Due to the industry’s dependence on imports, a number of companies were looking into possibilities for investment. Since the demand for petroleum products has increased by 6.1% year over year, the demand for natural gas has increased by 6.4%. The government aims to raise the refining capacity to 450 million metric tonnes annually (MMTPA) by 2030. Therefore, India’s oil and gas industry has a bright future.